Tokenized but Illiquid? Evidence from Real-World Asset Markets

Pith reviewed 2026-06-28 16:23 UTC · model grok-4.3

The pith

Tokenized real-world assets exhibit uneven liquidity, with gold-backed tokens showing broader holder bases and more persistent activity than treasury or credit tokens.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

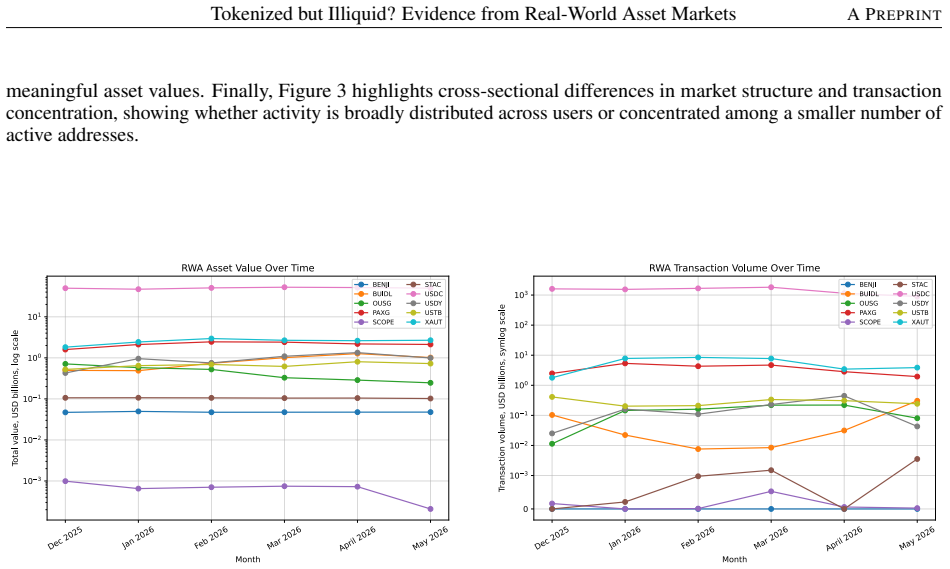

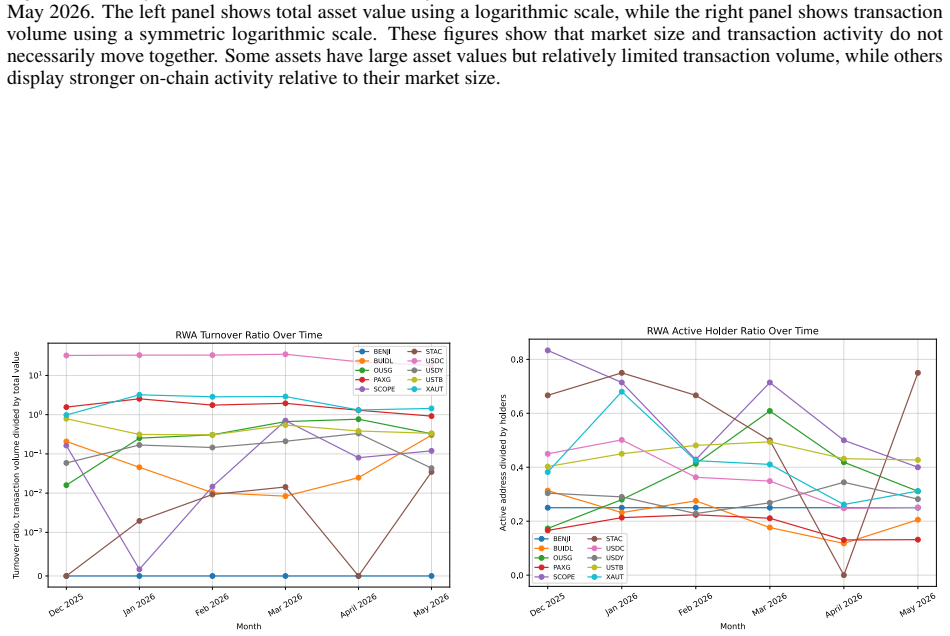

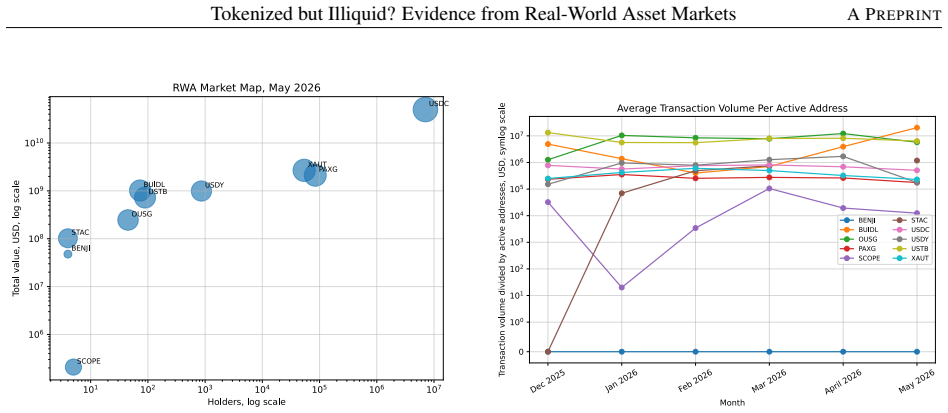

The study finds substantial heterogeneity in observed liquidity across real-world asset categories, with gold-backed tokens exhibiting broader holder bases and more persistent on-chain activity than many treasury and private-credit products, while outstanding asset value alone does not reliably predict liquidity measures such as turnover or active addresses.

What carries the argument

An Ethereum monthly panel of non-stablecoin real-world asset tokens analyzed with liquidity proxies of turnover, active addresses, and active-month indicators through descriptive statistics, group tests, and exploratory panel regressions.

If this is right

- Tokenization and liquidity must be treated as distinct outcomes that require separate measurement.

- Gold-backed tokens produce higher levels of holder engagement and persistence than treasury or private-credit tokens.

- Outstanding asset value functions as an unreliable signal of actual on-chain market activity.

- Category-specific traits shape observed liquidity more strongly than asset scale.

Where Pith is reading between the lines

- Tokenization programs could shift focus toward features that increase holder diversity instead of emphasizing asset volume growth.

- The category differences observed here may appear on other blockchains, pointing to the value of broader network comparisons.

- Platforms and regulators could apply these activity-based metrics to evaluate whether tokenization initiatives achieve their intended market effects.

Load-bearing premise

The liquidity proxies of turnover, active addresses, and active-month indicator accurately capture meaningful observed market activity rather than artifacts of data coverage or wallet behavior.

What would settle it

