VIX options in Bergomi models

Pith reviewed 2026-06-28 11:52 UTC · model grok-4.3

The pith

Bergomi models admit closed-form leading asymptotics for VIX option prices in the joint short-maturity and small-vol-of-vol limit.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

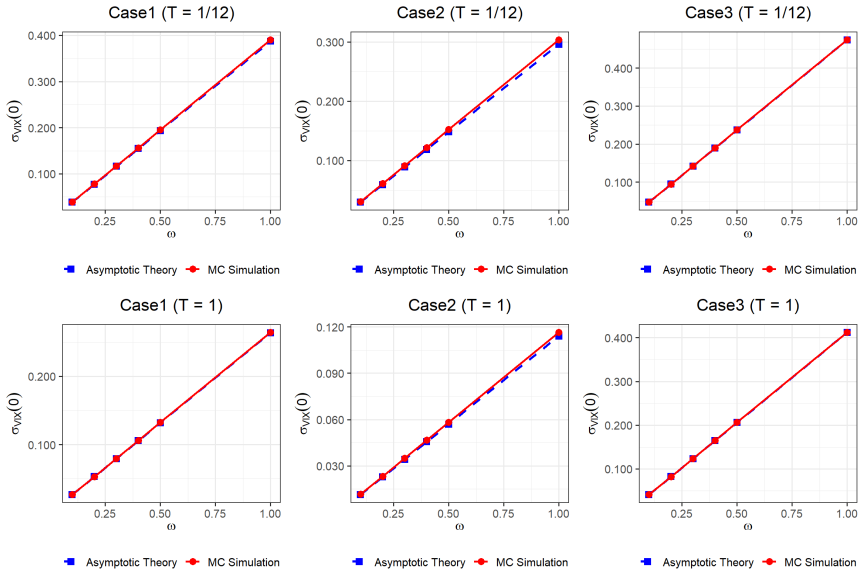

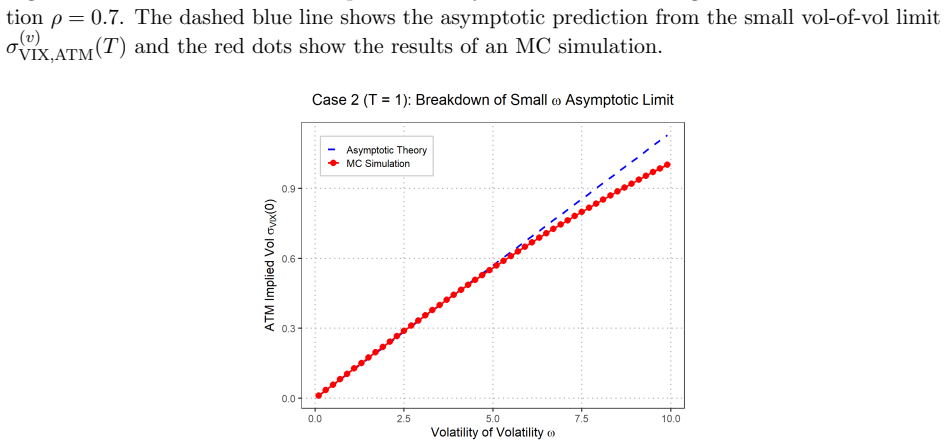

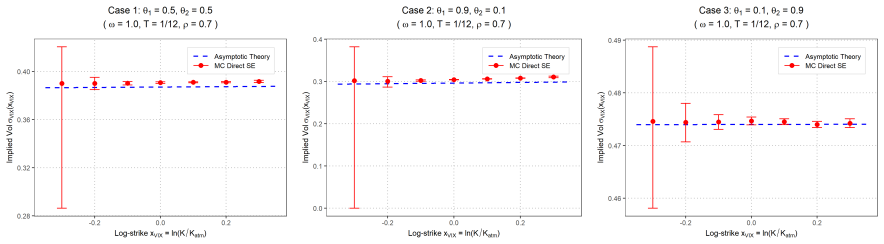

In the Bergomi stochastic-volatility model driven by forward-variance curves, the leading-order asymptotics of VIX call and put prices are obtained in closed form when maturity tends to zero while the volatility-of-volatility coefficient tends to zero. The derivation holds uniformly for the one-factor, two-factor, and N-factor specifications, delivering explicit expressions that translate into small-maturity expansions of the VIX implied volatility across strikes.

What carries the argument

The joint short-maturity and small-vol-of-vol asymptotic expansion of the VIX option price, which reduces the pricing integral to explicit leading terms involving the model's forward-variance dynamics.

If this is right

- The closed-form expressions allow direct evaluation of VIX option prices without simulation for arbitrarily small maturities.

