Design-Based Inference for Time-Series GMM

Pith reviewed 2026-07-01 02:28 UTC · model grok-4.3

The pith

For locally correctly specified time-series GMM, conventional HAC estimators converge to a larger variance than the design-based one and are therefore conservative for the finite-history estimand.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

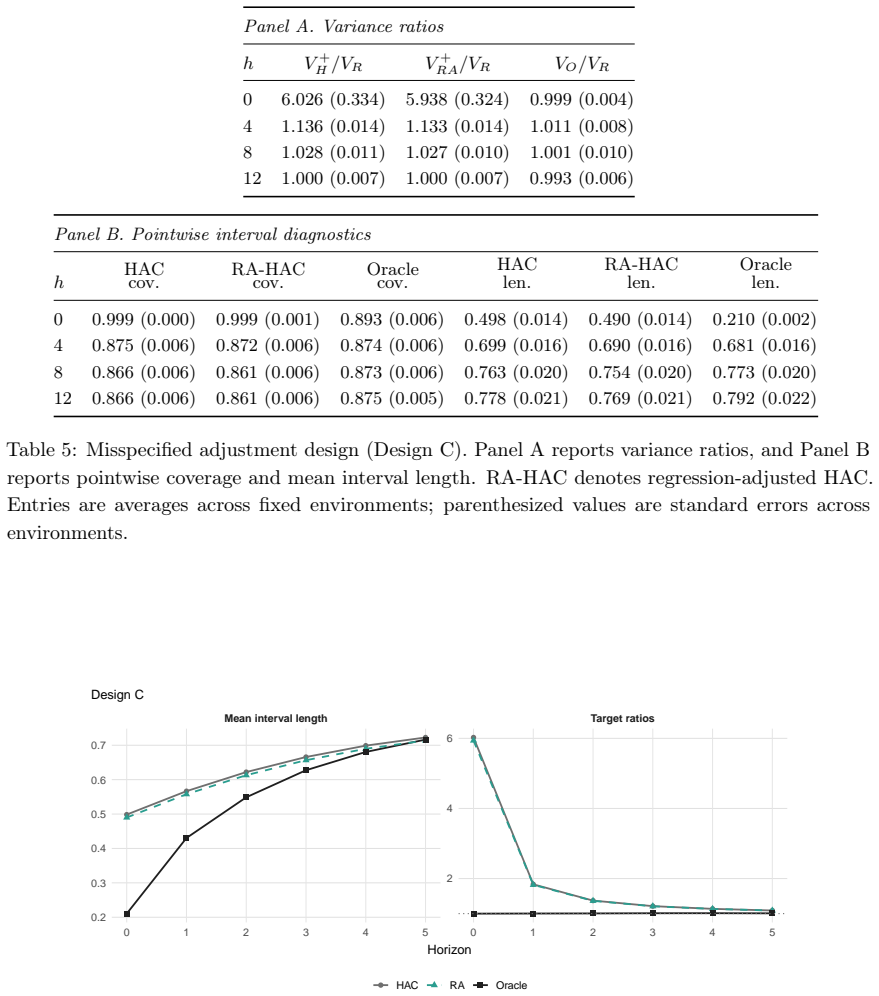

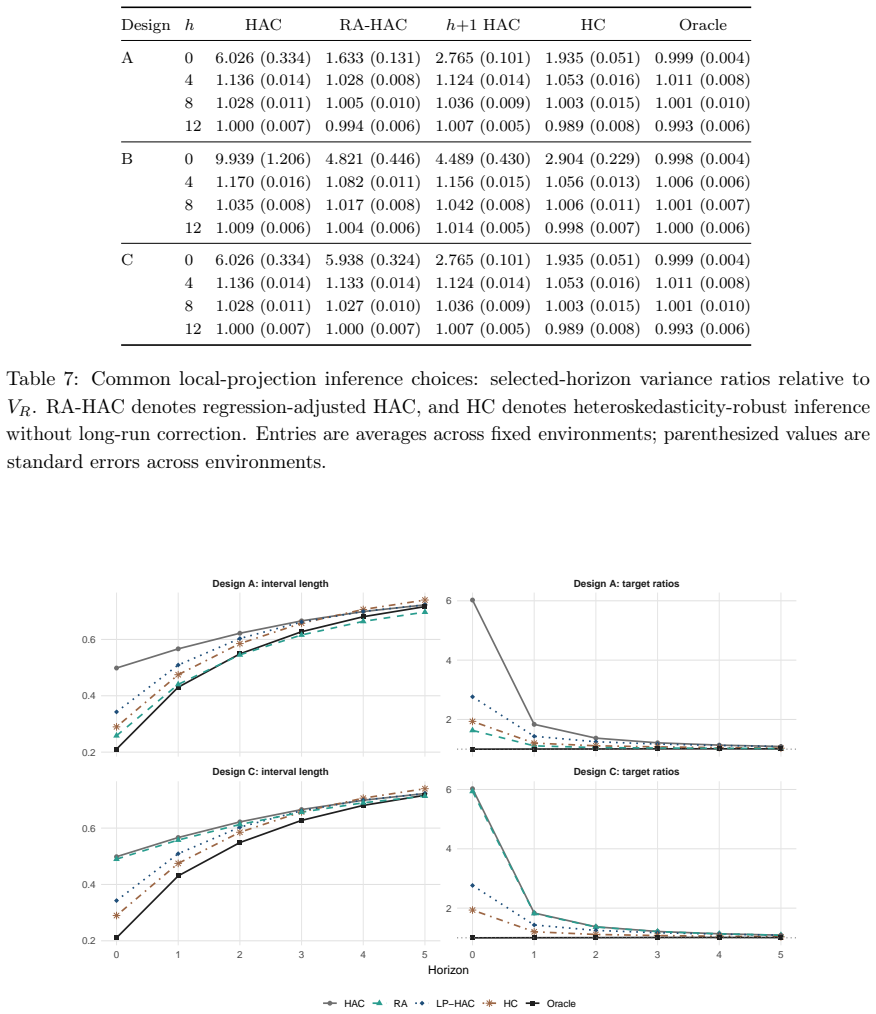

For locally correctly specified GMM estimators, the centered moment has design long-run variance Ω_R, which determines the sandwich covariance for the finite-history estimand. Conventional HAC estimators instead converge to Ω_R^+ = Ω_R + Ω_μ, where Ω_μ ≽ 0 is the long-run variance of the centered mean-moment path. HAC inference is therefore conservative for scalar functions of the finite-history estimand. Projection adjustment using predetermined covariates can reduce this HAC variance limit in Loewner order and, under an additional long-run orthogonality condition, yields a tighter conservative bound on the corresponding asymptotic covariance.

What carries the argument

The design long-run variance Ω_R of the centered moment path under conditioning on the historical environment, which supplies the correct sandwich covariance for the finite-history estimand.

If this is right

- HAC inference is conservative for scalar functions of the finite-history estimand.

- Projection adjustment using predetermined covariates reduces the HAC variance limit in Loewner order.

- Under an additional long-run orthogonality condition the adjusted estimator yields a tighter conservative bound.

