Optimal payoff under Bregman-Wasserstein divergence constraints

Pith reviewed 2026-05-23 17:31 UTC · model grok-4.3

The pith

Optimal payoff for expected utility maximizers is derived explicitly under Bregman-Wasserstein divergence constraints to a benchmark.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

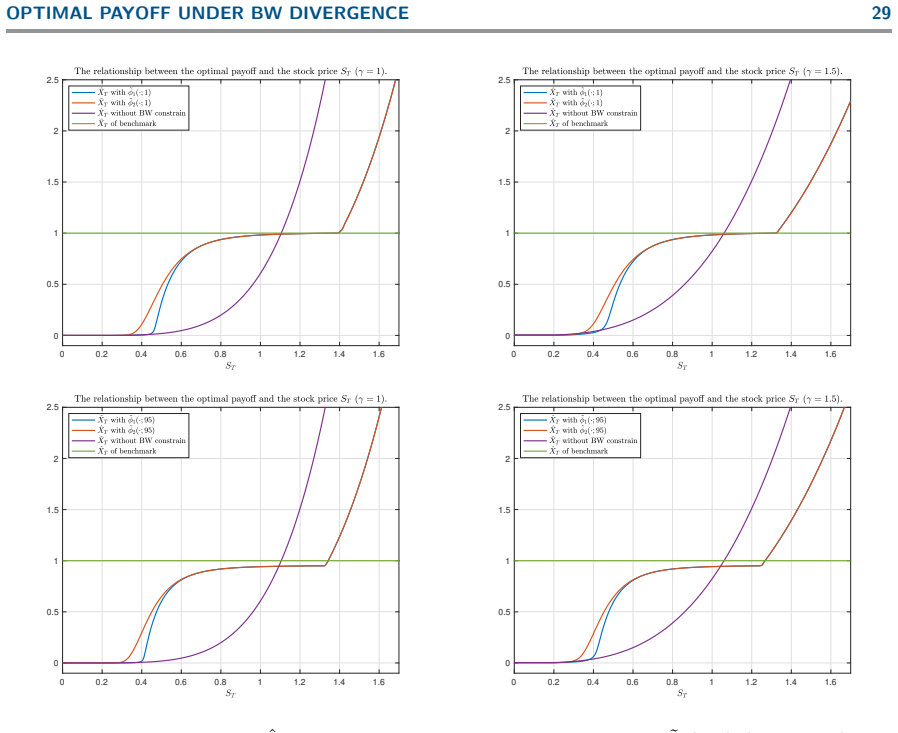

We provide the optimal payoff in the setting where an expected utility maximizer's payoff is constrained via a Bregman-Wasserstein divergence generated by a convex function phi. Unlike the case when phi(x)=x^2 which recovers the Wasserstein distance, the asymmetry permits penalizing positive deviations differently than negative ones. Numerical examples illustrate that the choice of phi allows to better align the payoff choice with the objectives of investors.

What carries the argument

The Bregman-Wasserstein divergence generated by a convex function phi, which constrains the distance between the chosen payoff and the benchmark in the utility maximization problem.

If this is right

- The optimal payoff admits an explicit form once phi is fixed.

- The asymmetry of the divergence allows separate control over penalties for outperformance versus underperformance relative to the benchmark.

- Numerical choices of phi produce payoffs that align more closely with investor objectives than the symmetric Wasserstein case.

Where Pith is reading between the lines

- The same explicit-solution approach could be tested on other benchmark-constrained problems in portfolio selection where over- and under-performance carry unequal costs.

- Specific families of phi might be calibrated to match observed investor behavior in real market data.

Load-bearing premise

The deviation between the chosen payoff and the benchmark is assessed via a Bregman-Wasserstein divergence generated by a convex function phi.

What would settle it

A concrete counterexample in which another feasible payoff yields strictly higher expected utility than the derived candidate while satisfying the same Bregman-Wasserstein constraint for a chosen phi would falsify the optimality claim.

