Identifiability of Contagion Components amid Environmental Fluctuations in Aggregated Default Counts

Pith reviewed 2026-05-12 01:46 UTC · model grok-4.3

The pith

Most annual default clustering arises from cross-year shifts in conditions rather than within-year contagion after aggregation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

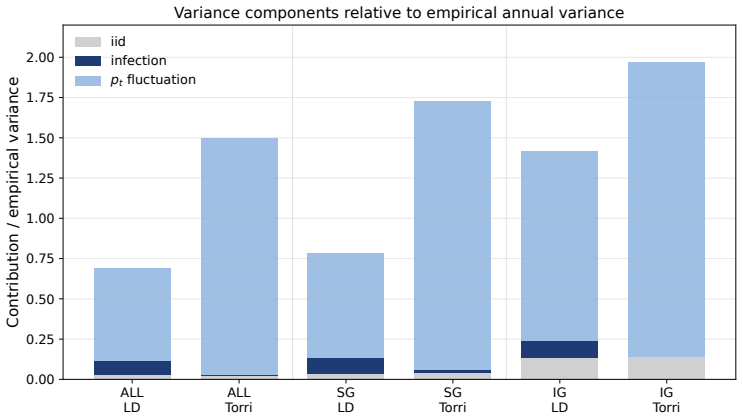

Under the hierarchical specification, cross-year movements in default conditions account for most variation in annual default counts, leaving threshold-type contagion with no separable stable component while cumulative contagion retains a small but detectable persistent element in variance decomposition and tail behavior.

What carries the argument

Variance decomposition and tail comparison across the Lo-Davis cumulative contagion model, Torri threshold contagion model, and Vasicek common-factor model, first under i.i.d. assumptions and then under a hierarchical model that lets default probability vary by year.

If this is right

- Threshold contagion is absorbed into macro variation and cannot be recovered from aggregate counts.

- Cumulative contagion leaves a small stable component that survives aggregation.

- The Vasicek common-factor structure fits observed clustering better than either contagion model under i.i.d. conditions.

- Identifiability of contagion from coarse data depends on the precise form of the interaction mechanism.

Where Pith is reading between the lines

- Finer-grained data on individual defaults or timing within years would be needed to separate contagion from macro effects more reliably.

- Risk models that rely solely on aggregate counts may attribute cumulative-contagion effects to macro shocks instead.

- The same identifiability limits may apply to other aggregated contagion settings such as interbank lending or supply-chain defaults.

Load-bearing premise

The three chosen dependence structures are the only relevant ones, and letting default probability change freely each year fully captures macroeconomic heterogeneity without leftover confounding.

What would settle it

After fitting the hierarchical macro component to real annual default counts, check whether the remaining variance and extreme tail quantiles match the small persistent residual predicted by the Lo-Davis model or the zero residual predicted by the Torri model.

Figures

read the original abstract

Can contagion components be identified in aggregated default counts when default probabilities fluctuate with the economic environment? We study this question as an identifiability problem for coarse-grained default-count distributions. Three dependence mechanisms are compared: cumulative contagion in the Davis--Lo model, threshold-type contagion in the Torri model, and common-factor dependence in the Vasicek model. Under an i.i.d. specification, the Vasicek model gives the best overall fit, indicating that a smooth mixture induced by environmental fluctuations can reproduce much of the observed annual default clustering. We then introduce a hierarchical specification in which the baseline default probability varies across years. This extension separates cross-year environmental fluctuations from within-year contagion. Most of the variance of annual default counts is explained by fluctuations in default conditions. The remaining component, however, depends on the contagion mechanism. Threshold-type contagion is largely absorbed into environmental heterogeneity, whereas cumulative contagion leaves a small but persistent signature in both variance decomposition and tail behavior. These results clarify when contagion remains identifiable after aggregation and when it becomes indistinguishable from environmental fluctuations.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper investigates whether contagion effects can be identified separately from macroeconomic fluctuations in aggregated annual default count data. It compares three dependence structures—cumulative contagion (Lo-Davis model), threshold-type contagion (Torri model), and common-factor dependence (Vasicek model)—first under an i.i.d. specification and then under a hierarchical extension that allows default probabilities to vary freely across years. The central finding is that cross-year macro variation absorbs most clustering, with residual contagion effects being model-dependent: absent after aggregation in the Torri model but leaving a small persistent component visible in variance decompositions and tail behavior for the Lo-Davis model.