A replication or alternative data collection showing no meaningful difference in active addresses or turnover between gold-backed tokens and treasury tokens would undermine the reported heterogeneity across categories.

Figures

read the original abstract

Real-world asset tokenization is often presented as a mechanism for improving the liquidity of traditionally illiquid assets. However, on-chain representation and secondary-market liquidity are distinct outcomes. This paper examines whether tokenized real-world assets exhibit meaningful observed liquidity and identifies the token characteristics associated with higher market activity. Using token-level data from RWA.xyz and supplemental contract-level observations from Etherscan, the study constructs an Ethereum-based monthly panel of non-stablecoin real-world assets across three prominent categories: U.S. Treasury-backed tokens, gold-backed commodity tokens, and private-credit-related tokens. Liquidity is measured using turnover, active addresses, and an active-month indicator. The empirical design combines descriptive statistics, non-parametric group tests, and exploratory panel regressions suited to short and sparse token histories. The results show substantial heterogeneity across asset categories. Gold-backed tokens exhibit broader holder bases and more persistent on-chain activity than many Treasury and private-credit-related products, while outstanding asset value alone does not reliably predict observed liquidity. The paper contributes to the literature by developing a clearer empirical measurement framework for real-world-asset liquidity and showing that tokenization and liquidity should be analyzed as distinct outcomes.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper constructs an Ethereum monthly panel of non-stablecoin RWAs from RWA.xyz and Etherscan data across Treasury-backed, gold-backed, and private-credit categories. Liquidity is proxied by turnover, active addresses, and an active-month indicator. Descriptive statistics, non-parametric tests, and exploratory regressions on short/sparse histories show substantial cross-category heterogeneity: gold-backed tokens display broader holder bases and more persistent activity, while outstanding asset value alone does not predict observed liquidity. The central claim is that tokenization and secondary-market liquidity are distinct outcomes.

