Multivariate Rough Volatility

Pith reviewed 2026-05-23 07:05 UTC · model grok-4.3

The pith

A multivariate fractional Ornstein-Uhlenbeck process for log-volatilities captures asymmetries in cross-covariances and resulting spillover effects.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

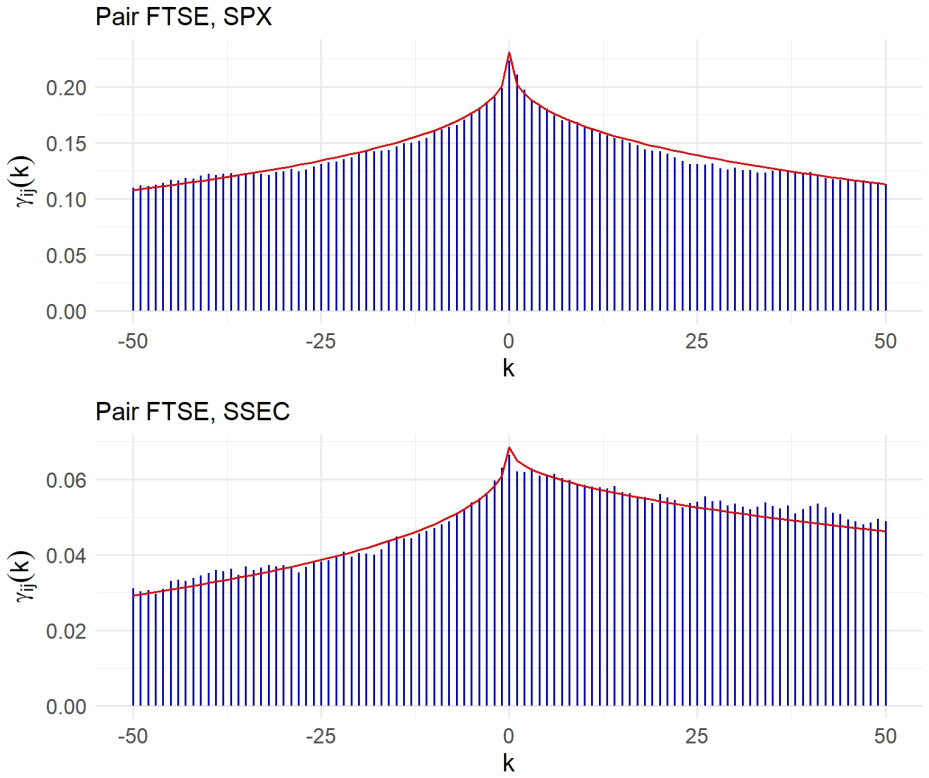

The joint dynamics of log-volatilities are modeled by a multivariate fractional Ornstein-Uhlenbeck process, which permits different Hurst exponents in each marginal and nontrivial interdependencies. This captures the strong correlations and asymmetries in the empirical cross-covariance functions of realized volatility time series. The asymmetries produce spillover effects that are derived analytically in the model and quantified using empirical parameter estimates. The analysis confirms behaviors close to non-stationarity and rough trajectories.

What carries the argument

multivariate fractional Ornstein-Uhlenbeck process for the joint dynamics of log-volatilities, allowing varying Hurst exponents and interdependencies to generate correlated rough paths and asymmetric cross-covariances.

If this is right

- The model analytically derives spillover effects from the asymmetric cross-covariances.

- Spillover magnitudes can be computed from estimated model parameters.

- The generalized method of moments estimator jointly identifies all parameters with established asymptotic properties.

- Different Hurst exponents can be accommodated for different volatility series.

- Empirical fits confirm strong correlations and rough, near-nonstationary trajectories.

Where Pith is reading between the lines

- Such a model could enable better forecasting of volatility transmissions in multi-asset portfolios.

- Extensions might incorporate the model into pricing frameworks for options on multiple underlyings.

- Testing the predicted spillovers on out-of-sample data or during market stress periods would provide further validation.

