The P behind Q: Empirical Evidence from Physical Drift in Put-Call Parity

Pith reviewed 2026-05-20 21:51 UTC · model grok-4.3

The pith

Physical drift from the underlying enters the capital-using process that enforces risk-neutral put-call parity.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

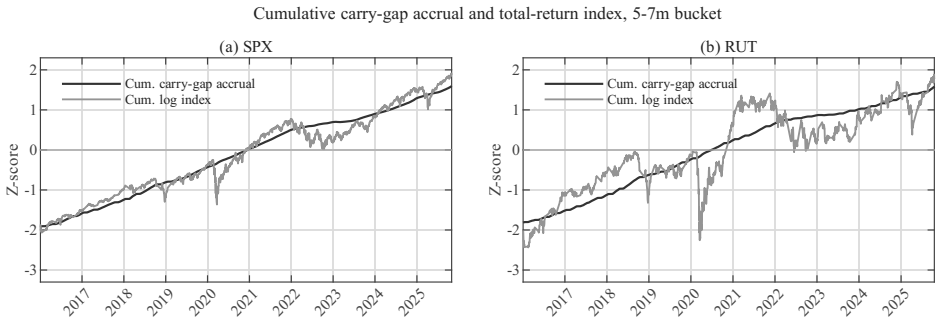

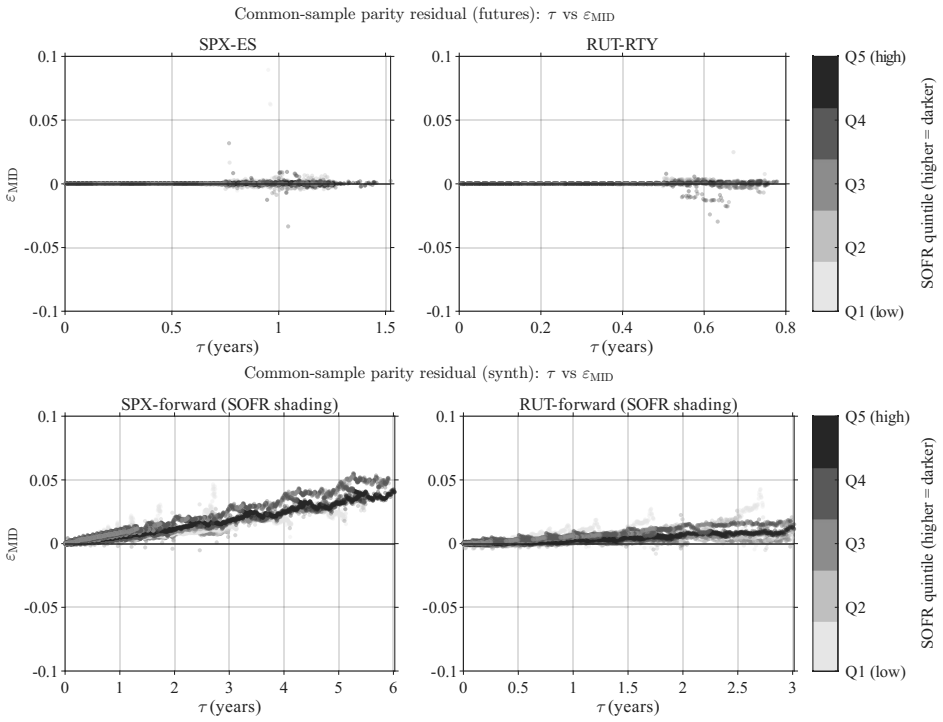

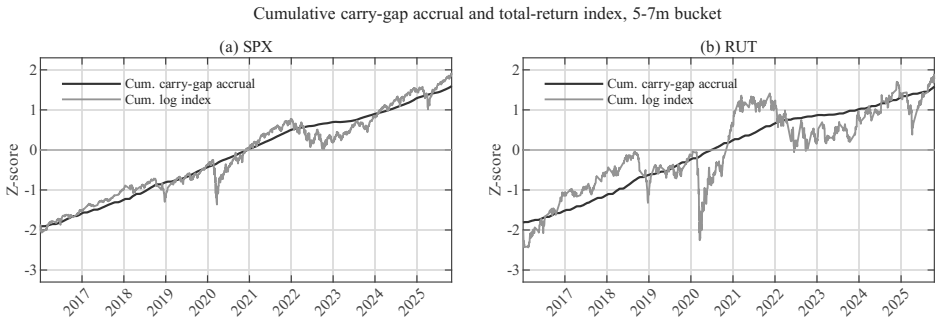

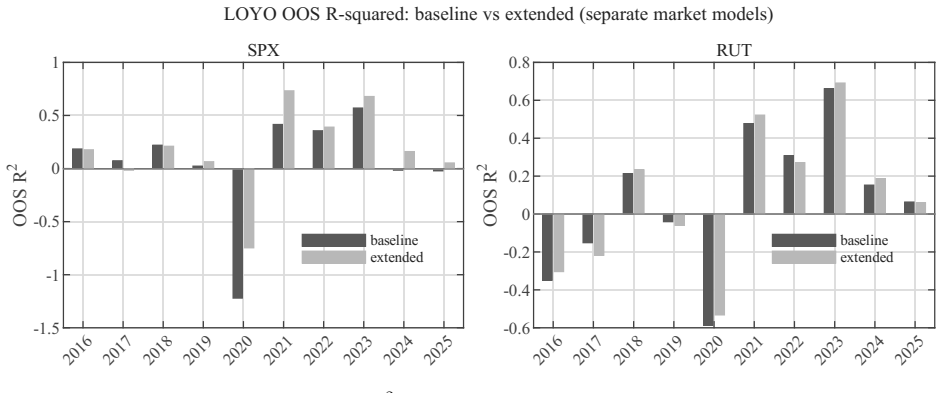

Put-call parity is a terminal-payoff identity whose enforcement consumes capital. In SPX and RUT options the quoted parity remains tightly compressed, yet the synthetic-traded forward channel exhibits a systematic wedge against OIS rates. A drift-preserving GBM term r μ̂ τ raises the explanatory power of the carry gap both in-sample and in leave-one-year-out tests, most noticeably for SPX. The pattern indicates that physical drift enters the enforcement process rather than the option payoffs themselves.

What carries the argument

The drift-preserving GBM term r μ̂ τ that augments the model of the carry gap between synthetic forwards and OIS rates.

If this is right

- The physical drift term improves both in-sample and leave-one-year-out fit of the carry gap.

- The improvement is stronger in SPX than in RUT.

- Quoted parity stays compressed while the synthetic forward channel retains the wedge.

- Physical drift affects the capital-using arbitrage channel that upholds risk-neutral parity.

Where Pith is reading between the lines

- Similar wedges may appear in other capital-intensive parity relations once the same drift adjustment is applied.

- The result suggests that risk-neutral pricing routines could be refined by embedding limited-capital dynamics when quoting synthetic forwards.

- A direct test would compare periods of abundant versus scarce arbitrage capital to see whether the required drift adjustment shrinks.

Load-bearing premise

The systematic wedge between synthetic-traded forwards and OIS rates is produced by finite arbitrage capital rather than by credit risk, liquidity premia, or data artifacts.

What would settle it

Finding that the drift term no longer improves carry-gap fit in new out-of-sample periods or when measured arbitrage capital rises would falsify the central claim.

Figures

read the original abstract