Figures

read the original abstract

We study optimal payoff choice for an expected utility maximizer under the constraint that their payoff is not allowed to deviate ``too much'' from a given benchmark. We solve this problem when the deviation is assessed via a Bregman-Wasserstein (BW) divergence, generated by a convex function $\phi$. Unlike the Wasserstein distance (i.e., when $\phi(x)=x^2$) the inherent asymmetry of the BW divergence makes it possible to penalize positive deviations different than negative ones. As a main contribution, we provide the optimal payoff in this setting. Numerical examples illustrate that the choice of $\phi$ allow to better align the payoff choice with the objectives of investors.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies the problem of choosing an optimal payoff for an expected-utility maximizer subject to a constraint that the payoff cannot deviate too much from a given benchmark, where deviation is measured by a Bregman-Wasserstein divergence generated by an arbitrary convex function φ. Unlike the symmetric Wasserstein case (φ(x)=x²), the asymmetry of the BW divergence permits different penalization of positive and negative deviations. The central claim is an explicit closed-form expression for the optimal payoff; numerical examples are provided to illustrate how the choice of φ aligns the solution with investor objectives.

Significance. If the derivation is valid for general convex φ, the result supplies a tractable, asymmetric extension of existing Wasserstein-constrained portfolio problems. The explicit payoff formula would be a useful theoretical and computational contribution in quantitative finance, particularly for applications where one-sided risk constraints matter. The numerical illustrations provide concrete evidence of practical flexibility.

major comments (2)

- [§3, Theorem 3.1] §3, Theorem 3.1 (or the main derivation of the optimal payoff): the explicit form X^*=T(B) with deterministic transport map T relies on the Bregman cost D_φ satisfying the twist condition or c-convexity so that the dual problem yields a deterministic coupling. For arbitrary convex φ this need not hold (e.g., when φ'' changes sign or is not strictly convex), and the manuscript does not state or verify the required regularity on φ. This assumption is load-bearing for the claimed closed-form optimality.

- [§2.2] §2.2 (definition of the BW constraint) and the subsequent optimization: the problem is posed as an expectation under the physical measure, yet the BW divergence is defined via an optimal-transport problem between the law of the payoff and the benchmark law. The manuscript does not clarify whether the constraint is enforced pathwise or in law, nor how the utility maximizer interacts with the measure-theoretic formulation; this affects whether the stated pointwise argmax solution remains optimal.

minor comments (2)

- [§2] Notation for the convex function φ and the resulting divergence D_φ is introduced without an explicit list of standing assumptions (strict convexity, twice differentiability, etc.). Adding a short paragraph or assumption box would improve readability.

- [§4] The numerical examples in §4 would benefit from a table reporting the realized BW divergence values and utility gains for each φ, to make the comparison quantitative rather than visual only.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. The comments highlight important points regarding the regularity assumptions and the measure-theoretic formulation. We address each major comment below and indicate the revisions we will make.

read point-by-point responses

-

Referee: [§3, Theorem 3.1] §3, Theorem 3.1 (or the main derivation of the optimal payoff): the explicit form X^*=T(B) with deterministic transport map T relies on the Bregman cost D_φ satisfying the twist condition or c-convexity so that the dual problem yields a deterministic coupling. For arbitrary convex φ this need not hold (e.g., when φ'' changes sign or is not strictly convex), and the manuscript does not state or verify the required regularity on φ. This assumption is load-bearing for the claimed closed-form optimality.

Authors: We agree that the deterministic transport map in Theorem 3.1 requires the Bregman cost to satisfy the twist condition, which holds when φ is strictly convex, twice continuously differentiable, and φ'' > 0 everywhere. While the manuscript refers to an 'arbitrary convex function φ', the derivation implicitly uses these conditions to guarantee c-convexity and a deterministic optimal coupling. We will revise the statement of Theorem 3.1 (and the surrounding discussion in §3) to explicitly list the required assumptions on φ. This narrows the claim but preserves the closed-form result under the stated conditions. revision: yes

-

Referee: [§2.2] §2.2 (definition of the BW constraint) and the subsequent optimization: the problem is posed as an expectation under the physical measure, yet the BW divergence is defined via an optimal-transport problem between the law of the payoff and the benchmark law. The manuscript does not clarify whether the constraint is enforced pathwise or in law, nor how the utility maximizer interacts with the measure-theoretic formulation; this affects whether the stated pointwise argmax solution remains optimal.

