Fast-excursion limit of the Heston model

Pith reviewed 2026-06-27 22:23 UTC · model grok-4.3

The pith

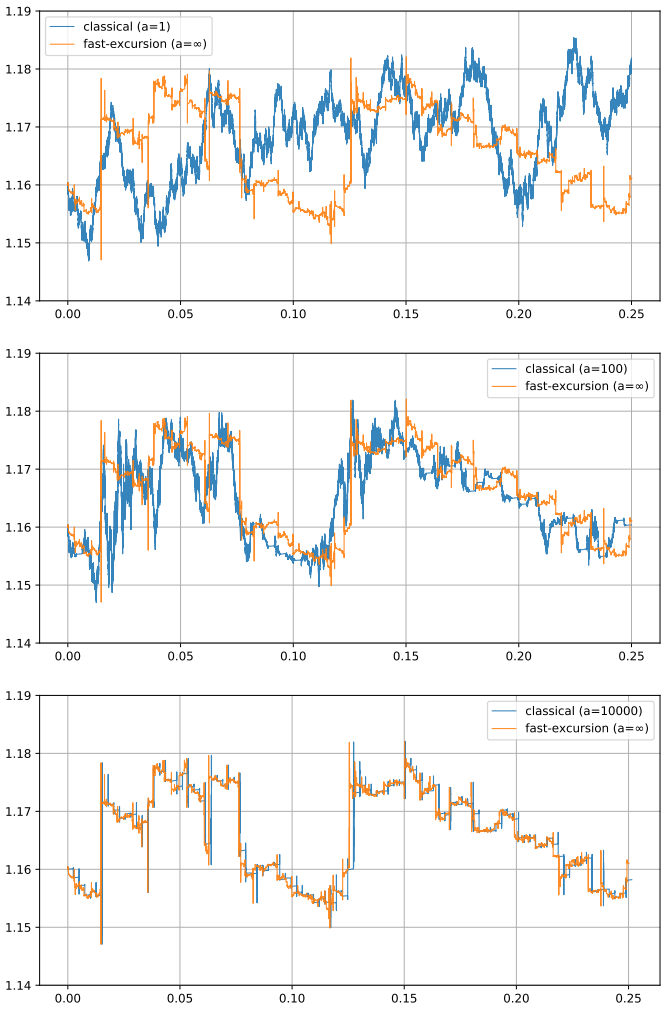

The Heston model under fast reversion produces price paths that traverse entire intervals instantaneously.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

