Multiscale Dynamic Dependence Estimation over Networks

Pith reviewed 2026-06-30 04:51 UTC · model grok-4.3

The pith

Net-LSW processes model multiscale time-varying dependencies on networks by embedding graph topology in the covariance of increments.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

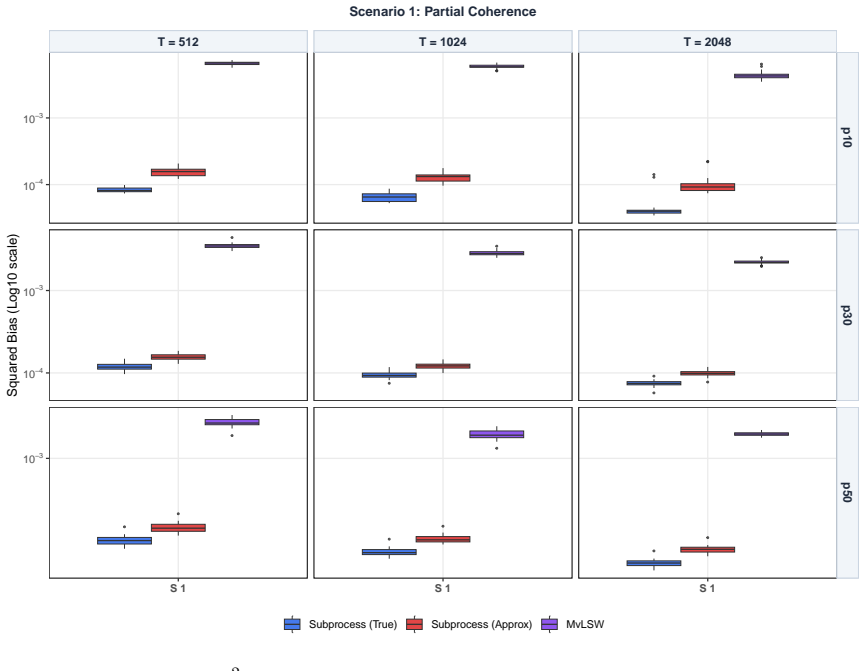

