Tuning in to Frequencies: How Global Assets Align with U.S. Put-Call Parity Residuals

Pith reviewed 2026-05-21 00:45 UTC · model grok-4.3

The pith

Global assets explain US put-call parity residuals after funding and volatility controls.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

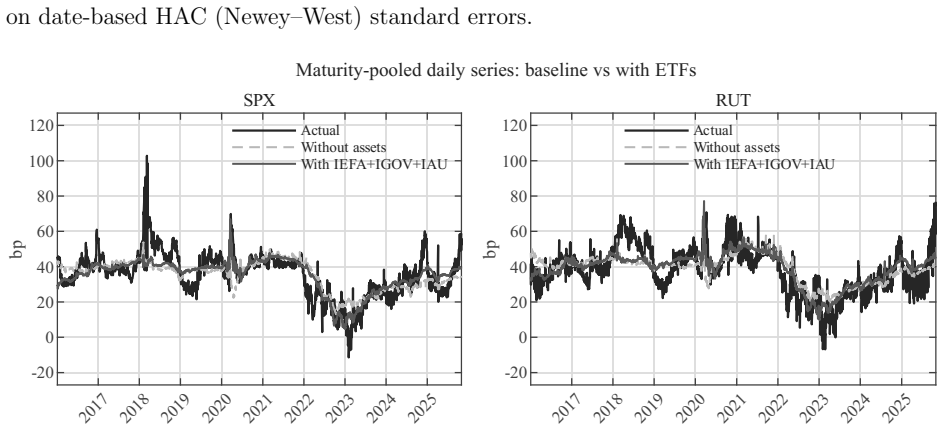

Put-call parity is risk-neutral only at terminal payoff, yet its enforcement uses capital and is therefore path-dependent. After controlling for OIS-based funding, volatility, trading frictions, and financial-condition variables, the residuals in the SPX-RUT carry gap still align with outside-option information contained in the global assets IEFA, IGOV, and IAU. The alignment survives multiple robustness layers and supports a reduced-form P-Q link in which parity enforcement reflects physical-measure investment opportunities.

What carries the argument

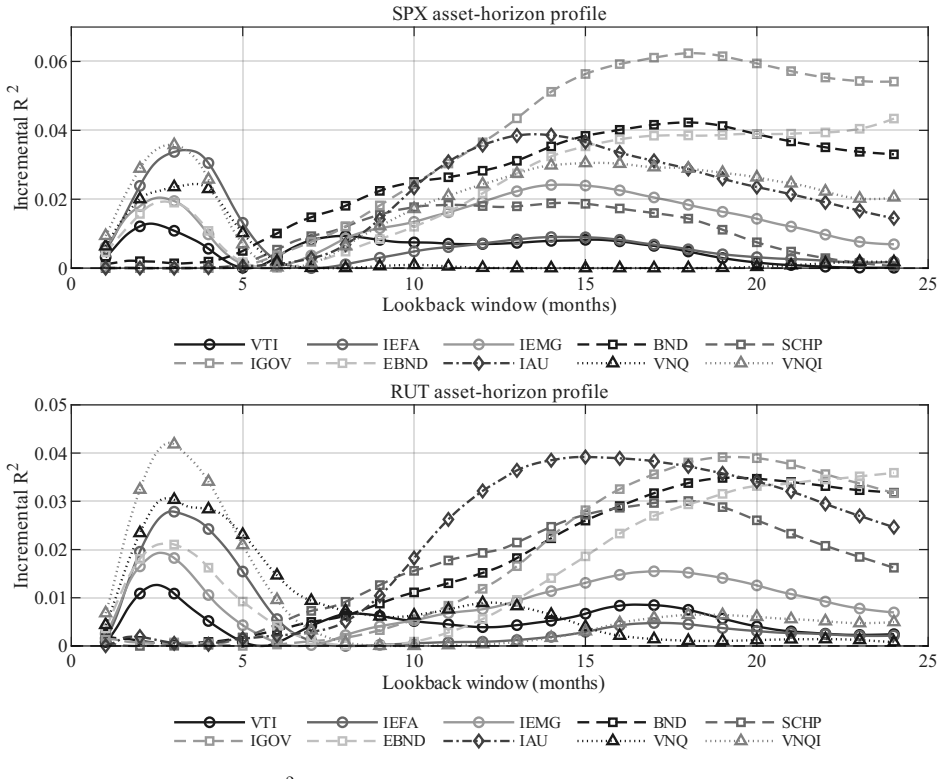

The incremental explanatory power of global asset returns (IEFA, IGOV, IAU) added after US-centered controls and robustness transformations to account for the put-call parity residual.

If this is right

- US index parity residuals carry information about international investment opportunities once local controls are removed.

- Arbitrageurs with finite capital weigh global alternatives when deciding whether to enforce put-call parity.

