Sparse Tree-Based Aggregation for Time Series Regressions

Pith reviewed 2026-06-28 07:51 UTC · model grok-4.3

The pith

StarTime uses a temporal tree to aggregate lags at varying frequencies and reduce dimensionality in high-order time series regressions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

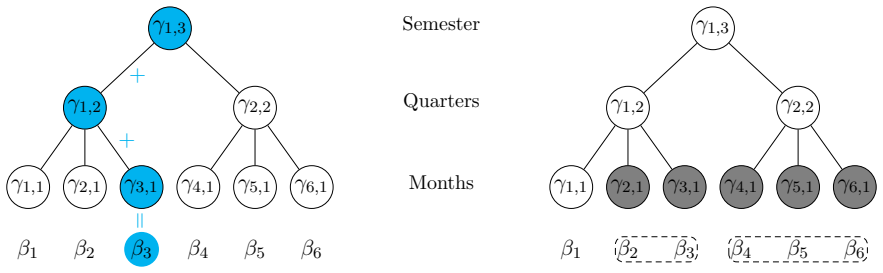

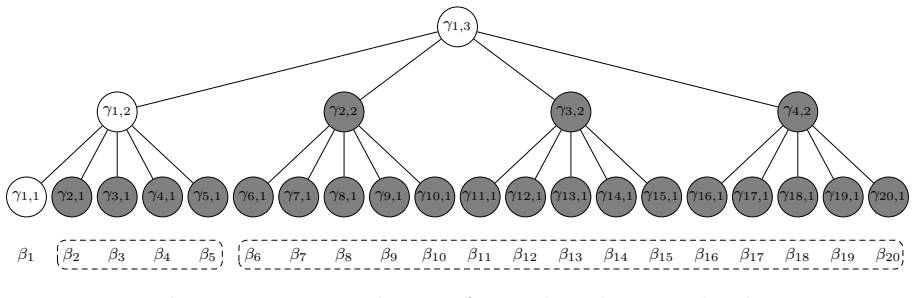

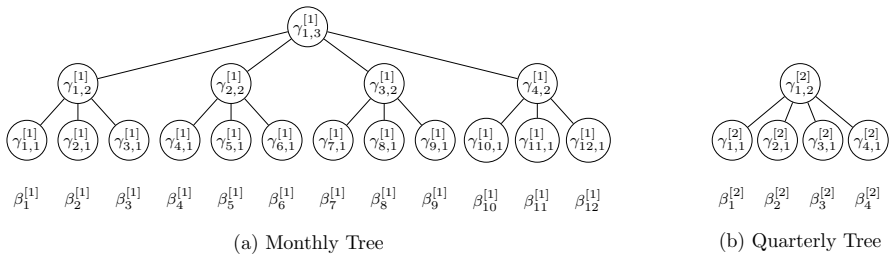

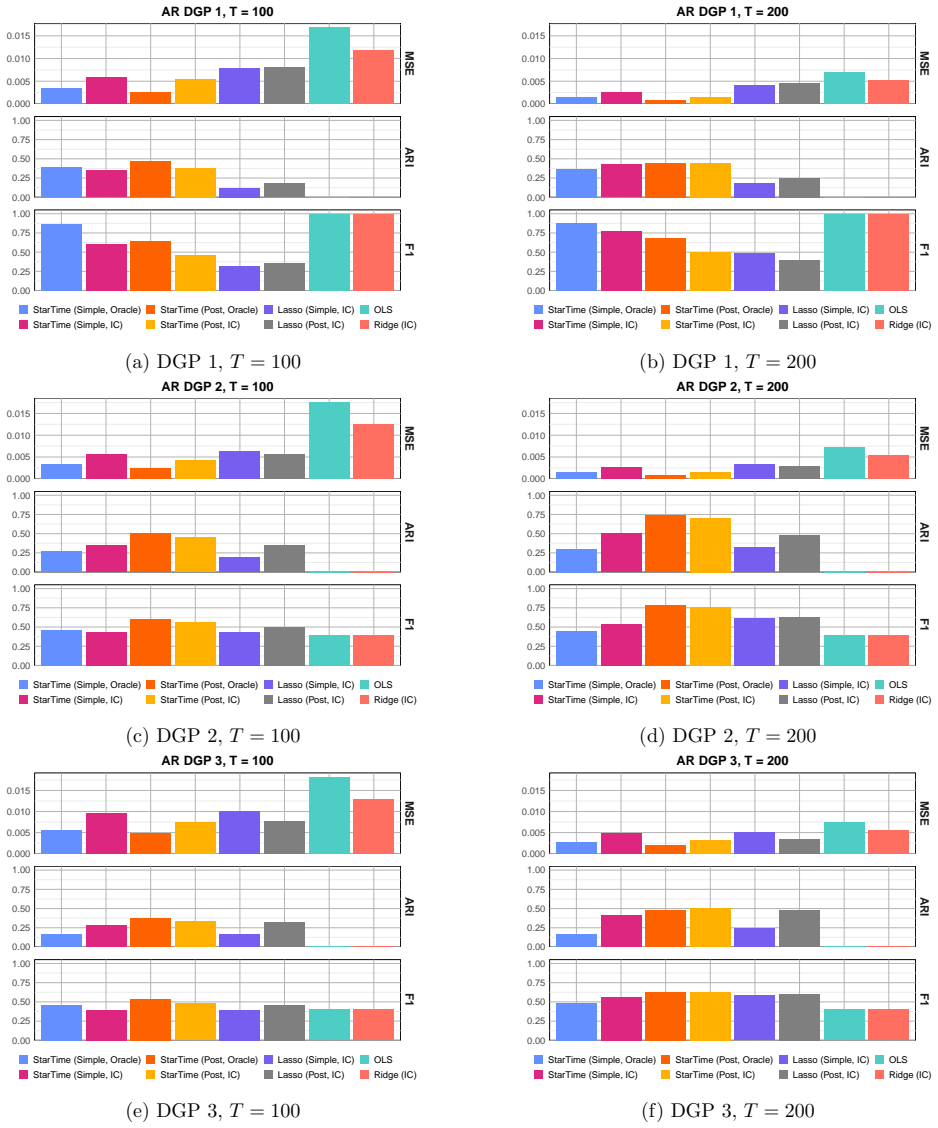

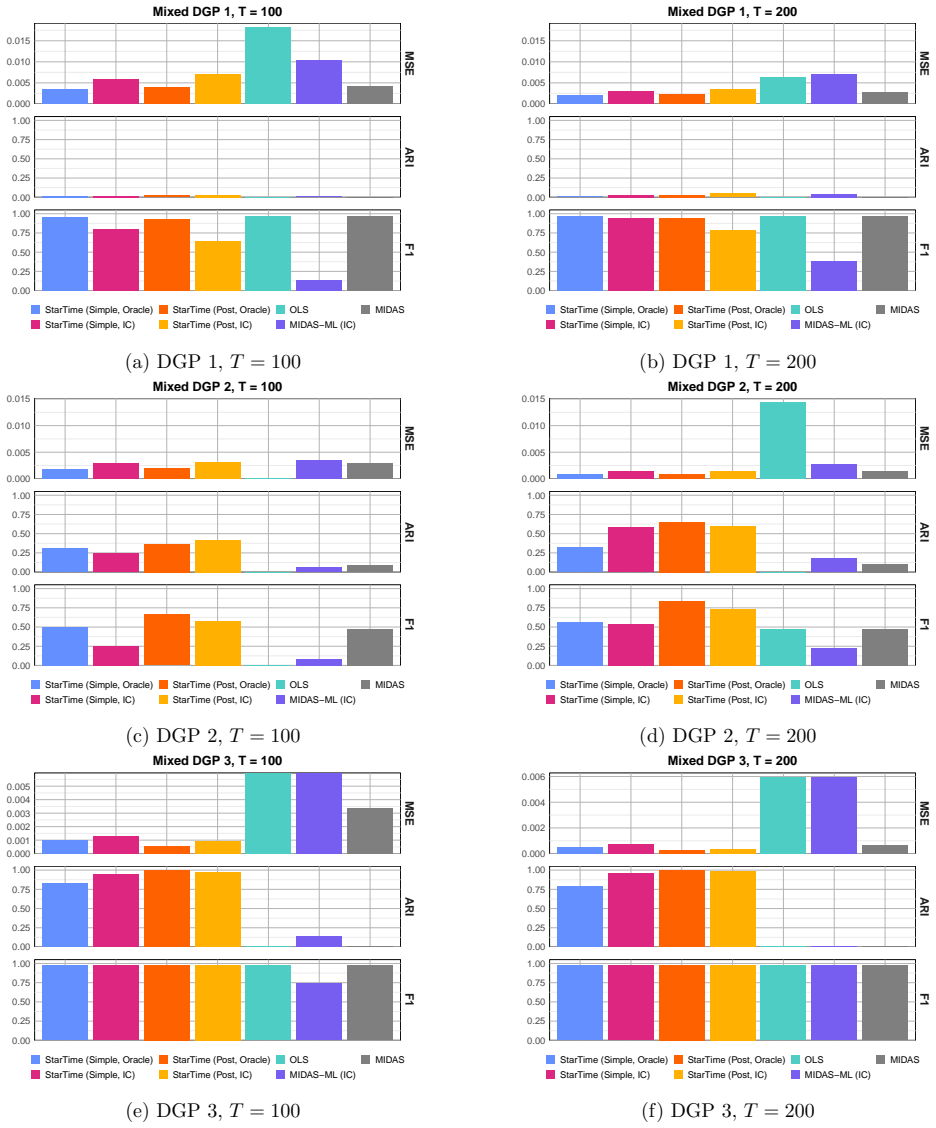

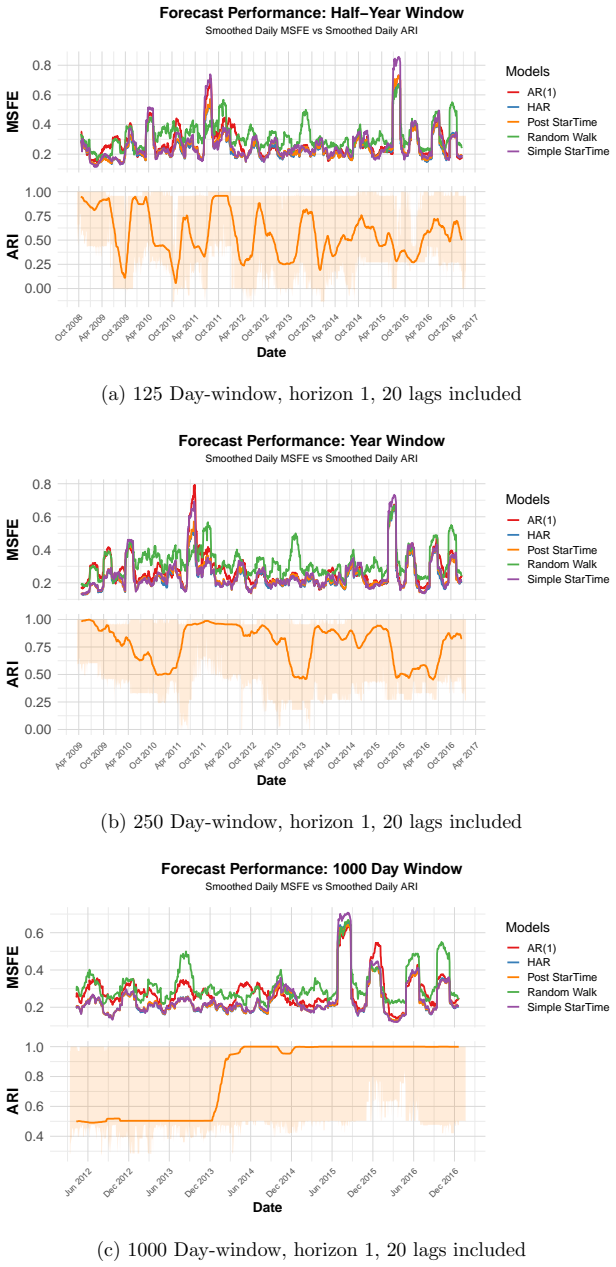