Load-bearing premise

The joint dynamics of log-volatilities are generated by a multivariate fractional Ornstein-Uhlenbeck process with possibly different Hurst exponents per marginal.

What would settle it

Observing realized volatility time series whose cross-covariance functions lack the predicted asymmetries or whose spillover patterns do not match the analytically derived effects from the fitted parameters would challenge the model's validity.

Figures

read the original abstract

Motivated by empirical evidence from the joint behavior of realized volatility time series, we propose to model the joint dynamics of log-volatilities using a multivariate fractional Ornstein-Uhlenbeck process. This model is a multivariate version of the Rough Fractional Stochastic Volatility model introduced in [Gatheral, Jaisson, and Rosenbaum, Quant. Finance, 2018]. It allows for different Hurst exponents in the different marginal components and non trivial interdependencies. We discuss the main features of the model and propose a Generalized Method of Moments estimator that jointly identifies its parameters. We derive the asymptotic theory of the estimator and perform a simulation study that confirms the asymptotic theory in finite sample. We conduct an extensive empirical investigation of all realized-volatility time series covering the entire span of about two decades in the Oxford-Man realized library, and of a small spot-volatility system. Our analysis shows that these time series are strongly correlated and can exhibit asymmetries in their empirical cross-covariance function, accurately captured by our model. These asymmetries lead to spillover effects, which we derive analytically within our model and compute based on empirical estimates of model parameters. Moreover, in accordance with the existing literature, we observe behaviors close to non-stationarity and rough trajectories.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a multivariate fractional Ornstein-Uhlenbeck process for the joint dynamics of log-volatilities, allowing heterogeneous Hurst exponents and non-trivial cross-dependencies. It develops a GMM estimator, derives its asymptotic theory, validates the asymptotics via simulation, and applies the model empirically to realized-volatility series from the Oxford-Man library (plus a spot-volatility system). The central empirical claim is that the model accurately reproduces observed asymmetries in cross-covariance functions, from which analytic spillover effects are derived and computed using fitted parameters; the analysis also reports near-non-stationary and rough behavior consistent with prior literature.

Significance. If the multivariate fOU construction is well-defined for distinct Hurst parameters and the GMM estimator is consistent, the work supplies a flexible multivariate extension of the rough-volatility model together with closed-form spillover expressions and an extensive two-decade empirical calibration. The simulation confirmation of asymptotics and the joint identification of all parameters (including cross-dependence) are concrete strengths.

major comments (1)

- [§2 (model definition)] Model definition (presumably §2): when H_i ≠ H_j the cross-covariance kernel must obey a Hölder regularity condition of order min(H_i, H_j) for the full covariance operator to remain positive semi-definite. The manuscript does not report any verification that the estimated parameters satisfy this restriction for the fitted models used to compute spillover effects; this is load-bearing for the analytic derivations and the claim that the model “accurately captures” the observed asymmetries.

Simulated Author's Rebuttal

We thank the referee for the careful reading and for identifying this important technical point on the model construction. We address the comment below.

read point-by-point responses

-

Referee: Model definition (presumably §2): when H_i ≠ H_j the cross-covariance kernel must obey a Hölder regularity condition of order min(H_i, H_j) for the full covariance operator to remain positive semi-definite. The manuscript does not report any verification that the estimated parameters satisfy this restriction for the fitted models used to compute spillover effects; this is load-bearing for the analytic derivations and the claim that the model “accurately captures” the observed asymmetries.

Authors: We agree that the Hölder regularity condition of order min(H_i, H_j) on the cross-covariance kernel is required to guarantee that the covariance operator remains positive semi-definite when the Hurst exponents differ. The multivariate fOU process is defined via a linear combination of fractional Brownian motions with a positive-definite instantaneous covariance matrix, and the resulting covariance kernels are constructed to satisfy the necessary regularity for the operator to be well-defined. However, the manuscript does not explicitly verify that the GMM-estimated parameters obey this condition for the pairs used in the spillover calculations. In the revised version we will add this verification (both in the model section and for all reported empirical fits), confirming that the fitted (H_i, H_j, cross-correlation) triples satisfy the required Hölder bound. This will be reported as an additional table or statement in the empirical section. revision: yes