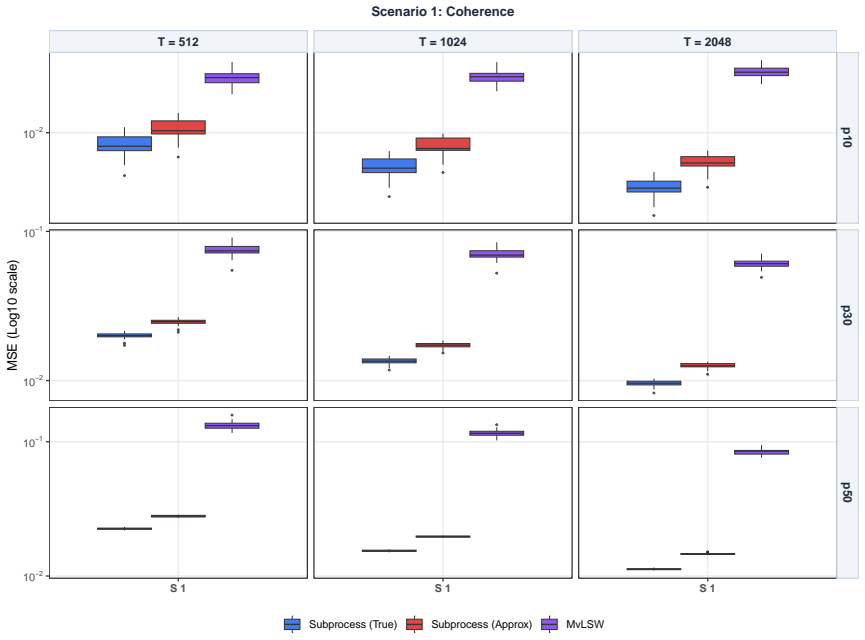

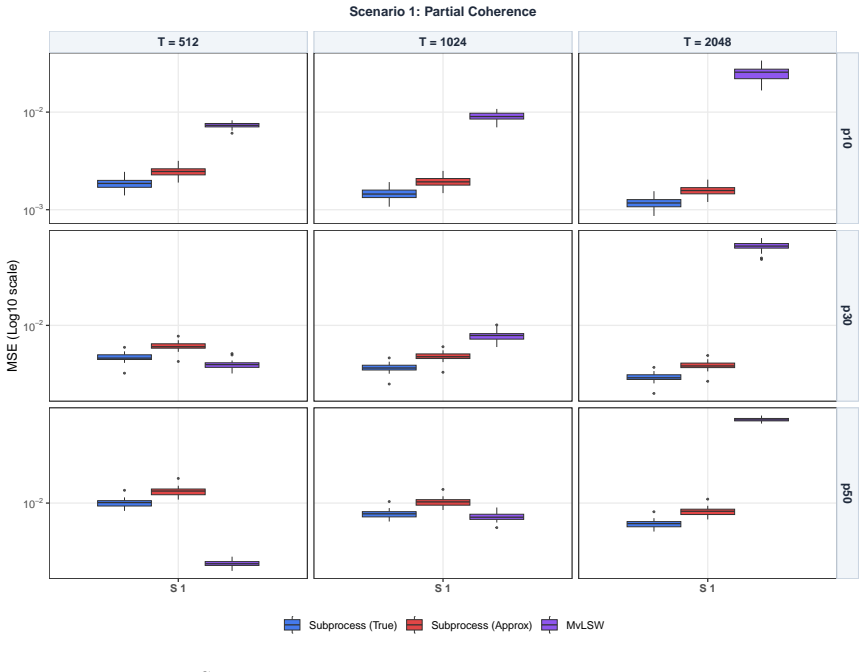

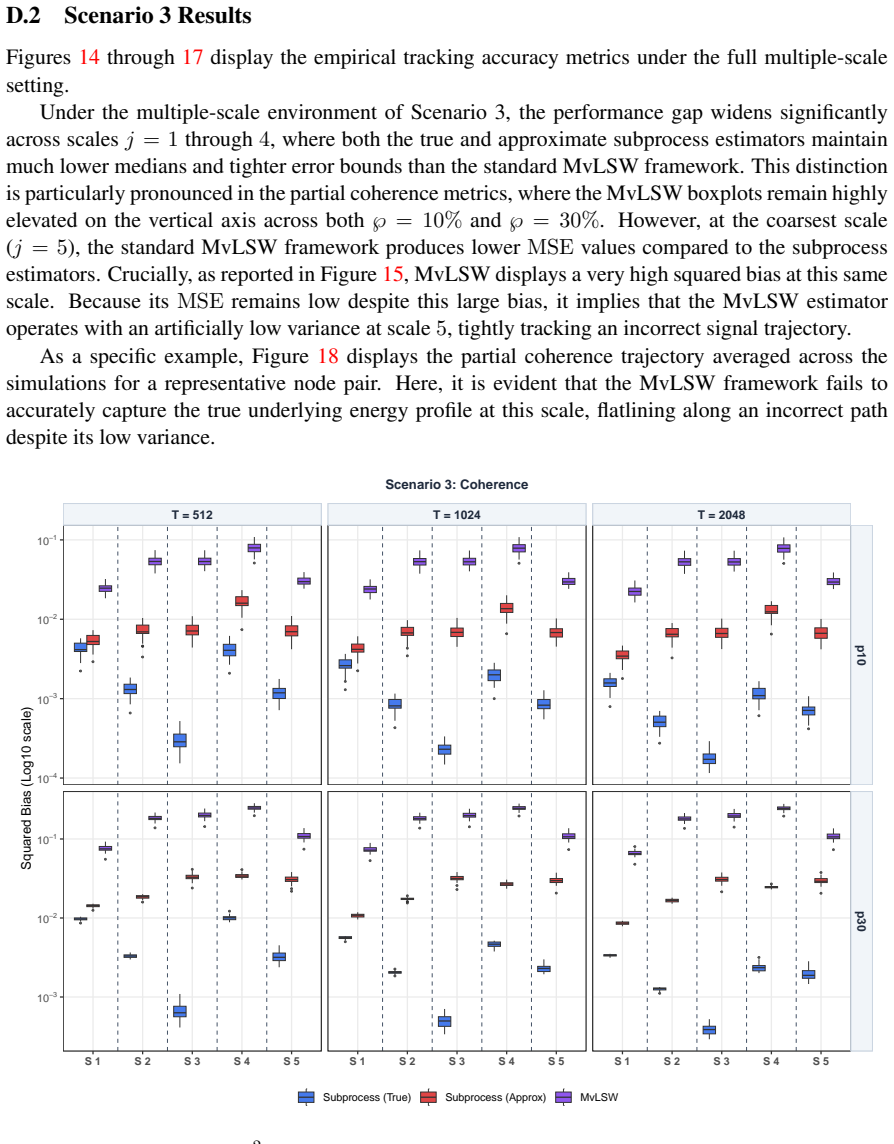

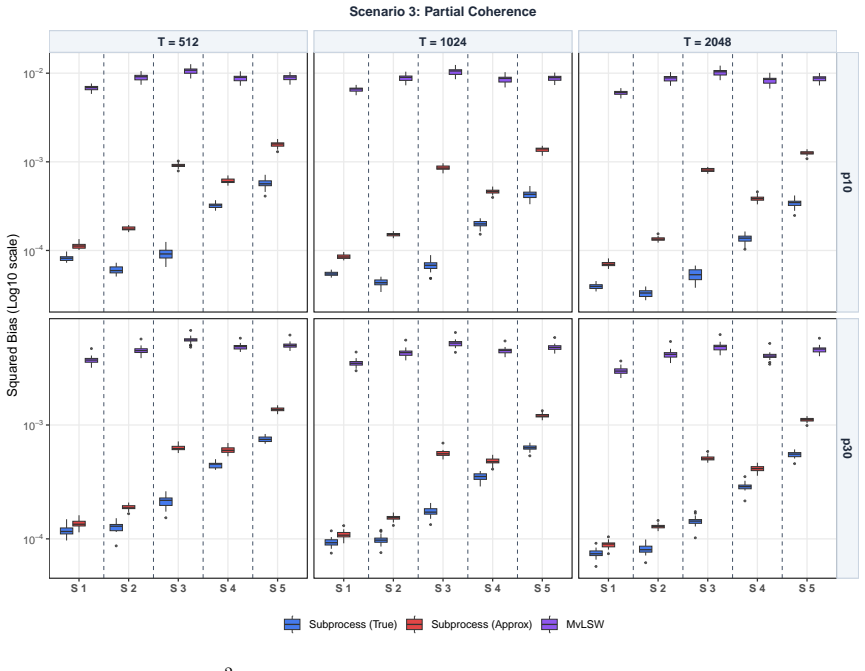

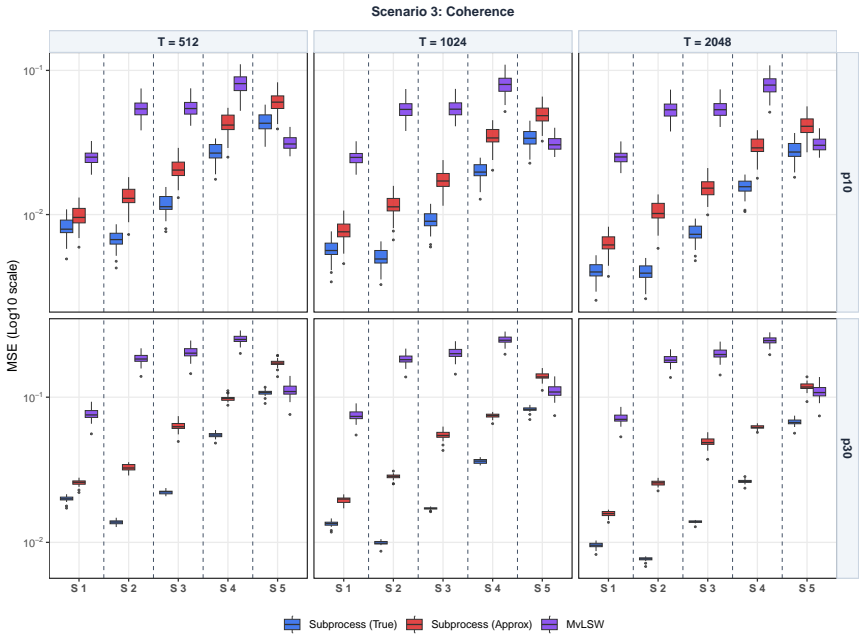

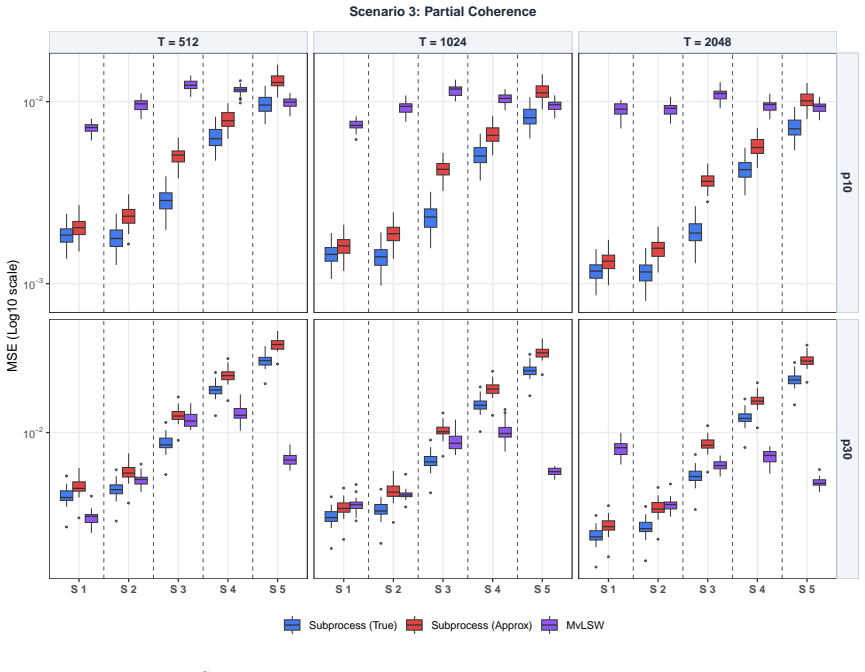

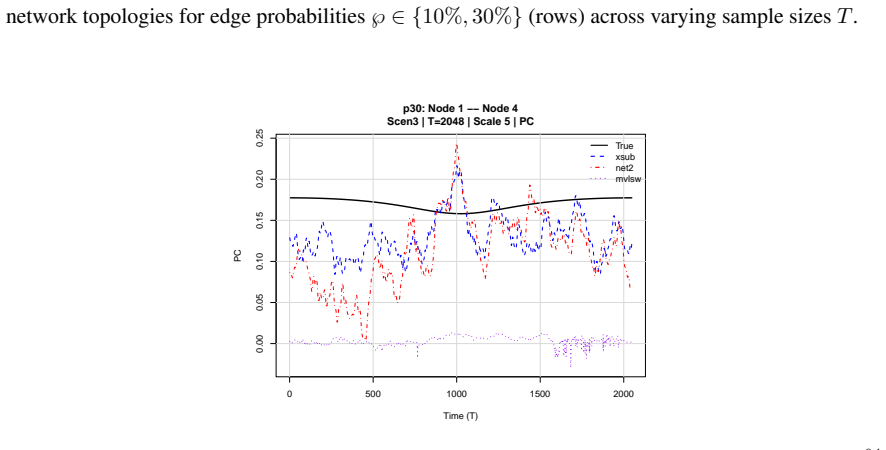

The Net-LSW framework extends locally stationary wavelet processes to networks by encoding the graph directly in the covariance structure of the process's random increments, allowing definition of the local partial correlation graph for time- and scale-dependent dependence structures, with a consistent subprocess-based estimator for inference.

