Semiparametric Local Projections

Pith reviewed 2026-06-27 05:06 UTC · model grok-4.3

The pith

A semiparametric local projection estimator identifies nonlinear impulse response functions at the root-T rate.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The semiparametric local projection estimator, built from a doubly robust moment condition that identifies the average response function as a linear functional of a nonparametric conditional mean augmented by a density ratio capturing the effect of shifting the shock of interest, combined with cross-fitting, is root-T consistent and asymptotically normal for nonlinear impulse response functions in a broad class of structural dynamic models.

What carries the argument

Doubly robust moment condition identifying the average response as a linear functional of a nonparametric conditional mean augmented by a density ratio for the shock shift, paired with cross-fitting to address serial dependence.

If this is right

- The estimator applies to models featuring nonlinearly transformed regressors.

- It accommodates state-dependent coefficients without parametric restrictions on the dependence.

- It handles nonlinear interactions between shocks and state variables.

- It delivers asymptotic normality usable for confidence intervals around the nonlinear responses.

- Finite-sample behavior is reliable across a range of nonlinear data generating processes.

Where Pith is reading between the lines

- The framework could support policy analysis in settings where responses change with the size or sign of the shock.

- It may integrate with flexible nonparametric estimators for the conditional mean to handle higher-dimensional states.

- Researchers might compare its efficiency to fully nonparametric local projections in the same models.

- The approach could extend to panel or multi-country settings if cross-fitting is adapted for cross-sectional dependence.

Load-bearing premise

The doubly robust moment condition must correctly identify the average response function via the nonparametric conditional mean and the density ratio adjustment for the shock.

What would settle it

Monte Carlo simulations drawn from a known nonlinear structural model in the target class where the estimator fails to recover the true impulse responses at the root-T rate or exhibits non-normal finite-sample behavior.

Figures

read the original abstract

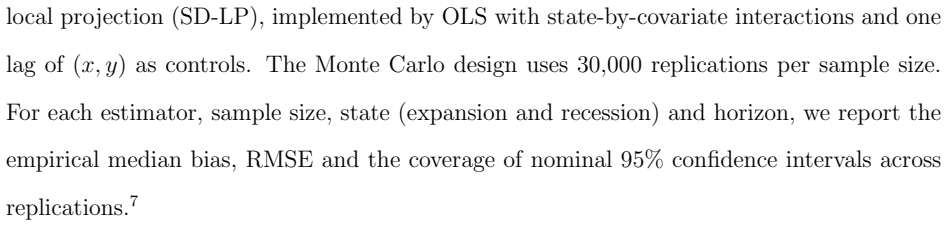

We propose a semiparametric local projection estimator of nonlinear impulse response functions for a broad class of structural dynamic models relevant for applied macroeconomics, including models with nonlinearly transformed regressors, state dependent coefficients, and nonlinear interactions between shocks and state variables. The estimator is based on a doubly robust moment condition that identifies the average response function as a linear functional of a nonparametric conditional mean, augmented by a density ratio that captures the effect of shifting the shock of interest. We combine this moment condition with cross-fitting that handles serial dependence. The resulting estimator is $\sqrt{T}$-consistent and asymptotically normal. We examine the finite-sample performance of the estimator across a range of nonlinear data generating processes and illustrate its use in two empirical examples.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims to develop a semiparametric local projection estimator for nonlinear impulse response functions applicable to a broad class of structural dynamic models that include nonlinear regressor transformations, state-dependent coefficients, and nonlinear shock-state interactions. Identification relies on a doubly robust moment condition expressing the target functional via a nonparametric conditional mean plus a density ratio for the shock shift; cross-fitting is used to accommodate serial dependence and deliver √T-consistency together with asymptotic normality. Finite-sample behavior is assessed via Monte Carlo experiments across several nonlinear DGPs, and the estimator is applied in two empirical illustrations.

Significance. If the stated √T-consistency and normality results hold, the estimator supplies a practical semiparametric tool for recovering nonlinear IRFs without committing to a fully parametric model. The doubly robust construction and the explicit treatment of serial dependence via cross-fitting are genuine strengths that improve robustness relative to standard local-projection or fully nonparametric alternatives. Simulation evidence across multiple DGPs and the two empirical examples further support applicability in applied macroeconometrics.

minor comments (2)

- The abstract and introduction would benefit from an explicit statement of the minimal regularity conditions (e.g., on the density ratio and the nonparametric rate) required for the cross-fitting argument to deliver the parametric rate under serial dependence.

- Notation for the target functional (average response) and the two nuisance functions should be introduced with a single consistent symbol set early in the paper to avoid later confusion when the moment condition is stated.

