Bayesian Extreme Value Theory with Hawkes-AR-Gumbel Dependence for Extreme CVaR Estimation in Operational Risk

Pith reviewed 2026-05-25 02:46 UTC · model grok-4.3

The pith

A Hawkes-AR-Gumbel dependence model inside Bayesian EVT recovers the true structure of operational losses and produces accurate extreme CVaR estimates where independent assumptions underestimate by 40 percent.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

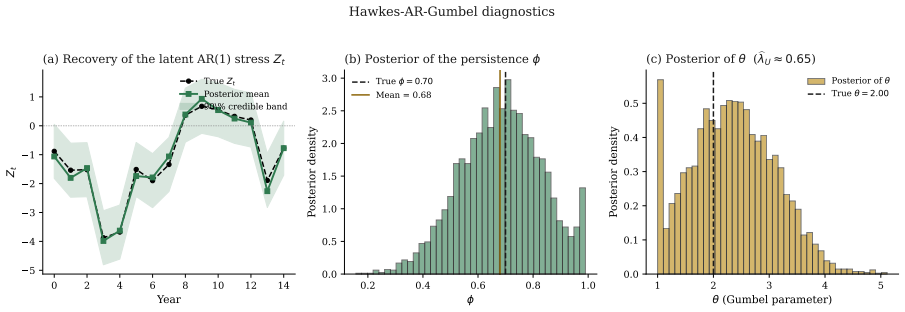

The Hawkes-AR-Gumbel model, consisting of an autoregressive latent stress process, Hawkes self-excitation for frequency, and Gumbel copula for upper-tail dependence, when embedded in a Bayesian EVT framework with HMC inference, recovers the true dependence structure in simulated operational risk data and produces correct CVaR estimates at levels up to 99.995 percent, whereas the independent model underestimates by about 40 percent.

What carries the argument

The Hawkes-AR-Gumbel dependence architecture that combines an autoregressive latent stress process, Hawkes self-excitation for frequency clustering, and an asymmetric Gumbel copula linking frequency and severity innovations.

If this is right

- The independent LDA underestimates CVaR at 99.995 percent by approximately 40 percent on data containing the modeled dependence.

- A shared latent factor model with symmetric dependence fails to capture temporal persistence, event clustering, and upper-tail asymmetry.

- Full posterior distributions obtained via Hamiltonian Monte Carlo propagate parameter uncertainty into the tail estimates.

- Posterior predictive Monte Carlo simulation delivers CVaR at arbitrary confidence levels beyond the 99.9 percent regulatory threshold.

Where Pith is reading between the lines

- Testing the same models on real operational-loss databases would reveal whether the 40 percent gap persists outside the simulated setting.

- Persistent stress regimes implied by the autoregressive component suggest that capital buffers should remain elevated for multiple periods after a large loss event.

- The framework can be extended to other copula families or to multivariate severity distributions without changing the inference machinery.

Load-bearing premise

The comparison data were generated under exactly the same dependence mechanisms that the proposed model assumes.

What would settle it

Whether the Hawkes-AR-Gumbel model produces materially higher CVaR estimates than the independent LDA at the 99.995 percent level when both are fitted to actual bank operational-loss records whose dependence structure is unknown.

Figures

read the original abstract

Operational risk capital estimation under Basel II/III requires quantifying aggregate losses at extreme confidence levels of 99.9% and beyond, yet the standard Loss Distribution Approach (LDA) assumes independence between loss frequency and severity, an assumption frequently violated during stress episodes. Furthermore, MLE of tail parameters ignores parameter uncertainty, leading to overconfident risk estimates at extreme quantiles. We propose a Bayesian framework that combines Extreme Value Theory with a dynamic dependence architecture, the Hawkes-AR-Gumbel model, for operational risk Conditional Value-at-Risk (CVaR) estimation at confidence levels up to 99.995%. The model integrates three mechanisms that capture empirically documented features of operational losses: an autoregressive latent stress process that captures persistence of crisis regimes, a Hawkes selfexcitation component for frequency that generates event clustering and overdispersion, and a Gumbel copula for upper-tail dependence that links frequency and severity innovations through an asymmetric copula concentrating dependence in the extreme tail. Inference is performed via Hamiltonian Monte Carlo using PyMC, yielding full posterior distributions for all parameters, and CVaR at arbitrary confidence levels is estimated through posterior predictive Monte Carlo simulation. We compare three models on simulated operational risk data: the independent model (standard LDA), a shared latent factor model with symmetric dependence, and the proposed Hawkes-AR-Gumbel model. The independent model underestimates CVaR at 99.995% by approximately 40%, while the shared factor model fails to capture temporal persistence, event clustering, and upper-tail asymmetry. The HawkesAR-Gumbel model recovers the true dependence structure and correctly estimates CVaR at extreme levels.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a Bayesian framework combining Extreme Value Theory with a Hawkes-AR-Gumbel dependence model (autoregressive latent stress process, Hawkes self-excitation for frequency, and Gumbel copula for upper-tail dependence between frequency and severity) to estimate operational risk CVaR at extreme levels up to 99.995%. Inference uses Hamiltonian Monte Carlo in PyMC for full posteriors, with CVaR obtained via posterior predictive simulation. On simulated data, the authors claim the Hawkes-AR-Gumbel model recovers the true dependence structure and yields accurate extreme CVaR, while the independent LDA model underestimates CVaR at 99.995% by approximately 40% and a shared latent factor model fails to capture persistence, clustering, and asymmetry.

