Optimal Execution under Liquidity Uncertainty

Pith reviewed 2026-05-19 10:05 UTC · model grok-4.3

The pith

The value function for optimal share execution under stochastic resilience and liquidity regimes is the unique viscosity solution to a system of variational HJB inequalities.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

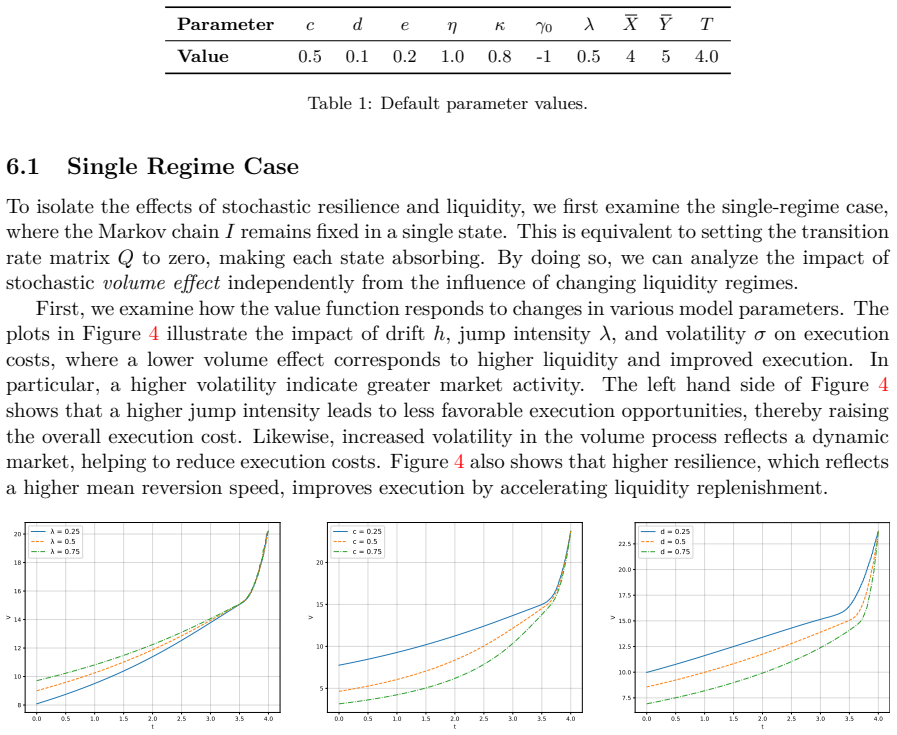

For the optimal execution problem with general limit-order-book shapes, a stochastic volume-effect process governing the decay of price impact, and a finite-state Markov chain driving abrupt liquidity shifts, the value function is the unique viscosity solution to the system of variational Hamilton-Jacobi-Bellman inequalities. The free boundary separating the execution region from the continuation region admits further analytical study, and the model is illustrated by numerical examples for different book configurations.

What carries the argument

The system of variational Hamilton-Jacobi-Bellman inequalities satisfied by the value function, whose free boundary demarcates execution from continuation.

If this is right

- The optimal purchase schedule can be approximated by solving the HJB system numerically for any fixed limit-order-book shape.

- The location of the free boundary depends explicitly on the current resilience level and the active liquidity regime.

- Abrupt shifts in the Markov chain produce jumps in the continuation value that alter the timing of optimal purchases.

- General limit-order-book shapes enter the HJB system only through the instantaneous impact term, leaving the viscosity-solution argument unchanged.

Where Pith is reading between the lines

- The same viscosity framework could be applied to the symmetric selling problem by reversing the sign of the control.

- If the Markov chain is replaced by a continuous-state diffusion for liquidity, the system would become a single integro-differential HJB equation whose free boundary might still be characterizable.

- The numerical examples suggest that execution becomes more front-loaded when the probability of moving to a low-liquidity regime rises.

Load-bearing premise

Market resilience decays according to the chosen stochastic volume-effect process and liquidity changes occur only by switching among the finite number of regimes in the Markov chain.

What would settle it

Numerical solution of the HJB system for a given resilience process and Markov chain produces an execution schedule whose realized cost, when simulated in a market whose liquidity dynamics differ markedly from the modeled processes, exceeds the cost of simple time-weighted averaging.