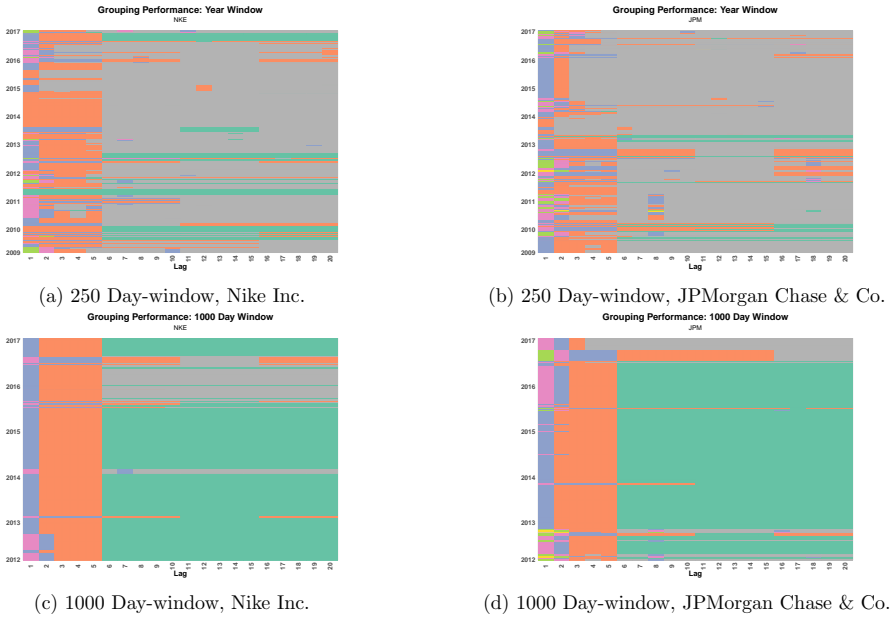

StarTime is a convex penalization method that arranges lags hierarchically in a temporal tree from high to low frequency and then selects which coefficients to aggregate at possibly different frequencies, to sparsify, or to combine both operations, delivering new error bounds for estimation accuracy in high-order autoregressions and mixed-frequency regressions.

What carries the argument

The temporal tree that organizes lags from high to low frequency so that the penalization can select aggregation at chosen nodes or sparsity.

If this is right

- Improved finite-sample estimation accuracy and recovery of both aggregation patterns and sparsity relative to standard benchmarks.

- New theoretical error bounds that justify the use of tree-structured aggregation in high-dimensional time series settings.

- Direct applicability to financial and macroeconomic regressions that mix high-frequency and low-frequency variables.

- Flexible selection of aggregation levels that can vary across different parts of the lag structure.

