Matrix Approximation of Bachelier Option Prices and Greeks under Stochastic Volatility models

Pith reviewed 2026-06-25 19:32 UTC · model grok-4.3

The pith

A linear algebra method computes Bachelier option prices and Greeks for infinitely many strikes from a fixed set of expectations.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under stochastic volatility Bachelier-type models, the option price and its Greeks admit a matrix representation that isolates strike dependence; consequently a finite number of expectations suffices to recover the full price and Greek surfaces inside a stated interval of convergence.

What carries the argument

The matrix approximation of the Bachelier pricing operator obtained through elementary linear algebra, which encodes the model expectations once and then evaluates them at any strike by matrix-vector multiplication.

If this is right

- Prices and Greeks for any number of strikes are obtained from the same fixed number of expectations.

- An explicit convergence interval is supplied for the SABR model.

- The same finite-expectation procedure applies to the rough Bergomi model.

- Greeks are recovered at the same computational cost as the prices themselves.

Where Pith is reading between the lines

- The fixed-cost structure could make repeated surface recalibrations practical in trading systems.

- Analogous matrix factorizations might be tested on other convex payoffs beyond vanilla calls and puts.

- Error bounds derived from the matrix norm could be used to choose the number of expectations in advance.

Load-bearing premise

The asset-price process must be a stochastic volatility Bachelier-type model for which the matrix approximation converges inside the interval of interest.

What would settle it

For the SABR model, evaluate the matrix approximation and the true prices at strikes lying outside the derived convergence range and check whether the difference exceeds ordinary numerical tolerance.

