A Triptych Approach for Reverse Stress Testing of Complex Portfolios

Pith reviewed 2026-05-25 14:48 UTC · model grok-4.3

The pith

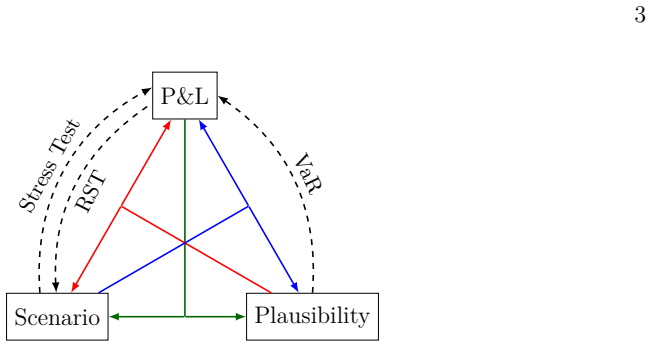

An extended reverse stress test derives any one of plausibility, loss level or scenario from the other two.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

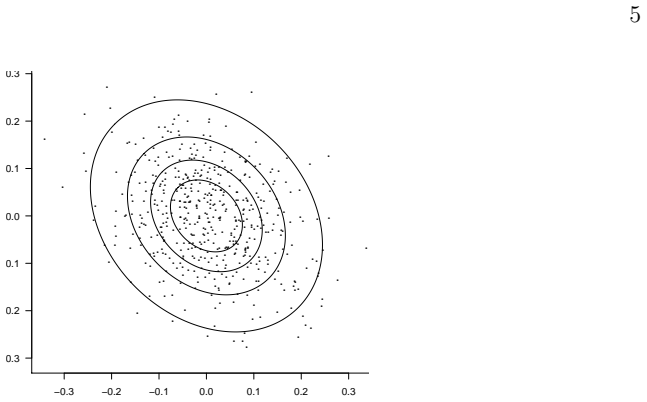

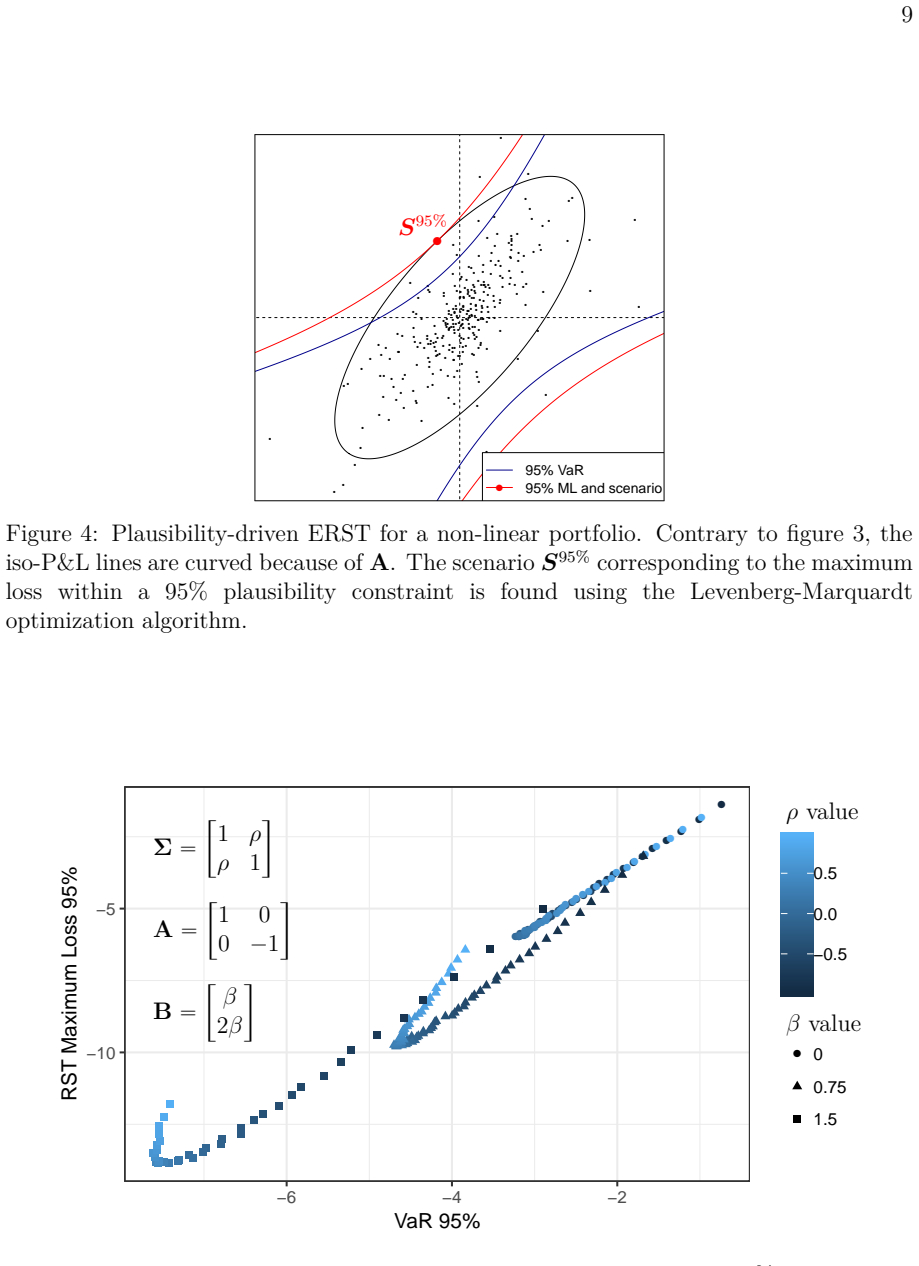

We present an Extended RST (ERST) triptych approach with three variables: level of plausibility, level of loss and scenario. In our approach, any two of these variables can be derived by providing the third as the input. We advocate and demonstrate that ERST is a powerful tool for both simple linear and complex portfolios and for both risk management as well as day-to-day portfolio management decisions. An updated new version of the Levenberg-Marquardt optimization algorithm is introduced to derive ERST in certain complex cases.

What carries the argument

The ERST triptych, in which plausibility level, loss level, and scenario are treated as interdependent so that any one can be derived when the other two are supplied.

If this is right

- ERST supplies a forward-looking risk measure that regulators and firms prefer to VaR for funds with many strategies and non-linear payoffs.

- A user can fix plausibility and loss to recover the implied scenario, or fix any other pair.

- The same framework serves both top-down risk oversight and day-to-day portfolio rebalancing decisions.

- The algorithm extension makes the triptych usable for the non-linear payoff structures common in alternative risk premia products.

Where Pith is reading between the lines

- Regulators could publish standardized values for one variable and require firms to report the other two, creating comparable stress metrics across funds.

- Portfolio managers could embed the solver in real-time systems to test what scenario would produce a target loss at a chosen plausibility level.

- The numerical approach might be tested on portfolios containing hundreds of strategies to check scaling behavior.

