Recognition: no theorem link

Deep Learning for Solving and Estimating Dynamic Models in Economics and Finance

Pith reviewed 2026-05-15 01:25 UTC · model grok-4.3

The pith

Deep learning methods solve and estimate high-dimensional dynamic stochastic models in economics and finance by embedding equilibrium conditions into neural-network training.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that deep learning methods such as Deep Equilibrium Nets, Physics-Informed Neural Networks, deep surrogate models, and Gaussian-process dynamic programming can solve and estimate high-dimensional dynamic stochastic models in economics and finance that strain classical tensor-product grid methods.

What carries the argument

Deep Equilibrium Nets and Physics-Informed Neural Networks, which embed the model's equilibrium conditions or partial differential equations directly into the neural-network loss function to train approximations to policy and value functions.

If this is right

- High-dimensional heterogeneous-agent and overlapping-generations models with aggregate risk become routinely solvable.

- Structural estimation by simulated method of moments extends to economies with many state variables and frictions.

- Continuous-time macro-finance models with occasionally binding constraints can be solved without discretization grids.

- Climate-economy models under uncertainty support sensitivity analysis and policy design with quantified approximation error.

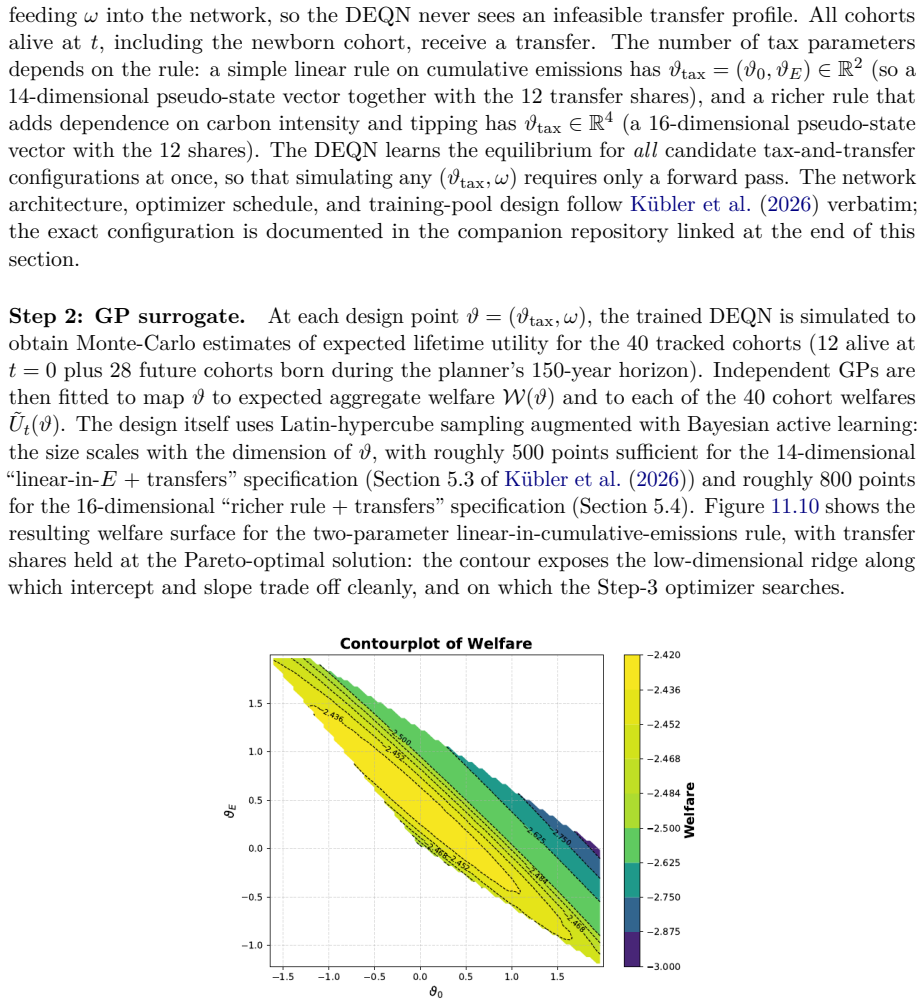

- Gaussian-process dynamic programming combined with active learning scales value-function iteration to very large continuous state spaces.

Where Pith is reading between the lines

- If the methods remain stable at scale, they could support real-time policy evaluation in models previously considered computationally prohibitive.

- The surrogate-model and uncertainty-quantification components may enable tighter integration between structural estimation and machine-learning forecasting pipelines.

- Active-learning variants could reduce the number of model evaluations needed for accurate solutions in high-dimensional spaces.

