Characterizing Path-Independent Fees: A Route to Zero Impermanent Loss in CPMMs

Pith reviewed 2026-05-07 05:29 UTC · model grok-4.3

The pith

Fees that depend only on the pool invariant k=xy make trades in constant-product market makers path-independent and can eliminate impermanent loss for specific starting states.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

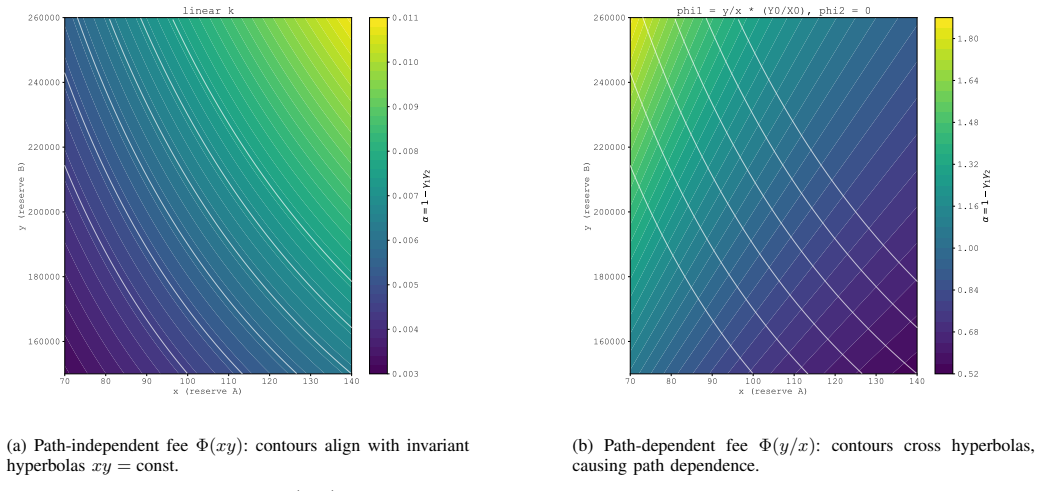

The paper establishes that path independence in constant-product market makers is achieved precisely when the combined fee factor depends only on the current pool invariant k = x y. For fees satisfying this condition, the pool state evolves according to a system of ordinary differential equations that admits a closed-form integral solution for the exchange. A parametric family of such fee functions can be chosen to produce zero impermanent loss relative to a given initial pool composition, yet it is proven that no single fee function in the class can achieve zero impermanent loss simultaneously for every possible initial state.

What carries the argument

The combined fee factor that is required to depend only on the current value of the pool invariant k=xy; this dependence ensures that the net effect of any sequence of trades is the same regardless of order or splitting.

Load-bearing premise

Fees are automatically reinvested into the pool and the continuous dynamics of the reserves can be modeled by ordinary differential equations whose right-hand sides depend on the reserves only through the invariant k.

What would settle it

Running the same net trade once as a single large swap and once as a sequence of small swaps under a fee whose factor depends only on k, then checking whether the final reserve ratios are identical; or starting the pool at the specified initial state, applying the parametric fee, and verifying that the liquidity provider's value after price change equals the no-fee hold value.

Figures

read the original abstract

Constant Product Market Makers use fees that are typically fixed proportions of trade size. When these fees are automatically reinvested into the pool, as in Uniswap~V2 and some designs of Uniswap V4, the final state after a trade can depend on how the trade is split into smaller transactions. This path dependence complicates the risk assessment for liquidity providers and affects composability guarantees. We characterize the functional class of fee structures that ensure path independence: the combined fee factor must depend only on the current pool invariant k=xy. For this class, we derive a system of ordinary differential equations governing pool dynamics and obtain a closed-form integral exchange formula. Within this class, we construct a parametric family of fee functions that achieve zero Impermanent Loss for a given initial pool state, and prove that no universal fee function can eliminate Impermanent Loss for all initial states simultaneously. We analyze implications for arbitrage windows and slippage, and validate our theory through controlled simulations. Our framework provides protocol designers with a principled approach to fee optimization that aligns liquidity provider and trader incentives while preserving composability.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript characterizes the functional class of fee structures in constant-product market makers (CPMMs) that ensure path-independent pool states when fees are automatically reinvested: the combined fee factor must depend only on the current invariant k = x y. From this class the authors derive a system of ODEs governing pool dynamics, obtain a closed-form integral exchange formula, construct a parametric family of fee functions that achieve zero impermanent loss for any fixed initial pool state, and prove that no single fee function can eliminate impermanent loss for all initial states simultaneously. The work also analyzes implications for arbitrage windows and slippage and validates the results via controlled simulations.