- Small-maturity asymptotics of the VIX implied-volatility smile become explicit functions of the model's variance-curve parameters.

- The same leading-order formulas apply without change of structure when the number of factors is increased from one to N.

- Numerical tests in the paper confirm that the leading term already captures the dominant behavior for the chosen small-parameter regime.

Where Pith is reading between the lines

- The same expansion technique could be applied to other variance-curve models that share the Bergomi structure of stochastic forward variances.

- Calibration routines for short-dated VIX options could use these formulas as an analytic anchor before adding higher-order corrections.

- The predicted small-maturity VIX smile shape supplies a concrete benchmark that market data at very short tenors could be checked against.

Load-bearing premise

The Bergomi forward-variance dynamics must permit a joint expansion in small maturity and small volatility of volatility whose leading term closes in explicit form without being overwhelmed by higher-order contributions.

What would settle it

Fix a one-factor Bergomi parameter set with maturity equal to 0.01 and volatility-of-volatility equal to 0.01; numerically compute the exact VIX option price by Monte Carlo or PDE methods and test whether the closed-form asymptotic formula lies inside a 5 percent relative error band.

Figures

read the original abstract

We present a study of the leading-order asymptotics for VIX option prices in Bergomi models in the short-maturity and small volatility-of-volatility regimes. Both out-of-the-money (OTM) and at-the-money (ATM) asymptotics are considered for one-factor, two-factor Bergomi and $N$-factor models. The leading-order asymptotics are obtained in closed-form, which are translated into predictions for the small-maturity asymptotics of the VIX implied volatility. Numerical illustrations are provided to illustrate the efficiency of the closed-form asymptotic formulas.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript derives leading-order asymptotic expansions for VIX option prices (both OTM and ATM) in one-factor, two-factor, and general N-factor Bergomi models in the joint short-maturity and small volatility-of-volatility limit. The leading terms are obtained in closed form, converted into explicit predictions for the small-maturity asymptotics of VIX implied volatility, and supported by numerical illustrations.

Significance. If the closed-form derivations are correct, the results supply practical, explicit approximations for VIX options under Bergomi dynamics, which are widely used for forward-variance modeling. The N-factor generalization and the translation to implied-volatility asymptotics add value for calibration and benchmarking in quantitative finance.

minor comments (3)

- [Introduction] The abstract states that the leading-order terms are obtained in closed form, but the manuscript should include at least one explicit leading-term expression (e.g., for the one-factor case) in the introduction or a dedicated section to allow immediate verification of the claimed closed-form nature.

- [Numerical section] Numerical illustrations are mentioned; the captions or text should explicitly state the parameter values, number of Monte Carlo paths or quadrature points used, and the precise regime (maturity and vol-of-vol values) to facilitate reproducibility.

- [Model setup] Notation for the forward-variance curve and the volatility-of-volatility scaling parameter should be introduced once with a clear table or list before the asymptotic analysis begins.

Simulated Author's Rebuttal

We thank the referee for the positive summary, significance assessment, and recommendation of minor revision. No specific major comments appear in the report, so we have no point-by-point items to address.

Circularity Check

No significant circularity

full rationale

The paper performs a standard small-noise asymptotic expansion on the forward-variance dynamics of the Bergomi model in the joint short-maturity / small vol-of-vol limit. Leading-order terms for VIX option prices (OTM and ATM) are stated to be obtained in closed form directly from the model SDEs for one-, two-, and N-factor cases, then converted to implied-volatility asymptotics. No fitted parameters are renamed as predictions, no self-citation chain is load-bearing for the central derivation, and no ansatz or uniqueness result is smuggled in. The derivation chain is therefore self-contained against the model equations and does not reduce to its own inputs by construction.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

, Journal =

Bergomi, L. , Journal =. Smile dynamics , volume=

-

[2]

, Journal =

Bergomi, L. , Journal =. Smile dynamics

-

[3]

, Title =

Bergomi, L. , Title =

-

[4]

and Guyon, J

Bergomi, L. and Guyon, J. , Journal =. The smile in stochastic volatility models , Year =

-

[5]

and De Marco, S

Bourgey, F. and De Marco, S. and Gobet, E. , Journal =. Weak approximations and

-

[6]

and Agarwal, A

Liao, Y. and Agarwal, A. and Bourgey, F. , Journal =. Implied volatility expansions for

-

[7]

, Journal =

Ould Aly, S. , Journal =. Forward variance dynamics: Bergomi's model revisited , Volume =

-

[8]

, Journal =

Guyon, J. , Journal =. The smile of stochastic volatility: Revisiting the

-

[9]

, Journal =

Guyon, J. , Journal =. The

-

[10]

and Muguruza, A

Lacombe, C. and Muguruza, A. and Stone, H. , Journal =. Asymptotics for volatility derivatives in multi-factor rough volatility models , Volume =

