A Two-Stage Decision Support System for Sustainability-Aware Long Short Portfolio Optimization

Pith reviewed 2026-06-25 19:16 UTC · model grok-4.3

The pith

A two-stage system integrates ESG factors into long-short portfolio optimization and delivers competitive or superior performance.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that ESG-enhanced long-short portfolios constructed via the proposed two-stage process offer competitive and often superior performance compared to their non-ESG counterparts and the market-value-weighted benchmark.

What carries the argument

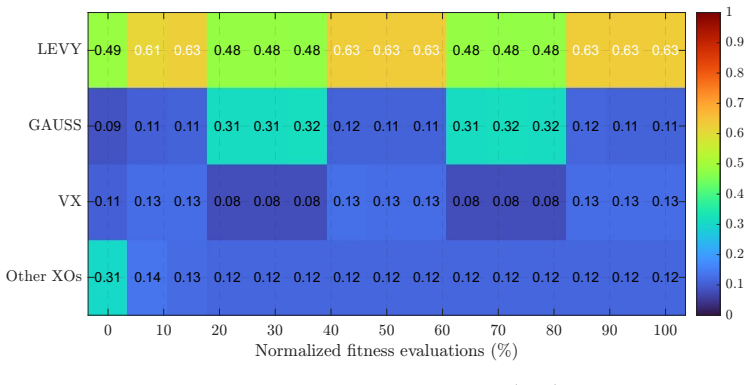

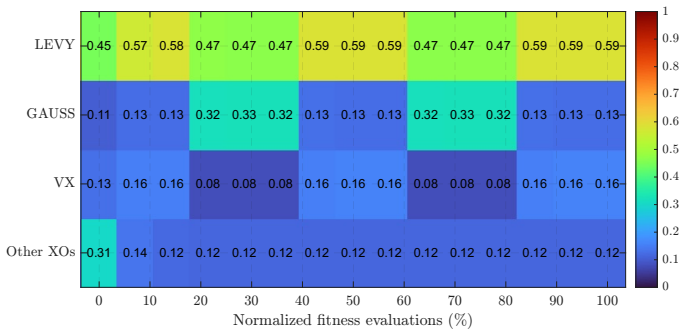

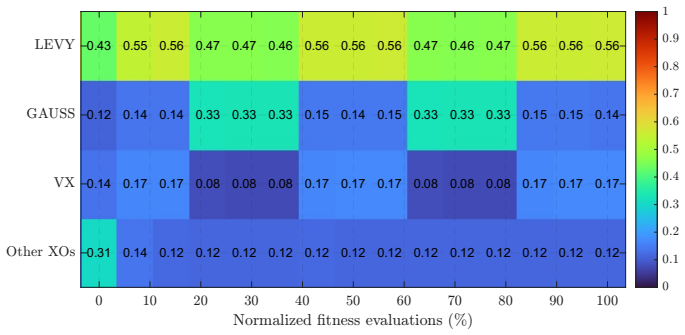

The TODIMSort multi-criteria classification procedure combined with an adaptive particle swarm optimization solver that selects recombination operators dynamically and applies projection-based constraint repair.

If this is right

- The classification step generates opportunity sets that adapt to prevailing market regimes and investor priorities.

- The optimization maximizes the Omega ratio while satisfying budget, bound, and leverage constraints.

- The adaptive solver improves upon standard particle swarm methods in exploration and solution quality.

- ESG integration does not detract from ex post profitability and can enhance it.

Where Pith is reading between the lines

- This framework could extend to other asset classes or regions to test generalizability of the performance advantage.

- Future work might incorporate predictive models to anticipate regime shifts before the classification step.

- The approach treats ESG as an active component in selection rather than a post-hoc filter.