Significance. If the measurement framework and heterogeneity results hold after robustness checks on data coverage, the paper supplies a useful empirical distinction between on-chain representation and actual market activity for RWAs, with direct implications for token design and market monitoring.

major comments (3)

- [Data and methods] Data and methods section: the claim of comparable liquidity measurement across Treasury, gold, and private-credit tokens rests on RWA.xyz plus Etherscan delivering unbiased turnover and active-address counts, yet the manuscript provides no category-specific audit of contract architectures, bridging patterns, or scraping completeness that could produce differential under-counting.

- [Results] Results section (exploratory regressions): with short and sparse token histories explicitly noted, the panel specifications do not report how missing months or low-activity tokens are handled (e.g., selection into the active-month indicator or fixed-effects structure), leaving the heterogeneity estimates vulnerable to coverage artifacts.

- [Descriptive statistics] Table or figure presenting category-level statistics: sample sizes, number of tokens per category, and fraction of months with non-zero activity are not stated in the abstract or summary statistics, preventing assessment of whether the reported differences in holder bases and persistence are statistically powered.

minor comments (2)

- [Abstract] The abstract states 'supplemental Etherscan observations' without specifying which variables or tokens receive this supplementation or how conflicts with RWA.xyz are resolved.

- [Liquidity measures] Notation for the active-month indicator and turnover definition should be introduced with explicit formulas to aid replication.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify the presentation of our empirical framework. We respond to each major comment below and indicate planned revisions.

read point-by-point responses

-

Referee: [Data and methods] Data and methods section: the claim of comparable liquidity measurement across Treasury, gold, and private-credit tokens rests on RWA.xyz plus Etherscan delivering unbiased turnover and active-address counts, yet the manuscript provides no category-specific audit of contract architectures, bridging patterns, or scraping completeness that could produce differential under-counting.

Authors: We agree that the manuscript would benefit from explicit discussion of potential measurement differences. In revision we will add a dedicated paragraph in the Data and Methods section that reviews the main contract patterns observed via Etherscan for each category (e.g., ERC-20 vs. more complex structures) and notes the reliance on RWA.xyz aggregation. A full independent audit of every bridging path is outside the scope of this exploratory study, but we will flag this as a limitation. revision: partial

-

Referee: [Results] Results section (exploratory regressions): with short and sparse token histories explicitly noted, the panel specifications do not report how missing months or low-activity tokens are handled (e.g., selection into the active-month indicator or fixed-effects structure), leaving the heterogeneity estimates vulnerable to coverage artifacts.

Authors: The referee correctly identifies an omission. We will revise the Results section to state explicitly that the panel is unbalanced, that the active-month indicator equals one only in months with positive turnover or active addresses, and that regressions are estimated with token fixed effects on the observed months. We will also add a short robustness subsection that re-estimates the models after dropping tokens with fewer than three active months. revision: yes

-

Referee: [Descriptive statistics] Table or figure presenting category-level statistics: sample sizes, number of tokens per category, and fraction of months with non-zero activity are not stated in the abstract or summary statistics, preventing assessment of whether the reported differences in holder bases and persistence are statistically powered.