-

[11]

and Alfeus, M

Kyakutwika, N. and Alfeus, M. and Schlogl, E. , Journal =. Pricing and calibration of

-

[12]

SSRN:1118245 , Title =

B\". SSRN:1118245 , Title =

-

[13]

, Journal =

Gatheral, J. , Journal =. Consistent modeling of

-

[14]

Econometrica , volume=

Transform analysis and asset pricing for affine jump-diffusions , author=. Econometrica , volume=

-

[15]

and Wang, X

Pirjol, D. and Wang, X. and Zhu, L. , Journal =. Short-maturity asymptotics for

-

[16]

and Pirjol, D

Guo, D. and Pirjol, D. and Wang, X. and Zhu, L. , Journal =

-

[17]

Management Science , volume=

A jump-diffusion model for option pricing , author=. Management Science , volume=. 2002 , publisher=

2002

-

[18]

and Dotsis, G

Psychoyios, D. and Dotsis, G. and Markellos, R. N. , journal =. A jump diffusion model for. 2010 , volume =

2010

-

[19]

and Chang, C.-H

Lin, Y.-N. and Chang, C.-H. , journal =. 2009 , volume =

2009

-

[20]

and Tauchen, G

Todorov, V. and Tauchen, G. , journal =. The jump component of. 2011 , volume =

2011

-

[21]

, journal =

Eraker, B. , journal =. Do stock prices and volatility jump?. 2004 , volume =

2004

-

[22]

, journal =

Eraker, B. , journal =. Jump and volatility risk premiums implied by. 2010 , volume =

2010

-

[23]

and Stisen, M

Kokholm, T. and Stisen, M. , journal =. Consistent Modelling of. 2013 , volume =

2013

-

[24]

and Ni, J

Zang, X. and Ni, J. and Huang, J.-Z. and Wu, L. , journal =. Double-jump diffusion model for. 2017 , volume =

2017

-

[25]

and Li, S

Jing, B. and Li, S. and Ma, Y. , journal =. Consistent pricing of. 2020 , volume =

2020

-

[26]

and Stisen, M

Kokholm, T. and Stisen, M. , journal =. Joint pricing of. 2015 , volume =

2015

-

[27]

and Li, L

Li, J. and Li, L. and Zhang, G. , journal =. Pure jump models for pricing and hedging. 2017 , volume =

2017

-

[28]

, journal =

Park, Y.-H. , journal =. The effects of asymmetric volatility and jumps on the pricing of. 2016 , volume =

2016

-

[29]

and Illand, C

Abi Jaber, E. and Illand, C. and Li, S. , journal=. 2023 , volume=

2023

-

[30]

and Song, X

Akahori, J. and Song, X. and Wang, Tai-Ho , journal=. 2022 , pages=

2022

-

[31]

Review of Financial Studies , year=

A closed-form solution for options with stochastic volatility with applications to bond and currency options , author=. Review of Financial Studies , year=

-

[32]

Journal of Finance , year=

The pricing of options on assets with stochastic volatilities , author=. Journal of Finance , year=

-

[33]

Finance and Stochastics , year=

On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility , author=. Finance and Stochastics , year=

-

[34]

and Nualart, E

Al\'os, E. and Nualart, E. and Pravosud, M. , journal=. On the implied volatility of

-

[35]

and Badran, A

Baldeaux, J. and Badran, A. , journal=. Consistent modelling of

-

[36]

and Caramellino, L

Baldi, P. and Caramellino, L. , journal=. General. 2011 , pages=

2011

-

[37]

Quantitative Finance , year=

Asymptotics and calibration of local volatility models , author=. Quantitative Finance , year=

-

[38]

and Gobet, E

Bompis, R. and Gobet, E. , journal=. Analytical approximations of local-. 2018 , pages=

2018

-

[39]

and Badescu, A

Cao, H. and Badescu, A. and Cui, Z. and Jayaraman, S.K. , journal =. Valuation of. 2020 , pages =

2020

-

[40]

Finance and Stochastics , year=

Pricing options on realized variance , author=. Finance and Stochastics , year=

-

[41]

Annual Reviews of Finance and Economics , year=

Volatility derivatives , author=. Annual Reviews of Finance and Economics , year=

-

[42]

2019 , note=

A log-normal type stochastic volatility model with quadratic drift , author=. 2019 , note=

2019

-

[43]

and Costanzino, N

Cheng, W. and Costanzino, N. and Liechty, J. and Mazzucato, A. and Nistor, V. , journal=. 2011 , pages=

2011

-

[44]

Journal of Portfolio Management , year=

The Constant elasticity of variance option pricing model , author=. Journal of Portfolio Management , year=