Load-bearing premise

The neural-network approximations remain accurate and stable when applied to the equilibrium conditions and dynamics of the high-dimensional models without introducing material bias or convergence failures.

What would settle it

A direct numerical comparison in which the deep-learning solutions produce policy functions or equilibrium prices that deviate materially from known analytical solutions or converged low-dimensional grid benchmarks on a specific high-dimensional test case.

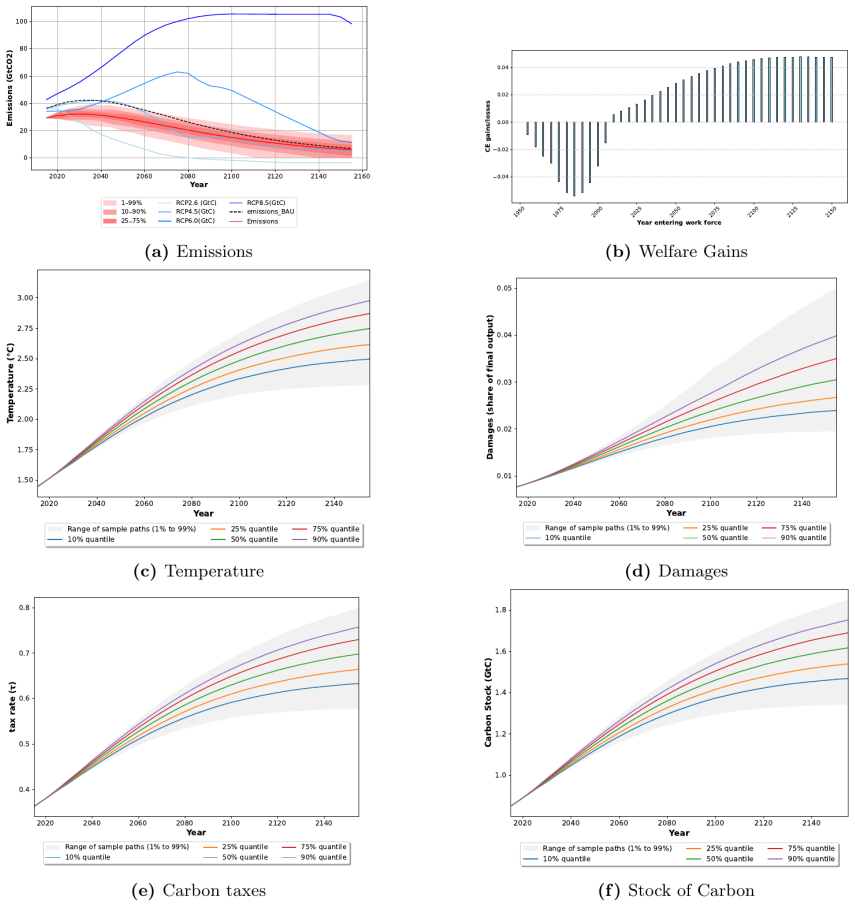

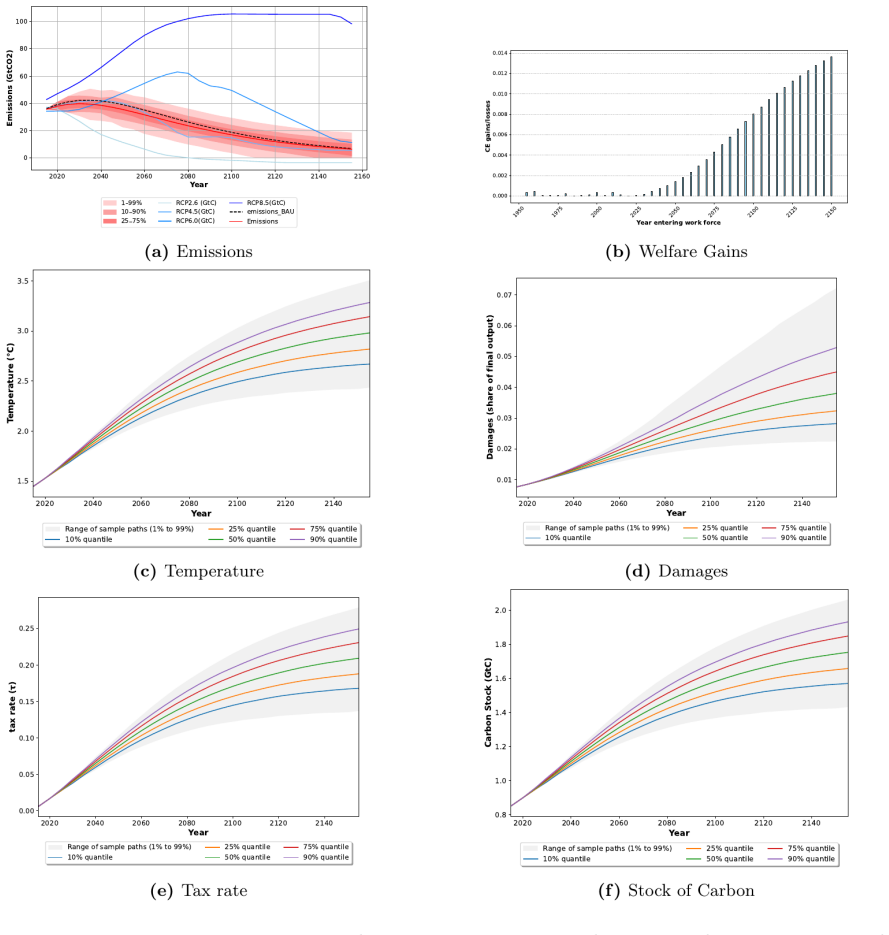

Figures

read the original abstract

This script offers an implementation-oriented introduction to deep learning methods for solving and estimating high-dimensional dynamic stochastic models in economics and finance. Its starting point is the curse of dimensionality: heterogeneous-agent economies, overlapping-generations models with aggregate risk, continuous-time models with occasionally binding constraints, climate-economy models, and macro-finance environments with many assets and frictions generate state and parameter spaces that strain classical tensor-product grid methods. The exposition is organized around four complementary methodologies. Deep Equilibrium Nets embed discrete-time equilibrium conditions into neural-network loss functions. Physics-Informed Neural Networks approximate continuous-time Hamilton--Jacobi--Bellman, Kolmogorov forward, and related partial differential equations. Deep surrogate models provide fast, differentiable approximations to expensive structural models, while Gaussian processes add a probabilistic layer that quantifies approximation uncertainty; together they support estimation, sensitivity analysis, and constrained policy design. Gaussian-process-based dynamic programming, combined with active learning and dimension reduction, extends value-function iteration to very large continuous state spaces. Applications span representative-agent and international real business cycle models, overlapping-generations and heterogeneous-agent economies, continuous-time macro-finance, structural estimation by simulated method of moments, and climate economics under uncertainty. Companion notebooks in TensorFlow and PyTorch invite hands-on experimentation. These notes are a deliberately subjective and inevitably incomplete snapshot of a rapidly evolving field, aimed at equipping PhD students and researchers to engage with this frontier hands-on.