Circularity Check

No circularity; model definition, GMM estimation, and analytic derivations are independent

full rationale

The paper introduces a multivariate fractional OU extension of the Gatheral et al. (2018) univariate model, specifies a GMM estimator that matches model moments to empirical data, derives the estimator's asymptotics, and computes spillover effects from the closed-form cross-covariance structure. These steps rely on the model's explicit kernel and standard GMM theory rather than any fitted quantity being renamed as a prediction or any self-citation chain. The derivation chain is self-contained against external benchmarks and does not reduce any claimed result to its own inputs by construction.

Axiom & Free-Parameter Ledger

free parameters (2)

- Hurst exponents

- Cross-dependence parameters

axioms (1)

- domain assumption Joint log-volatility dynamics are generated by a multivariate fractional Ornstein-Uhlenbeck process

Reference graph

Works this paper leans on

-

[1]

The multivariate fractional Ornstein–Uhlenbeck process , journal =

Ranieri Dugo and Giacomo Giorgio and Paolo Pigato , keywords =. The multivariate fractional Ornstein–Uhlenbeck process , journal =. 2026 , issn =. doi:https://doi.org/10.1016/j.spa.2025.104814 , url =

-

[2]

Mazzonetto, Sara and Pigato, Paolo , journal=

-

[3]

Scandinavian Journal of Statistics , volume=

Contrast function estimation for the drift parameter of ergodic jump diffusion process , author=. Scandinavian Journal of Statistics , volume=. 2020 , publisher=

work page 2020

-

[4]

Available at SSRN: https://ssrn.com/abstract=4428407 , year=

Tests for Hurst effect , author=. Available at SSRN: https://ssrn.com/abstract=4428407 , year=

-

[5]

Ben Alaya, M. and Kebaier, A. , title =. Stochastic Analysis and Applications , volume =. 2013 , publisher =

work page 2013

-

[6]

Scandinavian Journal of Statistics , volume =

Kessler, Mathieu , title =. Scandinavian Journal of Statistics , volume =

-

[7]

Mathematical Finance , volume =

Fukasawa, Masaaki and Takabatake, Tetsuya and Westphal, Rebecca , title =. Mathematical Finance , volume =

-

[8]

Giulia Livieri and Saad Mouti and Andrea Pallavicini and Mathieu Rosenbaum , title =. IISE Transactions , volume =. 2018 , publisher =

work page 2018

-

[9]

and Hoffmann, Marc and Liu, Yanghui and Rosenbaum, Mathieu and Szymanski, Gr goire , year=

Chong, Carsten H. and Hoffmann, Marc and Liu, Yanghui and Rosenbaum, Mathieu and Szymanski, Gr goire , year=. Statistical inference for rough volatility: Central limit theorems , volume=. The Annals of Applied Probability , publisher=. doi:10.1214/23-aap2002 , number=

-

[10]

arXiv preprint arXiv:2210.01214 , year=

Statistical inference for rough volatility: Minimax Theory , author=. arXiv preprint arXiv:2210.01214 , year=

-

[11]

Bayer, C. and Friz,. Pricing under rough volatility , journal =. 2016 , publisher =. doi:10.1080/14697688.2015.1099717 , URL =

-

[12]

Turbocharging Monte Carlo pricing for the rough Bergomi model

Bayer, C. and Friz,. Short-time near-the-money skew in rough fractional volatility models , JOURNAL =. 2019 , NUMBER =. doi:10.1080/14697688.2018.1529420 , URL =

-

[13]

Quantitative Finance , volume=

Time reversal invariance in finance , author=. Quantitative Finance , volume=. 2009 , publisher=

work page 2009

-

[14]

Quantitative Finance , volume =

Marcus Cordi and Damien Challet and Serge Kassibrakis , title =. Quantitative Finance , volume =. 2021 , publisher =

work page 2021

-

[15]

Communications in Nonlinear Science and Numerical Simulation , volume =. 2023 , issn =. doi:https://doi.org/10.1016/j.cnsns.2023.107582 , url =