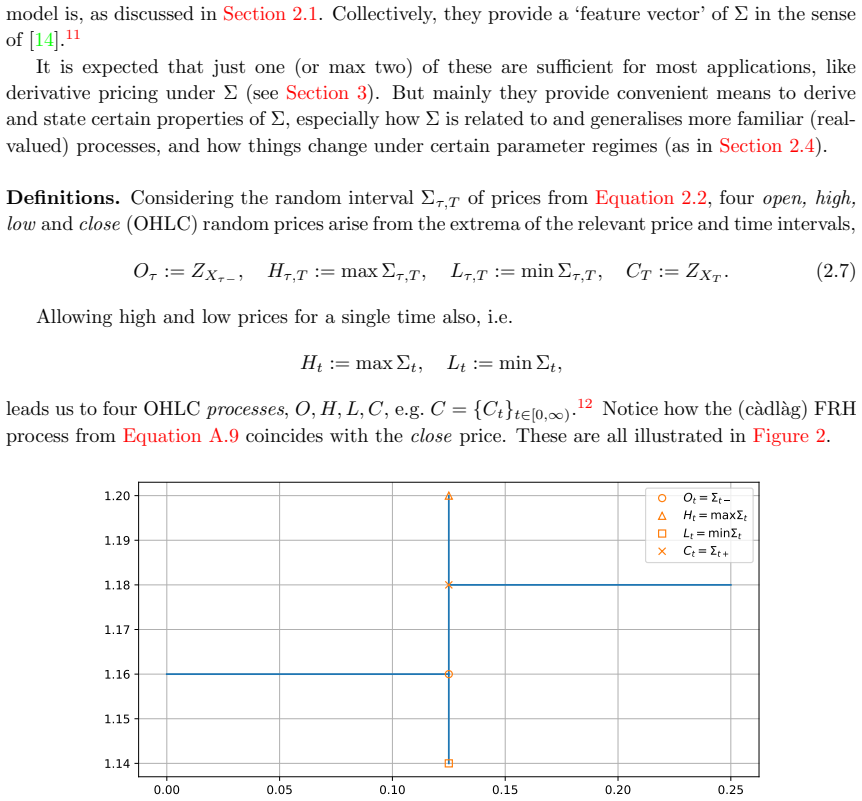

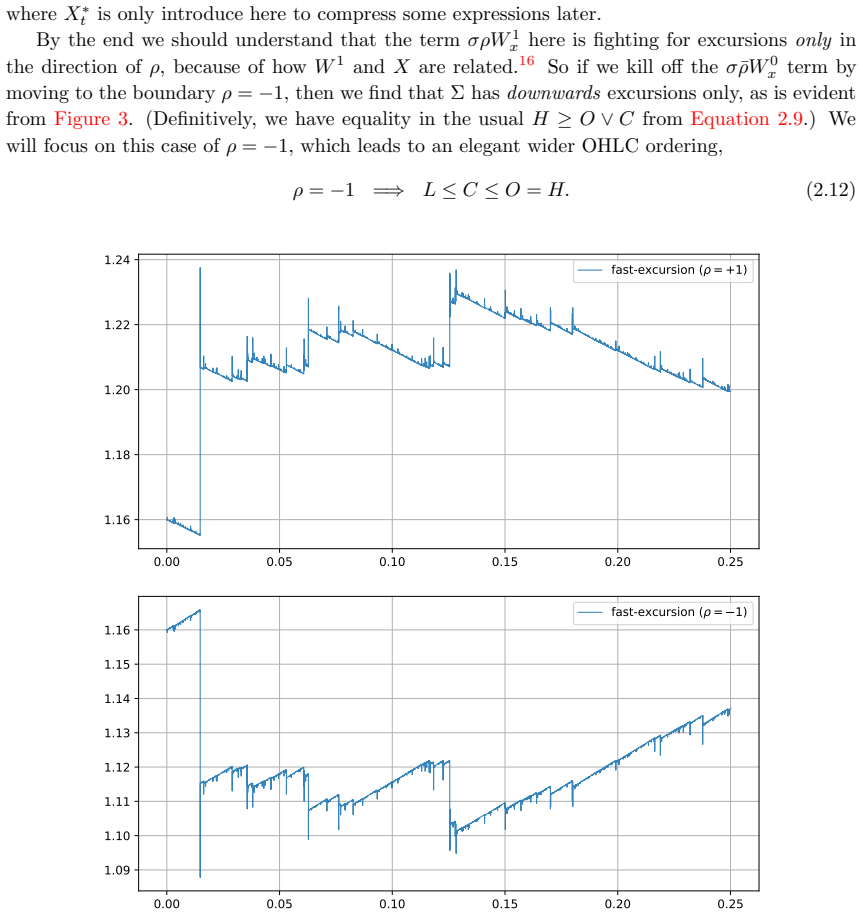

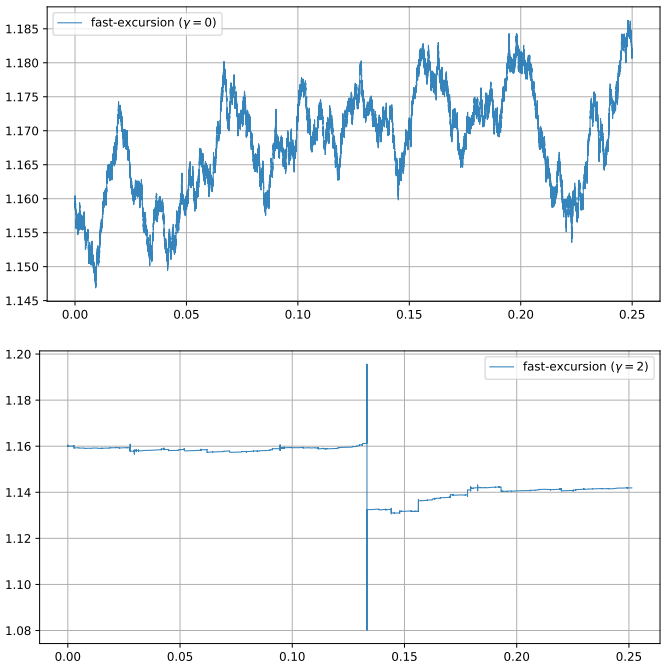

Under Mechkov's fast-reversion limit the Heston price process converges to an interval-valued process that exists as a lift of a subordinated Levy process through selections in the theory of random closed sets; this limit is non-degenerate and escapes the Skorokhod topologies while leaving vanilla prices unchanged.

What carries the argument

The fast-excursion limit applied to the Heston model, which yields interval-valued selections of random closed sets that lift subordinated Levy processes.