Where Pith is reading between the lines

- The same tree logic could be adapted to spatial or network data where observations have a natural hierarchical scale.

- StarTime might be combined with existing mixed-frequency nowcasting tools to handle real-time data releases without manual lag truncation.

- If the tree is misspecified in practice, a data-driven way to learn the hierarchy itself would be a natural next step.

Load-bearing premise

The temporal tree correctly reflects the true hierarchical frequency relationships among lags so that aggregation at selected nodes preserves the underlying dynamics.

What would settle it

A Monte Carlo experiment in which the data-generating process has lag relationships that violate the assumed tree hierarchy and StarTime then produces higher mean squared error than ordinary lasso or the unaggregated model.

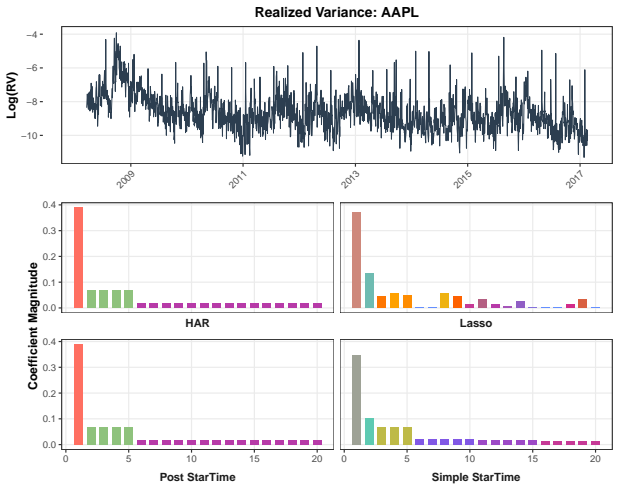

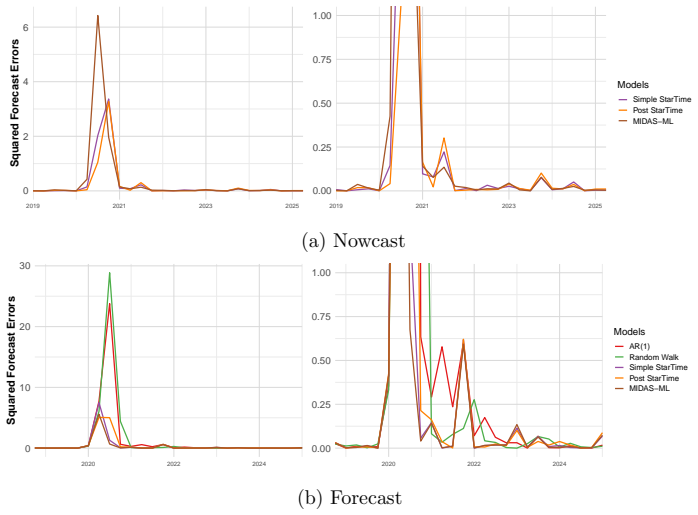

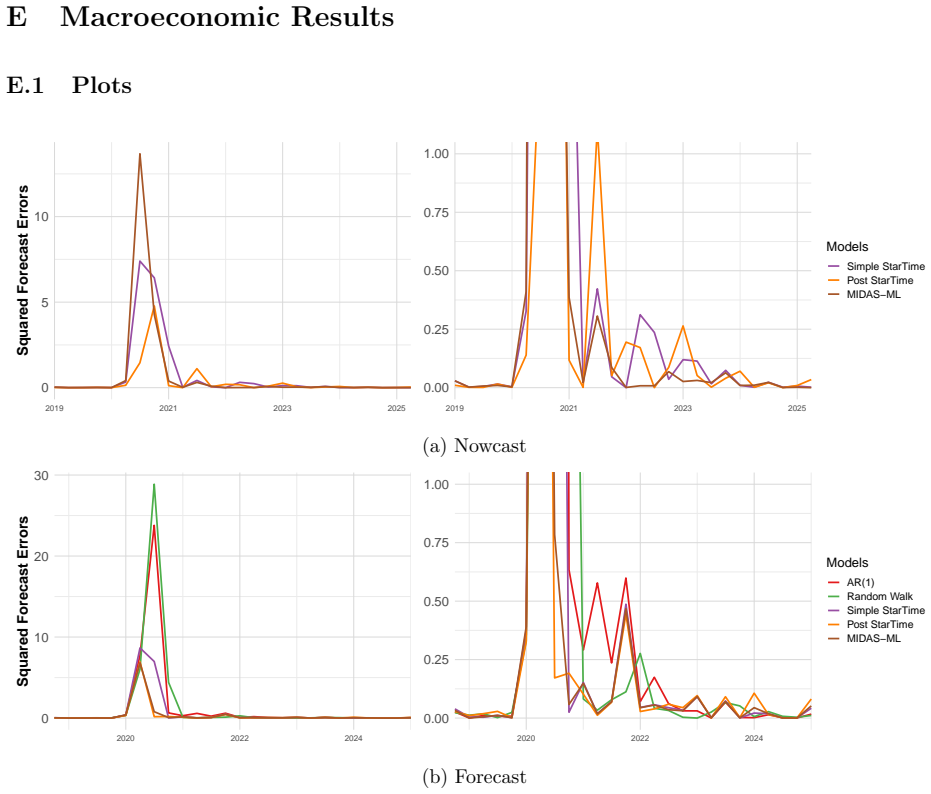

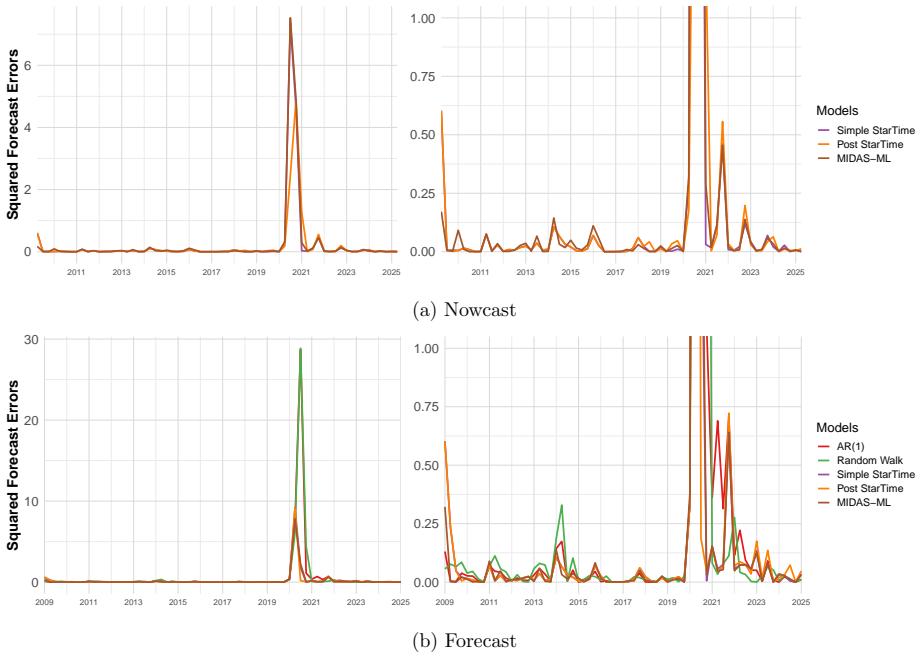

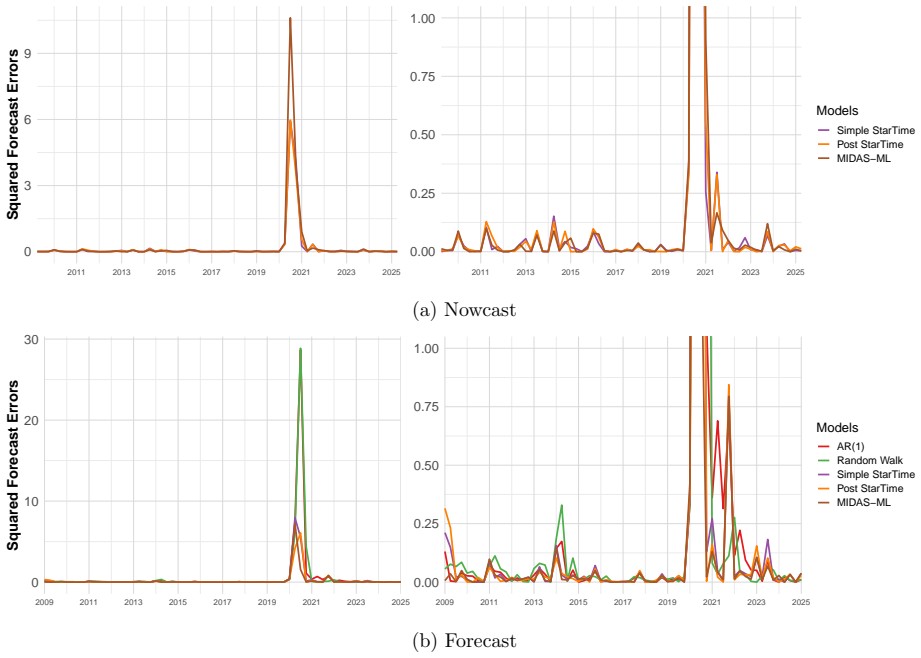

Figures

read the original abstract

High-dimensional time series regressions are often regularized to produce sparse coefficients. We show that temporal aggregation provides a powerful alternative to reduce dimensionality in high-order autoregressions and mixed-frequency regressions. To this end, we propose StarTime (Sparse Tree-based Aggregation for Time Series), a convex penalization method that uses a temporal tree to arrange lags hierarchically from high to low frequency. StarTime then flexibly selects coefficients to be aggregated at possibly varying frequencies, sparse or a combination thereof. We provide new error bounds for StarTime, demonstrate improved estimation accuracy and recovery of aggregation and sparsity in simulations relative to benchmarks, and illustrate StarTime's relevance for financial and macroeconomic applications.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes StarTime, a convex penalization method for high-dimensional time series regressions that arranges lags in a temporal tree from high to low frequency and selects coefficients for aggregation at varying frequencies (or sparsity, or combinations thereof). It claims this reduces dimensionality in high-order autoregressions and mixed-frequency regressions, provides new error bounds, and yields improved estimation accuracy and recovery of aggregation/sparsity patterns relative to benchmarks in simulations, with relevance to financial and macroeconomic applications.

