Dynamic Consumer Demand at Large Scale

Pith reviewed 2026-05-25 02:24 UTC · model grok-4.3

The pith

A dynamic factor model pools heterogeneity across products and categories to improve demand prediction in large retail settings with sparse data.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The dynamic product-level factor model factorizes individual-product coefficients through a shared latent factor structure to capture correlated heterogeneity in baseline preferences, price sensitivity, and inertia; this yields substantially better predictive performance than static factor models and mixed logit benchmarks when individual histories are sparse and produces more elastic demand estimates by accounting for inertia.

What carries the argument

The dynamic product-level factor model that factorizes individual-product coefficients via shared latent factors to represent joint heterogeneity in preferences, price sensitivity, and inertia.

If this is right

- Demand estimates become more elastic once inertia is incorporated.

- Predictive gains are largest when individual purchase histories are short.

- The factor structure enables scaling to high-dimensional product and category spaces.

- Information pools across individuals and categories without separate per-person estimation.

Where Pith is reading between the lines

- The approach could support multi-category pricing policies by linking elasticities through the shared factors.

- Extensions might test whether the same structure improves forecasts in non-retail dynamic choice settings such as subscription services.

- If the latent factors prove stable over time, the model could reduce data requirements for new product introductions.

Load-bearing premise

The shared latent factor structure is assumed to adequately represent and pool the joint heterogeneity in baseline preferences, price sensitivity, and inertia across individuals and categories without substantial misspecification.

What would settle it

A hold-out test on real retail transaction data with sparse individual histories where the dynamic factor model shows no improvement in predictive accuracy over static models or where demand elasticities do not rise when inertia is included would falsify the central claim.

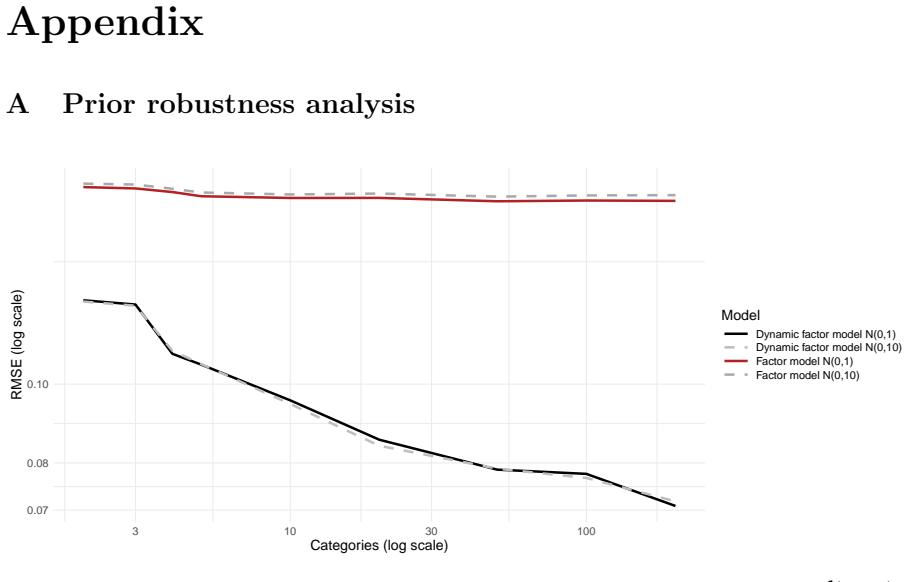

Figures

read the original abstract

We study consumer demand in large-scale retail settings with many products, multiple categories and repeated purchase behavior. While inertia and brand loyalty are well documented, existing discrete choice models typically focus on single categories or become computationally infeasible in high-dimensional environments. We propose a dynamic product-level factor model that captures heterogeneity in baseline preferences, price sensitivity and inertia through a shared latent factor structure. By factorizing individual-product coefficients, the model pools information across individuals and categories and allows for correlated heterogeneity. We estimate the model using Bayesian variational inference, enabling scalable estimation with tens of thousands of parameters. In a simulation study calibrated to realistic retail data, we show that the dynamic factor model substantially improves predictive performance relative to static factor models and mixed logit benchmarks, particularly when individual purchase histories are sparse. Accounting for inertia also leads to more elastic demand estimates, underscoring the importance of dynamics for measuring consumer responsiveness. Our results highlight dynamic factor models as a scalable and flexible approach for demand estimation in modern, high-dimensional retail markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a dynamic product-level factor model for estimating consumer demand in large-scale retail settings with many products and categories. The model factorizes individual-product coefficients to capture correlated heterogeneity in baseline preferences, price sensitivity, and inertia, estimated via scalable Bayesian variational inference. A simulation study calibrated to realistic retail data shows improved out-of-sample predictive performance relative to static factor models and mixed logit benchmarks (especially with sparse purchase histories) and more elastic demand estimates when inertia is included.

