Recognition: unknown

Optimal Insurance Menu Design under the Expected-Value Premium Principle

Pith reviewed 2026-05-10 07:36 UTC · model grok-4.3

The pith

Optimal insurance menus use excess-of-loss coverage with decreasing risk loadings to screen both private risk attitudes and types.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

When risk attitude is private information, the optimal coverage takes the form of excess-of-loss insurance with linear pricing in terms of the risk loading, designed to screen risk preferences. In contrast, when risk type is unobserved, the coverage is restricted to an excess-of-loss form and an ordinary differential equation characterizes the optimal risk loading. Under mild conditions, existence and uniqueness hold, and equilibrium contracts exhibit nonlinear pricing with decreasing risk loadings so higher-risk individuals face lower loadings to induce self-selection.

What carries the argument

The risk loading function in an excess-of-loss indemnity, chosen to satisfy incentive compatibility in the Stackelberg menu design problem under mean-variance utilities.

If this is right

- Equilibrium contracts exhibit nonlinear pricing.

- Higher-risk individuals receive lower risk loadings to ensure self-selection.

- The optimal loading satisfies an ODE whose solution exists and is unique under mild conditions.

- The shape of the pricing schedule and contracts depends on the distributions of unobserved heterogeneity.

Where Pith is reading between the lines

- Empirical insurance data could test whether loadings decrease with observed risk proxies as predicted.

- Relaxing the excess-of-loss restriction might produce menus with different profit and welfare properties.

- The ODE approach could extend to other multi-dimensional screening settings with continuous types.

- Numerical solutions for specific parameter values illustrate how heterogeneity affects contract menus.

Load-bearing premise

Coverage functions are restricted to excess-of-loss form when risk type is unobserved.

What would settle it

A concrete loss distribution and risk-aversion mapping where a menu of non-excess-of-loss contracts yields strictly higher insurer profit than the ODE-derived excess-of-loss solution.

