Designing entry-monotone risk-sharing pools

Pith reviewed 2026-06-28 16:25 UTC · model grok-4.3

The pith

Convex risk measures turn institutional risk sharing into a totally balanced game with nonempty cores and entry-monotone allocation rules under verifiable conditions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Institutional risk sharing with cash-additive convex risk measures forms a totally balanced cooperative game, guaranteeing that every coalition possesses a nonempty core and therefore admits stable allocations; moreover, certain structural conditions on the underlying risks make the Arrow-Debreu pricing surplus rule or the proportional-cost surplus allocation rule population-monotonic.

What carries the argument

The transferable-utility cooperative game whose characteristic function assigns to each coalition the minimum cost of its aggregate risk under the agents' cash-additive risk measures.

If this is right

- Every coalition admits at least one stable allocation of the total risk cost.

- Stable risk pools exist for any finite collection of risk-averse agents.

- Under the stated structural conditions, the Arrow-Debreu pricing rule keeps every existing participant's net cost from rising when new members join.

- The proportional-cost surplus rule likewise satisfies entry monotonicity when the same structural conditions hold.

- These conditions appear naturally in pooled insurance and credit portfolios, giving designers explicit tests for monotonicity.

Where Pith is reading between the lines

- Pool designers could check convexity and the structural conditions on real portfolios before launching or expanding a pool.

- The framework suggests examining whether other common allocation rules, such as the nucleolus, also inherit entry monotonicity under the same conditions.

- If the structural conditions fail, the paper leaves open whether weaker monotonicity notions, short of full population monotonicity, might still hold.

Load-bearing premise

Institutional risk sharing with deterministic side payments can be represented as a transferable-utility game whose value for each coalition equals exactly the minimum cost of covering that coalition's risk.

What would settle it

A family of convex cash-additive risk measures on a finite set of agents together with a coalition whose core is empty would falsify the total-balancedness claim.

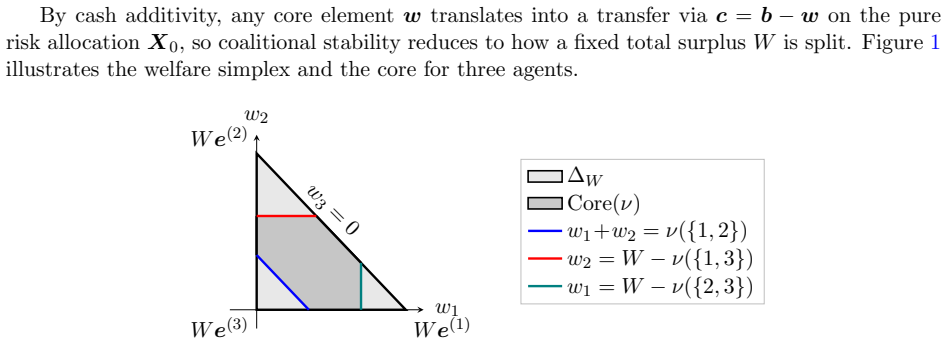

Figures

read the original abstract

While risk pooling lowers the total cost of risk, efficiency alone does not make a pool viable. Participants need terms that ensure their participation, that are immune to subgroups breaking away, and that allow new members to join. Under cash-additive risk measures, the minimum cost of a coalition's risk determines the value created by that coalition, and deterministic side payments redistribute that value among participants. Institutional risk sharing is thus a transferable-utility cooperative game. We prove that the game is totally balanced whenever the risk measures are convex (agents are risk averse), so every coalition has a nonempty core and stable allocations always exist. We then analyze entry monotonicity through Population-Monotonic Allocation Schemes (Sprumont, 1990), a strong requirement that is notoriously difficult to construct and has received limited attention in risk sharing. We find several structural conditions that ensure that either the Arrow--Debreu pricing surplus allocation rule or the proportional-cost surplus allocation rule satisfies this entry-monotonicity property, the latter being a novel cooperative notion we propose. These verifiable structural conditions naturally arise in pooled (re)insurance and credit portfolios, providing pool designers with a practical toolkit for building risk pools that remain stable and attractive as they expand.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models institutional risk sharing under cash-additive convex risk measures as a transferable-utility cooperative game whose value function is the minimum cost of the coalition's aggregate risk. It proves that the game is totally balanced, so every coalition has a nonempty core. It then derives structural conditions under which the Arrow-Debreu pricing surplus allocation rule and the proposed proportional-cost surplus allocation rule satisfy population monotonicity (entry monotonicity) via Population-Monotonic Allocation Schemes.