Figures

read the original abstract

We study an optimal execution strategy for purchasing a large block of shares over a fixed time horizon. The execution problem is subject to a general price impact that gradually dissipates due to market resilience. We allow for general limit order book shapes to characterize instantaneous market impact. To model the resilience dynamics, we introduce a stochastic process that governs the rate at which the deviation between the impacted and unaffected prices decays. This volume-effect process reflects fluctuations in market activity that drive the pace of liquidity replenishment. Additionally, we incorporate stochastic liquidity variations through a regime-switching Markov chain to capture abrupt shifts in market conditions. We study this singular control problem, where the trader optimally determines the timing and rate of purchases to minimize execution costs. The associated value function to this optimization problem is shown to satisfy a system of variational Hamilton-Jacobi-Bellman inequalities. Moreover, we establish that it is the unique viscosity solution to this HJB system and study the analytical properties of the free boundary separating the execution and continuation regions. To illustrate our results, we present numerical examples under different limit-order book configurations, highlighting the interplay between price impact, resilience dynamics, and stochastic liquidity regimes in shaping the optimal execution strategy.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies optimal execution of a large block purchase over a fixed horizon under general price impact that dissipates according to a stochastic resilience process (volume-effect process) and abrupt liquidity shifts modeled by a finite-state Markov chain. The trader solves a singular stochastic control problem to minimize costs by choosing timing and rate of purchases. The central claims are that the value function satisfies a system of variational Hamilton-Jacobi-Bellman inequalities, is the unique viscosity solution to this system, and that the free boundary separating execution and continuation regions admits analytical study; numerical examples under varying limit-order-book shapes illustrate the results.

Significance. If the viscosity uniqueness and free-boundary properties are established rigorously, the work extends singular-control techniques to execution problems with stochastic resilience and regime switches, providing a framework that captures realistic fluctuations in market activity and liquidity. This is relevant for algorithmic trading and market-microstructure modeling. The choice of viscosity solutions is natural for the singular-control setting with jumps in regimes, and the numerical illustrations help show the interplay among impact, resilience, and liquidity regimes.

major comments (1)

- [Abstract and §3] Abstract and §3 (Main results): the claim that the value function is the unique viscosity solution to the variational HJB system is load-bearing for the entire analysis, yet the provided outline does not include the verification step that the stochastic resilience process and Markov-chain liquidity dynamics satisfy the required regularity and growth conditions for the comparison principle; without this explicit check the uniqueness result cannot be confirmed from the given information.

minor comments (2)

- [Abstract] The abstract mentions numerical examples under different LOB configurations but does not specify the exact shapes, parameter values, or discretization scheme used; adding these details would improve reproducibility.

- [Model section] Notation for the resilience process and the regime-switching generator should be introduced with a dedicated table or list of symbols to avoid ambiguity when reading the HJB system.

Simulated Author's Rebuttal

We thank the referee for their careful reading of our manuscript and for the constructive feedback. We address the major comment below.

read point-by-point responses

-

Referee: [Abstract and §3] Abstract and §3 (Main results): the claim that the value function is the unique viscosity solution to the variational HJB system is load-bearing for the entire analysis, yet the provided outline does not include the verification step that the stochastic resilience process and Markov-chain liquidity dynamics satisfy the required regularity and growth conditions for the comparison principle; without this explicit check the uniqueness result cannot be confirmed from the given information.

Authors: We acknowledge the referee's observation. The uniqueness of the viscosity solution is indeed central to our results. While the manuscript invokes standard comparison principles for such HJB systems with regime switches, we agree that an explicit verification of the regularity and growth conditions for the stochastic resilience process and the Markov-chain liquidity dynamics should be provided to make the application of the comparison principle fully rigorous. In the revised manuscript, we will include this verification in Section 3, detailing how our assumptions ensure the necessary conditions hold. This addition will not alter the main claims but will enhance the completeness of the proof. revision: yes

Circularity Check

No significant circularity; derivation relies on standard viscosity techniques

full rationale

The paper introduces a stochastic resilience process and finite-state Markov chain for liquidity, formulates the singular control problem, and applies standard techniques from stochastic control to show that the value function satisfies and is the unique viscosity solution to the system of variational HJB inequalities. The free-boundary analysis follows from the model dynamics without any reduction of claimed results to fitted parameters, self-citations, or definitional tautologies. All steps are independent of the target claims and rest on established theory for regime-switching singular control problems.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Price impact dissipates according to a stochastic process governing the decay rate between impacted and unaffected prices.

- domain assumption Liquidity variations are captured by a regime-switching Markov chain.

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The associated value function ... is shown to satisfy a system of variational Hamilton–Jacobi–Bellman inequalities. Moreover, we establish that it is the unique viscosity solution to this HJB system and study the analytical properties of the free boundary separating the execution and continuation regions.