Load-bearing premise

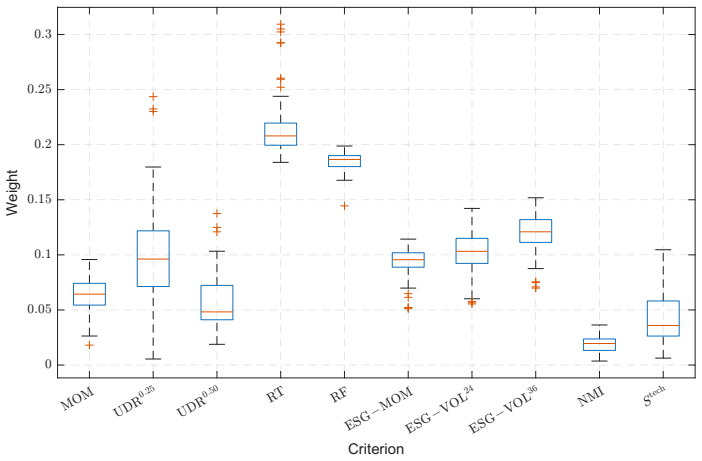

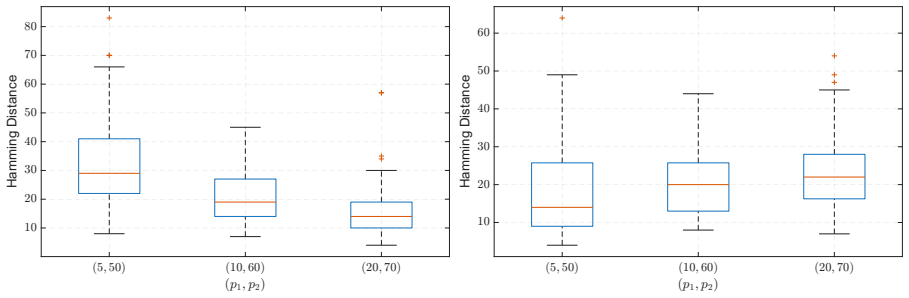

The multi-criteria classification step using TODIMSort with MEREC-derived weights produces sets of long and short opportunities that meaningfully adapt to market regimes and investor priorities.

What would settle it

Out-of-sample testing on a held-out period or different index where ESG portfolios underperform non-ESG versions and the benchmark on a consistent basis would falsify the performance advantage.

Figures

read the original abstract

This paper proposes a two-stage decision support system for long-short portfolio optimization under environmental, social, and governance (ESG) considerations. In the first stage, assets are evaluated using a multi-criteria procedure based on TODIMSort, with criterion weights derived using the MEREC (Removal Effects of Criteria) method. This allows assets to be assigned to classes ordered according to preferences that respond to market conditions and investor priorities, thus generating sets of long and short opportunities that dynamically adapt to the prevailing regime. In the second stage, we formulate a non-convex portfolio optimization problem that maximizes the Omega ratio while respecting budget, bound and leverage constraints. To solve it, we introduce an adaptive particle swarm solver equipped with a controller that selects, at each iteration, the most suitable recombination operator from a diverse pool of operators and combines it with a projection-based repair mechanism for constraint management. The empirical study, conducted on 421 stocks in the STOXX Europe 600 index, examines both the exploration capabilities and solution quality of the proposed solver compared to state-of-the-art benchmarks, as well as the ex post profitability of the resulting portfolio strategies. The results show that ESG-enhanced long-short portfolios offer competitive and often superior performance compared to their non-ESG counterparts and the market-value-weighted benchmark.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a two-stage decision support system for sustainability-aware long-short portfolio optimization. Stage 1 uses TODIMSort with MEREC-derived criterion weights to classify assets into ordered preference classes, generating regime-adaptive long and short opportunity sets. Stage 2 formulates and solves a non-convex Omega-ratio maximization problem subject to budget, bound, and leverage constraints via an adaptive particle-swarm optimizer that dynamically selects recombination operators and applies projection-based repair. The empirical component evaluates the solver on 421 STOXX Europe 600 stocks and reports that the resulting ESG-enhanced long-short portfolios are competitive with or superior to non-ESG counterparts and the market-value-weighted benchmark.