Significance. If the superiority holds under misspecification or on real loss data, the approach would meaningfully advance operational risk modeling by addressing the independence assumption in standard LDA and incorporating parameter uncertainty via full Bayesian inference. The posterior predictive Monte Carlo for CVaR at arbitrary levels is a methodological strength for regulatory applications under Basel frameworks.

major comments (2)

- [Simulation study (abstract and methods)] The simulation study (described in the abstract) generates data exclusively from the Hawkes-AR-Gumbel process itself. This renders the reported recovery of the 'true dependence structure' and the 40% CVaR underestimation by the independent model tautological by construction, rather than a test of the model's ability to handle unknown dependence. The central claim of superiority therefore requires additional experiments on data from qualitatively different DGPs (e.g., Clayton copula, non-Hawkes clustering, or Gaussian copula) or real operational loss series.

- [Inference and results sections] No posterior diagnostics, parameter recovery metrics (bias, coverage), or convergence checks for the HMC sampler are referenced in support of the claim that the model 'recovers the true dependence.' Without these, the numerical performance claims (including the 40% gap) cannot be evaluated for reliability.

minor comments (1)

- [Abstract] The abstract would benefit from a brief statement of the simulation design parameters (e.g., true values of Hawkes intensity, AR coefficients, Gumbel parameter) to allow readers to assess the scope of the recovery claim.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify the scope and robustness of our simulation study and inference procedures. We address each major comment below.

read point-by-point responses

-

Referee: The simulation study (described in the abstract) generates data exclusively from the Hawkes-AR-Gumbel process itself. This renders the reported recovery of the 'true dependence structure' and the 40% CVaR underestimation by the independent model tautological by construction, rather than a test of the model's ability to handle unknown dependence. The central claim of superiority therefore requires additional experiments on data from qualitatively different DGPs (e.g., Clayton copula, non-Hawkes clustering, or Gaussian copula) or real operational loss series.

Authors: We agree that data generated from the Hawkes-AR-Gumbel process primarily validates parameter recovery and quantifies the bias from the independence assumption when that assumption is violated. To address generalizability under misspecification, we will add new simulation experiments in the revised manuscript using qualitatively different DGPs, specifically a Clayton copula (lower-tail dependence) and a non-Hawkes autoregressive clustering process, and report CVaR performance of all three models on these data. revision: yes

-

Referee: No posterior diagnostics, parameter recovery metrics (bias, coverage), or convergence checks for the HMC sampler are referenced in support of the claim that the model 'recovers the true dependence.' Without these, the numerical performance claims (including the 40% gap) cannot be evaluated for reliability.

Authors: We acknowledge that explicit reporting of sampler diagnostics and recovery metrics is necessary for evaluating the reliability of the posterior estimates. In the revised manuscript we will add HMC convergence diagnostics (trace plots, R-hat values, effective sample sizes) together with parameter recovery metrics (bias, RMSE, and 95% coverage rates) computed from the simulation study. revision: yes

Circularity Check

All reported performance gains and structure recovery are shown only on data simulated from the exact Hawkes-AR-Gumbel process itself

specific steps

-

fitted input called prediction

[Abstract]

"We compare three models on simulated operational risk data: the independent model (standard LDA), a shared latent factor model with symmetric dependence, and the proposed Hawkes-AR-Gumbel model. The independent model underestimates CVaR at 99.995% by approximately 40%, while the shared factor model fails to capture temporal persistence, event clustering, and upper-tail asymmetry. The HawkesAR-Gumbel model recovers the true dependence structure and correctly estimates CVaR at extreme levels."