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript is an implementation-oriented tutorial introducing four deep-learning approaches—Deep Equilibrium Nets, Physics-Informed Neural Networks, deep surrogate models, and Gaussian-process dynamic programming—for solving and estimating high-dimensional dynamic stochastic models in economics and finance. It frames these methods as practical responses to the curse of dimensionality in heterogeneous-agent, overlapping-generations, continuous-time macro-finance, and climate-economy settings, supplies companion TensorFlow/PyTorch notebooks, and positions the notes as a subjective snapshot of the literature aimed at PhD students and researchers.

Significance. If the neural-network approximations remain accurate and stable for the equilibrium conditions and dynamics described, the paper would be significant as a hands-on bridge between classical solution techniques and scalable deep-learning tools, enabling faster iteration on otherwise intractable models and supporting estimation, sensitivity analysis, and policy design in macro-finance and climate economics.

major comments (1)

- [methodologies overview and applications] The central claim that the four methodologies can reliably address models that strain tensor-product grids rests on the accuracy and stability of the neural approximations; the manuscript treats these properties as established by the cited literature without providing new error bounds, convergence diagnostics, or side-by-side benchmarks against classical methods within the text itself.

minor comments (3)

- [abstract] The abstract states that the notes are 'deliberately subjective and inevitably incomplete'; a short explicit statement of scope limitations (e.g., which model classes are omitted) would help readers calibrate expectations.

- [throughout] Notation for state variables, value functions, and equilibrium conditions is introduced separately for each methodology; a brief consolidated table or appendix would improve cross-section readability.