Significance. If the derivations hold, the work supplies a practical, verifiable toolkit for constructing stable and expandable risk pools that arise naturally in (re)insurance and credit portfolios. The total-balancedness result leverages the dual representation of convex risk measures in a direct and standard way, while the introduction of the proportional-cost surplus rule and its entry-monotonicity conditions constitute a useful addition to the risk-sharing literature.

minor comments (3)

- [Abstract] Abstract, paragraph 3: the phrase 'verifiable structural conditions' is used without even a one-sentence indication of their form; adding a brief qualifier would improve readability for practitioners.

- [Setup / Section 2] The definition and axiomatic motivation of the 'proportional-cost surplus allocation rule' (introduced as a novel notion) appear only after the main existence results; moving a concise formal definition to the setup section would aid comprehension.

- [Section 4] The reference to Sprumont (1990) for PMAS is appropriate, but the manuscript does not discuss how the risk-sharing application differs from the classic public-good or cost-sharing settings in which PMAS are typically studied.

Simulated Author's Rebuttal

We thank the referee for the positive summary, significance assessment, and recommendation of minor revision. No specific major comments appear in the report, so there are no individual points requiring point-by-point rebuttal or revision.

Circularity Check

No significant circularity identified

full rationale

The paper models institutional risk sharing as a TU cooperative game where v(S) is the inf-convolution of convex cash-additive risk measures. Total balancedness is shown via the dual representation v(S) = sup_Q [sum (E_Q[-X_i] - α_i(Q))], which expresses the game as the pointwise supremum of additive games; this is a direct mathematical consequence of convexity and does not reduce to any fitted input, self-definition, or self-citation chain. The entry-monotonicity analysis relies on verifiable structural conditions for allocation rules, which are independent of the balancedness proof. No load-bearing step collapses to its own inputs by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Risk measures are cash-additive

- domain assumption Risk measures are convex when agents are risk averse

invented entities (1)

-

proportional-cost surplus allocation rule

no independent evidence

Reference graph

Works this paper leans on

-

[1]

and Tan, Ken Seng and Zhuang, Sheng Chao , title =

Boonen, Tim J. and Tan, Ken Seng and Zhuang, Sheng Chao , title =. ASTIN Bulletin , volume =. 2016 , doi =

2016

-

[2]

1995 , publisher=

Microeconomic Theory , author=. 1995 , publisher=

1995

-

[3]

Operations Research , year =

Anily, Shoshana and Haviv, Moshe , title =. Operations Research , year =

-

[4]

Management Science , note =

On the Expansion of Risk Pooling , author =. Management Science , note =

-

[5]

Inf-Convolution and Optimal Allocations for Mixed-

Xia, Zichao and Zou, Zhenfeng and Hu, Taizhong , year = 2023, journal =. Inf-Convolution and Optimal Allocations for Mixed-

2023

-

[6]

Economic Theory , volume =

Optimal Contracting under Mean-Volatility Joint Ambiguity Uncertainties , author =. Economic Theory , volume =

-

[7]

Mathematical Programming , volume =

Quantile-Based Risk Sharing with Heterogeneous Beliefs , author =. Mathematical Programming , volume =

-

[8]

Solvency

Weber, Stefan , year = 2018, journal =. Solvency

2018

-

[9]

Operations Research , volume =

Quantile-Based Risk Sharing , author =. Operations Research , volume =

-

[10]

Mathematics and Financial Economics , volume =

Pareto Optimal Allocations and Optimal Risk Sharing for Quasiconvex Risk Measures , author =. Mathematics and Financial Economics , volume =

-

[11]

Comonotone

Ravanelli, Claudia and Svindland, Gregor , year = 2014, journal =. Comonotone

2014

-

[12]

European Actuarial Journal , volume =

Remarks on Quantiles and Distortion Risk Measures , author =. European Actuarial Journal , volume =

-

[13]

Journal of Economic Theory , volume =

Efficient Allocations under Ambiguity , author =. Journal of Economic Theory , volume =

-

[14]

Mathematical Finance , volume =

Optimal Risk Sharing for Law Invariant Monetary Utility Functions , author =. Mathematical Finance , volume =

-

[15]

Finance and Stochastics , volume =

Optimal Capital and Risk Allocations for Law- and Cash-Invariant Convex Functions , author =. Finance and Stochastics , volume =

-

[16]

Finance and Stochastics , volume =

Optimal Risk Sharing with Non-Monotone Monetary Functionals , author =. Finance and Stochastics , volume =

-

[17]

, title =

Arrow, Kenneth J. , title =. Econom\'etrie, Colloques Internationaux du Centre National de la Recherche Scientifique , volume =

-

[18]