What carries the argument

The Net-LSW process that encodes the graph directly in the covariance structure of the process's random increments, and the associated local partial correlation graph.

If this is right

- Consistent estimators exist for time- and scale-dependent local partial correlations under the model.

- Evolving dependence structures can be accurately recovered while respecting the underlying graph topology.

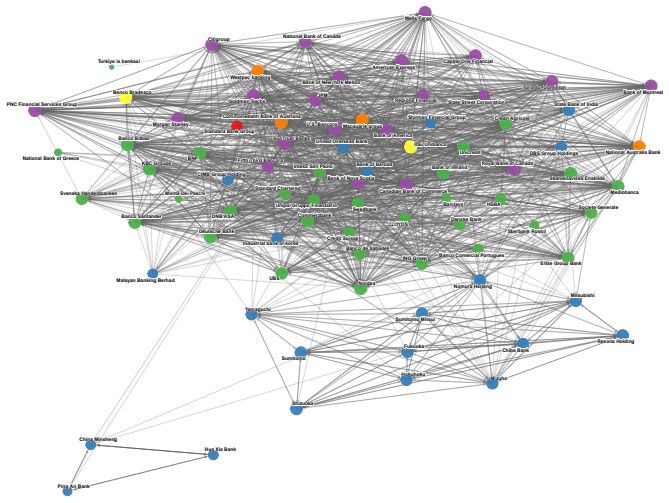

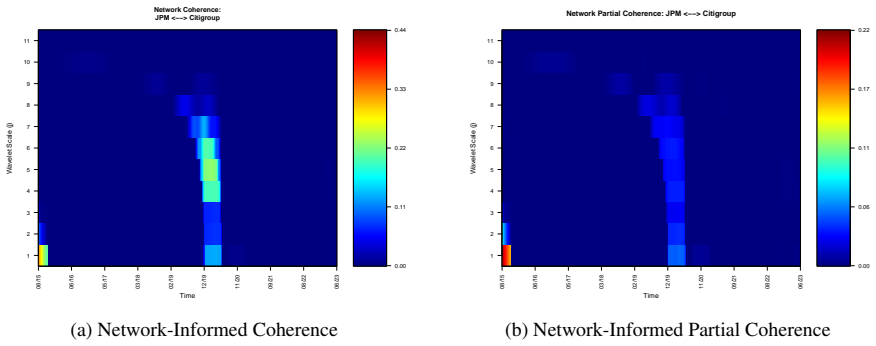

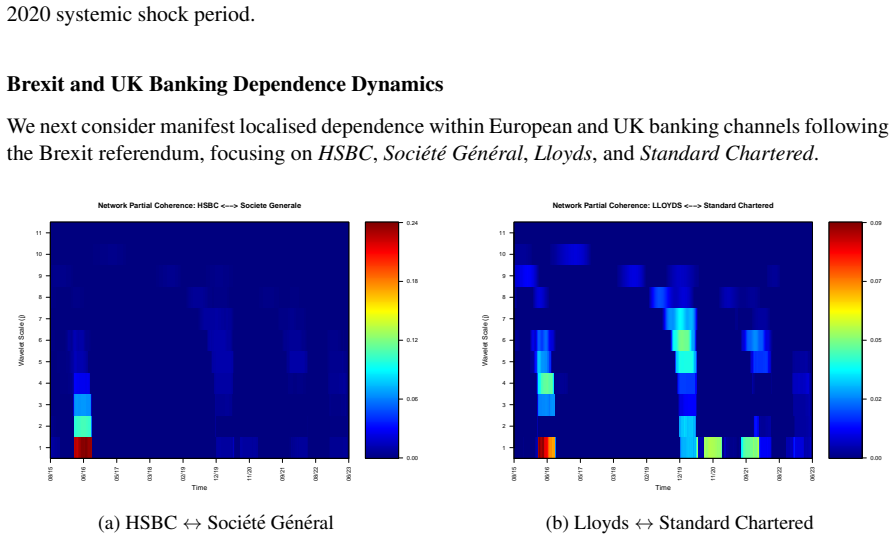

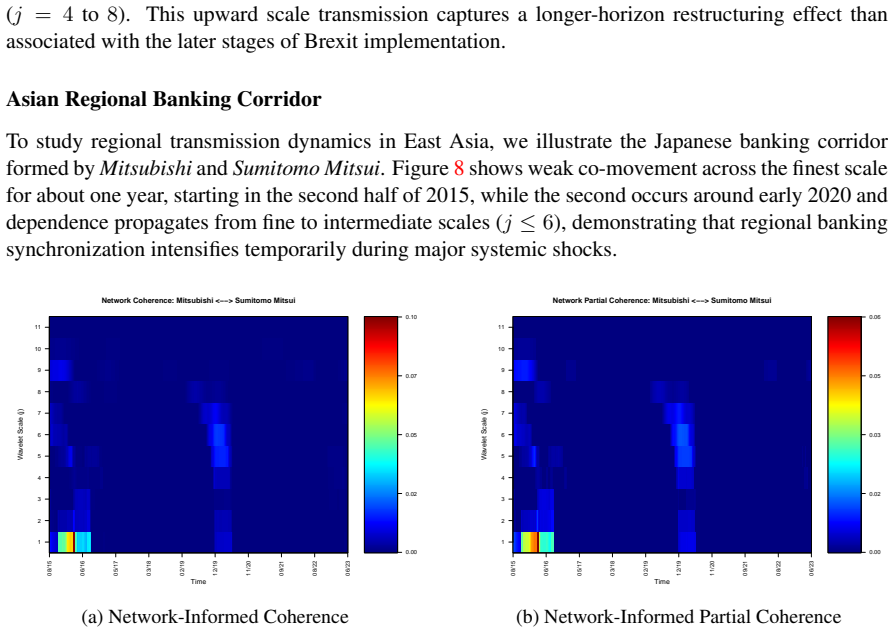

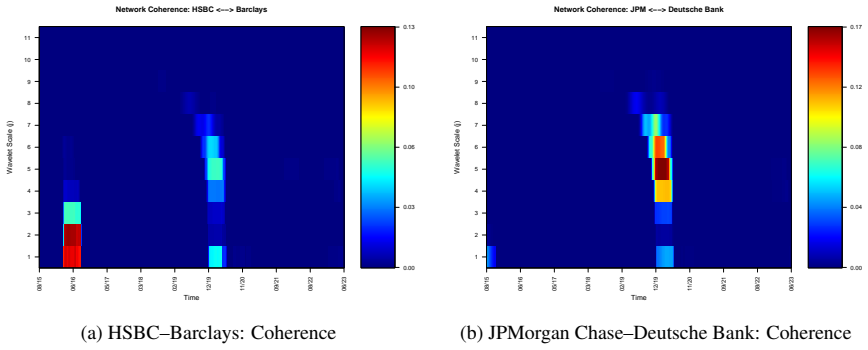

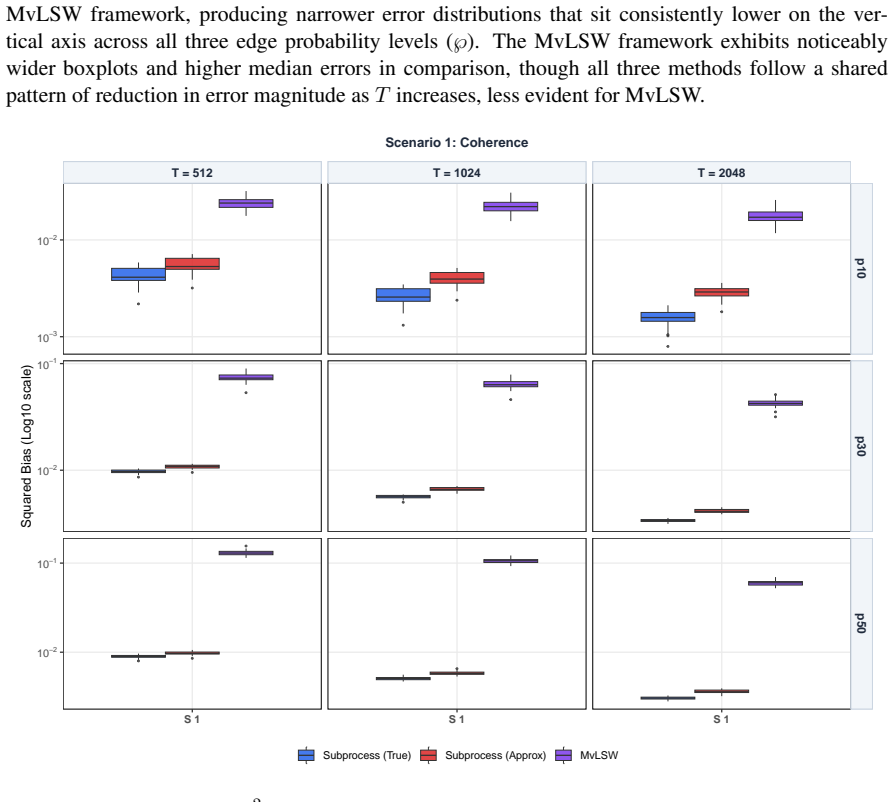

- Time-varying systemic shifts can be identified in applications such as global financial networks during shocks like Brexit and COVID-19.

- Multiscale analysis of nonstationary cross-dependencies structured by networks is enabled.

Where Pith is reading between the lines

- Similar methods could extend to other domains with networked time series, such as neural signals or traffic data.

- Forecasting performance might improve by using the estimated local partial correlations to inform predictions.

- The framework's consistency properties suggest it could handle larger networks if computational scalability is addressed.

Load-bearing premise

The subprocess-based estimation scheme yields consistent estimators for the time- and scale-dependent local partial correlations under the Net-LSW model.