The simulation generates loss sequences under the exact Hawkes-AR-Gumbel dependence the model assumes; fitting the model to this data and reporting that it 'recovers the true dependence structure' and correctly estimates CVaR is tautological. The 40% gap versus the independent model is expected by construction and does not constitute an out-of-sample or misspecification test.

full rationale

The paper's central claim—that the Hawkes-AR-Gumbel model recovers the true dependence structure and yields accurate extreme CVaR while the independent LDA underestimates by ~40%—is demonstrated exclusively via comparisons on synthetic data generated from the model's own mechanisms (autoregressive latent stress, Hawkes self-excitation, Gumbel copula). This makes the reported recovery and superiority statistically forced by construction rather than an independent test. No results on real operational loss data or qualitatively different dependence structures are provided in the abstract or described simulation setup.

Axiom & Free-Parameter Ledger

free parameters (4)

- Hawkes intensity parameters

- AR latent stress coefficients

- Gumbel copula parameter

- EVT shape and scale parameters

axioms (2)

- domain assumption Loss frequency and severity are linked only through the specified copula and latent process; no other channels exist.

- domain assumption Posterior predictive Monte Carlo simulation yields unbiased CVaR estimates at 99.995%.

Reference graph

Works this paper leans on

-

[1]

Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical Finance, 9 0 (3): 0 203--228, 1999

work page 1999

-

[2]

Emmanuel Bacry, Iacopo Mastromatteo, and Jean-Fran c ois Muzy. H awkes processes in finance. Market Microstructure and Liquidity, 1 0 (1): 0 1550005, 2015

work page 2015

-

[3]

August A. Balkema and Laurens de Haan . Residual life time at great age. The Annals of Probability, 2 0 (5): 0 792--804, 1974

work page 1974

-

[4]

Basel Committee on Banking Supervision . International convergence of capital measurement and capital standards: A revised framework (comprehensive version). Technical report, Bank for International Settlements, 2006

work page 2006

-

[5]

Smooth extremal models in finance and insurance

Val\'erie Chavez-Demoulin and Paul Embrechts. Smooth extremal models in finance and insurance. Journal of Risk and Insurance, 71 0 (2): 0 183--199, 2004

work page 2004

-

[6]

Stuart G. Coles and Elwyn A. Powell. B ayesian methods in extreme value modelling: A review and new developments. International Statistical Review, 64 0 (1): 0 119--136, 1996

work page 1996

-

[7]

Cope, Giulio Mignola, Gianluca Antonini, and Roberto Ugoccioni

Eric W. Cope, Giulio Mignola, Gianluca Antonini, and Roberto Ugoccioni. Challenges and pitfalls in measuring operational risk from loss data. The Journal of Operational Risk, 4 0 (4): 0 3--27, 2009

work page 2009

-

[8]

Modelling Extremal Events for Insurance and Finance

Paul Embrechts, Claudia Kl\"uppelberg, and Thomas Mikosch. Modelling Extremal Events for Insurance and Finance. Springer, 1997

work page 1997

-

[9]

Paul Embrechts, Alexander J. McNeil, and Daniel Straumann. Correlation and dependence in risk management: Properties and pitfalls. In Michael A. H. Dempster, editor, Risk Management: Value at Risk and Beyond, pages 176--223. Cambridge University Press, 2002

work page 2002

-

[10]

Quantifying regulatory capital for operational risk

Paul Embrechts, Hansj\"org Furrer, and Roger Kaufmann. Quantifying regulatory capital for operational risk. Derivatives Use, Trading and Regulation, 9 0 (3): 0 217--233, 2003

work page 2003

-

[11]

Loss distribution approach for operational risk

Antoine Frachot, Pierre Georges, and Thierry Roncalli. Loss distribution approach for operational risk. Working paper, Groupe de Recherche Op\'erationnelle, Cr\'edit Lyonnais, 2001

work page 2001

-

[12]

Modelling operational risk using extreme value theory and skew t -copulas

Betty Johanna Garz\'on-Rozo, Jonathan Crook, and Fernando Moreira. Modelling operational risk using extreme value theory and skew t -copulas. Working paper, University of Edinburgh Business School, 2023

work page 2023

-

[13]