Significance. If the central results hold, the paper supplies a mathematically principled route to fee design that can remove path dependence and impermanent loss for chosen initial states while preserving composability guarantees. The impossibility result for a universal zero-IL fee is a clean negative contribution, and the closed-form exchange formula could be useful for protocol analysis. The framework directly addresses incentive alignment between liquidity providers and traders in designs such as Uniswap V2/V4. The continuous approximation, however, limits immediate applicability to production discrete-trade implementations.

major comments (2)

- [Characterization of path-independent fees and ODE derivation] The path-independence characterization (abstract and the derivation that dk is a function of k alone) is obtained in the continuous infinitesimal-trade limit. In actual CPMM implementations trades are atomic and finite; applying a k-dependent factor at the start of each discrete trade produces a jump in k, so the product of factors after a split-trade sequence generally differs from the single-trade case. The manuscript does not prove or demonstrate exact discrete path-independence for the constructed family, which is load-bearing for the claim that these fees “ensure path independence” in CPMMs.

- [Zero-IL parametric family and impossibility result] The parametric family that achieves zero IL for a given initial state and the impossibility proof for a universal fee both rely on the integrated ODE solution. Because the zero-IL guarantee is shown only inside the continuous approximation, it is unclear whether the family still yields exactly zero IL (or even path independence) under discrete finite trades. The simulations mentioned in the abstract are not described in sufficient detail to confirm exact invariance for split versus single trades.

minor comments (2)

- [Simulation validation] The description of the controlled simulations lacks concrete parameters (number of trades, discretization granularity, exact metric used to test path independence). Adding these details would strengthen the validation section.

- [Notation and definitions] Notation for the “combined fee factor” should be introduced with an explicit equation number early in the manuscript so that later references (e.g., to the ODE system) are unambiguous.

Simulated Author's Rebuttal

We are grateful to the referee for the thorough review and valuable feedback on our manuscript. The comments highlight important considerations regarding the continuous approximation used in our analysis. We address each major comment below and outline the revisions we plan to make to strengthen the paper.

read point-by-point responses

-

Referee: The path-independence characterization (abstract and the derivation that dk is a function of k alone) is obtained in the continuous infinitesimal-trade limit. In actual CPMM implementations trades are atomic and finite; applying a k-dependent factor at the start of each discrete trade produces a jump in k, so the product of factors after a split-trade sequence generally differs from the single-trade case. The manuscript does not prove or demonstrate exact discrete path-independence for the constructed family, which is load-bearing for the claim that these fees “ensure path independence” in CPMMs.

Authors: We appreciate the referee's observation that our path-independence result is derived under the continuous approximation. Indeed, the characterization that the combined fee factor depends only on k, leading to dk being a function of k alone, is obtained by considering infinitesimal trades. In discrete atomic trades, as noted, the state jumps, and exact path independence may not hold for finite trade sizes. However, the continuous model provides a principled foundation for fee design, and for small trades relative to pool size, the discrete behavior approximates the continuous case closely. We will revise the manuscript to explicitly state the scope of the path-independence guarantee as holding in the continuous limit. Additionally, we will add a new subsection discussing the discrete implementation, including an analysis of the error introduced by finite trades and numerical examples showing that for the proposed family, the path dependence is minimized. This addresses the load-bearing claim by qualifying it appropriately. revision: yes

-

Referee: The parametric family that achieves zero IL for a given initial state and the impossibility proof for a universal fee both rely on the integrated ODE solution. Because the zero-IL guarantee is shown only inside the continuous approximation, it is unclear whether the family still yields exactly zero IL (or even path independence) under discrete finite trades. The simulations mentioned in the abstract are not described in sufficient detail to confirm exact invariance for split versus single trades.