Authors: The BW divergence constraint is enforced at the level of the laws (i.e., between the pushforward measures of X and B under the physical measure P). The optimization is an expectation under P, but the feasible set is defined via the OT problem between the marginal laws. The pointwise argmax solution yields a deterministic map X = T(B), which induces a coupling supported on the graph of T; this coupling is optimal for the dual formulation and therefore satisfies the law-level constraint. We will add a clarifying paragraph in §2.2 that explicitly distinguishes the pathwise payoff from the distributional constraint and confirms that the deterministic map remains optimal in this measure-theoretic setting. revision: yes

Circularity Check

No circularity: optimal payoff derived from external divergence constraint

full rationale

The paper states it solves for the optimal payoff of an expected utility maximizer subject to a Bregman-Wasserstein divergence constraint generated by an arbitrary convex phi. The abstract and skeptic summary present this as a mathematical derivation under an externally defined divergence, with no indication that the claimed optimum is obtained by fitting parameters to data, redefining the objective in terms of itself, or relying on a load-bearing self-citation whose content reduces to the present result. No equations or steps are shown that equate the output payoff to an input by construction. The derivation is therefore treated as self-contained against the stated external constraint.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel echoes?

echoesECHOES: this paper passage has the same mathematical shape or conceptual pattern as the Recognition theorem, but is not a direct formal dependency.

arg min ... -u(˘G(t)) + λ c(˘G) + μ Bϕ(˘G, ˘Fb) ... ht(y) := -u(y) + μ ϕ(y) + λ y ˘FφT(1-t) - μ ϕ'(˘Fb(t)) y

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Bregman generator ϕ ... Bϕ(z1,z2) := ϕ(z1)-ϕ(z2)-ϕ'(z2)(z1-z2)

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Forward citations

Cited by 1 Pith paper

-

Distributionally Robust Insurance under Bregman-Wasserstein Divergence

Closed-form optimal indemnity functions and worst-case distributions are derived for alpha-maxmin VaR insurance demand and for minimizing worst-case convex distortion risk measures subject to VaR constraints, using as...

Reference graph

Works this paper leans on

-

[1]

Balder, E. J. (1984). A general approach to lower semicontinuity and lower closure in optimal control theory. SIAM journal on control and optimization , 22(4):570--598

work page 1984

-

[2]

Barbu, V. and Precupanu, T. (2012). Convexity and optimization in Banach spaces . Springer Science & Business Media

work page 2012

-

[3]

Basak, S. and Shapiro, A. (2001). Value-at-risk-based risk management: optimal policies and asset prices. The review of financial studies , 14(2):371--405

work page 2001

-

[4]

Bayraktar, E., Belak, C., Christensen, S., and Seifried, F. T. (2022). Convergence of optimal investment problems in the vanishing fixed cost limit. SIAM Journal on Control and Optimization , 60(5):2712--2736

work page 2022

-

[5]

Belak, C., Mich, L., and Seifried, F. T. (2022). Optimal investment for retail investors. Mathematical Finance , 32(2):555--594

work page 2022

-

[6]

Bernard, C., Boyle, P. P., and Vanduffel, S. (2014). Explicit representation of cost-efficient strategies. Finance , 35(2):5--55

work page 2014

-

[7]

Bernard, C., Chen, J. S., and Vanduffel, S. (2015a). Rationalizing investors’ choices. Journal of Mathematical Economics , 59:10--23

-

[8]

Bernard, C., Junike, G., Lux, T., and Vanduffel, S. (2024a). Cost-efficient payoffs under model ambiguity. Finance and Stochastics , pages 1--33

-

[9]

Bernard, C., Moraux, F., R\"uschendorf, L., and Vanduffel, S. (2015b). Optimal payoffs under state-dependent constraints. Quantitative Finance , 15(7):1157--1173

-

[10]