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We introduce a stochastic volume effect governed by a jump diffusion process ... Liquidity regimes are incorporated through a finite-state Markov chain

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Optimal Trade Execution in an Order Book Model with Stochastic Liquidity Parameters

Julia Ackermann, Thomas Kruse, and Mikhail Urusov. “Optimal Trade Execution in an Order Book Model with Stochastic Liquidity Parameters”. In: SIAM Journal on Financial Mathematics 12.2 (2021), pp. 788–822. doi: 10.1137/20M135409X

-

[2]

Dynamic optimal execution in a mixed-market-impact Hawkes price model

Aur´ elien Alfonsi and Pierre Blanc. “Dynamic optimal execution in a mixed-market-impact Hawkes price model”. In: Finance and Stochastics 20 (Jan. 2016). doi: 10.1007/s00780-015-0282-y

-

[3]

Optimal execution strategies in limit order books with general shape functions

Aur´ elien Alfonsi, Antje Fruth, and Alexander Schied. “Optimal execution strategies in limit order books with general shape functions”. In: Quantitative Finance 10.2 (2010), pp. 143–157. doi: 10.1080/14697680802595700

-

[4]

Optimal Trading with Stochastic Liquidity and Volatility

Robert Almgren. “Optimal Trading with Stochastic Liquidity and Volatility”. In: SIAM Journal on Financial Mathematics 3.1 (2012), pp. 163–181. doi: 10.1137/090763470

-

[5]

High Frequency Trading in a Limit Order Book

Marco Avellaneda and Sasha Stoikov. “High Frequency Trading in a Limit Order Book”. In: Quantitative Finance 8 (Apr. 2008), pp. 217–224. doi: 10.1080/14697680701381228

-

[6]

A stochastic representation theorem with applications to optimization and obstacle problems

Peter Bank and Nicole El Karoui. “A stochastic representation theorem with applications to optimization and obstacle problems”. In: The Annals of Probability 32.1A (2004), pp. 103–136

work page 2004

-

[7]

Optimal Trade Execution in Illiquid Markets

Erhan Bayraktar and Michael Ludkovski. “Optimal Trade Execution in Illiquid Markets”. In: Mathematical Finance 21.4 (2011), pp. 681–701. doi: https://doi.org/10.1111/j.1467-9965.2010.00446.x

-

[8]

Optimal liquidation under stochastic liquidity

Dirk Becherer, Todor Bilarev, and Peter Frentrup. “Optimal liquidation under stochastic liquidity”. In: Finance and Stochastics 22.1 (Jan. 2018), pp. 39–68. issn: 1432-1122. doi: 10.1007/s00780-017-0346-2

-

[9]

Optimal control of execution costs

Dimitris Bertsimas and Andrew W. Lo. “Optimal control of execution costs”. In: Journal of Financial Markets 1.1 (1998), pp. 1–50. issn: 1386-4181. doi: https://doi.org/10.1016/S1386-4181(97)00012-8

-

[10]

Weak Dynamic Programming Principle for Viscosity Solutions

Bruno Bouchard and Nizar Touzi. “Weak Dynamic Programming Principle for Viscosity Solutions”. In: SIAM Journal on Control and Optimization 49.3 (2011), pp. 948–962. doi: 10.1137/090752328

-

[11]

How Markets Slowly Digest Changes in Supply and Demand

Jean-Philippe Bouchaud, J. Doyne Farmer, and Fabrizio Lillo. “How Markets Slowly Digest Changes in Supply and Demand”. In: Handbook of Financial Markets: Dynamics and Evolution. North-Holland, 2009, pp. 57–160. doi: https://doi.org/10.1016/B978-012374258-2.50006-3

-

[12]

Slow Decay of Impact in Equity Markets

X. Brokmann, E. S´ eri´ e, J. Kockelkoren, and J.-P. Bouchaud. “Slow Decay of Impact in Equity Markets”. In: Market Microstructure and Liquidity 01.02 (2015), p. 1550007. doi: 10.1142/S2382626615500070

-

[13]

The regularity of free boundaries in higher dimensions

Luis A. Caffarelli. “The regularity of free boundaries in higher dimensions”. In: Acta Mathematica 139.1 (1977), pp. 155–184. doi: 10.1007/BF02392236. 28

-

[14]

Optimal execution with stochastic delay

´Alvaro Cartea and Leandro S´ anchez-Betancourt. “Optimal execution with stochastic delay”. In: Finance and Stochastics 27.1 (Jan. 2023), pp. 1–47. issn: 1432-1122. doi: 10.1007/s00780-022-00491-w

-

[15]

Trading with Small Nonlinear Price Impact

Thomas Cay´ e, Martin Herdegen, and Johannes Muhle-Karbe. “Trading with Small Nonlinear Price Impact”. In: The Annals of Applied Probability 30.2 (2020), pp. 706–746. issn: 10505164, 21688737

work page 2020

-

[16]