If this is right

- Hitting probabilities for continuously monitored barrier options increase because the process can cross the barrier during an excursion.

- Vanilla option prices remain identical to those of the classical Heston model.

- The process admits simulation via price-time parametric representations that converge visibly to the limit.

- The construction supplies a concrete example of a stochastic-volatility limit that requires the theory of random closed sets rather than standard path spaces.

Where Pith is reading between the lines

- The same limiting construction could be applied to other stochastic-volatility diffusions whose reversion speed is sent to infinity.

- Interval-valued selections might furnish a tractable way to embed path-dependent risk into Levy-driven models without introducing additional state variables.

- Market quotes on short-dated barrier options could be used to back out an effective excursion width and test consistency with the predicted hitting-rate uplift.

Load-bearing premise

Mechkov's fast-reversion limit applied to the classical Heston model produces a well-defined non-degenerate process whose paths are interval-valued selections of random closed sets rather than standard cadlag functions.

What would settle it

Numerical paths generated from the original Heston model at successively higher reversion speeds fail to converge in distribution to an interval-valued process that raises barrier hitting probabilities by the reported order of magnitude.

Figures

read the original abstract

This article introduces an unconventional model for price processes in finance that emerges from the classical Heston model under Mechkov's fast-reversion limit. This new fast-excursion Heston model exhibits instantaneous (i.e. fast) excursions through an interval of prices at each time, which are invisible to vanilla options but critical for hitting probabilities and continuously monitored exotics. Theoretically, the model provides a rare example of a non-degenerate limit of stochastic volatility models that escapes the Skorokhod topologies. This leads us to a class of interval-valued processes which exist as lifts of subordinated Levy processes, through the concept of selections in the theory of random closed sets. On the practical side, we show how the model can be simulated using price-time parametric representations, and utilise a purpose-built classical Heston simulation scheme in order to visualise convergence. Finally we demonstrate how this model raises hitting probabilities for barrier options considerably (of order 10% for one-month EURUSD options), due to taking excursion risk into account.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that applying Mechkov's fast-reversion limit to the classical Heston model produces a 'fast-excursion Heston model' whose paths consist of instantaneous excursions through price intervals. These excursions are invisible to vanilla options but affect hitting probabilities and continuously monitored exotics. The construction is presented as a rare non-degenerate limit of stochastic volatility models that escapes Skorokhod topologies, realized instead as interval-valued processes that exist as lifts of subordinated Lévy processes via selections of random closed sets. The manuscript also describes simulation via price-time parametric representations, visual convergence from a custom Heston simulator, and an approximate 10% increase in barrier-option hitting probabilities for one-month EURUSD options.

Significance. A rigorously derived non-degenerate limit outside Skorokhod space with concrete implications for exotic-option pricing would be a notable contribution to mathematical finance. The invocation of random-closed-set selections to obtain interval-valued lifts of Lévy processes is potentially innovative, but the absence of explicit scaling, limiting-object identification, or measurability verification prevents assessment of whether these strengths are realized.

major comments (2)

- [Abstract] Abstract: the central claim that Mechkov's fast-reversion scaling applied to the Heston SDEs yields a non-degenerate limit whose paths are interval-valued selections of random closed sets (rather than càdlàg functions) is stated without any explicit scaling, SDE limit calculation, or verification that the requisite measurability and closed-set conditions hold.

- [Abstract] Abstract: no analytic construction is supplied identifying the limiting object as a lift of a subordinated Lévy process; the only supporting evidence mentioned is visual convergence from a purpose-built simulator, which cannot substitute for the missing derivation.

minor comments (2)

- [Abstract] The reference to 'Mechkov's fast-reversion limit' should include a precise bibliographic citation to the source paper.

- The reported 10% increase in hitting probabilities for one-month EURUSD barrier options would benefit from explicit simulation parameters, number of paths, and direct numerical comparison against the classical Heston model under identical seeds.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive feedback. The major comments correctly note that the abstract is concise and omits explicit details of the scaling and derivations. These elements are developed in the body of the manuscript, but we agree the abstract should be revised for clarity. We address each point below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central claim that Mechkov's fast-reversion scaling applied to the Heston SDEs yields a non-degenerate limit whose paths are interval-valued selections of random closed sets (rather than càdlàg functions) is stated without any explicit scaling, SDE limit calculation, or verification that the requisite measurability and closed-set conditions hold.