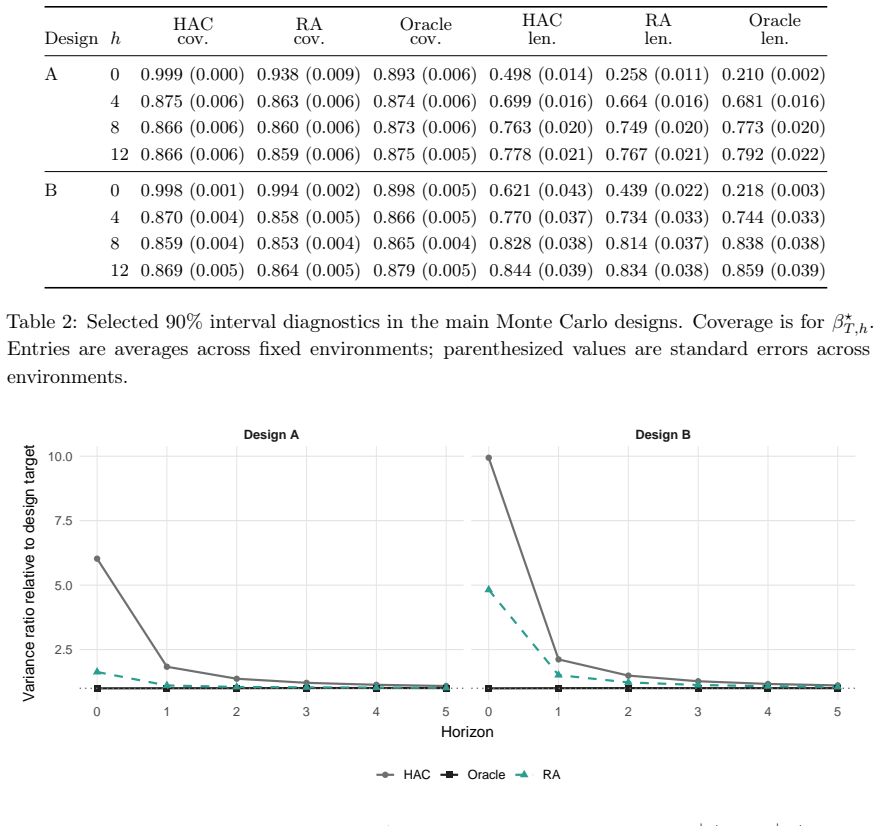

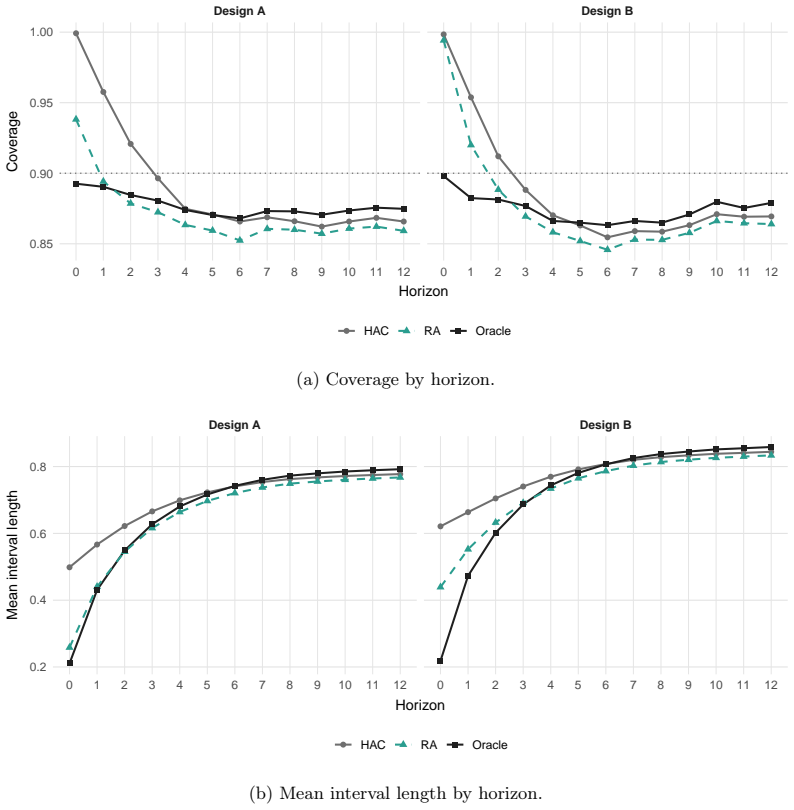

- Monte Carlo evidence shows when the distinction between the two variance limits is quantitatively important.