Authors: We agree that both the parametric family for zero IL and the impossibility result are established within the continuous ODE framework. The zero-IL property is exact in the continuous dynamics for the chosen initial state, and the impossibility shows no single fee eliminates IL universally in that model. For discrete trades, the IL will be approximately zero when trades are not too large. Regarding the simulations, we acknowledge that the current description in the manuscript is brief. We will expand the simulation section with full details on the setup (e.g., pool sizes, trade sequences, fee parameters), the metrics used (IL calculation, path comparison), and results including tables or figures comparing single trades to split trades for the parametric family, confirming near-zero IL and path independence in the discrete approximation. We will also make the simulation code available as supplementary material. revision: yes

Circularity Check

Path-independence characterization and zero-IL family derived from continuous ODE model without circular reduction

full rationale

The paper posits that path independence holds precisely when the combined fee factor depends only on the current invariant k=xy, then derives the governing ODE system and closed-form integral exchange formula directly from this autonomous dependence. Within the same class it constructs a parametric family solving for zero impermanent loss at a fixed initial state and proves no single function works for all initials. This is a standard modeling choice rather than a circular reduction: the path-independence result follows immediately from the fact that dk is a function of k alone, and the zero-IL family is obtained by solving the resulting integral equation for the target property. No parameters are fitted to data and then relabeled as predictions, no load-bearing self-citations appear, and no ansatz is imported via prior work. The entire derivation remains self-contained inside the stated continuous approximation and reinvestment assumption, warranting only a minimal circularity score.

Axiom & Free-Parameter Ledger

free parameters (1)

- parameters of the parametric fee family

axioms (2)

- domain assumption Fee structures can be represented such that the combined fee factor depends only on the current pool invariant k=xy

- domain assumption Pool dynamics under reinvested fees can be modeled by a system of ordinary differential equations

Reference graph

Works this paper leans on

-

[1]

Financially-stable automated market making for decentralized fixed-rate lending and trading,

T. Tran, D. A. Tran, and K. Truong, “Financially-stable automated market making for decentralized fixed-rate lending and trading,” in 2024 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2024

work page 2024

-

[2]

Dynamic fee for reducing impermanent loss in decentralized exchanges,

I. Lebedeva, D. Umnov, Y . Yanovich, I. Melnikov, and G. Ovchin- nikov, “Dynamic fee for reducing impermanent loss in decentralized exchanges,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[3]

I. Melnikov, I. Lebedeva, D. Bogutsky, and Y . Yanovich, “Smarter risks for smart contracts: Machine learning approach to credit scoring and risk assessment in defi,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[4]

Crosslink: A decentralized framework for secure cross-chain smart contract ex- ecution,

T. Hossain, F. H. Bappy, T. Shaila Zaman, and T. Islam, “Crosslink: A decentralized framework for secure cross-chain smart contract ex- ecution,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[5]

R. Vlasov, V . Gorgadze, and A. Barger, “The Impact of the Exchange Fees on Impermanent Loss of Liquidity Providers for Conservative Automated Market Makers,”The Journal of The British Blockchain Association, may 27 2025

work page 2025

-

[6]

S. C. Zeller, P.-N. K. Kandora, D. Kirste, N. Kannengießer, S. Reben- nack, and A. Sunyaev, “Automated market makers: A stochastic opti- mization approach for profitable liquidity concentration,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[7]

Proactive market mak- ing and liquidity analysis for everlasting options in defi ecosystems,

H. Mohanty, G. Zaarour, and B. Krishnamachari, “Proactive market mak- ing and liquidity analysis for everlasting options in defi ecosystems,” in 2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[8]

D. A. Zetzsche, D. W. Arner, and R. P. Buckley, “Decentralized finance,” Journal of Financial Regulation, vol. 6, no. 2, pp. 172–203, 2020

work page 2020

-

[9]

H. Adams, N. Zinsmeister, and D. Robinson, “Uniswap v2 core,” 2020, whitepaper

work page 2020

-

[10]

On the quality of cryptocurrency markets: Centralized versus decentralized exchanges,