-

[16]

Nualart, David and Rascanu, Aurel , journal =

-

[18]

arXiv preprint arXiv:2504.15985 , year=

Modeling and Forecasting Realized Volatility with Multivariate Fractional Brownian Motion , author=. arXiv preprint arXiv:2504.15985 , year=

-

[19]

On the Curvature of the Smile in Stochastic Volatility Models , journal =

Al\`. On the Curvature of the Smile in Stochastic Volatility Models , journal =. 2017 , doi =

work page 2017

- [20]

-

[21]

The Review of Financial Studies , volume =

Implied Stochastic Volatility Models. The Review of Financial Studies , volume =. 2020 , issn =. doi:10.1093/rfs/hhaa041 , url =

-

[22]

Alós, Elisa and Le\'on, Jorge and Vives, Josep , year =. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility , volume =. Finance and Stochastics , doi =

-

[23]

SIAM Journal on Financial Mathematics , volume=

On smile properties of volatility derivatives: Understanding the VIX skew , author=. SIAM Journal on Financial Mathematics , volume=. 2022 , publisher=

work page 2022

-

[24]

Identification of the multivariate fractional

Amblard,. Identification of the multivariate fractional. IEEE Trans. Signal Process. , FJOURNAL =. 2011 , NUMBER =. doi:10.1109/TSP.2011.2162835 , URL =

- [25]

-

[26]

Special Functions , publisher=

Andrews,. Special Functions , publisher=. 1999 , collection=

work page 1999

-

[27]

An introduction to numerical analysis, 2nd ed , author=. 2008 , publisher=

work page 2008

-

[28]

Bally, Vlad and Caramellino, Lucia and Poly, Guillaume , TITLE =. Probab. Theory Related Fields , FJOURNAL =. 2019 , NUMBER =. doi:10.1007/s00440-018-0869-2 , URL =

-

[29]

Regularization lemmas and convergence in total variation , volume =

Bally, Vlad and Caramellino, Lucia and Poly, Guillaume , year =. Regularization lemmas and convergence in total variation , volume =. Electronic Journal of Probability , doi =

-

[30]

A regularity structure for rough volatility , journal =

Bayer, Christian and Friz,. A regularity structure for rough volatility , journal =. doi:https://doi.org/10.1111/mafi.12233 , url =. https://onlinelibrary.wiley.com/doi/pdf/10.1111/mafi.12233 , year =

-

[31]

Log-Modulated Rough Stochastic Volatility Models , journal =

Bayer, Christian and Harang,. Log-Modulated Rough Stochastic Volatility Models , journal =. 2021 , doi =

work page 2021

-

[32]

Finance and Stochastics , year=

Hybrid scheme for Brownian semistationary processes , author=. Finance and Stochastics , year=

-

[33]

Cammarota, Valentina , TITLE =. Trans. Amer. Math. Soc. , FJOURNAL =. 2019 , NUMBER =. doi:10.1090/tran/7779 , URL =

-

[34]

The Annals of Probability , number =

Cammarota, Valentina and Marinucci, Domenico , title =. The Annals of Probability , number =. 2018 , doi =

work page 2018

-

[35]

Random Eigenfunctions on Flat Tori: Uuniversality for the Number of Intersections

Chang,. Random Eigenfunctions on Flat Tori: Uuniversality for the Number of Intersections. International Mathematics Research Notices , volume =. 2018 , issn =. doi:10.1093/imrn/rny267 , url =

-

[36]

Adaptive global thresholding on the sphere , journal =

Claudio Durastanti , keywords =. Adaptive global thresholding on the sphere , journal =. 2016 , issn =. doi:https://doi.org/10.1016/j.jmva.2016.07.009 , url =

-

[37]

Forde, Martin and Fukasawa, Masaaki and Gerhold, Stefan and Smith, Benjamin , year =. The Riemann–Liouville field and its GMC as H → 0 , and skew flattening for the rough Bergomi model , volume =. Statistics & Probability Letters , doi =

-

[38]