Significance. If the error bounds hold under the stated conditions and the simulation results are robust, the method offers a structured alternative to standard regularization by exploiting temporal hierarchies for dimensionality reduction. The explicit combination of aggregation and sparsity via tree-based penalization is a clear strength, as is the provision of new theoretical bounds (when verified) and the reproducible simulation benchmarks.

minor comments (2)

- [Abstract] The abstract states that 'new error bounds' are provided, but without a named section or equation reference in the provided material it is unclear whether these are derived under the same assumptions as the tree construction; adding an explicit statement of the bound (e.g., in the theory section) would strengthen the central claim.

- The simulation section should clarify whether aggregation levels are chosen ex ante or involve any post-hoc selection, as this directly affects the interpretation of the reported accuracy gains over benchmarks.

Simulated Author's Rebuttal

We thank the referee for the positive assessment of our manuscript, the accurate summary of StarTime's contributions, and the recommendation for minor revision. No specific major comments were raised in the report.

Circularity Check

No significant circularity detected

full rationale

The paper introduces StarTime as a new convex penalization method based on a temporal tree structure for aggregating lags in high-dimensional time series regressions. It claims new error bounds derived from the method's formulation and validates performance via external simulations and applications. No load-bearing step in the abstract or described claims reduces by construction to fitted parameters, self-citations, or renamed inputs; the derivation chain appears self-contained with independent theoretical and empirical content.

Axiom & Free-Parameter Ledger

free parameters (1)

- penalty tuning parameter

axioms (1)

- domain assumption The temporal tree arranges lags hierarchically from high to low frequency without loss of information for the regression problem.

Reference graph

Works this paper leans on

-

[1]

Journal of Financial Econometrics , volume=

A simple approximate long-memory model of realized volatility , author=. Journal of Financial Econometrics , volume=

-

[2]

Andersen, T. G. and Bollerslev, T. and Diebold, F. X. and Labys, P. , year =. Modeling and forecasting realized volatility , journal =

-

[3]

and Santa-Clara, P

Ghysels, E. and Santa-Clara, P. and Valkanov, R. , year =. The

-

[4]

The realized Laplace transform of volatility , volume =

Todorov, Viktor and Tauchen, George , year =. The realized Laplace transform of volatility , volume =. Econometrica , doi =

-

[5]

, title =

Litvinova, J. , title =. 2003 , note =

2003

-

[6]

Leverage and volatility feedback effects in high-frequency data , volume =

Bollerslev, Tim and Litvinova, Julia and Tauchen, George , year =. Leverage and volatility feedback effects in high-frequency data , volume =. Journal of Financial Econometrics , doi =

-

[7]

Nowcasting: The real-time informational content of macroeconomic data , journal =. 2008 , issn =. doi:https://doi.org/10.1016/j.jmoneco.2008.05.010 , url =

-

[8]

Temporal aggregation and economic time series , volume =

Rossana, Robert and Seater, John , year =. Temporal aggregation and economic time series , volume =

-

[9]

A comparison of MIDAS and bridge equations , journal =

Christian Schumacher , keywords =. A comparison of MIDAS and bridge equations , journal =. 2016 , issn =. doi:https://doi.org/10.1016/j.ijforecast.2015.07.004 , url =

-

[10]

Temporal aggregation of univariate and multivariate time series models: A survey , volume =

Veredas, David and Silvestrini, Andrea , year =. Temporal aggregation of univariate and multivariate time series models: A survey , volume =. Journal of Economic Surveys , doi =

-

[11]

Wu , journal =

Takeshi Amemiya and Roland Y. Wu , journal =. The effect of aggregation on prediction in the autoregressive model , urldate =

-

[12]

Some consequences of temporal aggregation and systematic sampling for ARMA and ARMAX models , journal =. 1973 , issn =. doi:https://doi.org/10.1016/0304-4076(73)90015-8 , url =

-

[13]

G. C. Tiao , journal =. Asymptotic behaviour of temporal aggregates of time series , urldate =

-

[14]

Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =

Zou, Hui and Hastie, Trevor , title = ". Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =. 2005 , month =. doi:10.1111/j.1467-9868.2005.00503.x , url =

-

[15]

On the use of high frequency measures of volatility in MIDAS regressions , journal =. 2016 , issn =. doi:https://doi.org/10.1016/j.jeconom.2016.04.012 , url =

-

[16]

Journal of the American Statistical Association , volume =

Xiaohan Yan and Jacob Bien , title =. Journal of the American Statistical Association , volume =. 2021 , publisher =. doi:10.1080/01621459.2020.1796677 , URL =

-

[17]