What would settle it

Simulation results showing that the estimated local partial correlations do not match the known time- and scale-dependent structures in data generated from the Net-LSW model would falsify the consistency of the estimators.

Figures

read the original abstract

In numerous scientific and industrial settings, observed multivariate time series are often nonstationary in nature, i.e., comprise data whose second order properties vary over time. An additional feature of many modern datasets is that the cross-dependencies of such series are structured by an underlying network, giving rise to complex interactions between temporal dynamics and network topology. In this article we propose Locally Stationary Wavelet processes on Networks (Net-LSW), a new framework for modelling multiscale, time-varying dependencies that explicitly incorporates the network structure. Unlike traditional multivariate approaches, the Net-LSW process encodes the graph directly in the covariance structure of the process's random increments. We also introduce the concept of the local partial correlation graph, which connects edges in the graph to non-zero entries in the time- and scale-dependent dependence structure of a nonstationary process. For inference on the local cross-nodal (partial) dependence, we develop a novel subprocess-based estimation scheme and establish its desirable consistency properties. Simulation studies further demonstrate that the proposed framework accurately recovers evolving dependence structures whilst respecting the underlying graph topology. Finally, we apply our framework to daily stock price volatilities across a global bank network, demonstrating its ability to capture multiscale, highly nonstationary dependencies and identify time-varying systemic shifts during major financial shocks, including Brexit and the COVID-19 pandemic.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces the Net-LSW model, which extends locally stationary wavelet processes to multivariate time series whose second-order structure is constrained by an underlying network graph. It defines a local partial correlation graph that links graph edges to non-zero time- and scale-dependent partial correlations, develops a subprocess-based estimator for these quantities, establishes consistency of the estimator, demonstrates accurate recovery of evolving dependence structures in simulations, and applies the method to daily stock volatilities on a global bank network to identify multiscale shifts during Brexit and COVID-19.

Significance. If the consistency result holds under explicit conditions, the framework supplies a topology-respecting, multiscale approach to nonstationary network time series that is directly applicable to financial systemic-risk monitoring and similar domains. The simulation recovery of graph-structured dependence and the real-data identification of crisis-induced changes constitute concrete strengths; the absence of machine-checked proofs or fully reproducible code is noted but does not diminish the methodological contribution.

major comments (1)

- [Inference section] Inference section (description of subprocess estimator and consistency claim): the central consistency result for the time- and scale-dependent local partial correlations is asserted under the Net-LSW model, yet the precise assumptions on network-induced mixing rates in the wavelet increment covariances, admissible wavelet families, and the relative rate of non-stationarity versus graph diameter are not stated; these conditions are load-bearing because the model encodes topology only through second-order increment structure and the estimator extracts partial correlations from subprocesses.

Simulated Author's Rebuttal

We thank the referee for their detailed review and constructive feedback on our manuscript. We address the major comment below and will incorporate the necessary clarifications in a revised version.

read point-by-point responses

-

Referee: [Inference section] Inference section (description of subprocess estimator and consistency claim): the central consistency result for the time- and scale-dependent local partial correlations is asserted under the Net-LSW model, yet the precise assumptions on network-induced mixing rates in the wavelet increment covariances, admissible wavelet families, and the relative rate of non-stationarity versus graph diameter are not stated; these conditions are load-bearing because the model encodes topology only through second-order increment structure and the estimator extracts partial correlations from subprocesses.

Authors: We agree that the consistency theorem for the subprocess-based estimator of local partial correlations requires explicit statement of the supporting assumptions. In the revised manuscript we will add a dedicated subsection in the Inference section that lists: (i) the network-induced mixing conditions on the wavelet increment covariances (adapted from the Net-LSW second-order structure), (ii) the admissible wavelet families (Daubechies with sufficient vanishing moments), and (iii) the relative rate condition between the non-stationarity bandwidth and the graph diameter. These will be stated as Assumptions A1–A3 immediately preceding the consistency result, with a brief justification of why they are natural under the model. revision: yes

Circularity Check

No circularity: consistency claims rest on model assumptions, not self-definition or fitted inputs

full rationale

The abstract and description present the Net-LSW model as encoding graph structure in increment covariances, introduce local partial correlation graphs, and develop a subprocess estimator whose consistency properties are claimed to be established under the model. No quoted step reduces a prediction to a fitted parameter by construction, renames a known result, or relies on a load-bearing self-citation whose content is unverified within the paper. The derivation chain is presented as self-contained against the stated Net-LSW assumptions, which is the normal non-circular case.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

2005 , publisher=

Matrix Algebra , author=. 2005 , publisher=

2005

-

[2]

1999 , Address =

Convergence of Probability Measures , Author =. 1999 , Address =

1999

-

[3]

2016 , publisher=

Introduction to Time Series and Forecasting , author=. 2016 , publisher=

2016

-

[4]

The Annals of Statistics , volume=

A likelihood approximation for locally stationary processes , author=. The Annals of Statistics , volume=. 2000 , publisher=

2000

-

[5]

, title =

Dahlhaus, R. , title =. Time Series Analysis: Methods and Applications , publisher =. 2012 , volume =

2012

-

[6]

2009 , edition =

An Intermediate Course in Probability , author=. 2009 , edition =

2009

-

[7]

