Risk-Aware Multi-Market Scheduling of Virtual Power Plants with Dynamic Network Tariffs

Pith reviewed 2026-05-07 12:36 UTC · model grok-4.3

The pith

Virtual power plants exploit market arbitrage with risk-averse bidding that aligns closer to physical output, while dynamic tariffs shift demand but cut expected profits by up to 65 percent.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

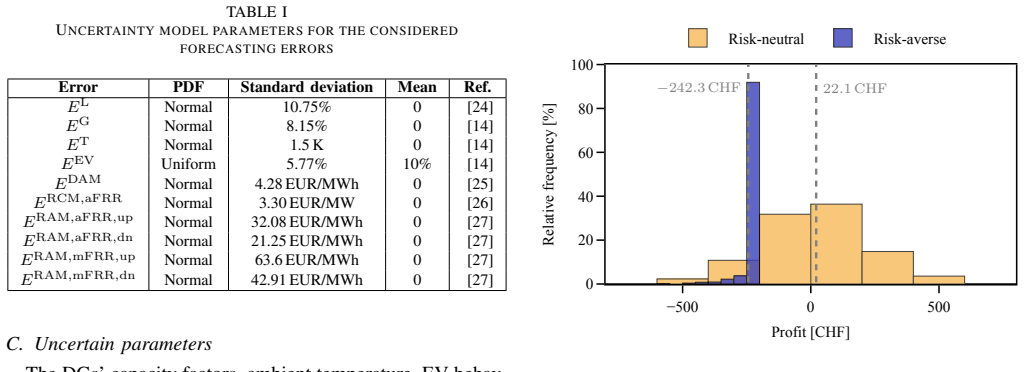

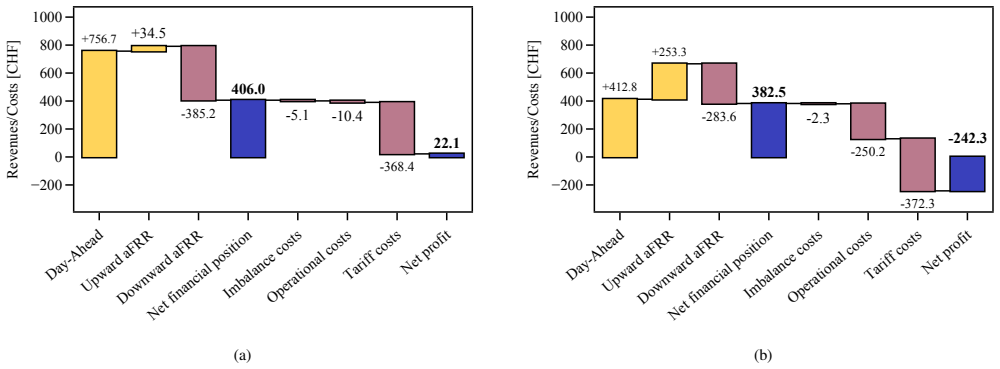

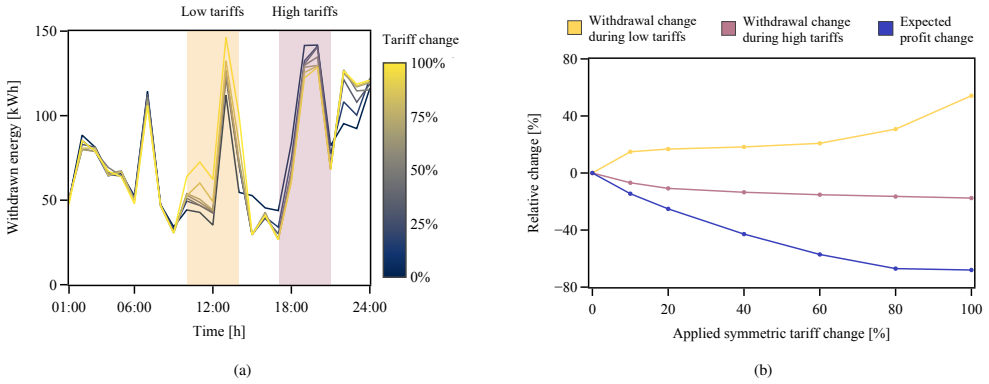

The central claim is that a two-stage stochastic optimization model jointly optimizing multi-market bids and local flexibility procurement via dynamic network tariffs, solved with Benders decomposition and incorporating conditional value-at-risk, shows in a realistic case study that risk-neutral and risk-averse virtual power plant strategies both exploit arbitrage opportunities, with risk aversion lowering profit volatility through tighter alignment to physical dispatch and dynamic tariffs unlocking demand shifts across the day at the cost of up to 65 percent lower expected profitability under strong signals.