Bernard, C., Pesenti, S. M., and Vanduffel, S. (2024b). Robust distortion risk measures. Mathematical Finance , 34(3):774--818

-

[11]

Bi, X., Yuan, L., Cui, Z., Fan, J., and Zhang, S. (2023). Optimal investment problem under behavioral setting: A L agrange duality perspective. Journal of Economic Dynamics and Control , 156:104751

work page 2023

-

[12]

Boudt, K., Dragun, K., and Vanduffel, S. (2022). The optimal payoff for a yaari investor. Quantitative Finance , 22(10):1839--1852

work page 2022

-

[13]

Boyd, S. and Vandenberghe, L. (2004). Convex optimization . Cambridge university press

work page 2004

-

[14]

Breeden, D. T. and Litzenberger, R. H. (1978). Prices of state-contingent claims implicit in option prices. The Journal of Business , 51(4):621--651

work page 1978

-

[15]

Burgert , C. and R\"uschendorf , L. (2006). On the optimal risk allocation problem. Stat. Decis. , 24(1):153--171

work page 2006

-

[16]

Carlier , G. and Dana , R.-A. (2006). Law invariant concave utility functions and optimization problems with monotonicity and comonotonicity constraints. Stat. Decis. , 24(1):127--152

work page 2006

-

[17]

Carlier, G. and Dana, R.-A. (2011). Optimal demand for contingent claims when agents have law invariant utilities. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , 21(2):169--201

work page 2011

-

[18]

Carlier, G. and Jimenez, C. (2007). On monge's problem for bregman-like cost functions. Journal of Convex Analysis , 14(3):647

work page 2007

-

[19]

Carr, P. and Chou, A. (1997). Breaking barriers: Presenting a method of static replication for barrier securities. Risk , 10:139--145

work page 1997

-

[20]

Chen, A., Stadje, M., and Zhang, F. (2024). On the equivalence between value-at-risk-and expected shortfall-based risk measures in non-concave optimization. Insurance: Mathematics and Economics , 117:114--129

work page 2024

-

[21]

Cuoco, D., He, H., and Isaenko, S. (2008). Optimal dynamic trading strategies with risk limits. Operations Research , 56(2):358--368

work page 2008

-

[22]

Dybvig, P. H. (1988). Distributional Analysis of Portfolio Choice . Journal of Business , 61(3):369--393

work page 1988

-

[23]

F\"ollmer , H. and Schied , A. (2004). Stochastic Finance. An Introduction in Discrete Time. Berlin: de Gruyter, 2nd revised and extended edition

work page 2004

-

[24]

Ghossoub, M. and Zhu, M. B. (2025). Risk-constrained portfolio choice under rank-dependent utility. Finance and Stochastics , 29(2):399--442

work page 2025

-

[25]

Harlow, W. V. (1991). Asset allocation in a downside-risk framework. Financial analysts journal , 47(5):28--40

work page 1991

-

[26]

He, H. and Zhou, X. Y. (2011). Portfolio choice via quantiles. Mathematical Finance , 21:203--231

work page 2011

-

[27]

He, X. D. and Jiang, Z. (2021). Optimal payoff under the generalized dual theory of choice. Operations Research Letters , 49(3):372--376

work page 2021

-

[28]

He, X. D. and Zhou, X. Y. (2016). Hope, fear, and aspirations. Mathematical Finance , 26(1):3--50

work page 2016

-

[29]

Jaimungal, S., Pesenti, S. M., Wang, Y. S., and Tatsat, H. (2022). Robust risk-aware reinforcement learning. SIAM Journal on Financial Mathematics , 13(1):213--226

work page 2022

-

[30]

Jin, H. and Zhou, X. Y. (2008). Behavioral portfolio selection in continuous time. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , 18(3):385--426

work page 2008

-

[31]

S., Rankin, C., and Wong, T.-K

Kainth, A. S., Rankin, C., and Wong, T.-K. L. (2025). Bregman-wasserstein divergence: Geometry and applications. IEEE Transactions on Information Theory

work page 2025

-

[32]

