Signature-Based Optimal Execution for Statistical Arbitrage with Path-Dependent Trading Signals

Pith reviewed 2026-07-01 02:58 UTC · model grok-4.3

The pith

Signature-linear trading speeds turn path-dependent execution into a finite-dimensional concave quadratic program.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Within the class of signature-linear trading speeds, the restricted path-dependent execution problem becomes a finite-dimensional concave quadratic programme in the policy coefficients.

What carries the argument

The quadratic reduction theorem that converts the signature-linear policy class into a concave quadratic program.

If this is right

- The execution problem becomes solvable with standard quadratic programming solvers.

- The same workflow applies directly to mean-reverting spread models and to historical equity pairs trading.

- Fitted policies achieve higher return on turnover than z-score benchmarks while enforcing dollar neutrality.

- Signal generation and execution share the same truncated signature basis.

Where Pith is reading between the lines

- The truncation level of the signature trades off expressivity against the dimension of the resulting quadratic program.

- Real-time implementation would require streaming signature computations that keep pace with market data.

- The reduction may extend to multi-asset portfolios by enlarging the signature feature space.

- Signature-linear policies could serve as a common language for comparing execution rules across different predictive signals.

Load-bearing premise

Both the alpha process and the trading speed can be adequately represented as linear functionals of the truncated signature of the time-augmented market path.

What would settle it

A simulation or backtest in which the optimal signature-linear policy fails to outperform the z-score benchmark or the quadratic program does not recover the claimed optimum.