What carries the argument

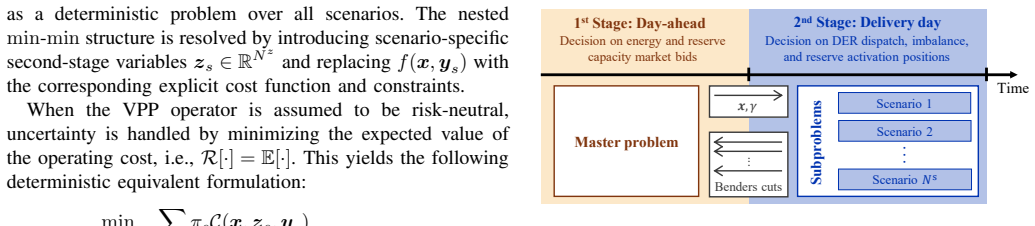

Two-stage stochastic optimization framework with Benders decomposition that integrates device-level constraints, network limitations, market uncertainties, and conditional value-at-risk to jointly optimize energy and reserve market bidding with dynamic network tariff responses.

If this is right

- Both risk-neutral and risk-averse strategies exploit arbitrage opportunities across energy and reserve markets.

- Risk aversion reduces profit volatility through closer alignment with physical dispatch.

- Dynamic tariffs unlock local flexibility by shifting demand across the day.

- Strong tariff signals reduce expected profitability by up to 65 percent with limited additional flexibility gains.

Where Pith is reading between the lines

- Moderate tariff levels may be needed to capture flexibility without eroding too much of the virtual power plant's revenue.

- The scheduling method could support grid operators facing rising shares of distributed resources by coordinating local responses without new wires.

- If real uncertainty distributions differ from the scenario set, the stability advantage of risk aversion may shrink in practice.

Load-bearing premise

A finite set of scenarios accurately captures device behavior, network limits, and market uncertainties, and Benders decomposition produces solutions close enough to optimal that the reported profit and flexibility results would hold under real conditions.

What would settle it

Deploying the virtual power plant in actual operation over multiple days and measuring whether profit volatility under risk-averse bidding stays as low as predicted and whether demand shifts from dynamic tariffs match the modeled levels without the full modeled profit reduction would test the central results.

Figures

read the original abstract

As the penetration of distributed energy resources (DERs) increases, harnessing their flexibility becomes critical for power system operations. Virtual power plants (VPPs) offer a promising solution. However, most existing scheduling tools rely on simplified DER or grid models and largely overlook local flexibility procurement mechanisms such as dynamic network tariffs. This paper proposes a two-stage stochastic optimization framework for VPP multi-market scheduling that integrates detailed device-level constraints, network limitations, and operational and market uncertainties. Conditional value-at-risk is incorporated to represent risk preferences, and Benders decomposition ensures tractability with extensive scenario sets. The model jointly optimizes bidding across energy and reserve markets while explicitly accounting for local flexibility procurement through dynamic network tariffs. The results from a realistic case study show that both risk-neutral and risk-averse strategies exploit arbitrage opportunities. However, risk aversion reduces profit volatility through closer alignment with physical dispatch. Dynamic tariffs unlock local flexibility by shifting demand across the day, though strong tariff signals reduce expected profitability by up to 65% with limited additional flexibility gains.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a two-stage stochastic optimization framework for the multi-market scheduling of virtual power plants (VPPs). It incorporates detailed device-level and network constraints, market and operational uncertainties through scenarios, and uses Conditional Value-at-Risk (CVaR) to account for risk aversion. Benders decomposition is employed to solve the model with large scenario sets. The framework jointly optimizes bids in energy and reserve markets while considering dynamic network tariffs for local flexibility. A realistic case study illustrates that both risk-neutral and risk-averse VPP strategies exploit arbitrage opportunities, with risk aversion leading to reduced profit volatility by better aligning bids with physical dispatch. Dynamic tariffs are shown to enable demand shifting, but strong tariff signals can reduce expected profits by up to 65% with limited additional flexibility benefits.