A. Barbon and A. Ranaldo, “On the quality of cryptocurrency markets: Centralized versus decentralized exchanges,”SSRN Electronic Journal, 2021

work page 2021

-

[11]

SoK : Decentralized exchanges ( DEX ) with automated market maker ( AMM ) protocols

J. Xu, K. Paruch, S. Cousaert, and Y . Feng, “Sok: Decentralized exchanges (dex) with automated market maker (amm) protocols,”ACM Computing Surveys, vol. 55, no. 11, p. 1–50, Feb. 2023. [Online]. Available: http://dx.doi.org/10.1145/3570639

-

[12]

Uniswap: Impermanent loss and risk profile of a liquidity provider,

A. A. Aigner and G. Dhaliwal, “Uniswap: Impermanent loss and risk profile of a liquidity provider,” 6 2021. [Online]. Available: http://arxiv.org/abs/2106.14404

-

[13]

Impermanent loss in uniswap v3,

S. Loesch, N. Hindman, M. B. Richardson, and N. Welch, “Impermanent loss in uniswap v3,”arXiv, 11 2021

work page 2021

-

[14]

Liquidity providers greeks and imperma- nent gain,

N. Bardoscia and A. Nodari, “Liquidity providers greeks and imperma- nent gain,”arXiv, 3 2023

work page 2023

-

[15]

Generalizing impermanent loss on decentralized exchanges with constant function market makers,

R. Tangri, P. Yatsyshin, E. A. Duijnstee, and D. Mandic, “Generalizing impermanent loss on decentralized exchanges with constant function market makers,”arXiv, 1 2023

work page 2023

-

[16]

Impermanent loss and gain of automated market maker smart contracts,

H. J. Kim, S. Choi, Y . T. Yoon, and S. Yoo, “Impermanent loss and gain of automated market maker smart contracts,”TechRxiv, 2022

work page 2022

-

[17]

Impermanent loss and slippage in automated market mak- ers (amms) with constant-product formula,

M. Labadie, “Impermanent loss and slippage in automated market mak- ers (amms) with constant-product formula,”SSRN Electronic Journal, 2022

work page 2022

-

[18]

A non-custodial portfolio manager, liquidity provider, and price sensor,

F. Martinelli and N. Mushegian, “A non-custodial portfolio manager, liquidity provider, and price sensor,” Balancer Labs, Tech. Rep., 2019. [Online]. Available: https://docs.balancer.fi/whitepaper.pdf

work page 2019

-

[19]

Amm- based dex on the xrp ledger,

W. H. Cruz, F. Dahi, Y . Feng, J. Xu, A. Malhotra, and P. Tasca, “Amm- based dex on the xrp ledger,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[20]

A comparison of impermant loss for various cfmms,

H. J. Kim, G. M. Lee, J. Lee, S. Kang, S. W. Chae, and J.-S. Park, “A comparison of impermant loss for various cfmms,” in2024 IEEE International Conference on Blockchain (Blockchain). IEEE, 8 2024, pp. 542–548

work page 2024

-

[21]

´Alvaro Cartea, F. Drissi, and M. Monga, “Predictable losses of liquidity provision in constant function markets and concentrated liquidity mar- kets,”Applied Mathematical Finance, vol. 30, 2023

work page 2023

-

[22]

Risks and returns of uniswap v3 liquidity providers,

L. Heimbach, E. Schertenleib, and R. Wattenhofer, “Risks and returns of uniswap v3 liquidity providers,” 5 2022. [Online]. Available: http://arxiv.org/abs/2205.08904

-

[23]

D. Mancino, A. Leporati, M. Viviani, and G. Denaro, “Decentraliza- tion or favoritism? an analysis of ethereum transactions and maximal extractable value strategies,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[24]

N. Diallo, L. Xu, D. Alsagheer, Y . Lu, and L. Shi, “Optimized consensus with dagwise: A gnn-enhanced approach for scalable and fault-tolerant dag-based bft,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), 2025

work page 2025

-

[25]

Optimal dynamic fees in automated market makers,

L. Baggiani, M. Herdegen, and L. S ´anchez-Betancourt, “Optimal dynamic fees in automated market makers,” 2025. [Online]. Available: https://arxiv.org/abs/2506.02869

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.