Figures

read the original abstract

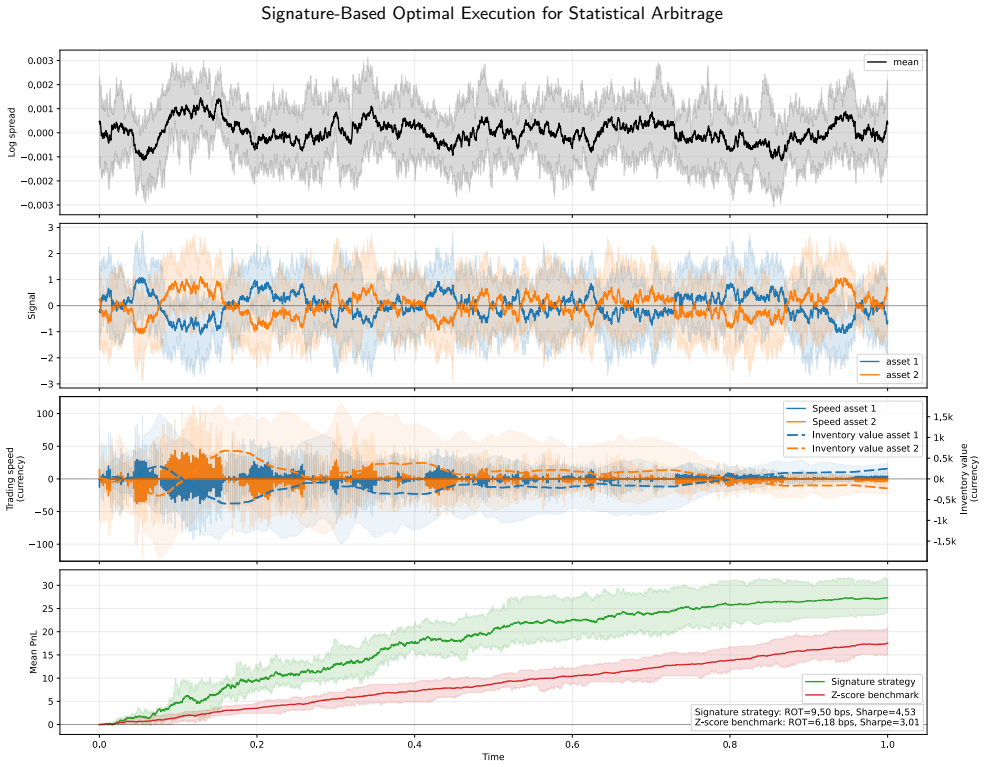

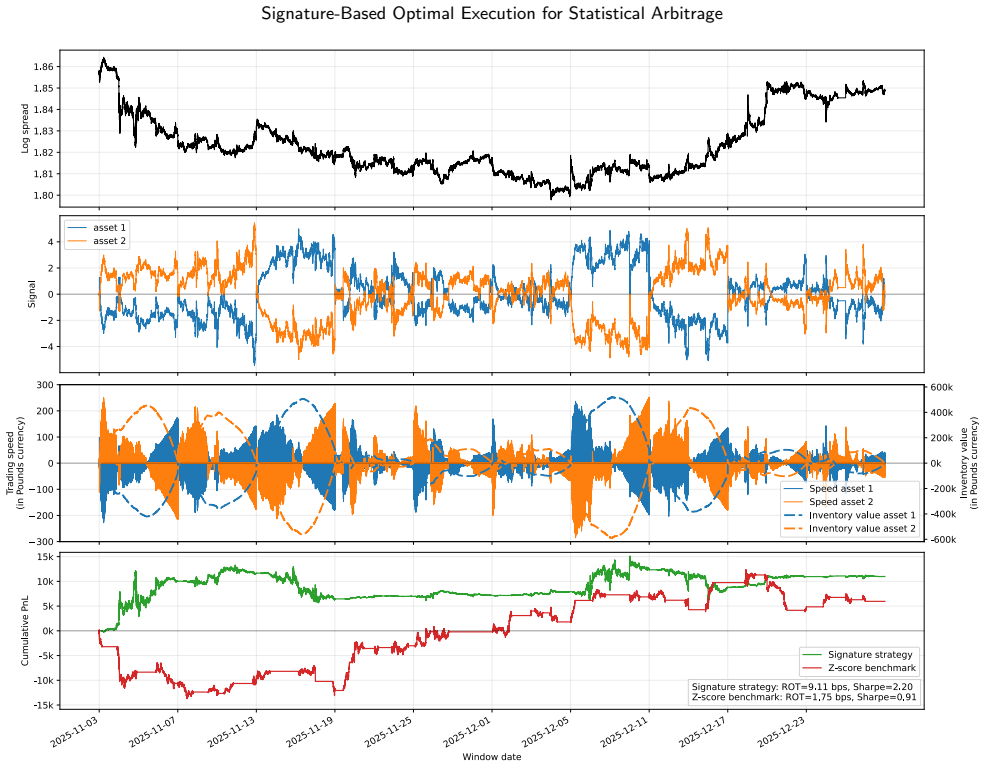

We develop a signature-based framework for optimal execution in statistical arbitrage strategies with path-dependent predictive signals. Both the alpha process and the trading speed are modelled as linear functionals of the truncated signature of a time-augmented market path, placing signal generation and execution on the same truncated signature basis. This allows the trading rule to react to the realised history of the signal while accounting for temporary impact, inventory exposure, terminal liquidation, and approximate dollar neutrality The main contribution is a quadratic reduction theorem: within the class of signature-linear trading speeds, the restricted path-dependent execution problem becomes a finite-dimensional concave quadratic programme in the policy coefficients. After running synthetic experiments under a mean-reverting log-spread model, we find that the fitted policy achieves a higher return on turnover than a z-score classical threshold benchmark. We shows how the same workflow can be deployed on a historical equity pairs-trading backtest, where the fitted signature policy again outperforms the benchmark in accounting terms.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a signature-based framework for optimal execution in statistical arbitrage with path-dependent predictive signals. Both the alpha process and trading speeds are represented as linear functionals of the truncated signature of a time-augmented market path. The central result is a quadratic reduction theorem showing that, within this signature-linear class, the execution problem (incorporating temporary impact, inventory, terminal liquidation, and approximate dollar neutrality) reduces to a finite-dimensional concave quadratic program over the policy coefficients. Synthetic experiments under a mean-reverting log-spread model and one equity pairs-trading backtest report that the fitted signature policy outperforms a classical z-score threshold benchmark in return-on-turnover and accounting metrics.

Significance. If the quadratic reduction theorem is correct and the signature-linear class is sufficiently expressive, the approach supplies a computationally tractable route to optimize genuinely path-dependent execution rules while remaining inside a concave quadratic program. This could usefully connect rough-path signature methods to practical stat-arb execution, especially when signals exhibit memory. The reported outperformance in the mean-reverting synthetic setting is consistent with low-order signatures capturing the dynamics, but broader applicability hinges on the class being dense enough for the true optimum.

major comments (3)