Significance. If the numerical results prove robust under validation, this work is significant for extending VPP scheduling by integrating dynamic network tariffs with risk management in a tractable stochastic framework. The demonstration of arbitrage opportunities, volatility reduction under CVaR, and the quantified trade-off with tariff strength offers practical insights for VPP operators and system flexibility procurement. The application of Benders decomposition to handle extensive scenarios and detailed constraints strengthens its potential applicability.

major comments (2)

- [Case Study and Numerical Results] The headline result that strong dynamic tariff signals reduce expected profitability by up to 65% (Abstract and case study section) lacks supporting information on the Benders decomposition optimality gap or any out-of-sample validation of the scenario set. This is load-bearing because the claimed alignment of risk-averse bids with physical dispatch and the tariff impact quantification depend on the solutions being near-optimal over a representative scenario distribution of prices, DER output, load, and network states.

- [Methodology (Benders Decomposition and Scenario Generation)] No sensitivity analysis is reported regarding the scenario reduction technique or the cardinality of the scenario set used in the two-stage stochastic program. Given that the framework relies on these scenarios to capture uncertainties, the absence of such checks raises concerns about the robustness of the comparisons between risk-neutral and risk-averse strategies.

minor comments (1)

- [Notation] Ensure consistent use of symbols for the CVaR risk-aversion parameter and tariff signals across equations and text to avoid potential confusion.

Simulated Author's Rebuttal

We are grateful to the referee for their insightful comments, which have helped us improve the clarity and robustness of our work. Below, we provide point-by-point responses to the major comments.

read point-by-point responses

-

Referee: [Case Study and Numerical Results] The headline result that strong dynamic tariff signals reduce expected profitability by up to 65% (Abstract and case study section) lacks supporting information on the Benders decomposition optimality gap or any out-of-sample validation of the scenario set. This is load-bearing because the claimed alignment of risk-averse bids with physical dispatch and the tariff impact quantification depend on the solutions being near-optimal over a representative scenario distribution of prices, DER output, load, and network states.

Authors: We thank the referee for this observation. In the revised manuscript, we have added the optimality gaps from the Benders decomposition in the case study results (all below 0.5%), which confirms the solutions are near-optimal. Regarding out-of-sample validation, the scenario generation method (described in Section III) uses a large set of historical data to ensure representativeness, and the comparisons between strategies are based on the same scenario set. We have included a discussion on this in the revised text. However, a dedicated out-of-sample test was not conducted; we note this as a direction for future research in the conclusions. The 65% reduction is thus supported by the in-sample results with small optimality gaps. revision: partial

-

Referee: [Methodology (Benders Decomposition and Scenario Generation)] No sensitivity analysis is reported regarding the scenario reduction technique or the cardinality of the scenario set used in the two-stage stochastic program. Given that the framework relies on these scenarios to capture uncertainties, the absence of such checks raises concerns about the robustness of the comparisons between risk-neutral and risk-averse strategies.

Authors: We agree that sensitivity analysis on the scenario set would strengthen the robustness claims. In the revised manuscript, we have added a new subsection (IV-D) presenting sensitivity results for scenario cardinalities ranging from 100 to 500 and two reduction techniques (fast-forward selection and k-means clustering). The key findings, including the profit reduction under dynamic tariffs and the benefits of risk aversion, remain consistent across these variations, with profit differences within 5%. This addition addresses the concern about the reliability of the strategy comparisons. revision: yes

Circularity Check

No circularity: standard stochastic programming applied to case study

full rationale

The paper defines a two-stage stochastic program with CVaR risk measure and Benders decomposition to solve a VPP multi-market bidding problem that includes device constraints, network limits, and dynamic tariffs. All reported outcomes (arbitrage exploitation, volatility reduction, and the 65% profit impact) are obtained by numerically solving this optimization model on an external case study; no parameter is fitted to the target metric and then re-labeled as a prediction, no result is defined in terms of itself, and no load-bearing step reduces to a self-citation whose content is unverified. The framework is therefore self-contained against external benchmarks and receives the lowest circularity score.

Axiom & Free-Parameter Ledger

free parameters (1)

- CVaR risk-aversion parameter

axioms (2)

- domain assumption Uncertainties in prices, renewable output, and demand can be adequately represented by a finite set of scenarios

- domain assumption Benders decomposition converges to a solution that is sufficiently close to the true optimum for the joint bidding-dispatch problem

Forward citations

Cited by 1 Pith paper

-

Efficient Multi-Market Scheduling of Virtual Power Plants via Spectral Representation of Uncertainty

Intrusive PCE reformulates stochastic multi-market VPP scheduling into a tractable deterministic spectral problem, matching scenario-based quality with up to 137x speedup on a Swiss grid case.