2009 , publisher=

The elements of statistical learning: data mining, inference, and prediction , author=. 2009 , publisher=

2009

-

[8]

Biometrika , number =

Isserlis, Leon , title =. Biometrika , number =

-

[9]

2026 , eprint=

Frequency-Domain Analysis of Time Series with Network-Structured Dependence: Application to Global Bank Connectedness , author=. 2026 , eprint=

2026

-

[10]

Electronic Journal of Statistics , volume=

The local partial autocorrelation function and some applications , author=. Electronic Journal of Statistics , volume=

-

[11]

Wavelet processes and adaptive estimation of the evolutionary wavelet spectrum , author=. J. Roy. Stat. Soc. B , volume=

-

[12]

Nason, G. P. , year=. Wavelet methods in statistics with

-

[13]

Nason, G. P. and Kovac, A. and Maechler, M. , title =

-

[14]

IEEE Transactions on Signal Processing , Year =

Estimating Time-Evolving Partial Coherence Between Signals via Multivariate Locally Stationary Wavelet Processes , Author =. IEEE Transactions on Signal Processing , Year =

-

[15]

Sanderson and P

J. Sanderson and P. Fryzlewicz and M. W. Jones , journal =. Estimating linear dependence between nonstationary time series using the locally stationary wavelet model , urldate =

-

[16]

Brillinger , title =

David R. Brillinger , title =

-

[17]

Knight and Matthew A

Marina I. Knight and Matthew A. Nunes and Jessica K. Hargreaves , title =. Journal of Computational and Graphical Statistics , volume =. 2024 , publisher =

2024

-

[18]

The Annals of Statistics , number =

Sumanta Basu and Suhasini Subba Rao , title =. The Annals of Statistics , number =. 2023 , doi =

2023

-

[19]

Graphical interaction models for multivariate time series

Dahlhaus, Rainer. Graphical interaction models for multivariate time series. Metrika

-

[20]

Biostatistics , volume =

Friedman, Jerome and Hastie, Trevor and Tibshirani, Robert , title =. Biostatistics , volume =

-

[21]

2026 , eprint=

Dynamic cross-scale wavelet coherence , author=. 2026 , eprint=

2026

-

[22]

Nason, G. P. and Silverman, B. W. , title =. Wavelets and Statistics , editor =. 1995 , publisher =

1995

-

[23]

and Sapatinas, Theofanis , title =

Abramovich, Felix and Bailey, Trevor C. and Sapatinas, Theofanis , title =. Journal of the Royal Statistical Society: Series D (The Statistician) , volume =. doi:https://doi.org/10.1111/1467-9884.00216 , url =. https://rss.onlinelibrary.wiley.com/doi/pdf/10.1111/1467-9884.00216 , year =

-

[24]

Convex Optimization in Signal Processing and Communications , editor =

Songsiri, Jitkomut and Dahl, Joachim and Vandenberghe, Lieven , title =. Convex Optimization in Signal Processing and Communications , editor =. 2009 , pages =

2009

-

[25]

Dahlhaus , title =

R. Dahlhaus , title =. The Annals of Statistics , number =. 1997 , doi =

1997

-

[26]

Bernoulli , number =

Rainer Dahlhaus and Stefan Richter and Wei Biao Wu , title =. Bernoulli , number =. 2019 , doi =

2019

-

[27]

Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =

Nason, G P , title =. Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =. 2013 , issn =. doi:10.1111/rssb.12015 , url =

-

[28]

Generalized impulse response analysis in linear multivariate models , journal =

H.Hashem Pesaran and Yongcheol Shin , keywords =. Generalized impulse response analysis in linear multivariate models , journal =. 1998 , issn =. doi:https://doi.org/10.1016/S0165-1765(97)00214-0 , url =

-

[29]

Jorge A. Connectedness in the global banking market network: Implications for risk management and financial policy , journal =. 2024 , issn =. doi:https://doi.org/10.1016/j.irfa.2024.103470 , url =

-

[30]

2025 , organization =

ConnectednessApproach: Connectedness Approach , author =. 2025 , organization =

2025

-

[31]

Management Science , volume =

Ando, Tomohiro and Greenwood-Nimmo, Matthew and Shin, Yongcheol , title =. Management Science , volume =. 2022 , doi =

2022

-

[32]

Model-free connectedness measures , journal =. 2023 , issn =. doi:https://doi.org/10.1016/j.frl.2023.103804 , url =

-

[33]

Dependency, centrality and dynamic networks for international commodity futures prices , journal =. 2020 , issn =. doi:https://doi.org/10.1016/j.iref.2020.01.004 , url =

-

[34]

Journal of Applied Econometrics , volume=

Estimating global bank network connectedness , author=. Journal of Applied Econometrics , volume=. 2018 , publisher=

2018

-

[35]

The Economic Journal , volume=

Measuring financial asset return and volatility spillovers, with application to global equity markets , author=. The Economic Journal , volume=. 2009 , publisher=

2009

-

[36]

Journal of Econometrics , volume=

On the network topology of variance decompositions: Measuring the connectedness of financial firms , author=. Journal of Econometrics , volume=. 2014 , publisher=

2014

-

[37]