Load-bearing premise

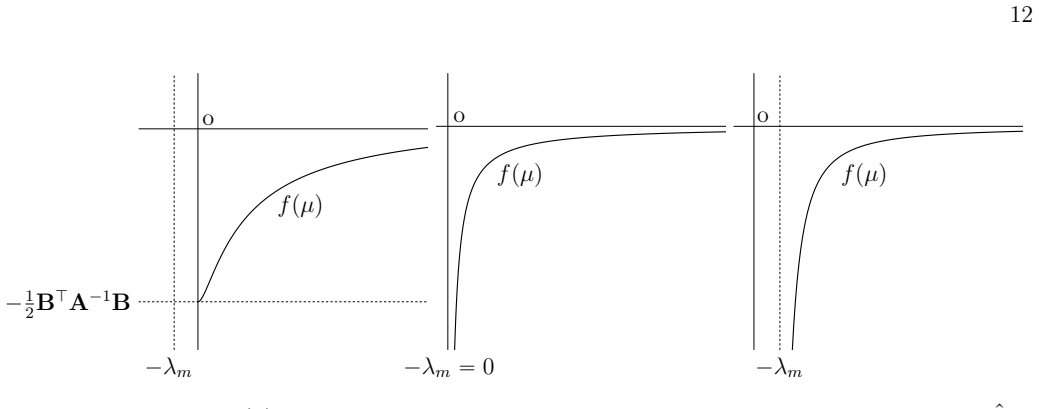

An updated Levenberg-Marquardt algorithm can reliably derive the missing variable even when portfolio payoffs are non-linear.

What would settle it

Apply the method to a synthetic portfolio whose exact mapping between plausibility, loss, and scenario is known in advance; the derived values must recover the known mapping within numerical tolerance.

Figures

read the original abstract

The quest for diversification has led to an increasing number of complex funds with a high number of strategies and non-linear payoffs. The new generation of Alternative Risk Premia (ARP) funds are an example that has been very popular in recent years. For complex funds like these, a Reverse Stress Test (RST) is regarded by the industry and regulators as a better forward-looking risk measure than a Value-at-Risk (VaR). We present an Extended RST (ERST) triptych approach with three variables: level of plausibility, level of loss and scenario. In our approach, any two of these variables can be derived by providing the third as the input. We advocate and demonstrate that ERST is a powerful tool for both simple linear and complex portfolios and for both risk management as well as day-to-day portfolio management decisions. An updated new version of the Levenberg - Marquardt optimization algorithm is introduced to derive ERST in certain complex cases.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes an Extended Reverse Stress Testing (ERST) triptych framework for complex portfolios with non-linear payoffs, such as Alternative Risk Premia funds. It defines three variables—level of plausibility, level of loss, and scenario—and claims that any two can be derived from the third as input. An updated version of the Levenberg-Marquardt algorithm is introduced to solve for the missing variable in complex cases, and the approach is presented as applicable to both risk management and day-to-day portfolio decisions, offering advantages over traditional VaR.