Journal of Machine Learning Research , volume=

Tree-based node aggregation in sparse graphical models , author=. Journal of Machine Learning Research , volume=. 2022 , author+an=

2022

-

[18]

Journal of Business & Economic Statistics , volume=

Machine learning time series regressions with an application to nowcasting , author=. Journal of Business & Economic Statistics , volume=. 2022 , publisher=

2022

-

[19]

Foundations and Trends in Machine Learning , volume=

Distributed optimization and statistical learning via the alternating direction method of multipliers , author=. Foundations and Trends in Machine Learning , volume=. 2011 , publisher=

2011

-

[20]

Journal of Classification , volume=

Comparing partitions , author=. Journal of Classification , volume=. 1985 , publisher=

1985

-

[21]

Journal of Statistical Software , year =

Regularization paths for generalized linear models via coordinate descent , author =. Journal of Statistical Software , year =

-

[22]

Mixed frequency data sampling regression models: The

Eric Ghysels and Virmantas Kvedaras and Vaidotas Zemlys , journal =. Mixed frequency data sampling regression models: The. 2016 , volume =

2016

-

[23]

2022 , note =

midasml: Estimation and prediction methods for high-dimensional mixed frequency time series data , author =. 2022 , note =

2022

-

[24]

2011 , publisher =

Statistics for high-dimensional data: Methods, theory and applications , author =. 2011 , publisher =

2011

-

[25]

and Molstad, A

Fu, J. and Molstad, A. J. and Zou, H. , year =. A direct approach to tree-guided feature aggregation for high-dimensional regression , howpublished =

-

[26]

2025 , url =

R: A Language and Environment for Statistical Computing , author =. 2025 , url =

2025

-

[27]

Journal of the American Statistical Association , year =

Data-driven tuning parameter selection for high-dimensional vector autoregressions , author =. Journal of the American Statistical Association , year =

-

[28]

Regression shrinkage and selection via the lasso , urldate =

Robert Tibshirani , journal =. Regression shrinkage and selection via the lasso , urldate =

-

[29]

Hoerl, A. E. and Kennard, R. W. , year =. Ridge regression: Biased estimation for nonorthogonal problems , journal =. doi:10.1080/00401706.1970.10488634 , url =

-

[30]

Extended BIC for small- n -large- P sparse GLM , urldate =

Jiahua Chen and Zehua Chen , journal =. Extended BIC for small- n -large- P sparse GLM , urldate =

-

[31]

HARd to beat: The overlooked impact of rolling windows in the era of machine learning , journal =. 2026 , pages =. doi:https://doi.org/10.1016/j.ijforecast.2025.06.003 , url =

-

[32]

Journal of Financial Econometrics , volume =

Hecq, Alain and Margaritella, Luca and Smeekes, Stephan , title =. Journal of Financial Econometrics , volume =. 2023 , doi =

2023

-

[33]

Journal of Statistical Software , year =

Stephan Smeekes and Ines Wilms , title =. Journal of Statistical Software , year =. doi:10.18637/jss.v106.i12 , url =

-

[34]

Journal of Computational and Graphical Statistics , volume =

Alain Hecq and Marie Ternes and Ines Wilms , title =. Journal of Computational and Graphical Statistics , volume =. 2022 , publisher =. doi:10.1080/10618600.2022.2058003 , URL =

-

[35]

Journal of Business & Economic Statistics , volume=

FRED-MD: A Monthly Database for Macroeconomic Research , author=. Journal of Business & Economic Statistics , volume=. 2016 , publisher=. doi:10.1080/07350015.2015.1086655 , url=

-

[36]

The Quarterly Journal of Economics , volume=

Measuring economic policy uncertainty , author=. The Quarterly Journal of Economics , volume=. 2016 , publisher=

2016

-

[37]

Taylor, Nick , year =. Forecasting returns in the. International Journal of Forecasting , volume =. doi:10.1016/j.ijforecast.2019.01.009 , url =

-

[38]

Amburgey, Aaron J. and McCracken, Michael W. , title =. Journal of Applied Econometrics , volume =. doi:https://doi.org/10.1002/jae.2943 , url =. https://onlinelibrary.wiley.com/doi/pdf/10.1002/jae.2943 , abstract =

-

[39]

Andrew J. Patton , keywords =. Volatility forecast comparison using imperfect volatility proxies , journal =. 2011 , note =. doi:https://doi.org/10.1016/j.jeconom.2010.03.034 , url =

-

[40]

2026 , howpublished =

Economic Policy Uncertainty Index , author =. 2026 , howpublished =

2026

-

[41]

Econometrica , volume =

The model confidence set , author =. Econometrica , volume =. 2011 , publisher =

2011

-

[42]

Journal of Business & Economic Statistics , volume =

Comparing predictive accuracy , author =. Journal of Business & Economic Statistics , volume =. 1995 , publisher =

1995

-

[43]

and Watson, Mark W

Stock, James H. and Watson, Mark W. , journal=. Why has. 2007 , publisher=

2007

-

[44]

and Watson, Mark W

Marcellino, Massimiliano and Stock, James H. and Watson, Mark W. , journal=. A comparison of direct and iterated multistep. 2006 , publisher=