Kassberger, S. and Liebmann, T. (2012). When are path-dependent payoffs suboptimal? Journal of Banking & Finance , 36(5):1304--1310

work page 2012

-

[33]

Klebaner, F., Landsman, Z., Makov, U., and Yao, J. (2017). Optimal portfolios with downside risk. Quantitative Finance , 17(3):315--325

work page 2017

-

[34]

Lopes, L. L. (1987). Between hope and fear: The psychology of risk. Advances in Experimental Social Psychology , 20:255--295

work page 1987

-

[35]

Magnani, J., Rabanal, J. P., Rud, O. A., and Wang, Y. (2022). Efficiency of dynamic portfolio choices: An experiment. The Review of Financial Studies , 35(3):1279--1309

work page 2022

-

[36]

Nachman, D. (1988). Spanning and completeness with options. The Review of Financial Studies , 1(3):311--328

work page 1988

-

[37]

Pesenti, S. M. and Jaimungal, S. (2023). Portfolio optimisation within a W asserstein ball. SIAM Journal on Financial Mathematics , 14(4):1175--1214

work page 2023

-

[38]

Pesenti, S. M. and Vanduffel, S. (2024). Optimal transport divergences induced by scoring functions. Operations Research Letters , 57:107146

work page 2024

-

[39]

Quiggin, J. (1993). Generalized Expected Utility Theory -- The Rank-Dependent Model . Kluwer Academic Publishers

work page 1993

-

[40]

Ross, S. (1976). Options and efficiency. The Quarterly Journal of Economics , 90(1):75--89

work page 1976

-

[41]

R \"u schendorf, L. and Vanduffel, S. (2020). On the construction of optimal payoffs. Decisions in Economics and Finance , pages 1--25

work page 2020

-

[42]

Shefrin, H. M. and Statman, M. (2000). Behavioral portfolio theory. Journal of Financial and Quantitative Analysis , 35(2):127--151

work page 2000

-

[43]

Tversky, A. and Kahneman, D. (1992). Advances in prospect theory: C umulative representation of uncertainty. Journal of Risk and Uncertainty , 5(4):297--323

work page 1992

-

[44]

Von Hammerstein, E. A., L \"u tkebohmert, E., R \"u schendorf, L., and Wolf, V. (2014). Optimality of payoffs in l \'e vy models. International Journal of Theoretical and Applied Finance , 17(06):1450041

work page 2014

-

[45]

von Neumann, J. and Morgenstern, O. (1947). Theory of Games and Economic Behavior. Princeton University Press, 2nd edition

work page 1947

-

[46]

Wei, P. (2021). Risk management with expected shortfall. Mathematics and Financial Economics , pages 1--37

work page 2021

-

[47]

Xia, J. and Zhou, X. Y. (2016). Arrow--debreu equilibria for rank-dependent utilities. Mathematical Finance , 26(3):558--588

work page 2016

-

[48]

Xu, Z. Q. (2014). A new characterization of comonotonicity and its application in behavioral finance. Journal of Mathematical Analysis and Applications , 418(2):612--625

work page 2014

-

[49]

Xu, Z. Q. (2016). A note on the quantile formulation. Mathematical Finance , 26(3):589--601

work page 2016

-

[50]

Xu , Z. Q. and Zhou , X. Y. (2013). Optimal stopping under probability distortion. Ann. Appl. Probab. , 23(1):251--282

work page 2013

-

[51]

Yaari, M. (1987). The dual theory of choice under risk. Econometrica , 55:95--115

work page 1987

-

[52]

Zhang, S., Jin, H. Q., and Zhou, X. Y. (2011). Behavioral portfolio selection with loss control. Acta Mathematica Sinica, English Series , 27(2):255--274

work page 2011

-

[53]

" write newline "" before.all 'output.state := FUNCTION fin.entry add.period write newline FUNCTION new.block output.state before.all = 'skip after.block 'output.state := if FUNCTION not #0 #1 if FUNCTION and 'skip pop #0 if FUNCTION or pop #1 'skip if FUNCTION new.block.checka empty 'skip 'new.block if FUNCTION field.or.null duplicate empty pop "" 'skip ...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.