-

[45]

Econometrica , year=

A theory of the term structure of interest rates , author=. Econometrica , year=

-

[46]

and Gazzani, G

Cuchiero, C. and Gazzani, G. and M\". Joint calibration to. Mathematical Finance , volume=

-

[47]

and Nagardjasarma, J

Dassios, A. and Nagardjasarma, J. , journal=. The square-root process and. 2006 , pages=

2006

-

[48]

and Zeitouni, O

Dembo, A. and Zeitouni, O. , year=. Large Deviations Techniques and Applications , edition=

-

[49]

2006 , publisher=

The Volatility Surface , author=. 2006 , publisher=

2006

-

[50]

Trading and hedging local volatility , author=

-

[51]

European Finance Review , year=

The valuation of volatility options , author=. European Finance Review , year=

-

[52]

and Rouault, A

Donati-Martin, C. and Rouault, A. and Yor, M. and Zani, M. , journal=. Large deviations for squares of. 2004 , pages=

2004

-

[53]

The integrated square root process , author=

-

[54]

Risk , year=

Pricing with a smile , author=. Risk , year=

-

[55]

From implied to spot volatilities , author=

-

[56]

Mathematical Finance , year=

Asymptotics of implied volatility in local volatility models , author=. Mathematical Finance , year=

-

[57]

Wilmott , year=

Managing smile risk , author=. Wilmott , year=

-

[58]

and Forde, M

Figueroa-Lopez, J. and Forde, M. , journal=. The small-maturity smile for exponential. 2012 , pages=

2012

-

[59]

and Jacquier, A

Forde, M. and Jacquier, A. , journal=. Small-time asymptotics for implied volatility under the. 2009 , pages=

2009

-

[60]

Applied Mathematical Finance , year=

Small-time asymptotics for an uncorrelated local-stochastic volatility model , author=. Applied Mathematical Finance , year=

-

[61]

and Jacquier, A

Forde, M. and Jacquier, A. and Lee, R. , journal=. The small-time smile and term structure of implied volatility under the. 2012 , pages=

2012

-

[62]

and Smith, B

Forde, M. and Smith, B. , journal=. Markovian stochastic volatility with stochastic correlation - joint calibration and consistency of. 2023 , pages=

2023

-

[63]

Annals of Applied Probability , year=

Precise asymptotics: robust stochastic volatility models , author=. Annals of Applied Probability , year=

-

[64]

and Mazur, M

Goard, J. and Mazur, M. , journal=. Stochastic volatility models and the pricing of. 2013 , pages=

2013

-

[65]

, journal=

Guyon, J. , journal=. The joint. 2020 , volume=

2020

-

[66]

The quadratic rough Heston model and the joint S&P 500/VIX smile calibration problem , author=. arXiv:2001.01789 , year=

arXiv 2001

-

[67]

Advanced Methods in Option Pricing , author=

Analysis, Geometry and Modeling in Finance. Advanced Methods in Option Pricing , author=. 2008 , publisher=

2008

-

[68]

and Jacquier, A

Horvath, B. and Jacquier, A. and Tankov, P. , title =. SIAM Journal on Financial Mathematics , volume=

-

[69]

and Watanabe, S

Ikeda, N. and Watanabe, S. , title =. Osaka Journal of Mathematics , volume=

-

[70]

and Muguruza, A

Jacquier, A. and Muguruza, A. and Pannier, A. , title =. Advances in Applied Probability , year=

-

[71]

Recent Advances in Applied Probability , year =

Implied volatility: Statics, Dynamics and Probabilistic Interpretation , author =. Recent Advances in Applied Probability , year =

-

[72]

2000 , publisher=

Option Valuation Under Stochastic Volatility , author=. 2000 , publisher=

2000

-

[73]

2016 , publisher=

Option Valuation Under Stochastic Volatility II , author=. 2016 , publisher=

2016

-

[74]

Encyclopedia of Quantitative Finance , editor =

The constant elasticity of variance model , author =. Encyclopedia of Quantitative Finance , editor =. 2010 , publisher =

2010

-

[75]

Lian, G.H. and S.P. Zhu , journal =. Pricing

-

[76]

Correlations and bounds for stochastic volatility models , author =

-

[77]

Mathematical Finance , volume =

Explicit implied volatilities for multifactor local-stochastic volatility models , author=. Mathematical Finance , volume =

-

[78]

and Yor, M

Matsumoto, H. and Yor, M. , journal=. Exponential functionals of the

-

[79]

and Pirjol, D

Nandori, P. and Pirjol, D. , journal=. On the distribution of the time integral of the geometric

-

[80]

and Pascucci, A

Pagliarani, S. and Pascucci, A. , journal=. The exact

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.