Alan G. Hawkes. Spectra of some self-exciting and mutually exciting point processes. Biometrika, 58 0 (1): 0 83--90, 1971

work page 1971

-

[14]

Matthew D. Hoffman and Andrew Gelman. The N o- U - T urn S ampler: Adaptively setting path lengths in H amiltonian M onte C arlo. Journal of Machine Learning Research, 15 0 (47): 0 1593--1623, 2014

work page 2014

-

[15]

Dependence Modeling with Copulas

Harry Joe. Dependence Modeling with Copulas. Chapman and Hall/CRC, 2014

work page 2014

-

[16]

Alexander J. McNeil. Extreme value theory for risk managers. In Internal Modelling and CAD II, pages 93--113. Risk Books, 1999

work page 1999

-

[17]

McNeil, R\"udiger Frey, and Paul Embrechts

Alexander J. McNeil, R\"udiger Frey, and Paul Embrechts. Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press, revised edition, 2015

work page 2015

-

[18]

Marco Moscadelli. The modelling of operational risk: Experience with the analysis of the data collected by the B asel C ommittee. Temi di Discussione 517, Bank of Italy, 2004

work page 2004

-

[19]

Radford M. Neal. MCMC using H amiltonian dynamics. Handbook of Markov Chain Monte Carlo, pages 113--162, 2011

work page 2011

-

[20]

Roger B. Nelsen. An Introduction to Copulas. Springer, 2nd edition, 2006

work page 2006

-

[21]

On L ewis' simulation method for point processes

Yosihiko Ogata. On L ewis' simulation method for point processes. IEEE Transactions on Information Theory, 27 0 (1): 0 23--31, 1981

work page 1981

-

[22]

Omiros Papaspiliopoulos, Gareth O. Roberts, and Martin Sk\"old. A general framework for the parametrization of hierarchical models. Statistical Science, 22 0 (1): 0 59--73, 2007

work page 2007

-

[23]

Gareth W. Peters and Scott A. Sisson. B ayesian inference, M onte C arlo sampling and operational risk. Journal of Operational Risk, 1 0 (3): 0 27--50, 2006

work page 2006

-

[24]

Statistical inference using extreme order statistics

James Pickands III. Statistical inference using extreme order statistics. The Annals of Statistics, 3 0 (1): 0 119--131, 1975

work page 1975

-

[25]

Tyrrell Rockafellar and Stanislav Uryasev

R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 26 0 (7): 0 1443--1471, 2002

work page 2002

-

[26]

Wiecki, and Christopher Fonnesbeck

John Salvatier, Thomas V. Wiecki, and Christopher Fonnesbeck. Probabilistic programming in P ython using P y MC 3. PeerJ Computer Science, 2: 0 e55, 2016

work page 2016

-

[27]

Fonctions de r\'epartition \`a n dimensions et leurs marges

Abe Sklar. Fonctions de r\'epartition \`a n dimensions et leurs marges. Publications de l'Institut Statistique de l'Universit\'e de Paris, 8: 0 229--231, 1959

work page 1959

-

[28]

Validating bayesian inference algorithms with simulation-based calibration, 2020

Sean Talts, Michael Betancourt, Daniel Simpson, Aki Vehtari, and Andrew Gelman. Validating B ayesian inference algorithms with simulation-based calibration. arXiv preprint arXiv:1804.06788, 2018

-

[29]

Practical B ayesian model evaluation using leave-one-out cross-validation and WAIC

Aki Vehtari, Andrew Gelman, and Jonah Gabry. Practical B ayesian model evaluation using leave-one-out cross-validation and WAIC . Statistics and Computing, 27 0 (5): 0 1413--1432, 2017

work page 2017

-

[30]

Aki Vehtari, Andrew Gelman, Daniel Simpson, Bob Carpenter, and Paul-Christian B\"urkner. Rank-normalization, folding, and localization: An improved R for assessing convergence of MCMC (with discussion). Bayesian Analysis, 16 0 (2): 0 667--718, 2021

work page 2021

-

[31]

Ruin probabilities for risk processes with non-stationary arrivals and subexponential claims

Lingjiong Zhu. Ruin probabilities for risk processes with non-stationary arrivals and subexponential claims. Insurance: Mathematics and Economics, 53 0 (3): 0 544--550, 2013

work page 2013

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.