Significance. If the results hold, the work clarifies the limits of inferring contagion from coarse-grained data, which is directly relevant to credit risk modeling and regulatory capital calculations. The hierarchical approach combined with explicit variance decompositions and tail comparisons provides a quantitative framework for separating mechanisms, and the model-specific findings (no separable component in Torri versus small persistent in Lo-Davis) offer falsifiable distinctions that can guide empirical practice.

major comments (1)

- [Hierarchical specification and variance decomposition] Hierarchical extension (around the variance decomposition): the claim that year-specific default probabilities fully absorb macroeconomic heterogeneity and leave only model-dependent residuals is load-bearing for the conclusion that Torri contagion is absorbed while Lo-Davis retains a persistent component. Without robustness checks that include observable macro covariates (e.g., GDP or interest rates) alongside the year-specific probabilities, residual confounding cannot be ruled out, potentially altering the interpretation of the Lo-Davis tail and variance results.

minor comments (3)

- [Abstract and §1] The abstract and introduction would benefit from an explicit statement of the sample period, data source for default counts, and number of years/observations used in the fits.

- [Model definitions and estimation] Notation for the contagion intensity parameters and the hierarchical prior on default probabilities should be unified across the model definitions and estimation sections to avoid reader confusion.

- [i.i.d. model comparison] The tail behavior comparisons would be strengthened by reporting exact p-values or test statistics rather than qualitative statements about 'especially in the tail.'

Simulated Author's Rebuttal

We thank the referee for the constructive and insightful report. We address the single major comment below and have incorporated a partial revision to clarify the rationale and limitations of our hierarchical approach.

read point-by-point responses

-

Referee: Hierarchical extension (around the variance decomposition): the claim that year-specific default probabilities fully absorb macroeconomic heterogeneity and leave only model-dependent residuals is load-bearing for the conclusion that Torri contagion is absorbed while Lo-Davis retains a persistent component. Without robustness checks that include observable macro covariates (e.g., GDP or interest rates) alongside the year-specific probabilities, residual confounding cannot be ruled out, potentially altering the interpretation of the Lo-Davis tail and variance results.

Authors: We thank the referee for this important observation. The hierarchical specification is deliberately constructed to let default probabilities vary freely across years, thereby capturing all macroeconomic heterogeneity in a nonparametric manner rather than through specific observables. This design isolates the identifiability question: whether within-year contagion mechanisms generate distinguishable components once cross-year macro variation is fully absorbed. We agree that adding observable covariates such as GDP or interest rates would constitute a valuable robustness exercise. However, our focus is on the limits of inference from aggregated data without requiring detailed macro series, which is the typical setting for such models. We have added a new paragraph in Section 4.3 of the revised manuscript that explicitly discusses this point, notes the potential for residual confounding, and clarifies that the model-specific findings (absorption in Torri versus small persistent component in Lo-Davis) are conditional on the flexible year effects. This preserves the core identifiability conclusions while acknowledging the referee's concern. revision: partial

Circularity Check

No significant circularity detected

full rationale

The paper compares three posited dependence structures (Lo-Davis cumulative contagion, Torri threshold contagion, Vasicek common factor) via i.i.d. and hierarchical fits to aggregated default counts, then reports variance decompositions and tail behavior under the hierarchical extension. These steps are standard model-based inference: parameters are estimated from data, and conclusions about what remains after cross-year default-probability variation are direct outputs of the fitted models rather than inputs renamed as predictions. No self-citation is invoked as load-bearing justification, no quantity is defined in terms of itself, and no uniqueness theorem or ansatz is smuggled from prior author work. The derivation chain remains self-contained against the external data and the three explicit model specifications.

Axiom & Free-Parameter Ledger

free parameters (2)

- year-specific default probabilities

- contagion intensity parameters

axioms (2)

- domain assumption The Lo-Davis, Torri, and Vasicek models correctly represent the possible forms of default dependence

- ad hoc to paper Aggregated annual counts contain enough information to distinguish the mechanisms after hierarchical adjustment

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.