Authors: We accept this point. The revised manuscript will include a new table (or expanded Table 1) reporting, by category, the number of tokens, total token-months, and the share of months with non-zero activity. This information will also be referenced in the abstract and summary statistics section. revision: yes

Circularity Check

No circularity: purely observational empirical study using external data

full rationale

The paper constructs an Ethereum-based monthly panel from RWA.xyz and Etherscan, defines liquidity proxies (turnover, active addresses, active-month indicator), and reports descriptive statistics, non-parametric tests, and exploratory regressions. No equations, fitted parameters, or predictions are derived from the study's own outputs. No self-citations are load-bearing for any core claim. The analysis is self-contained against external benchmarks and does not reduce any result to its inputs by construction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard assumptions underlying non-parametric tests and short-panel regressions (including appropriate treatment of sparse token histories) are satisfied.

Reference graph

Works this paper leans on

-

[1]

World Economic Forum.Asset Tokenization in Financial Markets: The Next Generation of Value Exchange; World Economic Forum: Geneva, Switzerland, 2025

2025

-

[2]

Committee on Payments and Market Infrastructures.Tokenisation in the Context of Money and Other Assets: Concepts and Implications for Central Banks; Bank for International Settlements: Basel, Switzerland, 2024

2024

-

[3]

Agur, I.; Villegas-Bauer, G.; Mancini-Griffoli, T.; Martinez Peria, M.S.; Tan, B.Tokenization and Financial Market Inefficiencies; IMF Fintech Note 2025/001; International Monetary Fund: Washington, DC, USA, 2025

2025

-

[4]

752; OECD Publishing: Paris, France, 2025

Nassr, I.K.Tokenisation of Assets and Distributed Ledger Technologies in Financial Markets: Potential Imped- iments to Market Development and Policy Implications; OECD Business and Finance Policy Papers No. 752; OECD Publishing: Paris, France, 2025. https://doi.org/10.1787/bf84ff64-en

-

[5]

Financial Stability Board.The Financial Stability Implications of Tokenisation; Financial Stability Board: Basel, Switzerland, 2024

2024

-

[6]

International Organization of Securities Commissions.Tokenization of Financial Assets; FR/17/2025; IOSCO: Madrid, Spain, 2025

2025

-

[7]

Carapella, F.; Chuan, G.; Gerszten, J.; Hunter, C.; Swem, N. Tokenization: Overview and Financial Stability Implications.Finance and Economics Discussion Series2023,2023-060. https://doi.org/10.17016/FEDS.2023.060. 10 Tokenized but Illiquid? Evidence from Real-World Asset MarketsA PREPRINT

-

[8]

Swinkels, L. Empirical evidence on the ownership and liquidity of real estate tokens.Financial Innovation2023, 9, 45. https://doi.org/10.1186/s40854-022-00427-5

-

[9]

Kreppmeier, J.; Laschinger, R.; Steininger, B.I.; Dorfleitner, G. Real estate security token offerings and the secondary market: Driven by crypto hype or fundamentals?Journal of Banking & Finance2023,154, 106940. https://doi.org/10.1016/j.jbankfin.2023.106940

-

[10]

Laschinger, R.; Leonhard, H.; Dorfleitner, G.; Schäfers, W.Liquidity Mechanisms in Real-World Assets: The Empirical Case of Real Estate Tokenization; SSRN Working Paper 5036350, 2024

2024

-

[11]

1311; Bank for International Settlements: Basel, Switzerland, 2025

Cornelli, G.When Bricks Meet Bytes: Does Tokenisation Fill Gaps in Traditional Real Estate Markets?; BIS Working Papers No. 1311; Bank for International Settlements: Basel, Switzerland, 2025

2025

-

[12]

Available online:https://app.rwa.xyz/ (accessed on 31 May 2026

RW A.xyz.Analytics on Tokenized Real-World Assets. Available online:https://app.rwa.xyz/ (accessed on 31 May 2026

2026

-

[13]

Available online: https://etherscan.io/ (accessed on 31 May 2026)

Etherscan.Ethereum Blockchain Explorer. Available online: https://etherscan.io/ (accessed on 31 May 2026). 11

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.