Figures

read the original abstract

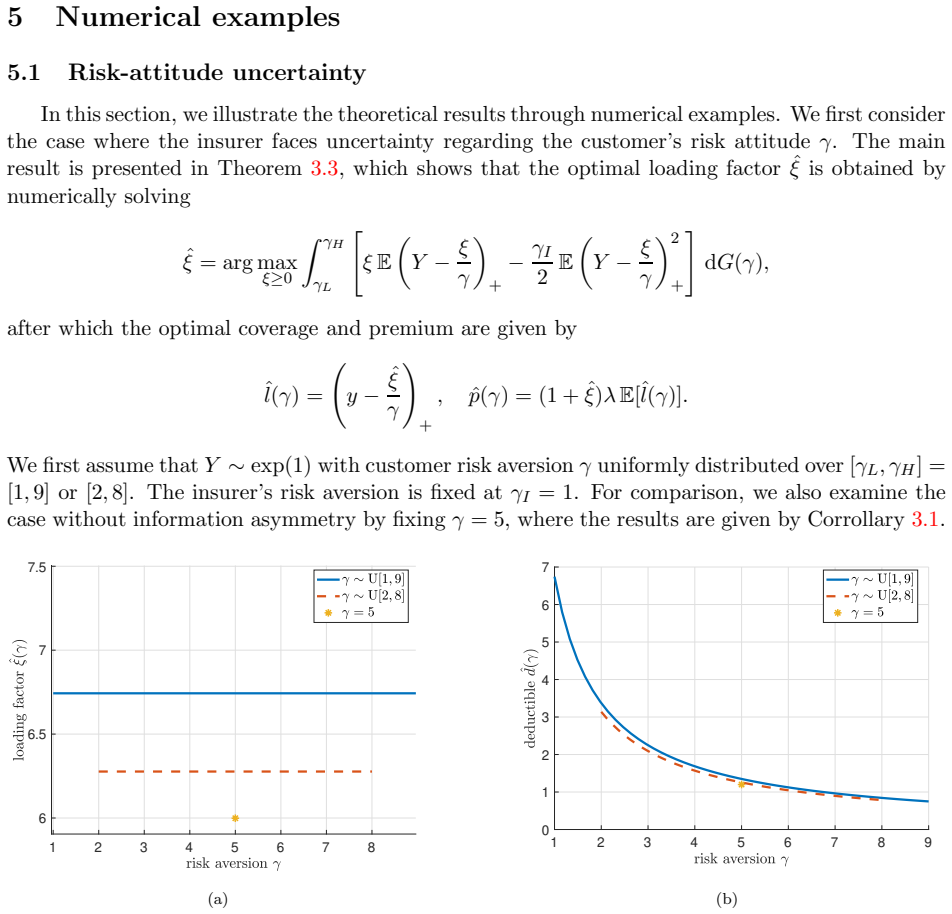

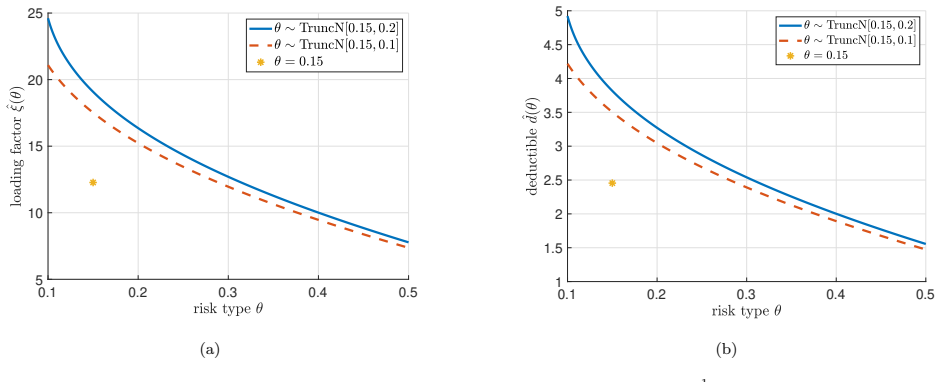

This paper studies optimal insurance design under asymmetric information in a Stackelberg framework, where a monopolistic insurer faces uncertainty about both the insured's risk attitude, captured by a risk-aversion parameter, and the insured's risk type, characterized by the loss distribution. In particular, when the risk type is unobservable, we allow the risk-aversion parameter to depend on the risk type. We construct a menu of contracts that maximizes the mean-variance utilities of both parties under the expected-value premium principle, subject to a truth-telling constraint that ensures the truthful revelation of private information. We show that when risk attitude is private information, the optimal coverage takes the form of excess-of-loss insurance with linear pricing in terms of the risk loading (defined as the premium minus the expected loss), designed to screen risk preferences. In contrast, when risk type is unobserved, we restrict the coverage function to an excess-of-loss form and derive an ordinary differential equation that characterizes the optimal risk loading. Under mild conditions, we establish the existence and uniqueness of the solution. The results show that equilibrium contracts exhibit nonlinear pricing with decreasing risk loadings, implying that higher-risk individuals face lower risk loadings in order to induce self-selection. Finally, numerical illustrations demonstrate how parameter values and the distributions of unobserved heterogeneity affect the structure of optimal contracts and the resulting pricing schedule.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies optimal menu design for insurance contracts in a Stackelberg monopolist-insurer setting with asymmetric information on both the insured's risk-aversion parameter and risk type (loss distribution). Under mean-variance utilities and the expected-value premium principle, it shows that private risk attitude alone yields excess-of-loss coverage with linear pricing in the risk loading. When risk type is also unobserved (allowing type-dependent risk aversion), the analysis restricts coverage to excess-of-loss form, derives an ODE for the optimal risk-loading function, proves existence and uniqueness under mild conditions, and obtains nonlinear pricing with decreasing loadings for higher-risk types to induce self-selection. Numerical examples illustrate dependence on parameter distributions.