Optimal Execution under Incomplete Information

Etienne Chevalier, Yadh Hafsi, and Vathana Ly Vath. “Optimal Execution under Incomplete Information”. In: (2024). doi: 10.48550/arXiv.2411.04616

-

[17]

Uncovering Market Disorder and Liquidity Trends Detection

Etienne Chevalier, Yadh Hafsi, and Vathana Ly Vath. “Uncovering Market Disorder and Liquidity Trends Detection”. In: (2023). doi: 10.48550/arXiv.2310.09273

-

[18]

Optimal execution with regime-switching market resilience

Chi Chung Siu, Ivan Guo, Song-Ping Zhu, and Robert J. Elliott. “Optimal execution with regime-switching market resilience”. In: Journal of Economic Dynamics and Control 101 (2019), pp. 17–40. issn: 0165-1889. doi: https://doi.org/10.1016/j.jedc.2019.01.006

-

[19]

Optimal liquidation under partial information with price impact

Katia Colaneri, Zehra Eksi, Rudiger Frey, and Michaela Szolgyenyi. “Optimal liquidation under partial information with price impact”. In: Stochastic Processes and their Applications 130.4 (2020), pp. 1913–1946. issn: 0304-4149. doi: https://doi.org/10.1016/j.spa.2019.06.004

-

[20]

A Finite Difference Scheme for Option Pricing in Jump Diffusion and Exponential L´ evy Models

Rama Cont and Ekaterina Voltchkova. “A Finite Difference Scheme for Option Pricing in Jump Diffusion and Exponential L´ evy Models”. In:SIAM Journal on Numerical Analysis 43.4 (2005), pp. 1596–1626. doi: 10.1137/S0036142903436186

-

[21]

User’s Guide to Viscosity Solutions of Second Order Artial Differential Equations

Michael Crandall, Hitoshi Ishii, and Pierre-Louis Lions. “User’s Guide to Viscosity Solutions of Second Order Artial Differential Equations”. In: Bulletin of the American Mathematical Society 27 (July 1992). doi: 10.1090/S0273-0979-1992-00266-5

-

[22]

Optimal execution with multiplicative price impact and incomplete information on the return

Felix Dammann and Giorgio Ferrari. “Optimal execution with multiplicative price impact and incomplete information on the return”. In: Finance and Stochastics 27.3 (July 2023), pp. 713–768. issn: 1432-1122. doi: 10.1007/s00780-023-00508-y

-

[23]

Stochastic equations, flows and measure-valued processes

Donald A. Dawson and Zenghu Li. “Stochastic equations, flows and measure-valued processes”. In: The Annals of Probability 40.2 (2012), pp. 813–857. doi: 10.1214/10-AOP629

-

[24]

Portfolio choice with small temporary and transient price impact

Ibrahim Ekren and Johannes Muhle-Karbe. “Portfolio choice with small temporary and transient price impact”. In: Mathematical Finance 29.4 (2019), pp. 1066–1115. doi: https://doi.org/10.1111/mafi.12204

-

[25]

On the fine structure of the free boundary for the classical obstacle problem

Alessio Figalli and Joaquim Serra. “On the fine structure of the free boundary for the classical obstacle problem”. In: Inventiones mathematicae 215.1 (2019), pp. 311–366. doi: 10.1007/s00222-018-0827-8

-

[26]

Optimal Trading with Signals and Stochastic Price Impact

Jean-Pierre Fouque, Sebastian Jaimungal, and Yuri F. Saporito. “Optimal Trading with Signals and Stochastic Price Impact”. In: SIAM Journal on Financial Mathematics 13.3 (2022), pp. 944–968. doi: 10.1137/21M1394473

-

[27]

Optimal trade execution in order books with stochastic liquidity

Antje Fruth, Torsten Schoneborn, and Mikhail Urusov. “Optimal trade execution in order books with stochastic liquidity”. In: Mathematical Finance 29.2 (2019), pp. 507–541. doi: https://doi.org/10.1111/mafi.12180

-

[28]

G. H. Hardy, J. E. Littlewood, and G. P´ olya. “Inequalities”. In: (1952). 29

work page 1952

-

[29]

Multi-dimensional optimal trade execution under stochastic resilience

Ulrich Horst and Xiaonyu Xia. “Multi-dimensional optimal trade execution under stochastic resilience”. In: Finance and Stochastics 23.4 (Oct. 2019), pp. 889–923. issn: 1432-1122. doi: 10.1007/s00780-019-00394-3

-

[30]