Simulated Author's Rebuttal

We thank the referee for the careful summary of the paper and the positive assessment of its contributions, particularly the doubly robust construction and handling of serial dependence via cross-fitting. The recommendation for minor revision is noted, though no specific major comments were raised in the report.

Circularity Check

No significant circularity identified

full rationale

The paper derives its √T-consistent estimator from an explicitly stated doubly robust moment condition that identifies the average response as a linear functional of a nonparametric conditional mean plus a density ratio, combined with cross-fitting to handle serial dependence. This follows standard semiparametric identification and rate arguments without reducing to self-defined quantities, fitted inputs renamed as predictions, or load-bearing self-citations. The abstract and construction are internally consistent with external semiparametric theory and contain no self-referential steps or imported uniqueness results.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The doubly robust moment condition identifies the average response function as a linear functional of a nonparametric conditional mean augmented by a density ratio

Reference graph

Works this paper leans on

-

[1]

and Aitken, C.G.G

Aitchinson, J. and Aitken, C.G.G. , title =. Biometrika , year =

-

[2]

and Kuersteiner, G.M

Angrist, J.D. and Kuersteiner, G.M. , title =. Review of Economics and Statistics , year =

-

[3]

and Haber, T

Ascari, G. and Haber, T. , title =. Economic Journal , year =

-

[4]

, title =

Ballarin, G. , title =

-

[5]

and Wehrli, A

Ballinari, D. and Wehrli, A. , title =

-

[6]

and Ramey, V.A

Ben Zeev, N. and Ramey, V.A. and Zubairy, S. , title =. AEA Papers and Proceedings , year =

-

[7]

and Blinder, A.S

Bernanke, B.S. and Blinder, A.S. , title =. American Economic Review , year =

-

[8]

and Mihov, I

Bernanke, B.S. and Mihov, I. , title =. Quarterly Journal of Economics , year =

-

[9]

and Ravenna, F

Cacciatore, M. and Ravenna, F. , title =. Economic Journal , year =

-

[10]

Journal of Money, Credit and Banking , volume=

Monetary policy and government debt , author=. Journal of Money, Credit and Banking , volume=. 2026 , publisher=

2026

-

[11]

and Martinez-Bruera, P

Caravello, T.E. and Martinez-Bruera, P. , title =

-

[12]

and Christensen, T.M

Chen, X. and Christensen, T.M. , title =. Journal of Econometrics , year =

-

[13]

and Chetverikov, D

Chernozhukov, V. and Chetverikov, D. and Demirer, M. and Duflo, E. and Hansen, C. and Newey, W. and Robins, J. , title =. Econometrics Journal , year =

-

[14]

and Newey, W.K

Chernozhukov, V. and Newey, W.K. and Singh, R. , title =. Econometrica , year =

-

[15]

2025 , eprint=

Automatic Debiased Machine Learning for Covariate Shifts , author=. 2025 , eprint=

2025

-

[16]

Journal of Business & Economic Statistics , volume=

Estimation of impulse response functions when shocks are observed at a higher frequency than outcome variables , author=. Journal of Business & Economic Statistics , volume=. 2022 , publisher=

2022

-

[17]

Journal of Money, Credit and Banking , volume=

Time variation in the inflation passthrough of energy prices , author=. Journal of Money, Credit and Banking , volume=. 2010 , publisher=

2010

-

[18]

Decomposing the Fiscal Multiplier , type =

Cloyne, James and Jord. Decomposing the Fiscal Multiplier , type =

-

[19]

State-Dependent Local Projections: Understanding Impulse Response Heterogeneity , type =

Cloyne, James and Jord. State-Dependent Local Projections: Understanding Impulse Response Heterogeneity , type =

-

[20]

and Giacomini, Raffaella and Jiao, Xiyu and Wang, Weining , title =

David, Joel M. and Giacomini, Raffaella and Jiao, Xiyu and Wang, Weining , title =. 2026 , note =

2026

-

[21]

, title =

Davidson, J. , title =

-

[22]

European Economic Review , volume=

Energy supply shocks’ nonlinearities on output and prices , author=. European Economic Review , volume=. 2025 , publisher=

2025

-

[23]

Journal of Monetary Economics , volume=

How sensitive are consumer expenditures to retail energy prices? , author=. Journal of Monetary Economics , volume=. 2009 , publisher=

2009

-

[24]

and Hoffmann, M

Falck, E. and Hoffmann, M. and H. Disagreement about inflation expectations and monetary policy transmission , journal =. 2021 , volume =

2021

-

[25]

and Gijbels, I

Fan, J. and Gijbels, I. , title =

-

[26]

and Gambetti, L

Forni, M. and Gambetti, L. and Maffei-Faccioli, N. and Sala, L. , title =. Journal of Money, Credit and Banking , year =