Significance. If the simulation results prove robust, the work would offer a computationally feasible method for incorporating dynamics and high-dimensional heterogeneity into discrete choice models, addressing a key limitation in modern retail demand estimation where individual histories are often sparse. The variational inference approach for handling tens of thousands of parameters is a notable technical strength for scalability.

major comments (1)

- [Simulation study] The central performance and elasticity claims rest entirely on a single simulation study (described in the abstract). Without details on robustness to alternative hyperparameter choices, holdout designs, or data-generating processes, it is difficult to assess whether the reported gains over static factors and mixed logit generalize beyond the calibrated setting.

Simulated Author's Rebuttal

We thank the referee for their constructive feedback. We address the single major comment below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Simulation study] The central performance and elasticity claims rest entirely on a single simulation study (described in the abstract). Without details on robustness to alternative hyperparameter choices, holdout designs, or data-generating processes, it is difficult to assess whether the reported gains over static factors and mixed logit generalize beyond the calibrated setting.

Authors: We agree that the simulation results would be strengthened by additional robustness checks. In the revised manuscript we will expand Section 4 to include (i) sensitivity to alternative hyperparameter values in the variational inference, (ii) alternative holdout designs that vary the share and length of sparse purchase histories, and (iii) two further data-generating processes that change the degree of inertia and the correlation structure of heterogeneity. These additions will clarify the extent to which the reported gains generalize beyond the baseline calibration, which itself is chosen to match key moments from scanner data. revision: yes

Circularity Check

No significant circularity

full rationale

The paper proposes a dynamic product-level factor model with shared latent factors for heterogeneity in preferences, price sensitivity, and inertia, estimated via Bayesian variational inference. Central performance claims rest on an external simulation study calibrated to realistic retail data, comparing out-of-sample predictions against static factor models and mixed logit benchmarks. No equations, fitted parameters, or self-citations are shown to reduce any reported prediction or result to the model's own inputs by construction. The factor-pooling structure is presented as a standard scalable approach without self-definitional loops or imported uniqueness theorems. This is a self-contained proposal with independent simulation evidence.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

dynamic product-level factor model ... uijct = θ'_i γ_jc − θ'_i λ_jc price_jct + θ'_i ρ_jc δ_ijc,t−1 (eq. 6)

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Bayesian variational inference ... mean-field Gaussian variational family

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Athey, S. and Blei, D. and Donnelly, R. and Ruiz, F. and Schmidt, T. , title =. AEA Papers and Proceedings , volume =. 2018 , pages =

work page 2018

-

[2]

Quantitative Marketing and Economics , pages=

Counterfactual inference for consumer choice across many product categories , author=. Quantitative Marketing and Economics , pages=

-

[3]

Journal of Machine Learning Research , volume=

Automatic differentiation variational inference , author=. Journal of Machine Learning Research , volume=

-

[4]

The Annals of Applied Statistics , volume=

SHOPPER: a probabilistic model of consumer choice with substitutes and complements , author=. The Annals of Applied Statistics , volume=. 2020 , pages=

work page 2020

-

[5]

Heiss, F. and McFadden, D. and Winter, J. and Wuppermann, A. and B. Zhou , title =. American Economic Review , volume=

-

[6]

American Economic Journal: Economic Policy , volume=

Power to choose? An analysis of consumer inertia in the residential electricity market , author=. American Economic Journal: Economic Policy , volume=

-

[7]

American Economic Review , volume=

The evolution of brand preferences: Evidence from consumer migration , author=. American Economic Review , volume=

-

[8]

Available at SSRN 3380390 , year=

Consumer inertia and market power , author=. Available at SSRN 3380390 , year=

-

[9]