Significance. If the excess-of-loss restriction is justified or without loss of generality, the explicit ODE characterization and equilibrium properties provide a concrete, computable description of screening menus under multidimensional private information. The combination of mean-variance preferences, expected-value pricing, and type-dependent risk aversion is a natural but under-explored setting; the existence/uniqueness result and the decreasing-loading property are potentially useful for both theory and calibration.

major comments (1)

- [Abstract] Abstract and the statement of the problem when risk type is unobserved: the paper explicitly imposes the restriction 'we restrict the coverage function to an excess-of-loss form' before deriving the ODE and the decreasing-loading property. No argument is given that the insurer's optimum must lie inside this subclass among all feasible indemnity schedules I(·). Because the subsequent ODE, existence/uniqueness claim, and nonlinear-pricing conclusion are derived only inside this restricted class, the restriction is load-bearing for the central results; a proof that no general I(·) can improve the objective (or a counter-example showing the restriction binds) is required.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review of our manuscript. The major comment on the excess-of-loss restriction is addressed below.

read point-by-point responses

-

Referee: [Abstract] Abstract and the statement of the problem when risk type is unobserved: the paper explicitly imposes the restriction 'we restrict the coverage function to an excess-of-loss form' before deriving the ODE and the decreasing-loading property. No argument is given that the insurer's optimum must lie inside this subclass among all feasible indemnity schedules I(·). Because the subsequent ODE, existence/uniqueness claim, and nonlinear-pricing conclusion are derived only inside this restricted class, the restriction is load-bearing for the central results; a proof that no general I(·) can improve the objective (or a counter-example showing the restriction binds) is required.

Authors: We acknowledge that the manuscript imposes the excess-of-loss restriction without a formal proof that the global optimum among all feasible indemnity schedules I(·) lies in this subclass. The restriction is adopted to obtain a tractable ODE characterization of the risk-loading function and to derive explicit results on existence, uniqueness, and the decreasing-loading property. In the revised manuscript we will expand the introduction and the relevant modeling section to motivate the focus on excess-of-loss contracts by reference to their prevalence in both the theoretical insurance literature and actual insurance products. We will also add an explicit remark stating that the reported results are derived under this assumption and that relaxing the restriction to general indemnity functions is left for future research. This revision clarifies the scope of the contribution without claiming optimality outside the considered class. revision: yes

- A rigorous proof that no general indemnity schedule I(·) can improve upon the excess-of-loss restriction, or a counter-example showing that the restriction is binding.

Circularity Check

No significant circularity; derivations follow from explicit optimization under stated model assumptions

full rationale

The paper conducts a Stackelberg optimization maximizing mean-variance utilities subject to truth-telling constraints under the expected-value premium principle. For private risk attitude it derives that excess-of-loss coverage emerges endogenously. For unobserved risk type it explicitly states the restriction to excess-of-loss form before deriving the characterizing ODE and proving existence/uniqueness under mild conditions. No step equates a claimed prediction or first-principles result to its inputs by construction, no self-citation chain supports a load-bearing uniqueness claim, and no fitted parameter is relabeled as a prediction. The analysis remains self-contained given the primitives and the openly declared restriction; the resulting nonlinear pricing and decreasing loadings are direct consequences of the constrained optimization rather than tautological.

Axiom & Free-Parameter Ledger

free parameters (1)

- distributions of risk types and risk-aversion parameters

axioms (4)

- domain assumption Both insurer and insured maximize mean-variance utilities

- domain assumption Premium follows the expected-value principle (expected loss plus loading)

- domain assumption Insurer acts as Stackelberg leader offering a menu first

- domain assumption Truth-telling (incentive compatibility) constraint must hold

Reference graph

Works this paper leans on

-

[1]

Rei nsurance contract design with adverse selection

Ka Chun Cheung, Sheung Chi Phillip Yam, and Fei Lung Yuen. Rei nsurance contract design with adverse selection. Scandinavian Actuarial Journal , 2019(9):784–798,

2019

-

[2]

Optimal design 27 of reinsurance contracts under adverse selection with a con tinuum of types

Ka Chun Cheung, Sheung Chi Phillip Yam, Fei Lung Yuen, and Yiy ing Zhang. Optimal design 27 of reinsurance contracts under adverse selection with a con tinuum of types. arXiv preprint arXiv:2504.17468,

-

[3]

Optimal insurance i n a monopoly: Dual utilities with hidden risk attitudes

Mario Ghossoub, Bin Li, and Benxuan Shi. Optimal insurance i n a monopoly: Dual utilities with hidden risk attitudes. arXiv preprint arXiv:2504.01095 ,

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.