-

[27]

Impulse response analysis for structural dynamic models with nonlinear regressors , journal =

Gon. Impulse response analysis for structural dynamic models with nonlinear regressors , journal =. 2021 , volume =

2021

-

[28]

State-dependent local projections , journal =

Gon. State-dependent local projections , journal =. 2024 , volume =

2024

-

[29]

Nonparametric Local Projections , note =

Gon. Nonparametric Local Projections , note =. 2024 , pages =

2024

-

[30]

and Lee, Q

Gourieroux, C. and Lee, Q. , title =

-

[31]

Economics Letters , volume=

Does the inflation pass-through of gasoline price shocks depend on the level of inflation? , author=. Economics Letters , volume=. 2024 , publisher=

2024

-

[32]

and Payne, J

Hall, G.J. and Payne, J. and Sargent, T.J. , title =

-

[33]

, title =

Hansen, B. , title =. Econometric Theory , year =

-

[34]

and Parmeter, C.F

Henderson, D.J. and Parmeter, C.F. , title =. Statistics and Probability Letters , year =

-

[35]

and Lagalo, L.G

Herrera, A.M. and Lagalo, L.G. and Wada, T. , title =. Journal of International Money and Finance , year =

-

[36]

and Jord

Huang, J. and Jord. High-Dimensional Nonparametric Local Projections , note =

-

[37]

Estimation and inference of impulse responses by local projections , journal =

Jord. Estimation and inference of impulse responses by local projections , journal =. 2005 , volume =

2005

-

[38]

and Vigfusson, R.J

Kilian, L. and Vigfusson, R.J. , title =. Quantitative Economics , year =

-

[39]

Journal of Applied Econometrics , volume=

Oil prices, gasoline prices, and inflation expectations , author=. Journal of Applied Econometrics , volume=. 2022 , publisher=

2022

-

[40]

Research Handbook on Inflation , pages=

Oil price shocks and inflation , author=. Research Handbook on Inflation , pages=. 2025 , publisher=

2025

-

[41]

Dynamic causal effects in a nonlinear world: The good, the bad, and the ugly , journal =

Koles. Dynamic causal effects in a nonlinear world: The good, the bad, and the ugly , journal =. 2025 , volume =

2025

-

[42]

and Pesaran, M.H

Koop, G. and Pesaran, M.H. and Potter, S.M. , title =. Journal of Econometrics , year =

-

[43]

and Racine, J.S

Li, Q. and Racine, J.S. , title =. Statistica Sinica , year =

-

[44]

and Racine, J.S

Li, Q. and Racine, J.S. , title =

-

[45]

, title =

Newey, W.K. , title =. Econometric Theory , year =

-

[46]

, title =

Newey, W.K. , title =. Journal of Econometrics , year =

-

[47]

and McFadden, D

Newey, W.K. and McFadden, D. , title =. Handbook of Econometrics, Volume

-

[48]

Nikolaishvili, Giorgi , title =

-

[49]

, title =

Potter, S.M. , title =. Journal of Economic Dynamics and Control , year =

-

[50]

and Li, Q

Racine, J.S. and Li, Q. , title =. Journal of Econometrics , year =

-

[51]

Manuscript, arXiv:1903.01637 , year=

When do common time series estimands have nonparametric causal meaning? , author=. Manuscript, arXiv:1903.01637 , year=

-

[52]

Declining volatility in the

Ramey, Valerie A and Vine, Daniel J , journal=. Declining volatility in the. 2006 , publisher=

2006

-

[53]

Oil, automobiles, and the

Ramey, Valerie A and Vine, Daniel J , journal=. Oil, automobiles, and the. 2011 , publisher=

2011

-

[54]

and Zubairy, S

Ramey, V.A. and Zubairy, S. , title =. Journal of Political Economy , year =

-

[55]

and Romer, D.H

Romer, C.D. and Romer, D.H. , title =. American Economic Review , year =

-

[56]

and Goldman, M

Semenova, V. and Goldman, M. and Chernozhukov, V. and Taddy, M. , title =. Quantitative Economics , year =

-

[57]

, title =

Stock, J.H. , title =. Journal of the American Statistical Association , year =

-

[58]

and Thwaites, G

Tenreyro, S. and Thwaites, G. , title =. American Economic Journal: Macroeconomics , year =

-

[59]

and Yang, M.J

Wieland, J.F. and Yang, M.J. , title =. Journal of Money, Credit and Banking , year =

-

[60]

2026 , note =

Winkler, Valentin , title =. 2026 , note =

2026

-

[61]

Andrews, Donald W. K. , title =. Econometrica , year =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.