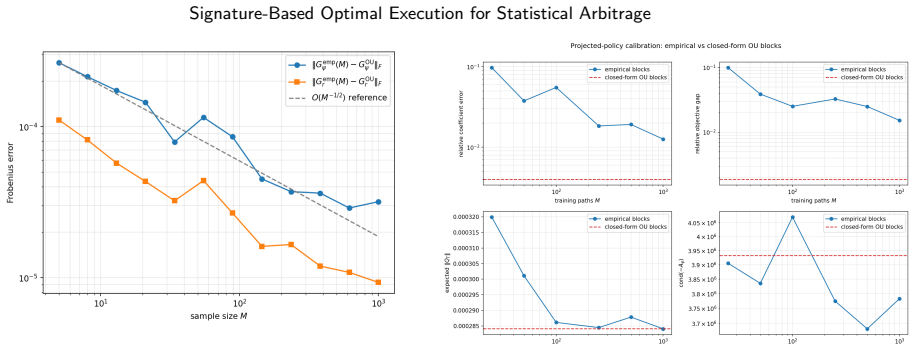

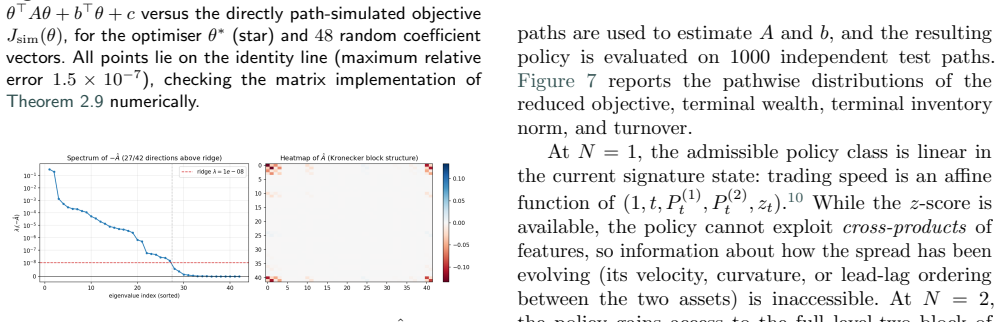

- [Section stating the quadratic reduction theorem] The quadratic reduction theorem is the load-bearing mathematical claim. The manuscript must supply a self-contained derivation (or at least the key steps establishing concavity and finite-dimensionality) rather than merely asserting the result; without it, the reduction from the infinite-dimensional path-dependent problem to the QP cannot be verified.

- [Synthetic experiments and backtest sections] The empirical claim that the signature-linear class captures relevant dynamics rests on outperformance versus a z-score benchmark in a mean-reverting log-spread model and a single equity backtest. No truncation-level sensitivity, no comparison against richer (non-linear or non-signature) policy classes, and no argument that the linear functional form can represent the optimal feedback law under impact and inventory penalties are provided; these omissions make the practical relevance of the restricted class untested.

- [Fitting and evaluation procedure] Policy coefficients are fitted directly to the same objective function later used to evaluate performance. This introduces dependence between the reported gains and the in-sample optimization procedure; out-of-sample or cross-validated evaluation would be required to substantiate generalization.

minor comments (2)

- [Abstract] Abstract contains the grammatical error 'We shows'.

- [Model setup] Notation for the time-augmented path and the precise truncation level should be stated once at the beginning and used consistently.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed report. We address each major comment below, indicating where revisions will be made to strengthen the manuscript.

read point-by-point responses

-

Referee: [Section stating the quadratic reduction theorem] The quadratic reduction theorem is the load-bearing mathematical claim. The manuscript must supply a self-contained derivation (or at least the key steps establishing concavity and finite-dimensionality) rather than merely asserting the result; without it, the reduction from the infinite-dimensional path-dependent problem to the QP cannot be verified.

Authors: We agree that a self-contained derivation is necessary for verifiability. In the revised manuscript we will insert a dedicated subsection containing the full proof of the quadratic reduction theorem. The proof will explicitly derive the finite-dimensional quadratic objective in the signature coefficients, confirm its concavity under the stated impact and penalty terms, and detail the steps that map the path-dependent execution problem onto the finite-dimensional QP. revision: yes

-

Referee: [Synthetic experiments and backtest sections] The empirical claim that the signature-linear class captures relevant dynamics rests on outperformance versus a z-score benchmark in a mean-reverting log-spread model and a single equity backtest. No truncation-level sensitivity, no comparison against richer (non-linear or non-signature) policy classes, and no argument that the linear functional form can represent the optimal feedback law under impact and inventory penalties are provided; these omissions make the practical relevance of the restricted class untested.