Reference graph

Works this paper leans on

-

[1]

Grid codes for renewable powered systems,

IRENA, “Grid codes for renewable powered systems,” International Renewable Energy Agency, Tech. Rep., 2022

work page 2022

-

[2]

Unlocking the potential of distributed energy resources,

IEA, “Unlocking the potential of distributed energy resources,” International Energy Agency, Tech. Rep., 2022, [online]. Avail- able: https://www.iea.org/reports/unlocking-the-potential-of-distributed- energy-resources. Accessed: May 26, 2025

work page 2022

-

[3]

On feasibility and flexibility operating regions of virtual power plants and TSO/DSO interfaces,

S. Riaz and P. Mancarella, “On feasibility and flexibility operating regions of virtual power plants and TSO/DSO interfaces,” in2019 IEEE Milan PowerTech, 2019, pp. 1–6

work page 2019

-

[4]

Stochastic optimization of trading strategies in sequential electricity markets,

E. Kraft, M. Russo, D. Keles, and V . Bertsch, “Stochastic optimization of trading strategies in sequential electricity markets,”European Journal of Operational Research, vol. 308, pp. 400–421, 2023

work page 2023

-

[5]

M. Vahedipour-Dahraie, H. Rashidizadeh-Kermani, M. Shafie-Khah, and J. P. S. Catal˜ao, “Risk-averse optimal energy and reserve scheduling for virtual power plants incorporating demand response programs,”IEEE Transactions on Smart Grid, vol. 12, no. 2, pp. 1405–1415, 2021

work page 2021

-

[6]

A. Fusco, D. Gioffr `e, A. F. Castelli, C. Bovo, and E. Martelli, “A multi-stage stochastic programming model for the unit commitment of conventional and virtual power plants bidding in the day-ahead and ancillary services markets,”Applied Energy, vol. 336, p. 120739, 2023

work page 2023

-

[7]

H. Nemati, P. S ´anchez-Mart´ın, L. Sigrist, L. Rouco, and ´Alvaro Ortega, “Flexible robust optimization for renewable-only vpp bidding on elec- tricity markets with economic risk analysis,”International Journal of Electrical Power & Energy Systems, vol. 167, p. 110594, 2025

work page 2025

-

[8]

Robust optimization based bidding strategy for virtual power plants in electricity markets,

Z. Liang and Y . Guo, “Robust optimization based bidding strategy for virtual power plants in electricity markets,” in2016 IEEE Power and Energy Society General Meeting (PESGM), 2016, pp. 1–5. 24th Power Systems Computation Conference PSCC 2026 Limassol, Cyprus — June 8-12, 2026

work page 2016

-

[9]

J.-H. Kim, J. S. Hwang, and Y .-S. Kim, “An igdt-wdrcc based optimal bidding strategy of vpp aggregators in new energy market considering multiple uncertainties,”Energy, vol. 313, p. 133712, 2024

work page 2024

-

[10]

Impact of distribution tariffs on prosumer demand response,

M. Avau, N. Govaerts, and E. Delarue, “Impact of distribution tariffs on prosumer demand response,”Energy Policy, vol. 151, 2021

work page 2021

-

[11]

E. Ghorbankhani and A. Badri, “A bi-level stochastic framework for VPP decision making in a joint market considering a novel demand response scheme,”International Transactions on Electrical Energy Sys- tems, vol. 28, no. 1, p. e2473, 2018

work page 2018

-

[12]

M. He, Z. Soltani, M. Khorsand, A. Dock, P. Malaty, and M. Esmaili, “Behavior-aware aggregation of distributed energy resources for risk- aware operational scheduling of distribution systems,”Energies, vol. 15, no. 24, 2022

work page 2022

-

[13]

Picasso implementation project (as of april 2025),

ENTSO-E, “Picasso implementation project (as of april 2025),” [Online]. Available: https://www.entsoe.eu/network codes/eb/picasso/, 2025, ac- cessed: Apr. 22, 2025

work page 2025

-

[14]

Power reserve capacity from virtual power plants with reliability and cost guarantees,

L. Zapparoli, B. Gjorgiev, and G. Sansavini, “Power reserve capacity from virtual power plants with reliability and cost guarantees,”IEEE Transactions on Power Systems, pp. 1–12, 2026

work page 2026

-

[15]