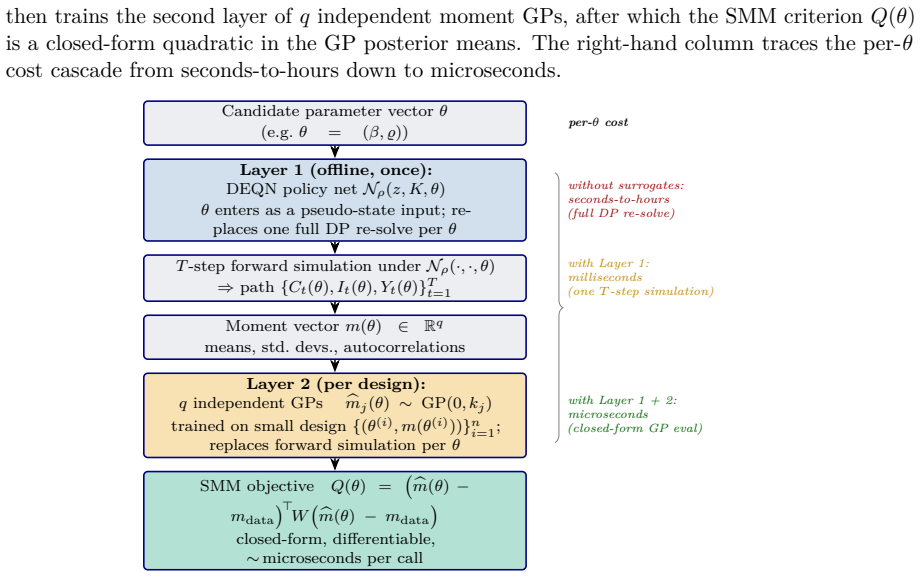

- [Gaussian-process dynamic programming] The description of Gaussian-process dynamic programming mentions active learning and dimension reduction but does not specify the exact acquisition function or reduction technique used in the accompanying notebook.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation and the recommendation of minor revision. We address the single major comment below.

read point-by-point responses

-

Referee: The central claim that the four methodologies can reliably address models that strain tensor-product grids rests on the accuracy and stability of the neural approximations; the manuscript treats these properties as established by the cited literature without providing new error bounds, convergence diagnostics, or side-by-side benchmarks against classical methods within the text itself.

Authors: We agree that the manuscript relies on accuracy and stability results established in the cited literature rather than deriving new error bounds or conducting original side-by-side benchmarks. This is consistent with the paper's stated scope as an implementation-oriented tutorial and subjective snapshot of the literature, whose goal is to equip readers to apply the methods and consult the original sources for theoretical details. To address the concern, we will add a concise new subsection titled 'Accuracy, Stability, and Practical Diagnostics' that summarizes key convergence guarantees and numerical validation practices from the referenced works (e.g., those on Deep Equilibrium Nets and PINNs). We will also insert brief pointers to existing benchmark studies in the applications sections and note in the introduction that users should perform model-specific verification. These changes preserve the tutorial focus while making the reliance on prior results more transparent. revision: partial

Circularity Check

No significant circularity

full rationale

The paper is an implementation-oriented tutorial and review that organizes four families of existing deep-learning methods (Deep Equilibrium Nets, PINNs, deep surrogates, Gaussian-process dynamic programming) for high-dimensional economic models. It does not advance new derivations, uniqueness theorems, or fitted parameters whose outputs are then relabeled as predictions within the manuscript itself. All central claims rest on summaries of prior literature plus external notebooks for verification; no equation or step reduces by construction to a self-defined input or self-citation chain. The accuracy and stability of the approximations are treated as established properties of the cited techniques rather than results derived inside this document.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard dynamic stochastic general equilibrium assumptions hold for the models discussed.

Reference graph

Works this paper leans on

-

[1]

Achdou, Y., Han, J., Lasry, J.-M., Lions, P.-L., and Moll, B. (2022). Income and wealth distribution in macroeconomics: A continuous-time approach.The Review of Economic Studies, 89(1):45–86. Adjemian, S., Bastani, H., Juillard, M., Karamé, F., Maih, J., Mihoubi, F., Mutschler, W., Pfeifer, J., Ratto, M., Rion, N., and Villemot, S. (2024). Dynare: Referen...

work page 2022

-

[2]

Solving Nonlinear and High-Dimensional Partial Differential Equations via Deep Learning

Dynare Working Papers 80, CEPREMAP. Aggarwal, C. C., Hinneburg, A., and Keim, D. A. (2001). On the surprising behavior of distance metrics in high dimensional space. InDatabase Theory — ICDT 2001, volume 1973 ofLecture Notes in Computer Science, pages 420–434. Springer. Aiyagari, S. R. (1994). Uninsured idiosyncratic risk and aggregate saving.The Quarterl...

work page internal anchor Pith review Pith/arXiv arXiv 2001

-

[3]

Bayer, C. and Luetticke, R. (2020). Solving discrete time heterogeneous agent models with aggre- gate risk and many idiosyncratic states by perturbation.Quantitative Economics, 11(4):1253–

work page 2020

-

[4]

Belkin, M., Hsu, D., Ma, S., and Mandal, S. (2019). Reconciling modern machine-learning practice and the classical bias–variance trade-off.Proceedings of the National Academy of Sciences, 116(32):15849–15854. Bellman, R. (1957).Dynamic Programming. Princeton University Press, Princeton, NJ. Bellman, R. (1961).Adaptive Control Processes: A Guided Tour. ’Ra...