Forde, Martin and Gerhold, Stefan and Smith, Benjamin , year =. Mathematical Finance , doi =

-

[39]

SIAM Journal on Financial Mathematics , volume =

Forde, Martin and Zhang, Hongzhong , title =. SIAM Journal on Financial Mathematics , volume =. 2017 , doi =

work page 2017

-

[40]

Quantitative Finance , volume =

Gatheral, Jim and Jaisson, Thibault and Rosenbaum, Mathieu , title =. Quantitative Finance , volume =. 2018 , publisher =. doi:10.1080/14697688.2017.1393551 , URL =

- [41]

-

[42]

doi:https://doi.org/10.1111/mafi.12173 , url =

The characteristic function of rough Heston models , journal =. doi:https://doi.org/10.1111/mafi.12173 , url =. https://onlinelibrary.wiley.com/doi/pdf/10.1111/mafi.12173 , year =

-

[43]

The Annals of Applied Probability , number =

Friz,. The Annals of Applied Probability , number =. 2021 , doi =

work page 2021

-

[44]

Friz,. Short-dated smile under rough volatility: asymptotics and numerics , journal =. 2022 , publisher =. doi:10.1080/14697688.2021.1999486 , URL =

-

[45]

The Step Stochastic Volatility Model (SSVM) , journal =

Friz, Peter and Pigato, Paolo and Seibel, Jonathan , year =. The Step Stochastic Volatility Model (SSVM) , journal =

-

[46]

Finance and Stochastics , year=

Asymptotic analysis for stochastic volatility\: martingale expansion , author=. Finance and Stochastics , year=

-

[47]

Quantitative Finance , volume =

Masaaki Fukasawa , title =. Quantitative Finance , volume =. 2017 , publisher =. doi:10.1080/14697688.2016.1197410 , URL =

-

[48]

Quantitative Finance , volume =

Masaaki Fukasawa , title =. Quantitative Finance , volume =. 2021 , publisher =. doi:10.1080/14697688.2020.1825781 , URL =

-

[49]

Finance and Stochastics , year=2014, volume=

Kun Gao and Roger Lee , title=. Finance and Stochastics , year=2014, volume=

work page 2014

-

[50]

Garnier, Josselin and S. 2017 , issue_date =. doi:10.1137/15M1036749 , journal =

-

[51]

Josselin Garnier and Knut Sølna , title=. Annals of Finance , year=. doi:10.1007/s10436-018-0325-4 , url=

-

[52]

Mathematical Finance , volume =

Garnier, Josselin and Sølna, Knut , title =. Mathematical Finance , volume =. doi:https://doi.org/10.1111/mafi.12186 , url =. https://onlinelibrary.wiley.com/doi/pdf/10.1111/mafi.12186 , year =

- [53]

-

[54]

Optimal Hedging Under Fast-Varying Stochastic Volatility , journal =

Garnier, Josselin and S. Optimal Hedging Under Fast-Varying Stochastic Volatility , journal =. 2020 , doi =

work page 2020

- [55]

-

[56]

Covariance function of vector self-similar processes , journal =

Fr\'ed\'eric Lavancier and Anne Philippe and Donatas Surgailis , volume =. Covariance function of vector self-similar processes , journal =. 2009 , issn =. doi:https://doi.org/10.1016/j.spl.2009.08.015 , url =

-

[57]

Quantitative Finance , volume=

On VIX futures in the rough Bergomi model , author=. Quantitative Finance , volume=. 2018 , publisher=

work page 2018

-

[58]

Gaussian Hilbert Spaces , publisher=

Janson, Svante , year=. Gaussian Hilbert Spaces , publisher=

-

[59]

A Central Limit Theorem and Higher Order Results for the Angular Bispectrum , volume =

Marinucci, Domenico , year =. A Central Limit Theorem and Higher Order Results for the Angular Bispectrum , volume =. Probability Theory and Related Fields , doi =

-

[60]

Marinucci, Domenico and Peccati, Giovanni , year=. Random Fields on the Sphere: Representation, Limit Theorems and Cosmological Applications , publisher=

-

[61]