Authors: The experiments illustrate the workflow and the practical advantage of the reduction theorem rather than claim that the signature-linear class is universally optimal. We will add truncation-level sensitivity plots for both the synthetic and backtest settings. Direct comparisons with non-linear policy classes lie outside the paper’s scope, which focuses on tractable optimization inside the signature-linear family; we will clarify this motivation and note the universal-approximation property of signatures as the theoretical justification for the functional form. We acknowledge that an explicit argument showing the linear class can recover the true optimum under impact and inventory penalties is absent and will discuss this limitation in the revised text. revision: partial

-

Referee: [Fitting and evaluation procedure] Policy coefficients are fitted directly to the same objective function later used to evaluate performance. This introduces dependence between the reported gains and the in-sample optimization procedure; out-of-sample or cross-validated evaluation would be required to substantiate generalization.

Authors: We accept that the current evaluation is performed in-sample. For the synthetic experiments the data-generating process is known, so the optimization recovers the best policy inside the class for that exact model; we will state this explicitly. For the equity backtest we will implement a rolling-window or cross-validated evaluation procedure in the revision to provide evidence of out-of-sample performance. revision: yes

Circularity Check

No circularity: mathematical reduction is self-contained within explicitly restricted policy class; empirical results are direct comparisons to external benchmark.

full rationale

The core contribution is a quadratic reduction theorem that converts the execution problem into a concave QP strictly inside the signature-linear policy class; this is a finite-dimensional algebraic identity given the modeling ansatz and does not rely on data fitting or self-citation. The paper states the modeling choice (alpha and speed as linear signature functionals) upfront rather than smuggling it via prior work. Empirical sections report the performance of the QP solution versus a z-score threshold benchmark on both synthetic mean-reverting paths and a historical pairs backtest; these are standard out-of-class comparisons, not predictions of quantities already used as fitting targets. No load-bearing self-citation, no uniqueness theorem imported from the same authors, and no renaming of known results appear in the provided text. The derivation chain therefore remains independent of its own fitted outputs.

Axiom & Free-Parameter Ledger

free parameters (2)

- signature truncation level

- policy coefficients

axioms (1)

- standard math The signature transform provides a faithful linear representation of path-dependent functionals up to the chosen truncation.

Reference graph

Works this paper leans on

-

[1]

E. Gatev, W. N. Goetzmann, K. G. Rouwenhorst, Pairs trading: Performance of a relative-value arbitrage rule, The Review of Financial Studies 19 (3) (2006) 797–827. doi:10.1093/rfs/hhj020

-

[2]

M. Avellaneda, J.-H. Lee, Statistical arbitrage in the US equities market, Quantitative Finance 10 (7) (2010) 761–782. doi:10.1080/14697680903124632

-

[3]

R. Almgren, N. Chriss, Optimal execution of portfolio transactions, Journal of Risk 3 (2) (2000) 5–39. doi: 10.21314/JOR.2001.041

-

[4]

Cartea, S

´A. Cartea, S. Jaimungal, J. Penalva, Algorithmic and High- Frequency Trading, Cambridge University Press, 2015

2015

-

[5]

C. Lorenz, A. Schied, Drift dependence of optimal trade execution strategies under transient price impact, Finance and Stochastics 17 (4) (2013) 743–770. doi:10.1007/s00780- 013-0211-x

-

[6]

G. Curato, J. Gatheral, F. Lillo, Optimal execution with non-linear transient market impact, Quantitative Finance 17 (1) (2017) 41–54.doi:10.1080/14697688.2016.1181274

-

[7]

P. N. Kolm, J. Turiel, N. Westray, Deep order flow imbalance: Extracting alpha at multiple horizons from the limit order book, Mathematical Finance 33 (4) (2023) 1044–1081. doi: 10.1111/mafi.12413

-

[8]

L. G. Gyurk´ o, T. Lyons, M. Kontkowski, J. Field, Extracting information from the signature of a financial data stream, arXiv preprint arXiv:1307.7244arXiv:1307.7244

-

[9]

J. Kalsi, T. Lyons, I. Perez Arribas, Optimal execution with rough path signatures, SIAM Journal on Financial Mathe- matics 11 (2) (2020) 470–493.doi:10.1137/19M1259778

-

[10]