2006

-

[45]

New housing registrations as a leading indicator of the

Cheung, Calista and Granovsky, Dmitry , year=. New housing registrations as a leading indicator of the

-

[46]

2024 , howpublished =

Cortes, Gustavo and LaPoint, Cameron , title =. 2024 , howpublished =

2024

-

[47]

Economic Perspectives , volume=

Monitoring financial stability: A financial conditions index approach , author=. Economic Perspectives , volume=. 2011 , publisher=

2011

-

[48]

NBER Macroeconomics Annual 1989, Volume 4 , pages=

New indexes of coincident and leading economic indicators , author=. NBER Macroeconomics Annual 1989, Volume 4 , pages=. 1989 , publisher=

1989

-

[49]

2025 , howpublished=

Business cycle dating procedure: Frequently asked questions , author=. 2025 , howpublished=

2025

-

[50]

Journal of Economic Literature , volume=

Forecasting volatility in financial markets: A review , author=. Journal of Economic Literature , volume=. 2003 , publisher=

2003

-

[51]

Unrestricted mixed data sampling (

Foroni, Claudia and Marcellino, Massimiliano and Schumacher, Christian , journal=. Unrestricted mixed data sampling (. 2015 , publisher=

2015

-

[52]

Statistical learning with sparsity: The lasso and generalizations , author=. 2015 , edition =. doi:10.1201/b18401 , url =

-

[53]

Journal of Econometrics , volume =

Lasso inference for high-dimensional time series , author =. Journal of Econometrics , volume =. 2023 , issn =

2023

-

[54]

Journal of Econometrics , volume=

An automated approach towards sparse single-equation cointegration modelling , author=. Journal of Econometrics , volume=. 2021 , publisher=

2021

-

[55]

Journal of Econometrics , volume=

Bayesian MIDAS penalized regressions: Estimation, selection, and prediction , author=. Journal of Econometrics , volume=. 2021 , publisher=

2021

-

[56]

Journal of Economic Surveys , volume=

Machine learning advances for time series forecasting , author=. Journal of Economic Surveys , volume=. 2023 , publisher=

2023

-

[57]

Econometric reviews , volume=

MIDAS regressions: Further results and new directions , author=. Econometric reviews , volume=. 2007 , publisher=

2007

-

[58]

Econometric Reviews , volume=

Lassoing the HAR model: A model selection perspective on realized volatility dynamics , author=. Econometric Reviews , volume=. 2016 , publisher=

2016

-

[59]

International Journal of Forecasting , volume=

The impact of sentiment and attention measures on stock market volatility , author=. International Journal of Forecasting , volume=. 2020 , publisher=

2020

-

[60]

Journal of Financial Econometrics , volume=

A machine learning approach to volatility forecasting , author=. Journal of Financial Econometrics , volume=. 2023 , publisher=

2023

-

[61]

Journal of Financial Econometrics , volume=

Volatility forecasting with machine learning and intraday commonality , author=. Journal of Financial Econometrics , volume=. 2024 , publisher=

2024

-

[62]

Journal of Financial Econometrics , volume=

When MIDAS meets LASSO: The power of low-frequency variables in forecasting value-at-risk and expected shortfall , author=. Journal of Financial Econometrics , volume=. 2025 , publisher=

2025

-

[63]

Journal of Financial Econometrics , volume=

High-dimensional Granger causality tests with an application to VIX and news , author=. Journal of Financial Econometrics , volume=. 2024 , publisher=

2024

-

[64]

Journal of Machine Learning Research , volume=

High dimensional forecasting via interpretable vector autoregression , author=. Journal of Machine Learning Research , volume=

-

[65]

Statistical Science , number =

Xiaohan Yan and Jacob Bien , title =. Statistical Science , number =. 2017 , doi =

2017

-

[66]

Journal of Econometrics , volume=

_1 -regularization of high-dimensional time-series models with non-Gaussian and heteroskedastic errors , author=. Journal of Econometrics , volume=. 2016 , publisher=

2016

-

[67]

1992 , publisher=

Business cycles: Theory, history, indicators, and forecasting , author=. 1992 , publisher=

1992

-

[68]

Journal of Economic Surveys , volume=

The resurgence of inventory research: What have we learned? , author=. Journal of Economic Surveys , volume=

-

[69]

Bernardi, M. and Catania, L. , title =. International Journal of Computational Economics and Econometrics , year =. doi:10.1504/IJCEE.2018.091037 , url =

-

[70]

Automatic time series forecasting: The forecast package for

Rob J Hyndman and Yeasmin Khandakar , journal =. Automatic time series forecasting: The forecast package for. 2008 , doi =

2008

-

[71]

, year =

Leamer, Edward E. , year =. Housing is the business cycle , type =

-

[72]

and Ng, Serena , title =

McCracken, Michael W. and Ng, Serena , title =. Federal Reserve Bank of. 2021 , volume =

2021

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.