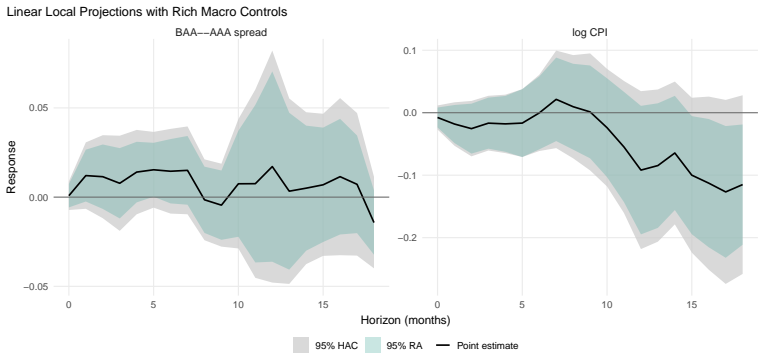

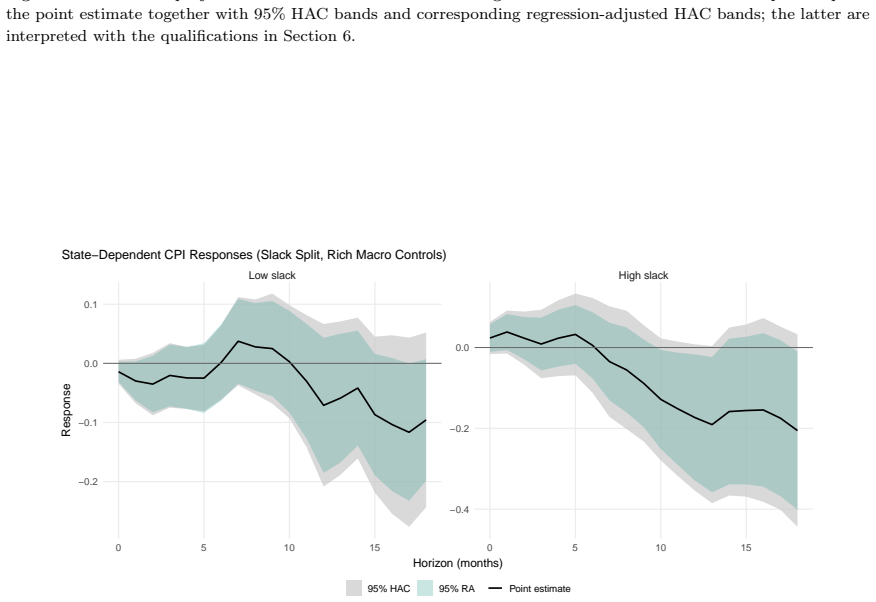

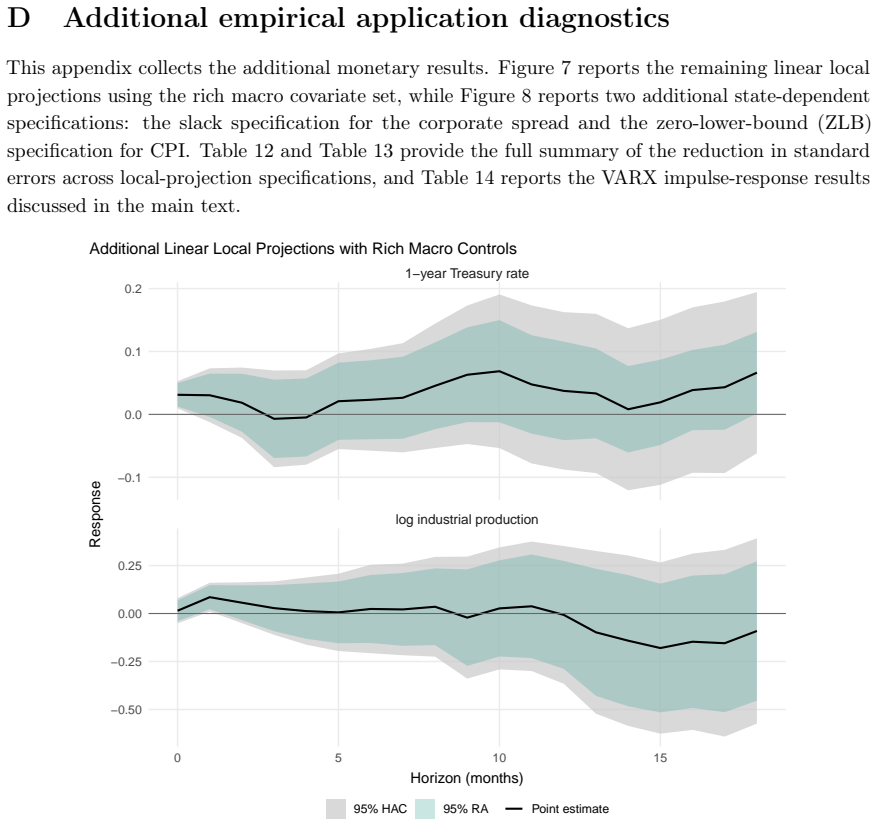

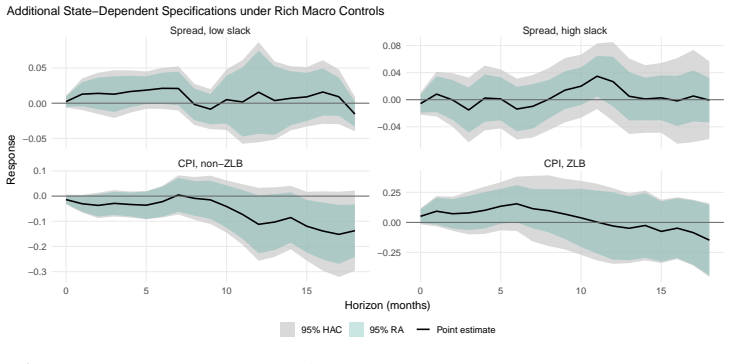

- In a monetary-policy application, standard-error reductions from rich macro covariates diagnose economically meaningful predictable variation in the mean-moment path.

Where Pith is reading between the lines

- If researchers adopt the design-based conditioning more widely, many existing HAC-based confidence intervals in macro time series could be replaced by narrower ones that remain valid under the design interpretation.

- The same conservatism argument may extend to other HAC-dependent procedures such as time-series IV or local projections.

- A direct test for whether the mean-moment path exhibits long-run variation could serve as a practical diagnostic for whether the projection adjustment is likely to matter.

- keywords:[

Load-bearing premise

Uncertainty arises solely from alternative realizations of shocks and instruments inside one fixed historical episode rather than from drawing an entirely new economy from a population.

What would settle it

A data set in which the long-run variance of the centered mean-moment path is exactly zero would make the HAC limit identical to Ω_R and remove the claimed conservatism.