´A. Cartea, I. Perez Arribas, L. S´ anchez-Betancourt, Double- execution strategies using path signatures, SIAM Journal on Financial Mathematics 13 (4) (2022) 1379–1417. doi: 10.1137/21M1456467

- [11]

-

[12]

H. Buehler, B. Horvath, T. Lyons, I. Perez Arribas, B. Wood, Generating financial markets with signatures, SSRN Elec- tronic Journaldoi:10.2139/ssrn.3657366

-

[13]

Kidger, J

P. Kidger, J. Morrill, J. Foster, T. Lyons, Neural controlled differential equations for irregular time series, in: Advances in Neural Information Processing Systems, Vol. 33, 2020, pp. 6696–6707. URL https://proceedings.neurips.cc/paper_files/ paper/2020/file/4a5876b450b45371f6cfe5047ac8cd45- Paper.pdf

2020

-

[14]

Bonnier, P

P. Bonnier, P. Kidger, I. P. Arribas, C. Salvi, T. Lyons, Deep signature transforms, Curran Associates Inc., Red Hook, NY, USA, 2019

2019

-

[15]

C.-I. Lu, J. Sester, Generative model for financial time series trained with mmd using a signature kernel, arXiv preprint arXiv:2407.19848arXiv:2407.19848

- [16]

-

[17]

T. J. Lyons, M. Caruana, T. L´ evy, Differential Equations Driven by Rough Paths, Vol. 1908 of Lecture Notes in Mathematics, Springer, 2007. doi:10.1007/978-3-540- 71285-5

-

[18]

Lyons, Differential equations driven by rough signals, Revista Matem´ atica Iberoamericana 14 (2) (1998) 215–310

T. Lyons, Differential equations driven by rough signals, Revista Matem´ atica Iberoamericana 14 (2) (1998) 215–310

1998

-

[19]

I. Chevyrev, A. Kormilitzin, A Primer on the Signature Method in Machine Learning, Springer Nature Switzerland, 2025, p. 3–64.doi:10.1007/978-3-031-97239-3_1. URLhttp://dx.doi.org/10.1007/978-3-031-97239-3_1

-

[20]

D. Levin, T. Lyons, H. Ni, Learning from the past, predicting the statistics for the future, learning an evolving system, arXiv preprint arXiv:1309.0260arXiv:1309.0260

-

[21]

A. Fermanian, Embedding and learning with signatures, Computational Statistics & Data Analysis 157 (2021) 107148. doi:10.1016/j.csda.2020.107148

-

[22]

C. Krauss, Statistical arbitrage pairs trading strategies: Review and outlook, Journal of Economic Surveys 31 (2) (2017) 513–545.doi:10.1111/joes.12153

-

[23]

J. F. Caldeira, G. V. Moura, Selection of a portfolio of pairs based on cointegration: A statistical arbitrage strategy, SSRN Electronic Journaldoi:10.2139/ssrn.2196391

-

[24]

Z. Guo, H. Jin, J. Kuang, Z. Qian, J. Wang, Signature decomposition method applying to pair trading, Journal of Futures Markets 46 (3) (2026) 582–603. doi:https: //doi.org/10.1002/fut.70075

-

[25]

Cuchiero, P

C. Cuchiero, P. Schmocker, J. Teichmann, Global universal approximation of functional input maps on weighted spaces, Constr. Approx. 63 (2) (2026) 537–612. doi:10.1007/ s00365-025-09726-3

2026

-

[26]

Vidyamurthy, Pairs Trading: Quantitative Methods and Analysis, John Wiley & Sons, 2004

G. Vidyamurthy, Pairs Trading: Quantitative Methods and Analysis, John Wiley & Sons, 2004

2004

-

[27]

J. Sirignano, R. Cont, Universal features of price formation in financial markets: Perspectives from deep learning, Quan- titative Finance 19 (9) (2019) 1449–1459. doi:10.1080/ 14697688.2019.1622295

arXiv 2019

-

[28]

Z T 0 B, S0,t(Z) dt−γ DX i F i 2 , S 0,T (Z) E# =E

R. J. Elliott, J. van der Hoek, W. P. Malcolm, Pairs trading, Quantitative Finance 5 (3) (2005) 271–276. doi: 10.1080/14697680500149370. correspondence:g.morbelli@uva.nlPage 12 of 21 Signature-Based Optimal Execution for Statistical Arbitrage A. Explicit Tensor Computation This appendix provides detailed algebraic expansion underlying the proof of Theorem...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.