Finance and Stochastics , volume =

Inf-Convolution of Risk Measures and Optimal Risk Transfer , author =. Finance and Stochastics , volume =

-

[19]

and Ghossoub, Mario , title =

Boonen, Tim J. and Ghossoub, Mario , title =. European Journal of Operational Research , volume =. 2023 , doi =

2023

-

[20]

Co-Monotone Allocations,

Landsberger, Michael and Meilijson, Isaac , year = 1994, journal =. Co-Monotone Allocations,

1994

-

[21]

Games and Economic Behavior , volume =

Population Monotonic Allocation Schemes for Cooperative Games with Transferable Utility , author =. Games and Economic Behavior , volume =

-

[22]

Denneberg, Dieter , year = 1994, publisher =. Non-

1994

-

[23]

Introduction to the Mathematics of Ambiguity , booktitle =

Marinacci, Massimo and Montrucchio, Luigi , editor =. Introduction to the Mathematics of Ambiguity , booktitle =

-

[24]

Proceedings of the American Mathematical Society , year = 1986, volume =

Schmeidler, David , title =. Proceedings of the American Mathematical Society , year = 1986, volume =

1986

-

[25]

2026 , journal =

Risk Sharing, Measuring Variability, and Distortion Riskmetrics , author =. 2026 , journal =

2026

-

[26]

ASTIN Bulletin: The Journal of the IAA , volume =

Pareto-Optimal Peer-to-Peer Risk Sharing with Robust Distortion Risk Measures , author =. ASTIN Bulletin: The Journal of the IAA , volume =

-

[27]

1971 , journal =

Cores of convex games , author =. 1971 , journal =

1971

-

[28]

2013 , publisher =

Mathematical Risk Analysis , author =. 2013 , publisher =

2013

-

[29]

2016 , publisher =

Set Functions, Games and Capacities in Decision Making , author =. 2016 , publisher =

2016

-

[30]

Mathematical Finance , volume =

Grechuk, Bogdan and Molyboha, Anton and Zabarankin, Michael , title =. Mathematical Finance , volume =

-

[31]

SSRN Electronic Journal , year=

Stable Risk Sharing and Its Monotonicity , author=. SSRN Electronic Journal , year=. doi:10.2139/ssrn.2987631 , note=

-

[32]

Advances in Mathematical Economics , editor=

On law invariant coherent risk measures , author=. Advances in Mathematical Economics , editor=. 2001 , publisher=

2001

-

[33]

Games and Economic Behavior , volume=

Stable allocations of risk , author=. Games and Economic Behavior , volume=. 2009 , publisher=

2009

-

[34]

Debreu, Gerard , title =

-

[35]

Journal of Risk , volume=

Coherent allocation of risk capital , author=. Journal of Risk , volume=

-

[36]

SIAM Journal on Applied Mathematics , volume =

Schmeidler, David , title =. SIAM Journal on Applied Mathematics , volume =. 1969 , publisher =

1969

-

[37]

Cores of exact games,

Schmeidler, David , journal=. Cores of exact games,. 1972 , publisher=

1972

-

[38]

, title =

Shapley, Lloyd S. , title =. Contributions to the Theory of Games II , editor =

-

[39]

Bondareva, O. N. , title =. Problemy Kibernetiki , volume =. 1963 , note =

1963

-

[40]

, title =

Shapley, Lloyd S. , title =. Naval Research Logistics Quarterly , volume =

-

[41]

and Shubik, Martin , title =

Shapley, Lloyd S. and Shubik, Martin , title =. Journal of Economic Theory , volume =. 1969 , doi =

1969

-

[42]

, title =

Weber, Robert J. , title =. The Shapley Value: Essays in Honor of Lloyd S. Shapley , editor =

-

[43]

, title =

Derks, J.J.M. , title =. International Journal of Game Theory , volume =

-

[44]

Journal of Economic Theory , volume =

Ichiishi, Tatsuro , title =. Journal of Economic Theory , volume =

-

[45]

Mathematical Economics and Game Theory: Essays in Honor of Oskar Morgenstern , editor =

Owen, Guillermo , title =. Mathematical Economics and Game Theory: Essays in Honor of Oskar Morgenstern , editor =

-

[46]

Introduction to the Theory of Cooperative Games , edition =

Peleg, Bezalel and Sudh. Introduction to the Theory of Cooperative Games , edition =

-

[47]

Peters, Hans , title =

-

[48]

, title =

Harsanyi, John C. , title =. Contributions to the Theory of Games

-

[49]

, title =

Yaari, Menahem E. , title =. Econometrica , volume =

-

[50]

, title =

Wang, Shaun S. , title =. ASTIN Bulletin , volume =

-

[51]