Figures

read the original abstract

This paper studies inference for time-series GMM when uncertainty comes from shock assignment within a realized historical episode. Rather than treating the data as one random draw from a population of hypothetical economies, the framework conditions on the historical environment and considers alternative realizations of shocks and instruments. For locally correctly specified GMM estimators, the centered moment has design long-run variance $\Omega_R$, which determines the sandwich covariance for the finite-history estimand. Conventional HAC estimators instead converge to $\Omega_R^+=\Omega_R+\Omega_\mu$, where $\Omega_\mu\succeq0$ is the long-run variance of the centered mean-moment path. HAC inference is therefore conservative for scalar functions of the finite-history estimand. Projection adjustment using predetermined covariates can reduce this HAC variance limit in Loewner order and, under an additional long-run orthogonality condition, yields a tighter conservative bound on the corresponding asymptotic covariance. Monte Carlo evidence shows when the distinction is quantitatively important. In a monetary-policy application, standard-error reductions from rich macro covariates provide a diagnostic for economically meaningful predictable variation in the mean-moment path.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a design-based framework for inference in time-series GMM estimators by conditioning on the realized historical environment and considering alternative assignments of shocks and instruments. Under local correct specification, the centered moment has design long-run variance Ω_R that governs the sandwich covariance for the finite-history estimand; conventional HAC estimators converge instead to Ω_R^+ = Ω_R + Ω_μ (Ω_μ ≽ 0), the long-run variance of the centered mean-moment path, implying conservatism for scalar functions of the estimand. Projection adjustments using predetermined covariates can reduce the HAC variance limit in the Loewner order and, under long-run orthogonality, tighten the conservative bound. Monte Carlo experiments illustrate when the distinction is quantitatively relevant, and a monetary-policy application shows that richer macro covariates can reduce standard errors as a diagnostic for predictable mean-moment variation.

Significance. If the central decomposition holds, the paper supplies a coherent design-based rationale for why standard HAC procedures can be conservative in finite-history time-series GMM settings and identifies a covariate-based adjustment that can tighten inference without leaving the conservative class. The explicit conditioning on historical shock assignment, the Monte Carlo calibration of when Ω_μ matters, and the monetary-policy illustration are concrete strengths that increase the result's applicability to macroeconometric work.

minor comments (2)

- The abstract states the variance decomposition and the Loewner-order reduction from projection adjustment; the main text should include an explicit statement of the rate conditions under which the HAC limit equals Ω_R + Ω_μ (e.g., the bandwidth and sample-size requirements relative to the history length).

- The monetary-policy application reports standard-error reductions from rich covariates; a table or figure comparing the design-based and conventional standard errors side-by-side for the key parameters would make the quantitative diagnostic clearer.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the paper, the clear summary of its contributions, and the recommendation for minor revision. No specific major comments were raised in the report.

Circularity Check

No significant circularity

full rationale

The derivation introduces a design-based conditioning on the realized historical episode and defines the design long-run variance Ω_R directly from that conditioning; the decomposition showing conventional HAC converging to the larger Ω_R + Ω_μ follows from the same explicit modeling choice rather than from any fitted parameter, self-citation chain, or ansatz smuggled in from prior work. No equation reduces to its own input by construction, and the central conservatism claim for scalar functions of the finite-history estimand remains independent of the paper's own fitted quantities.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Proposition 9.Consider the fixed-weight estimator obtained by settingbAN ≡A in the sample criterion

Define DT :=∇ θ GT (θ)⊤A¯mT (θ) θ=θ⋆ T , ζ T,t :=G T (θ⋆ T )⊤AeT,t + JT,t(θ⋆ T )−G T (θ⋆ T ) ⊤ A¯m⋆ T . Proposition 9.Consider the fixed-weight estimator obtained by settingbAN ≡A in the sample criterion. Suppose Assumptions 1, 3, 4, 6, 7, and 8 hold for this fixed A, but do not impose Assumption 5. SupposeDT → D with D nonsingular. Suppose also that, on ...

1996

-

[2]

The subtracted matrix is positive semidefinite because ΣLP C ⊤(CΣLP C ⊤)−1CΣLP = M ⊤M, where M := (CΣLP C ⊤)−1/2CΣLP

= Σ LP − ΣLP C ⊤(CΣLP C ⊤)−1CΣLP. The subtracted matrix is positive semidefinite because ΣLP C ⊤(CΣLP C ⊤)−1CΣLP = M ⊤M, where M := (CΣLP C ⊤)−1/2CΣLP. Hence the conditional covariance is weakly smaller thanΣLP in Loewner order. The tangent-space equivalence identifies the VAR influence vector with this restricted Gaussian influence vector onker(C) = Im(R...

1994

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.