Significance. If the performance claims survive rigorous out-of-sample validation and statistical testing, the work would supply a concrete, preference-responsive framework for embedding ESG criteria into long-short construction. The adaptive PSO solver for non-convex Omega problems constitutes a reusable algorithmic contribution, and the combination of MEREC weighting with TODIMSort for dynamic classification extends multi-criteria decision-making techniques into portfolio applications.

major comments (2)

- [Abstract] Abstract (empirical study paragraph): the central claim that 'ESG-enhanced long-short portfolios offer competitive and often superior performance' rests on ex-post results for 421 stocks without reported error bars, rolling-window out-of-sample protocol, or any statistical significance tests; these omissions directly undermine assessment of whether the reported superiority is robust or merely an artifact of in-sample fitting.

- [Abstract] First-stage description: the assertion that TODIMSort/MEREC classification 'dynamically adapt[s] to the prevailing regime' is load-bearing for the two-stage advantage, yet the abstract supplies no concrete illustration of how the resulting long/short sets change across market conditions or investor priority vectors.

minor comments (1)

- The abstract would be clearer if it stated the exact back-test horizon, rebalancing frequency, and precise performance metrics (e.g., annualized return, Sharpe, maximum drawdown) used to support the superiority claim.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback. We address the major comments point-by-point below, agreeing that the abstract requires revision for greater precision and illustration while preserving the manuscript's core contributions.

read point-by-point responses

-

Referee: [Abstract] Abstract (empirical study paragraph): the central claim that 'ESG-enhanced long-short portfolios offer competitive and often superior performance' rests on ex-post results for 421 stocks without reported error bars, rolling-window out-of-sample protocol, or any statistical significance tests; these omissions directly undermine assessment of whether the reported superiority is robust or merely an artifact of in-sample fitting.

Authors: We acknowledge that the abstract does not explicitly reference error bars, a rolling-window out-of-sample protocol, or statistical significance tests. The full manuscript presents ex-post performance results on the 421 STOXX Europe 600 stocks with benchmark comparisons. To address the concern, we will revise the abstract to note that the reported performance is supported by the evaluation framework and statistical comparisons detailed in the empirical section. This clarification will be added without overstating the validation approach. revision: yes

-

Referee: [Abstract] First-stage description: the assertion that TODIMSort/MEREC classification 'dynamically adapt[s] to the prevailing regime' is load-bearing for the two-stage advantage, yet the abstract supplies no concrete illustration of how the resulting long/short sets change across market conditions or investor priority vectors.

Authors: The abstract's brevity limits detail on the first stage. The manuscript body describes how TODIMSort with MEREC-derived weights produces regime-adaptive classifications responsive to market conditions and investor priorities. We will revise the abstract to include a brief illustrative statement showing, for example, how long and short opportunity sets shift under varying ESG weight vectors, thereby highlighting the dynamic adaptation. revision: yes

Circularity Check

No significant circularity identified

full rationale

The paper describes a two-stage empirical method: TODIMSort + MEREC classification in stage 1 to generate long/short sets, followed by Omega-ratio maximization via adaptive PSO in stage 2. The central claim is ex-post performance superiority of ESG portfolios versus non-ESG and market benchmarks on 421 STOXX Europe 600 stocks. No equation or result reduces by construction to fitted inputs; performance is measured on held-out historical data after portfolio construction. No self-citation chain, self-definitional step, or ansatz smuggling is present in the provided description. The derivation is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Technical Analysis from A to Z: Covers Every Trading Tool from the Absolute Breadth Index to the Zig Zag

Achelis, S.B., 2000. Technical Analysis from A to Z: Covers Every Trading Tool from the Absolute Breadth Index to the Zig Zag. 2 ed., McGraw-Hill Professional, New York, NY

2000

-

[2]

The peer performance ratios of hedge funds

Ardia, D., Boudt, K., 2018. The peer performance ratios of hedge funds. Journal of Banking and Finance 87, 351–368

2018

-

[3]