Put-call parity is a terminal-payoff identity, but its enforcement is capital-using. I study the carry gap, the annualized wedge between option-implied and OIS discount factors, in SPX and RUT index options. Quoted parity is tightly compressed, while the synthetic-traded forward channel leaves a systematic wedge. I interpret this wedge as an implementation premium under finite arbitrage capital. A drift-preserving GBM term, r {\mu}-hat {\tau}, improves in-sample and leave-one-year-out fit, especially in SPX. The evidence suggests that physical drift enters not option payoffs, but the process enforcing risk-neutral parity.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies the carry gap, defined as the annualized wedge between option-implied discount factors and OIS rates, in SPX and RUT index options. It documents that quoted parity is tightly compressed while the synthetic-traded forward channel exhibits a systematic wedge, which is interpreted as an implementation premium under finite arbitrage capital. The central claim is that incorporating a drift-preserving GBM term r μ̂ τ improves both in-sample and leave-one-year-out fit to the carry gap (especially in SPX), implying that physical drift enters the enforcement process of risk-neutral parity rather than option payoffs.

Significance. If the mechanism is substantiated, the result would link physical-measure dynamics to the maintenance of risk-neutral no-arbitrage relations under capital constraints, offering a bridge between P and Q measures with implications for arbitrage bounds and option pricing. The leave-one-year-out validation provides a modest robustness check, but the overall contribution hinges on whether the wedge is specifically attributable to arbitrage-capital limits rather than liquidity, credit, or data artifacts.

major comments (2)

- [Empirical Methodology] The estimation of μ̂ from the identical option data used to construct the carry gap (as implied by the free parameter list and the GBM functional form) introduces circularity that is load-bearing for the fit-improvement claim. The abstract states that r μ̂ τ improves in-sample and LOO fit, yet without an independent identification strategy or demonstration that the improvement survives alternative μ̂ specifications, the result may be mechanical rather than evidence for physical drift in enforcement.