- Models that treat parity as a pure risk-neutral condition at payoff miss the physical-measure channels that actually bind enforcement.

- The same residual logic should apply to other capital-constrained derivative relationships across borders.

Where Pith is reading between the lines

- If the alignment holds, flows into global ETFs could help forecast near-term shifts in US index parity residuals.

- Similar patterns may appear in equity options or futures on other major indices where capital is allocated globally.

Load-bearing premise

The added global assets supply independent outside-option information that is not already captured by the US-centered controls or by the robustness procedures.

What would settle it

Finding no improvement in explanatory power or out-of-sample fit when the global assets are added to fresh data windows or to specifications that further orthogonalize against US factors would falsify the claim of residual alignment.

Figures

read the original abstract

Put-call parity is risk-neutral at terminal payoff, but its enforcement is path-dependent and capital-using. I test whether the SPX and RUT carry gap is explained by OIS-based funding, volatility, trading-friction, and financial-condition variables, or also by residual outside-option information. Adding IEFA, IGOV, and IAU improves in-sample and leave-one-year-out fit after U.S.-centered controls. Gains survive broad-dollar neutralization, alternative blocks, PCA, residualization, and nested horizon selection. Results support reduced-form P-Q alignment: finite-capital parity enforcement reflects physical-measure investment opportunities, not payoff-level no-arbitrage failure.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript tests whether residuals from put-call parity on SPX and RUT are explained solely by U.S.-centered controls (OIS funding, volatility, trading frictions, financial conditions) or also by outside-option information from global assets (IEFA, IGOV, IAU). It reports that adding the global series improves both in-sample and leave-one-year-out fit; these gains survive dollar neutralization, alternative blocks, PCA, residualization, and nested horizon selection. The central conclusion is that finite-capital parity enforcement reflects physical-measure investment opportunities rather than a failure of payoff-level no-arbitrage.

Significance. If the result holds after the requested diagnostics, the work supplies concrete empirical support for reduced-form P-Q alignment under capital constraints, showing how global physical-measure opportunities can influence U.S. option-market residuals. The manuscript already includes leave-one-year-out validation and a battery of robustness procedures (dollar neutralization, PCA, residualization), which are positive features for an empirical finance paper.

major comments (1)

- [Robustness and results sections] The robustness procedures (dollar neutralization, PCA, residualization) are described as preserving the gains from the global assets, yet no post-robustness diagnostics are reported that directly test orthogonality. Incremental R², VIF, or factor-loading tables after these steps would be required to confirm that IEFA/IGOV/IAU supply explanatory power independent of shared global-factor loadings already captured by the U.S. controls.

minor comments (2)

- [Methods] Clarify the exact construction of the 'broad-dollar neutralization' variable and whether it is applied before or after the PCA step.

- [Abstract] The abstract refers to 'nested horizon selection'; a short footnote or sentence explaining the nesting criterion would aid readability.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on our manuscript. The suggestion for additional post-robustness diagnostics is well taken and will be incorporated to strengthen the evidence on the independent contribution of the global assets.

read point-by-point responses

-

Referee: [Robustness and results sections] The robustness procedures (dollar neutralization, PCA, residualization) are described as preserving the gains from the global assets, yet no post-robustness diagnostics are reported that directly test orthogonality. Incremental R², VIF, or factor-loading tables after these steps would be required to confirm that IEFA/IGOV/IAU supply explanatory power independent of shared global-factor loadings already captured by the U.S. controls.

Authors: We appreciate this point. The manuscript states that the fit improvements from the global series survive dollar neutralization, PCA, residualization, and related checks, but we agree that explicit post-procedure diagnostics would better demonstrate orthogonality to any shared global factors already absorbed by the U.S. controls. In the revised version we will add incremental R² tables and VIF statistics computed after each robustness step. Where feasible we will also report relevant factor loadings to confirm that IEFA, IGOV, and IAU retain explanatory power beyond the U.S.-centered variables. revision: yes

Circularity Check

No significant circularity; empirical tests are self-contained

full rationale

The paper conducts an empirical regression analysis testing whether global assets (IEFA, IGOV, IAU) add explanatory power to SPX/RUT put-call parity residuals after U.S.-centered controls, with reported improvements surviving dollar neutralization, PCA, residualization, and out-of-sample checks. No equations or steps reduce a claimed prediction or result to a fitted input by construction, no self-definitional loops appear, and no load-bearing self-citations substitute for independent verification. The central interpretation follows from the reported incremental fits and robustness procedures rather than from re-labeling or re-deriving the inputs themselves.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The carry gap is a Q-measure object... whether this Q-measure carry-space residual is separable from P-measure outside-option proxies... reduced-form P–Q alignment

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

GBM term = path-risk scale × opportunity-cost component... replaced the OIS rate... with low-frequency outside-option return proxies

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.