Authors: The scaling parameter and SDE limit calculation appear in Sections 2 and 3, where Mechkov's fast-reversion limit is applied to the Heston dynamics and the resulting interval-valued process is obtained via selections from random closed sets. Measurability follows from standard results in the theory of random closed sets (e.g., the measurable selection theorem). We acknowledge that these steps are not summarized in the abstract. We will revise the abstract to include a brief statement of the scaling (ε → 0) and the use of random-closed-set selections. revision: yes

-

Referee: [Abstract] Abstract: no analytic construction is supplied identifying the limiting object as a lift of a subordinated Lévy process; the only supporting evidence mentioned is visual convergence from a purpose-built simulator, which cannot substitute for the missing derivation.

Authors: The analytic identification of the limit as a lift of a subordinated Lévy process is given in Section 4, using the selection mechanism for random closed sets. The simulator results (Section 5) are presented only as numerical confirmation of convergence and are not offered as a substitute for the derivation. We will revise the abstract to reference the analytic construction explicitly. revision: yes

Circularity Check

No significant circularity; derivation applies external limit to Heston model

full rationale

The paper constructs its fast-excursion Heston model by applying Mechkov's fast-reversion limit to the classical Heston SDEs and then invoking selections from the theory of random closed sets to obtain interval-valued processes that lift subordinated Lévy processes. No quoted equations, fitted parameters, or self-citations appear in the abstract or description that would reduce the claimed limit object or its escape from Skorokhod space to a definitionally equivalent input. Simulation is used only for visualization of convergence, not as the source of the theoretical result. The derivation therefore remains self-contained as an application of cited external techniques rather than a self-referential renaming or fit.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Mechkov's fast-reversion limit exists and can be applied to the classical Heston model

invented entities (2)

-

fast-excursion Heston model

no independent evidence

-

interval-valued processes as lifts of subordinated Levy processes via selections of random closed sets

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Simulation of square-root processes made simple: applications to the Heston model

Eduardo Abi Jaber. “Simulation of square-root processes made simple: applications to the Heston model”. In:Risk(June 2025). Cutting Edge section.url:https://www.risk.net/ cutting-edge

2025

-

[2]

Volterra clocks and their pure-jump limits: hitting times of curved boundaries

Eduardo Abi Jaber, Elie Attal, and Andreas Søjmark. “Volterra clocks and their pure-jump limits: hitting times of curved boundaries”. In:arXiv preprint arXiv:2605.29073(May 2026). arXiv:2605.29073 [math.PR]

Pith/arXiv arXiv 2026

-

[3]

Reconciling Rough Volatility with Jumps

Eduardo Abi Jaber and Nathan De Carvalho. “Reconciling Rough Volatility with Jumps”. In:SIAM Journal on Financial Mathematics15.3 (2024), pp. 785–823.doi:10 . 1137 / 23M1558847

2024

-

[4]

Spike and hike modeling for interest rate derivatives: with an application to SOFR caplets

Leif Andersen and Dominique Bang. “Spike and hike modeling for interest rate derivatives: with an application to SOFR caplets”. In:Quantitative Finance24.8 (2024), pp. 1017–1033

2024

-

[5]

1017 / cbo9780511809781.url:https : / / doi

David Applebaum.L´ evy Processes and Stochastic Calculus(2nd ed.) Cambridge Univer- sity Press, 2009.doi:10 . 1017 / cbo9780511809781.url:https : / / doi . org / 10 . 1017 / cbo9780511809781

2009

-

[6]

Normal\\inverse Gaussian processes and the modelling of stock returns

O. E. Barndorff-Nielsen. “Normal\\inverse Gaussian processes and the modelling of stock returns”. In:Department of Mathematical Sciences, Aarhus University(1994)

1994

-

[7]

World Scientific, 2010.url:https://doi.org/10.1142/7928

Ole E Barndorff-Nielsen and Albert Shiryaev.Change of Time and Change of Measure. World Scientific, 2010.url:https://doi.org/10.1142/7928

-

[8]

Normal Inverse Gaussian Distributions and Stochastic Volatility Modelling

Ole E. Barndorff-Nielsen. “Normal Inverse Gaussian Distributions and Stochastic Volatility Modelling”. In:Scandinavian Journal of Statistics24.1 (1997), pp. 1–13.url:https://doi. org/10.1111/1467-9469.00045

-

[9]

Gerald Beer.Topologies on Closed and Closed Convex Sets. Vol. 268. Mathematics and Its Applications. Springer Dordrecht, 1993.doi:10.1007/978-94-015-8149-3

-

[10]

Jean Bertoin.L´ evy Processes. Vol. 121. Cambridge Tracts in Mathematics. Cambridge: Cam- bridge University Press, 1996.isbn: 978-0521646321