Significance. If the triptych relations and the updated solver are shown to be reliable, the framework could supply a flexible, forward-looking risk tool that allows regulators and managers to specify plausibility, loss, or scenario and recover the others, which is potentially useful for non-linear portfolios where standard stress testing is limited.

major comments (2)

- [Abstract] Abstract: the central claim that 'any two of these variables can be derived by providing the third as the input' and that the updated LM algorithm 'reliably derives' the missing variable for non-linear payoffs rests on an unstated mathematical mapping and solver modification; no equations, Jacobian definition, or damping schedule are supplied to support this.

- [Abstract] Abstract: no convergence analysis, basin-of-attraction study, or numerical comparison against standard LM or other solvers on non-linear test cases is referenced, which is load-bearing for the assertion that ERST succeeds for complex portfolios.

minor comments (2)

- [Abstract] The phrase 'updated new version' is redundant; 'updated version' suffices.

- [Abstract] The abstract would benefit from a single sentence indicating the nature of the portfolio examples (linear vs. non-linear) used to demonstrate the triptych.

Simulated Author's Rebuttal

We thank the referee for their constructive comments. We respond point-by-point to the major comments below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central claim that 'any two of these variables can be derived by providing the third as the input' and that the updated LM algorithm 'reliably derives' the missing variable for non-linear payoffs rests on an unstated mathematical mapping and solver modification; no equations, Jacobian definition, or damping schedule are supplied to support this.

Authors: The triptych relations and mapping between plausibility, loss and scenario are defined with explicit equations in Section 2. The updated Levenberg-Marquardt algorithm, including Jacobian and damping schedule modifications, is detailed in Section 4. We will revise the abstract to reference these sections and key solver aspects. revision: yes

-

Referee: [Abstract] Abstract: no convergence analysis, basin-of-attraction study, or numerical comparison against standard LM or other solvers on non-linear test cases is referenced, which is load-bearing for the assertion that ERST succeeds for complex portfolios.

Authors: Section 5 contains numerical examples applying the solver to complex non-linear portfolios that illustrate its practical reliability. A dedicated convergence or basin-of-attraction analysis is not included, as the paper's scope centers on the ERST framework and its use cases rather than solver theory; the empirical results support the claims within this scope. revision: no

Circularity Check

No circularity: methodological framework presented without self-referential reductions

full rationale

The paper introduces an Extended RST triptych with three variables (plausibility, loss, scenario) where any two are derived from the third via an updated Levenberg-Marquardt algorithm. No equations, fitted parameters, or derivations are shown that reduce by construction to the inputs (no self-definitional loops, no fitted quantities renamed as predictions, and no load-bearing self-citations). The central claim rests on the assertion that the algorithm enables the derivations for non-linear portfolios, but this is presented as a methodological contribution rather than a closed derivation chain that presupposes its own outputs. The approach is self-contained as a proposed framework without internal circular reductions.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

[BBP16] Joel BUN, Jean-Philippe BOUCHAUD, and Marc POTTERS. “Cleaning Correlation Matrices”. In:Risk Magazine(2016). [BRE+09] Thomas BREUER et al. “How to Find Plausible, Severe, and Useful Stress Scenarios”. In:International Journal of Central Banking(2009), pp. 205–224. [BRE06] Thomas BREUER. “Providing Against the Worst: Risk Capital for Worst Case Sce...

work page 2016

-

[2]

AFactor-ModelApproach for Correlation Scenarios and Correlation Stress Testing

[PW19] NataliePACKHAMandFabianWOEBBEKING.“AFactor-ModelApproach for Correlation Scenarios and Correlation Stress Testing”. In: Journal of Banking & Finance101 (Apr. 2019), pp. 92–103. [ROU97] Christophe ROUVINEZ. “Going Greek with VaR”. In: Risk Magazine 10 (Feb. 1997). [SAD] Jules SADEFO-KAMDEM. “Value at Risk and Expected Shortfall for Linear Portfolios...

work page 2019

-

[3]

Quantifying Backtest Overfitting in Alternative Beta Strategies

[SLP17] Antti SUHONEN, Matthias LENNKH, and Fabrice PEREZ. “Quantifying Backtest Overfitting in Alternative Beta Strategies”. In:Journal of Portfolio Management 43 (2017). [STU97] GeroldSTUDER.“MaximumLossofMeasurementofMarketRisk”.PhDthesis. Swiss Federal Institute of Technology, 1997

work page 2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.