Report on electricity transmission and distribution tariff methodologies in europe,

Agency for the Cooperation of Energy Regulators, “Report on electricity transmission and distribution tariff methodologies in europe,” ACER, Tech. Rep., January 2023

work page 2023

-

[16]

General balance group regulations,

Swissgrid, “General balance group regulations,” Swissgrid, Tech. Rep., 2025. [Online]. Available: https://www.swissgrid.ch/content/dam/swissgrid/customers/topics/legal- system/balance-group/1/01-Appendix-1-General-BG-Regulations-V2-6- en.pdf

work page 2025

-

[17]

Optimal sizing of capacitors placed on a radial distribution system,

M. Baran and F. Wu, “Optimal sizing of capacitors placed on a radial distribution system,”IEEE Transactions on Power Delivery, vol. 4, no. 1, pp. 735–743, 1989

work page 1989

-

[18]

A. Oneto, B. Gjorgiev, F. Tettamanti, and G. Sansavini, “Large-scale generation of geo-referenced power distribution grids from open data with load clustering,”Sustainable Energy, Grids and Networks, vol. 42, p. 101678, 2025

work page 2025

-

[19]

L. Zapparoli, A. Oneto, M. P. Herrera, B. Gjorgiev, G. Hug, and G. Sansavini, “Future deployment and flexibility of distributed energy resources in the distribution grids of switzerland,”Scientific Data, vol. 12, no. 1, p. 1491, 2025

work page 2025

-

[20]

ENTSO-E, “Transparency platform,” https://newtransparency.entsoe.eu/market/energyPrices, 2024, accessed: 2025-8-10

work page 2024

-

[21]

Ancillary services tenders and auction results,

Swissgrid AG, “Ancillary services tenders and auction results,” https://www.swissgrid.ch/en/home/customers/topics/ancillary- services/tenders.html, 2025, accessed: 2025-08-06

work page 2025

-

[22]

(2025) Regelleistung.net – data center: afrr capacity market data

50Hertz Transmission GmbH, Amprion GmbH, TenneT TSO GmbH, and TransnetBW GmbH. (2025) Regelleistung.net – data center: afrr capacity market data. Accessed: 2025-08-18. [Online]. Available: https://www.regelleistung.net/apps/datacenter/tenders/

work page 2025

-

[23]

EWZ, “Stromtarife 2024,” https://ewz.ch/dam/ewz/Privatkunden/Strom/ Tarife/Dokumente/Uebersicht Tarife ewz 2024.pdf, Tramstrasse 35, 8050 Z ¨urich, 2024, accessed: 2024-10-23

work page 2024

-

[24]

Short-term residential load forecasting based on lstm recurrent neural network,

W. Kong, Z. Y . Dong, Y . Jia, D. J. Hill, Y . Xu, and Y . Zhang, “Short-term residential load forecasting based on lstm recurrent neural network,” IEEE Transactions on Smart Grid, vol. 10, no. 1, pp. 841–851, 2019

work page 2019

-

[25]

J. Lago, G. Marcjasz, B. De Schutter, and R. Weron, “Forecasting day- ahead electricity prices: A review of state-of-the-art algorithms, best practices and an open-access benchmark,”Applied Energy, vol. 293, p. 116983, 2021

work page 2021

-

[26]

J. Cardo-Miota, E. P ´erez, and H. Beltran, “Deep learning-based fore- casting of the automatic frequency reserve restoration band price in the iberian electricity market,”Sustainable Energy, Grids and Networks, vol. 35, 2023

work page 2023

-

[27]

J. M. Failing, J. Cardo-Miota, E. P ´erez, H. Beltran, and J. Segarra- Tamarit, “Deep learning approaches for predicting the upward and downward energy prices in the spanish automatic frequency restoration reserve market,”Energy, vol. 320, 2025

work page 2025

-

[28]

A. Srinivasan, R. Wu, P. Heer, and G. Sansavini, “Impact of forecast uncertainty and electricity markets on the flexibility provision and economic performance of highly-decarbonized multi-energy systems,” Applied Energy, vol. 338, p. 120825, 2023

work page 2023

-

[29]

German Federal Office of Justice, “EnWG § 14a Netzorientierte Steuerung von steuerbaren Verbrauchseinrichtungen und steuerbaren Netzanschl¨ussen; Festlegungskompetenzen.” 24th Power Systems Computation Conference PSCC 2026 Limassol, Cyprus — June 8-12, 2026

work page 2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.