1996

-

[11]

Patrick Billingsley.Convergence of Probability Measures(2nd ed.) Wiley, 1999.url:https: //doi.org/10.1002/9780470316962

-

[12]

Comments on the life and mathematical legacy of Wolfgang Doeblin

Bernard Bru and Marc Yor. “Comments on the life and mathematical legacy of Wolfgang Doeblin”. In:Finance and Stochastics6.1 (Jan. 2002), pp. 3–47.issn: 0949-2984.doi:10. 1007/s780-002-8399-0.url:https://doi.org/10.1007/s780-002-8399-0

-

[13]

Espen Gaarder Haug.The Complete Guide to Option Pricing Formulas. 2nd. McGraw-Hill, 2007.isbn: 978-0071389976

2007

-

[14]

Conditional expectation and martingales of random sets

Christian Hess. “Conditional expectation and martingales of random sets”. In:Pattern Recog- nition32.9 (1999), pp. 1543–1567.doi:10.1016/S0031-3203(98)00185-3. 19

-

[15]

The Review of Financial Studies 6(2), 327–343 (1993) https://doi.org/10.1093/rfs/6.2.327

Steven L. Heston. “A Closed-Form Solution for Options with Stochastic Volatility with Ap- plications to Bond and Currency Options”. In:The Review of Financial Studies6.2 (1993), pp. 327–343.url:https://doi.org/10.1093/rfs/6.2.327

-

[16]

Pricing of first touch digitals under normal inverse Gaussian processes

Kudryavtsev and Levendorskii. “Pricing of first touch digitals under normal inverse Gaussian processes”. In: (2006).url:https://papers.ssrn.com/sol3/papers.cfm?abstract_id= 520045

2006

-

[17]

Lewis.A Simple Option Formula for General Jump-Diffusion and Other Exponential L´ evy Processes

Alan L. Lewis.A Simple Option Formula for General Jump-Diffusion and Other Exponential L´ evy Processes. Technical Report. OptionCity.net, 2001.url:http: // optioncity. net/ pubs/Exp_Levy.pdf

2001

-

[18]

Madan and Wim Schoutens.Applied Conic Finance

Dilip B. Madan and Wim Schoutens.Applied Conic Finance. Cambridge University Press, 2016.isbn: 9781107151697.doi:10.1017/cbo9781316585108

-

[19]

Mathematics PhD Theses, Imperial College London, 2021.url: https://doi.org/10.25560/92202

Ryan McCrickerd.On spatially irregular ordinary differential equations and a pathwise volatil- ity modelling framework. Mathematics PhD Theses, Imperial College London, 2021.url: https://doi.org/10.25560/92202

-

[20]

Fast-Reversion Limit of the Heston Model

Serguei Mechkov. “Fast-Reversion Limit of the Heston Model”. In:SSRN preprint. URL:https://ssrn.com/abstract=2418631(2015)

2015

-

[21]

Ilya Molchanov.Theory of Random Sets. 2nd. Springer, 2017.doi:10.1007/978-1-4471- 7349-6

-

[22]

Alexey A Muravlev. “Representation of a fractional Brownian motion in terms of an infinite- dimensional Ornstein-Uhlenbeck process”. In:Russian Mathematical Surveys66.2 (Apr. 2011), pp. 439–441.url:https://doi.org/10.1070/rm2011v066n02abeh004746

-

[23]

Springer Interna- tional Publishing, 2016.url:https://doi.org/10.1007/978-3-319-32408-1

Anatoliy Swishchuk.Change of Time Methods in Quantitative Finance. Springer Interna- tional Publishing, 2016.url:https://doi.org/10.1007/978-3-319-32408-1

-

[24]

Springer-Verlag New York, 2002.url:https : / / doi.org/10.1007/b97479

Ward Whitt.Stochastic-Process Limits. Springer-Verlag New York, 2002.url:https : / / doi.org/10.1007/b97479. A Background models This section provides an overview of existing models which help to see how the FEH model fits in. Themostrelevant models are the classical Heston model [15] and NIG L´ evy model [6], which are linked together through Mechkov’s F...

-

[25]

Theorem 2.18. I.e. the claim ofφ ε →φ 0 =φfollows fromf ε →f 0 uniformly over compacts asε→0.φ −1 ε →φ −1 0 =φ −1 then follows uniformly over compacts asε→0 by continuity. Recall that in Appendix D,Yis theinverseof Heston random ODE solutionX. So this convergence φ−1 ε →φ −1 from Lemma C.2 gives usY ε →Yasε→0 a.s., as required by using Equation D.1. D Sim...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.