A logit model of brand choice calibrated on scanner data , author=. Marketing Science , volume=

-

[10]

Decision-making under uncertainty: Capturing dynamic brand choice processes in turbulent consumer goods markets , author=. Marketing Science , volume=

-

[11]

Journal of Business & Economic Statistics , volume=

Modeling heterogeneity and state dependence in consumer choice behavior , author=. Journal of Business & Economic Statistics , volume=

-

[12]

Discrete Choice Methods with Simulation , author=

-

[13]

Frontiers in Econometrics , editor =

McFadden, Daniel , title =. Frontiers in Econometrics , editor =. 1974 , pages =

work page 1974

-

[14]

The Econometrics Journal , volume =

Aguirregabiria, Victor , title =. The Econometrics Journal , volume =

-

[15]

Aguiar, Victor H. and Kashaev, Nail , title =. 2019 , howpublished =. 1907.04853 , archivePrefix=

-

[16]

Aguiar, Victor H. and Kashaev, Nail , title =. Journal of Business & Economic Statistics , volume =

- [17]

-

[18]

Berry, Steven and Levinsohn, James and Pakes, Ariel , title =. Econometrica , volume =

-

[19]

Hoffman, Matthew D. and Blei, David M. and Wang, Chong and Paisley, John , title =. Journal of Machine Learning Research , volume =

- [20]

-

[21]

Kingma, Diederik P. and Welling, Max , title =. Proceedings of the International Conference on Learning Representations (ICLR) , year =

-

[22]

Journal of Statistical Software , volume =

Stan: A probabilistic programming language , author =. Journal of Statistical Software , volume =

-

[23]

The RAND Journal of Economics , volume =

State dependence and alternative explanations for consumer inertia , author =. The RAND Journal of Economics , volume =

- [24]

-

[25]

The RAND Journal of Economics , volume =

Mergers with differentiated products: The case of the ready-to-eat cereal industry , author =. The RAND Journal of Economics , volume =

-

[26]

Matrix Factorization Techniques for Recommender Systems , author =. Computer , volume =

-

[27]

Advances in Neural Information Processing Systems , year =

Probabilistic Matrix Factorization , author =. Advances in Neural Information Processing Systems , year =

-

[28]

Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability , volume =

Statistical inference in factor analysis , author =. Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability , volume =

-

[29]

Bayesian factor analysis and density estimation using a class of factor models , author =. Biometrika , volume =

-

[30]

Sparse Bayesian infinite factor models , author =. Biometrika , volume =

-

[31]

and Kucukelbir, Alp and McAuliffe, Jon D

Blei, David M. and Kucukelbir, Alp and McAuliffe, Jon D. , title =. Journal of the American Statistical Association , volume =

-

[32]

Bayesian Statistics and Marketing , author =

-

[33]

Annual Review of Economics , volume=

The use of scanner data for economics research , author=. Annual Review of Economics , volume=. 2022 , publisher=

work page 2022

-

[34]

RAND Journal of Economics , pages=

Empirically distinguishing informative and prestige effects of advertising , author=. RAND Journal of Economics , pages=

-

[35]

The Review of Economic Studies , volume=

Vertical relationships between manufacturers and retailers: Inference with limited data , author=. The Review of Economic Studies , volume=

-

[36]

Journal of Political Economy , volume=

Vertical contracts with endogenous product selection: An empirical analysis of vendor allowance contracts , author=. Journal of Political Economy , volume=

-

[37]

Common ownership and competition in the ready-to-eat cereal industry , author=. 2021 , institution=

work page 2021

- [38]

-

[39]

Journal of Political Economy , volume=

Rising markups and the role of consumer preferences , author=. Journal of Political Economy , volume=

-

[40]

Journal of Applied Econometrics , volume=

Mixed MNL Models For Discrete Response , author=. Journal of Applied Econometrics , volume=

-

[41]

A Conceptual Introduction to Hamiltonian Monte Carlo , author=. 2018 , eprint=

work page 2018

-

[42]

Estimation of Random Utility Models in

Yves Croissant , journal =. Estimation of Random Utility Models in. 2020 , volume =

work page 2020

-

[43]

Journal of Econometrics , volume=

Bayesian and classical approaches to instrumental variable regression , author=. Journal of Econometrics , volume=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.