Optimal stopping of switching diffusions with state dependent switching rates

R. H. Liu. “Optimal stopping of switching diffusions with state dependent switching rates”. In: Stochastics 88.4 (2016), pp. 586–605. doi: 10.1080/17442508.2015.1110152

-

[31]

Optimal portfolio execution problem with stochastic price impact

Guiyuan Ma, Chi Chung Siu, Song-Ping Zhu, and Robert J. Elliott. “Optimal portfolio execution problem with stochastic price impact”. In: Automatica 112 (2020), p. 108739. issn: 0005-1098. doi: https://doi.org/10.1016/j.automatica.2019.108739

-

[32]

K. W. Morton and D. F. Mayers. Numerical Solution of Partial Differential Equations: An Introduction. 2nd. Cambridge University Press, 2005. isbn: 9780521607933

work page 2005

-

[33]

Stochastic Liquidity as a Proxy for Nonlinear Price Impact

Johannes Muhle-Karbe, Zexin Wang, and Kevin Webster. “Stochastic Liquidity as a Proxy for Nonlinear Price Impact”. In: Operations Research 72.2 (2024), pp. 444–458. doi: 10.1287/opre.2022.0627

-

[34]

Optimal trading strategy and supply/demand dynamics

Anna A. Obizhaeva and Jiang Wang. “Optimal trading strategy and supply/demand dynamics”. In: Journal of Financial Markets 16.1 (2013), pp. 1–32. issn: 1386-4181. doi: https://doi.org/10.1016/j.finmar.2012.09.001

-

[35]

Optimal stopping, free boundary, and American option in a jump-diffusion model

Huyˆ en Pham. “Optimal stopping, free boundary, and American option in a jump-diffusion model”. In: Applied Mathematics and Optimization 35.2 (1997), pp. 145–164

work page 1997

-

[36]

Trade-throughs: Empirical Facts and Application to Lead-lag Measures

Fabrizio Pomponio and Fr´ ed´ eric Abergel. “Trade-throughs: Empirical Facts and Application to Lead-lag Measures”. In: Econophysics of Order-driven Markets: Proceedings of Econophys-Kolkata V. Milano: Springer Milan, 2011, pp. 3–16. doi: 10.1007/978-88-470-1766-5_1

-

[37]

Optimal Execution in a General One-Sided Limit-Order Book

Silviu Predoiu, Gennady Shaikhet, and Steven Shreve. “Optimal Execution in a General One-Sided Limit-Order Book”. In: SIAM J. Financial Math. 2 (Jan. 2011), pp. 183–212. doi: 10.1137/10078534X

-

[38]

P.E. Protter. Stochastic Integration and Differential Equations. Stochastic Modelling and Applied Probability. Springer Berlin Heidelberg, 2005. isbn: 9783540003137

work page 2005

-

[39]

R. Tyrrell Rockafellar. “Convex Analysis”. In: Princeton Mathematical Series 28 (1970)

work page 1970

-

[40]

Principles of Mathematical Analysis

Walter Rudin. “Principles of Mathematical Analysis”. In: (1976)

work page 1976

-

[41]

From the Optimal Singular Stochastic Control to the Optimal Stopping for Regime-Switching Processes

Jinghai Shao and Taoran Tian. “From the Optimal Singular Stochastic Control to the Optimal Stopping for Regime-Switching Processes”. In: SIAM Journal on Control and Optimization 61.3 (2023), pp. 1631–1650. doi: 10.1137/22M1506705

-

[42]

Optimal investment and consumption with transaction costs

Steven E. Shreve and H. Mete Soner. “Optimal investment and consumption with transaction costs”. In: Annals of Applied Probability 4.3 (1994), pp. 609–692

work page 1994

-

[43]

Linear models for the impact of order flow on prices. I. History dependent impact models

Eduardo Damian Taranto, Giacomo Bormetti, Jean-Philippe Bouchaud, Fabrizio Lillo, and Bence Toth. “Linear models for the impact of order flow on prices. I. History dependent impact models”. In: Quantitative Finance 18.6 (2018), pp. 903–915. doi: 10.1080/14697688.2017.1395903

-

[44]

Universal price impact functions of individual trades in an order-driven market

Wei-Xing Zhou. “Universal price impact functions of individual trades in an order-driven market”. In: Quantitative Finance 12.8 (2012), pp. 1253–1263. doi: 10.1080/14697688.2010.504733. 30 A Proofs of the Results in Section 3 A.1 Continuity Modulus Proof of Lemma 3. Let 0≤t≤s≤T, x∈[0,X], y≥0 and X∈At(x). Suppose ξis a nonnegative random variable with fini...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.