Mathematical Finance , volume =

Artzner, Philippe and Delbaen, Freddy and Eber, Jean-Marc and Heath, David , title =. Mathematical Finance , volume =

-

[52]

Stochastic Finance: An Introduction in Discrete Time , edition =

F. Stochastic Finance: An Introduction in Discrete Time , edition =

-

[53]

Convex Measures of Risk and Trading Constraints , journal =

F. Convex Measures of Risk and Trading Constraints , journal =

-

[54]

Econometrica , volume =

Borch, Karl , title =. Econometrica , volume =

-

[55]

Econometrica , volume =

Wilson, Robert , title =. Econometrica , volume =. 1968 , doi =

1968

-

[56]

To Split or Not to Split:

Tsanakas, Andreas , year = 2009, journal =. To Split or Not to Split:

2009

-

[57]

Mathematics of Operations Research , publisher =

Distributional Transforms, Probability Distortions, and Their Applications , author =. Mathematics of Operations Research , publisher =

-

[58]

Economic Theory , volume =

Competitive Equilibria in a Comonotone Market , author =. Economic Theory , volume =

-

[59]

Population-Monotonicity of the Nucleolus on a Class of Public Good Problems , year =

S. Population-Monotonicity of the Nucleolus on a Class of Public Good Problems , year =

-

[60]

Social Choice and Welfare , year =

Abe, Takaaki and Liu, Shuige , title =. Social Choice and Welfare , year =

-

[61]

George , year = 2007, series =

Shaked, Moshe and Shanthikumar, J. George , year = 2007, series =. Stochastic

2007

-

[62]

Journal of Risk and Insurance , volume =

Risk-Sharing Rules and Their Properties, with Applications to Peer-to-Peer Insurance , author =. Journal of Risk and Insurance , volume =

-

[63]

Insurance: Mathematics and Economics , volume =

Denuit, Michel and Dhaene, Jan , title =. Insurance: Mathematics and Economics , volume =. 2012 , doi =

2012

-

[64]

, title =

Denuit, Michel and Robert, Christian Y. , title =. Insurance: Mathematics and Economics , volume =. 2023 , doi =

2023

-

[65]

, title =

Denuit, Michel and Robert, Christian Y. , title =. Journal of Multivariate Analysis , volume =. 2021 , doi =

2021

-

[66]

The Annals of Mathematical Statistics , volume =

Efron, Bradley , title =. The Annals of Mathematical Statistics , volume =. 1965 , doi =

1965

-

[67]

Insurance: Mathematics and Economics , volume =

Equilibria and Efficiency in a Reinsurance Market , author =. Insurance: Mathematics and Economics , volume =

-

[68]

Journal of Risk and Insurance , volume =

Pareto-efficient Risk Sharing in Centralized Insurance Markets with Application to Flood Risk , author =. Journal of Risk and Insurance , volume =

-

[69]

Insurance: Mathematics and Economics , volume =

Stackelberg Equilibria with Multiple Policyholders , author =. Insurance: Mathematics and Economics , volume =

-

[70]

Pareto-Optimal Peer-to-Peer Risk Sharing with Robust Distortion Risk Measures , author =. ASTIN Bulletin , volume =. doi:10.1017/asb.2025.6 , copyright =

-

[71]

Mathematical Finance , volume =

Efficiency in Pure-Exchange Economies With Risk-Averse Monetary Utilities , author =. Mathematical Finance , volume =

-

[72]

Management Science , volume =

Submodular Risk Allocation , author =. Management Science , volume =

-

[73]

Journal of Multivariate Analysis , volume =

Cambanis, Stamatis and Huang, Steel and Simons, Gordon , title =. Journal of Multivariate Analysis , volume =

-

[74]

Comonotonic Improvement under Feasibility Constraints , author =

-

[75]

doi:10.48550/arXiv.2603.01434 , journal =

A. doi:10.48550/arXiv.2603.01434 , journal =

-

[76]

, year = 2026, month = mar, number =

Tam, Brandon and Ghossoub, Mario and Pesenti, Silvana M. , year = 2026, month = mar, number =. Dynamic. doi:10.48550/arXiv.2603.19414 , journal =

-

[77]

ASTIN Bulletin: The Journal of the IAA , volume =

Distortion Riskmetrics on General Spaces , author =. ASTIN Bulletin: The Journal of the IAA , volume =

-

[78]

On Comonotonicity of

Ludkovski, Michael and R. On Comonotonicity of. Statistics & Probability Letters , volume =

-

[79]

, title =

Pratt, John W. , title =. Management Science , volume =. 2000 , doi =

2000

-

[80]

Sovereign Climate and Disaster Risk Pooling:

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.