Geometric and Functional Analysis , year=

Non-Universality of Nodal Length Distribution for Arithmetic Random Waves , author=. Geometric and Functional Analysis , year=

-

[62]

Marinucci, Domenico and Rossi, Maurizia , TITLE =. J. Funct. Anal. , FJOURNAL =. 2015 , NUMBER =. doi:10.1016/j.jfa.2015.02.004 , URL =

-

[63]

Marinucci, Domenico and Rossi, Maurizia and Wigman, Igor , TITLE =. Ann. Inst. Henri Poincar\'. 2020 , NUMBER =. doi:10.1214/19-AIHP964 , URL =

-

[64]

Domenico Marinucci and Igor Wigman , title =. 2011 , publisher =. doi:10.1088/1751-8113/44/35/355206 , url =

-

[65]

Marinucci, Domenico and Wigman, Igor , TITLE =. Comm. Math. Phys. , FJOURNAL =. 2014 , NUMBER =. doi:10.1007/s00220-014-1939-7 , URL =

-

[66]

Normal Approximations with Malliavin Calculus: From Stein's Method to Universality , isbn =

Nourdin, Ivan and Peccati, Giovanni , year =. Normal Approximations with Malliavin Calculus: From Stein's Method to Universality , isbn =

-

[67]

Nourdin, Ivan and Peccati, Giovanni and Reinert, Gesine , TITLE =. J. Funct. Anal. , FJOURNAL =. 2009 , NUMBER =. doi:10.1016/j.jfa.2008.12.017 , URL =

-

[68]

The Malliavin calculus and related topics

Nualart, David , year =. The Malliavin calculus and related topics. Second edition , journal=

-

[69]

Pipiras, Vladas and Taqqu, Murad S. , year=. Long-Range Dependence and Self-Similarity , publisher=

-

[70]

Pipiras, Vladas and Taqqu, Murad S. , TITLE =. Probab. Theory Related Fields , FJOURNAL =. 2000 , NUMBER =. doi:10.1007/s440-000-8016-7 , URL =

-

[71]

Rossi, Maurizia , TITLE =. J. Theoret. Probab. , FJOURNAL =. 2019 , NUMBER =. doi:10.1007/s10959-018-0849-6 , URL =

- [72]

-

[73]

Todino, Anna Paola , TITLE =. J. Math. Phys. , FJOURNAL =. 2019 , NUMBER =. doi:10.1063/1.5048976 , URL =

-

[74]

Wang, Xiaohu and Xiao, Weilin and Yu, Jun , TITLE =. J. Econometrics , FJOURNAL =. 2023 , NUMBER =. doi:10.1016/j.jeconom.2021.08.001 , URL =

-

[75]

Random Graphs and Complex Networks , publisher=

Hofstad, Remco van der , year=. Random Graphs and Complex Networks , publisher=

-

[76]

Vidotto, Anna , TITLE =. J. Theoret. Probab. , FJOURNAL =. 2020 , NUMBER =. doi:10.1007/s10959-019-00883-3 , URL =

-

[77]

Representation of Lie Groups and Special Functions: Volume 2: Class I Representations, Special Functions, and Integral Transforms , author=. 1992 , publisher=

work page 1992

-

[78]

arXiv preprint arXiv:2105.05356 , year=

Multilevel Monte Carlo simulation for VIX options in the rough Bergomi model , author=. arXiv preprint arXiv:2105.05356 , year=

-

[79]

Quantitative Finance , volume=

Weak approximations and VIX option price expansions in forward variance curve models , author=. Quantitative Finance , volume=. 2023 , publisher=

work page 2023

-

[80]

Local volatility under rough volatility , JOURNAL =

Bourgey, Florian and. Local volatility under rough volatility , JOURNAL =. 2023 , NUMBER =. doi:10.1111/mafi.12392 , URL =

-

[81]

Catalini, Giulia and Pacchiarotti, Barbara , TITLE =. Stoch. Anal. Appl. , FJOURNAL =. 2023 , NUMBER =. doi:10.1080/07362994.2022.2120012 , URL =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.