-

[5]

Deisenroth, M. P., Faisal, A. A., and Ong, C. S. (2020).Mathematics for Machine Learning. Cambridge University Press, Cambridge. Deisenroth, M. P. and Rasmussen, C. E. (2011). PILCO: A model-based and data-efficient approach to policy search. InProceedings of the 28th International Conference on Machine Learning. Deisenroth, M. P., Rasmussen, C. E., and P...

-

[6]

Non-stochasticbestarmidentificationandhyperparameter optimization

Jamieson, K.andTalwalkar, A.(2016). Non-stochasticbestarmidentificationandhyperparameter optimization. InProceedings of the 19th International Conference on Artificial Intelligence and Statistics (AISTATS). Jensen, S. and Traeger, C. P. (2014). Optimal climate change mitigation under long-term growth uncertainty: Stochastic integrated assessment and analy...

work page 2016

-

[7]

Scaling Laws for Neural Language Models

Kahou, M. E., Fernández-Villaverde, J., Perla, J., and Sood, A. (2021). Exploiting symmetry in high-dimensional dynamic programming. NBER Working Paper 28981, National Bureau of Economic Research. Kaplan, G., Moll, B., and Violante, G. L. (2018). Monetary policy according to HANK.American Economic Review, 108(3):697–743. Kaplan, J., McCandlish, S., Henigh...

work page internal anchor Pith review Pith/arXiv arXiv 2021

-

[8]

Lasry, J.-M. and Lions, P.-L. (2007). Mean field games.Japanese Journal of Mathematics, 2(1):229–260. Leach, A. J. (2007). The climate change learning curve.Journal of Economic Dynamics and Control, 31(5):1728–1752. LeCun, Y., Bengio, Y., and Hinton, G. (2015). Deep learning.Nature, 521(7553):436–444. 321 Lee, B.-S. and Ingram, B. F. (1991). Simulation es...

work page 2007

-

[9]

Mish: A self regularized non-monotonic neural activation function.arXiv preprint arXiv:1908.08681,

Elsevier. Maliar, L., Maliar, S., and Valli, F. (2010). Solving the incomplete markets model with aggregate uncertainty using the Krusell–Smith algorithm.Journal of Economic Dynamics and Control, 34(1):42–49. Maliar, L., Maliar, S., and Winant, P. (2021). Deep learning for solving dynamic economic models.Journal of Monetary Economics, 122:76–101. Maliar, ...

-

[10]

Nordhaus, W. D. and Yang, Z. (1996). A regional dynamic general-equilibrium model of alternative climate-change strategies.The American Economic Review, pages 741–765. Norets, A. (2012). Estimation of dynamic discrete choice models using artificial neural network approximations.Econometric Reviews, 31(1):84–106. Novak, E. and Woźniakowski, H. (2008).Tract...

work page internal anchor Pith review Pith/arXiv arXiv doi:10.2139/ssrn.3282487 1996

-

[11]

Saltelli, A. and D’Hombres, B. (2010). Sensitivity analysis didn’t help. A practitioner’s critique of the Stern review.Global Environmental Change, 20(2):298–302. Saltelli, A., Ratto, M., Andres, T., Campolongo, F., Cariboni, J., Gatelli, D., Saisana, M., and Tarantola, S. (2008).Global Sensitivity Analysis: The Primer. Wiley. Santurkar, S., Tsipras, D., ...

work page 2010

-

[12]

324 Sargent, T. J. and Stachurski, J. (2026). Dynamic programming, volumes i and ii. QuantEcon open textbook series. Scheidegger, S. and Bilionis, I. (2019). Machine learning for high-dimensional dynamic stochastic economies.Journal of Computational Science, 33:68 –

work page 2026

-

[13]

Horovod: fast and easy distributed deep learning in TensorFlow

Scheidegger, S. and Treccani, A. (2018). Pricing american options under high-dimensional models with recursive adaptive sparse expectations.Journal of Financial Econometrics. Schlag, I., Irie, K., and Schmidhuber, J. (2021). Linear transformers are secretly fast weight programmers. InProceedings of the 38th International Conference on Machine Learning (IC...

work page internal anchor Pith review Pith/arXiv arXiv 2018

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.