- [Interpretation and Robustness] The interpretation of the wedge as an implementation premium caused by finite arbitrage capital is central to the mechanism but lacks supporting tests. No evidence is reported that the wedge covaries with capital-availability proxies, survives liquidity filters on quotes, or remains after controls for credit spreads or dividend-estimation artifacts in the synthetic forward; without these, the parametric improvement could reflect any persistent bias.

minor comments (2)

- [Data and Sample] Clarify the exact construction of the synthetic forward and the OIS rate series, including any exclusion criteria for option quotes and the precise definition of τ in the drift term.

- [Model Specification] The notation r μ̂ τ should be introduced with an explicit equation reference early in the text to avoid ambiguity in how the term is annualized and added to the parity relation.

Simulated Author's Rebuttal

We thank the referee for the insightful comments on our paper. We respond to each major comment below and outline the revisions we intend to implement to address the concerns raised.

read point-by-point responses

-

Referee: [Empirical Methodology] The estimation of μ̂ from the identical option data used to construct the carry gap (as implied by the free parameter list and the GBM functional form) introduces circularity that is load-bearing for the fit-improvement claim. The abstract states that r μ̂ τ improves in-sample and LOO fit, yet without an independent identification strategy or demonstration that the improvement survives alternative μ̂ specifications, the result may be mechanical rather than evidence for physical drift in enforcement.

Authors: We acknowledge the potential for perceived circularity in the estimation of μ̂. To address this, we will revise the manuscript to use μ̂ estimated independently from historical physical returns of the SPX and RUT indices, rather than fitting it directly to the carry gap series. We will also demonstrate that the in-sample and leave-one-year-out improvements hold under alternative specifications for μ̂, such as using pre-sample estimates or different rolling windows. This will clarify that the result reflects the role of physical drift rather than a mechanical fit. revision: yes

-

Referee: [Interpretation and Robustness] The interpretation of the wedge as an implementation premium caused by finite arbitrage capital is central to the mechanism but lacks supporting tests. No evidence is reported that the wedge covaries with capital-availability proxies, survives liquidity filters on quotes, or remains after controls for credit spreads or dividend-estimation artifacts in the synthetic forward; without these, the parametric improvement could reflect any persistent bias.

Authors: We agree that the interpretation as an implementation premium would benefit from additional empirical support. In the revised manuscript, we will add tests examining the covariance between the carry gap and proxies for arbitrage capital availability (e.g., VIX and funding liquidity measures). We will also apply liquidity filters to the quoted options, include controls for credit spreads, and address potential dividend estimation issues in the synthetic forward. These steps should help distinguish the finite-capital channel from other possible biases. revision: yes

Circularity Check

Fitting μ̂ to option-derived carry gap makes the reported fit improvement a constructed result rather than independent evidence

specific steps

-

fitted input called prediction

[Abstract]

"A drift-preserving GBM term, r μ̂ τ, improves in-sample and leave-one-year-out fit, especially in SPX. The evidence suggests that physical drift enters not option payoffs, but the process enforcing risk-neutral parity."

The parameter μ̂ is estimated from the same option data used to measure the carry gap; the improved fit is therefore achieved by tuning a free parameter to the residual the model is intended to explain, rendering the 'evidence' for physical drift entering parity enforcement statistically forced.

full rationale

The derivation chain centers on interpreting the wedge as an implementation premium and then introducing a single-parameter GBM correction r μ̂ τ that improves in-sample and LOO fit. Because μ̂ is obtained by fitting to the identical option-implied forward and OIS data that define the carry gap itself, the reported improvement reduces to a statistical fit of the residual being explained. This matches the fitted-input-called-prediction pattern and produces moderate circularity even though the GBM functional form is imported from outside the paper. No self-citation load-bearing or self-definitional steps appear in the supplied text.

Axiom & Free-Parameter Ledger

free parameters (1)

- μ̂ (physical drift estimate)

axioms (2)

- domain assumption Put-call parity is a terminal-payoff identity whose enforcement requires capital.

- ad hoc to paper GBM with constant drift is an adequate description of the enforcement process.

invented entities (1)

-

implementation premium

no independent evidence

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The baseline GBM term is this rσ√τ diffusion burden... drift-preserving extension adds a first-order directional margin-burden component proportional to rμτ

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

carry gap... implementation wedge under finite arbitrage capital

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.