Bollinger on Bollinger Bands

Bollinger, J.A., 2002. Bollinger on Bollinger Bands. McGraw-Hill, New York

2002

-

[4]

Real-coded evolutionary algorithms with parent-centric recombination, in: Proceedings of the IEEE International Congress on Evolutionary Compu- tation, Honolulu, USA

Deb, K., Joshi, D., Anand, A., 2002. Real-coded evolutionary algorithms with parent-centric recombination, in: Proceedings of the IEEE International Congress on Evolutionary Compu- tation, Honolulu, USA

2002

-

[5]

Particle swarm optimization with genetic recombination: a hybrid evolutionary algorithm

Duong, S., Konjo, H., Uezato, E., Yamamoto, T., 2010. Particle swarm optimization with genetic recombination: a hybrid evolutionary algorithm. Artificial Life and Robotics 15, 444–449. 12 Table 5: Pairwise comparisons in terms of variance differences between ESG, no-ESG, and benchmark portfolios under three limiting-profile configurations and leverage lev...

2010

-

[6]

Particle swarm optimization with discrete crossover, in: Proceedings of the IEEE International Congress on Evolutionary Computation, Cancun, Mexico

Engelbrecht, A.P., 2013. Particle swarm optimization with discrete crossover, in: Proceedings of the IEEE International Congress on Evolutionary Computation, Cancun, Mexico

2013

-

[7]

Particle swarm optimization with crossover: a review and empirical analysis

Engelbrecht, A.P., 2016. Particle swarm optimization with crossover: a review and empirical analysis. Artificial Intelligence Review 45, 131–165

2016

-

[8]

A novel hybrid particle swarm optimization based on Levy flight and wavelet mutation for global optimization

Gao, Y., Zhang, H., Duan, Y., Zhang, H., 2023. A novel hybrid particle swarm optimization based on Levy flight and wavelet mutation for global optimization. PLoS ONE 18, e0279572

2023

-

[9]

Particle swarm optimization with Gaussian mutation, in: Proceedings of the IEEE Swarm Intelligence Symposium, Indianapolis, USA

Higashi, N., Iba, H., 2003. Particle swarm optimization with Gaussian mutation, in: Proceedings of the IEEE Swarm Intelligence Symposium, Indianapolis, USA

2003

-

[10]

Trading Systems and Methods

Kaufman, P.J., 2013. Trading Systems and Methods. 5 ed., John Wiley and Sons, Hoboken, NJ

2013

-

[11]

Technical Analysis: The Complete Resource for Fi- nancial Market Technicians

Kirkpatrick, C.D., Dahlquist, J.R., 2010. Technical Analysis: The Complete Resource for Fi- nancial Market Technicians. FT Press, Upper Saddle River, NJ

2010

-

[12]

Robust performance hypothesis testing with the variance

Ledoit, O., Wolf, M., 2011. Robust performance hypothesis testing with the variance. Wilmott 55, 86–89. Løvberg, M., Rasmussen, T., Krink, T., 2001. Hybridparticleswarmoptimiserwithbreedingand subpopulations, in: Proceedings of the Genetic and Evolutionary Computation Conference, San Francisco, USA

2011

-

[13]

Information Theory, Inference, and Learning Algorithms

MacKay, D.J., 2003. Information Theory, Inference, and Learning Algorithms. Cambridge University Press. 13

2003

-

[14]

Accelerating particle swarm optimization using crisscross search

Meng, A., Li, Z., Chen, S., Guo, Z., 2016. Accelerating particle swarm optimization using crisscross search. Information Sciences 329, 52–72

2016

-

[15]

Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications

Murphy, J.J., 1999. Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance, New York

1999

-

[16]

Particle swarm optimization with a novel multi- parent crossover operator, in: Proceedings of the IEEE International Conference on Natural

Wang, W., Wu, Z., Liu, Y., Zeng, S., 2008. Particle swarm optimization with a novel multi- parent crossover operator, in: Proceedings of the IEEE International Conference on Natural

2008

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.