Garman and Michael J

Mark B. Garman and Michael J. Klass , journal =. On the Estimation of Security Price Volatilities from Historical Data , urldate =

-

[38]

Journal of Financial Econometrics , volume=

Measuring the frequency dynamics of financial connectedness and systemic risk , author=. Journal of Financial Econometrics , volume=. 2018 , publisher=

2018

-

[39]

Journal of Financial Economics , volume=

Econometric measures of connectedness and systemic risk in the finance and insurance sectors , author=. Journal of Financial Economics , volume=. 2012 , publisher=

2012

-

[40]

2025 , eprint=

Decomposing Global Bank Network Connectedness: What is Common, Idiosyncratic and When? , author=. 2025 , eprint=

2025

-

[41]

A. P. Dempster , journal =. Covariance Selection , urldate =

-

[42]

1996 , publisher=

Graphical Models , author=. 1996 , publisher=

1996

-

[43]

Priestley, M. B. , title =. Journal of the Royal Statistical Society: Series B (Methodological) , volume =. doi:https://doi.org/10.1111/j.2517-6161.1965.tb01488.x , url =. https://rss.onlinelibrary.wiley.com/doi/pdf/10.1111/j.2517-6161.1965.tb01488.x , abstract =

-

[44]

A Time-Vertex Signal Processing Framework: Scalable Processing and Meaningful Representations for Time-Series on Graphs , year=

Grassi, Francesco and Loukas, Andreas and Perraudin, Nathanaël and Ricaud, Benjamin , journal=. A Time-Vertex Signal Processing Framework: Scalable Processing and Meaningful Representations for Time-Series on Graphs , year=

-

[45]

Stationary time-vertex signal processing

Loukas, Andreas and Perraudin, Nathana \"e l. Stationary time-vertex signal processing. EURASIP Journal on Advances in Signal Processing

-

[46]

2026 , eprint=

Uncertainty Principle for Vertex-Time Graph Signal Processing , author=. 2026 , eprint=

2026

-

[47]

and Xu, Shuwen , journal=

Jiang, Junzheng and Feng, Hairong and Tay, David B. and Xu, Shuwen , journal=. Theory and Design of Joint Time-Vertex Nonsubsampled Filter Banks , year=

-

[48]

Frequency analysis of time-varying graph signals , year=

Loukas, Andreas and Foucard, Damien , booktitle=. Frequency analysis of time-varying graph signals , year=

-

[49]

2016 , eprint=

Modelling, Detrending and Decorrelation of Network Time Series , author=. 2016 , eprint=

2016

-

[50]

and Leeming, Kathryn and Nason, Guy P

Knight, Marina I. and Leeming, Kathryn and Nason, Guy P. and Nunes, Matthew A. , year=. Generalized Network Autoregressive Processes and the. doi:10.18637/jss.v096.i05 , journal=

-

[51]

Technometrics , volume =

Hang Yin and Abolfazl Safikhani and George Michailidis , title =. Technometrics , volume =. 2023 , publisher =

2023

-

[52]

Estimating time-varying networks for high-dimensional time series , journal =

Jia Chen and Degui Li and Yu-Ning Li and Oliver Linton , keywords =. Estimating time-varying networks for high-dimensional time series , journal =. 2025 , issn =. doi:https://doi.org/10.1016/j.jeconom.2024.105941 , url =

-

[53]

The Annals of Statistics , volume =

Estimation of Grouped Time-Varying Network Vector Autoregressive Models , author =. The Annals of Statistics , volume =. 2026 , publisher =

2026

-

[54]

Xuening Zhu and Ganggang Xu and Jianqing Fan , keywords =. Simultaneous estimation and group identification for network vector autoregressive model with heterogeneous nodes , journal =. 2025 , issn =. doi:https://doi.org/10.1016/j.jeconom.2023.105564 , url =

-

[55]

Journal of Time Series Analysis , volume=

Trend locally stationary wavelet processes , author=. Journal of Time Series Analysis , volume=. 2022 , publisher=

2022

-

[56]

Electronic Journal of Statistics , volume=

Modelling time-varying first and second-order structure of time series via wavelets and differencing , author=. Electronic Journal of Statistics , volume=. 2022 , publisher=

2022

-

[57]

PLoS Computational Biology , volume =

Achard, Sophie and Bullmore, Ed , title =. PLoS Computational Biology , volume =. 2007 , doi =

2007

-

[58]

The Annals of Applied Statistics , volume =

Fiecas, Mark and Ombao, Hernando , title =. The Annals of Applied Statistics , volume =. 2011 , month =

2011

-

[59]

2025 , eprint=

Conditionally specified graphical modeling of stationary multivariate time series , author=. 2025 , eprint=

2025

-

[60]

Bernoulli , number =

Jonas Krampe and Suhasini Subba Rao , title =. Bernoulli , number =. 2024 , doi =

2024

-

[61]

Biometrika , volume =

Palasciano, H A and Knight, M I and Nason, G P , title =. Biometrika , volume =. 2025 , issn =

2025

-

[62]

Journal of Statistical Software , author=

Multivariate Locally Stationary Wavelet Analysis with the mvLSW R Package , volume=. Journal of Statistical Software , author=. 2019 , pages=. doi:10.18637/jss.v090.i11 , abstract=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.