Figures

read the original abstract

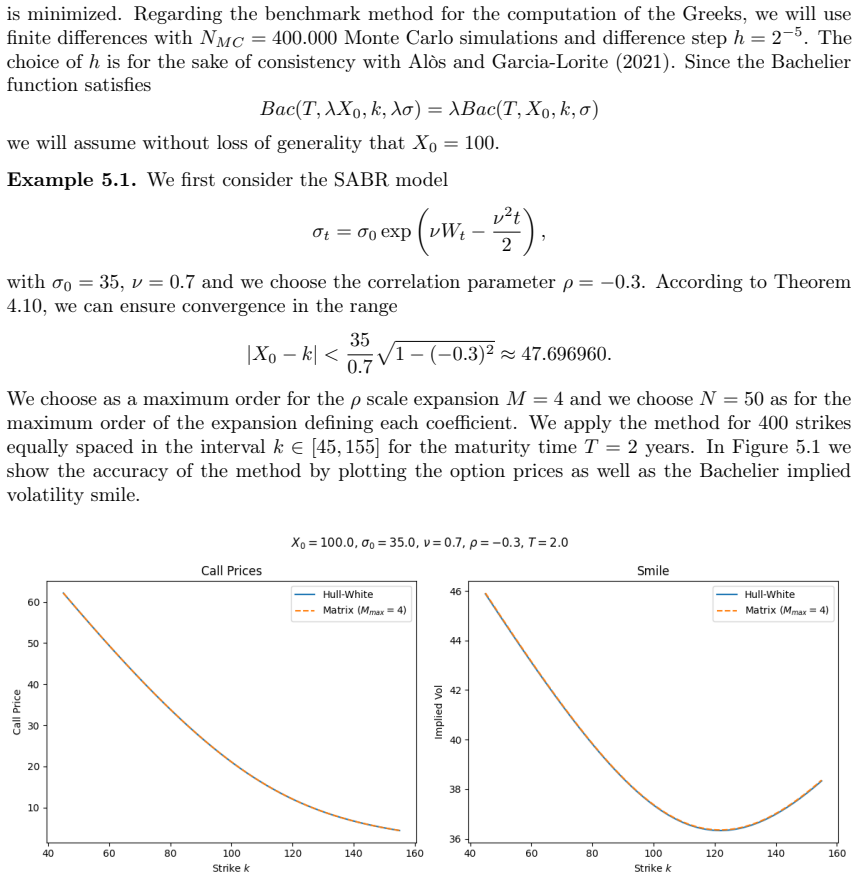

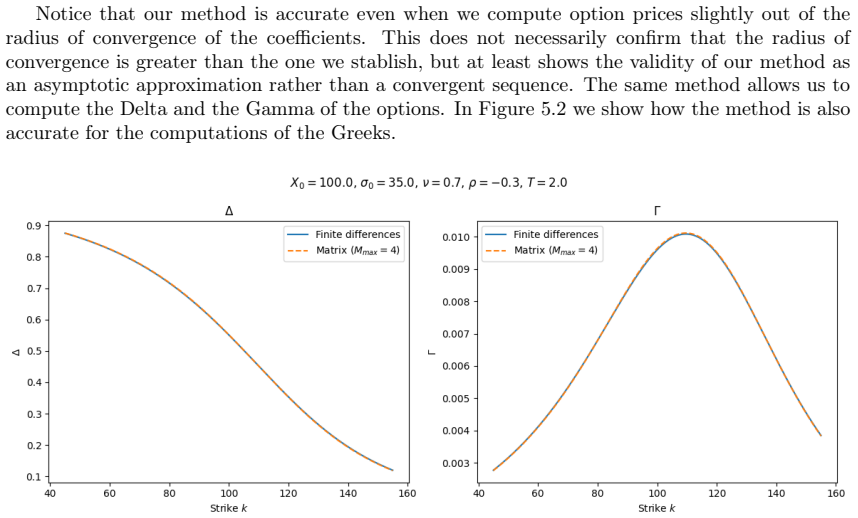

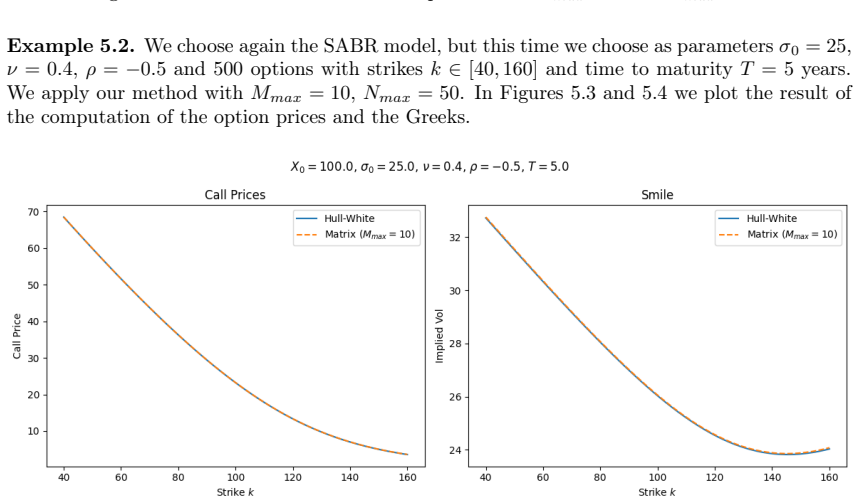

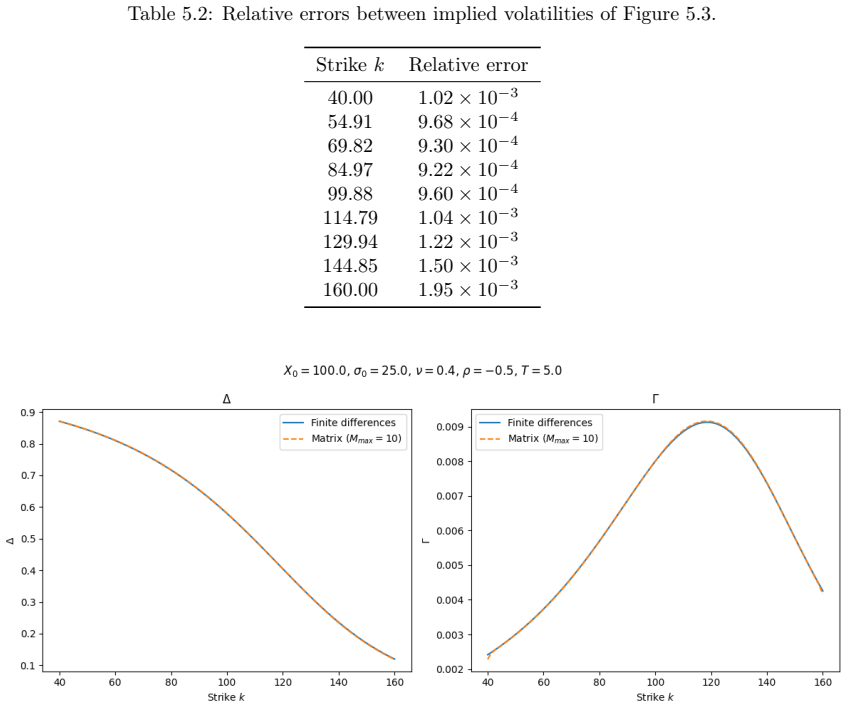

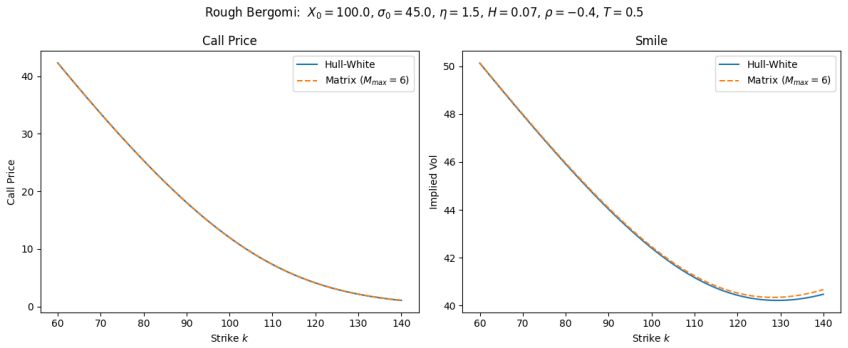

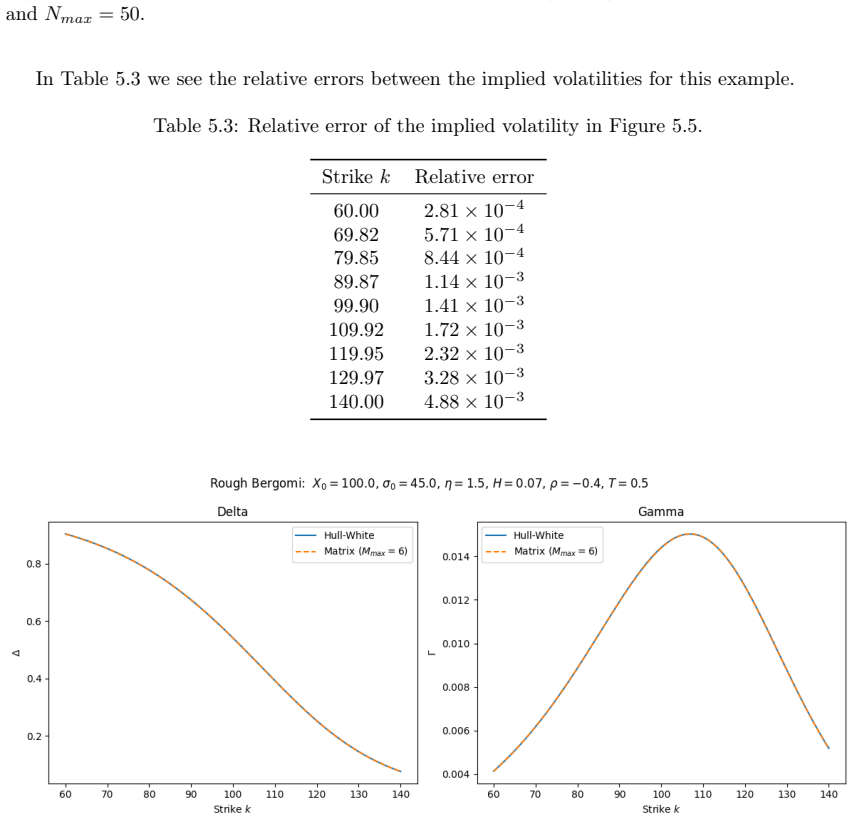

In this paper, we present a numerical method for option pricing and the computation of Greeks under stochastic volatility Bachelier-type models, based on elementary linear algebra. The method allows option prices and Greeks to be computed for infinitely many strikes (within a range of convergence) by evaluating only a finite number of expectations, independent of the number of strikes. For the SABR model, we derive an explicit range of convergence. Numerical examples are provided for both the SABR and the rough Bergomi models.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents a numerical method based on elementary linear algebra for computing Bachelier option prices and Greeks under stochastic volatility models. The central claim is that prices and Greeks for infinitely many strikes (within a derived range of convergence) can be obtained from only a finite number of expectations whose results are then combined via matrix operations, independent of strike count. An explicit convergence interval is supplied for the SABR model, and numerical illustrations are given for both SABR and rough Bergomi.

Significance. If the linear-algebra reduction and convergence statements hold, the method offers a practical efficiency gain for repeated pricing and Greek calculations across strike grids in models without closed forms. The explicit SABR convergence range is a concrete strength that supports falsifiable use of the technique.

minor comments (2)

- [Abstract / Introduction] The abstract states that an explicit range of convergence is derived for SABR; the introduction or §2 should restate this range with the precise conditions on model parameters so readers can immediately assess applicability.

- [Numerical examples] Numerical examples for SABR and rough Bergomi are mentioned; the corresponding section should include a table or figure comparing the matrix method against a benchmark (e.g., Monte Carlo) with reported error metrics and timings to quantify the claimed independence from strike count.

Simulated Author's Rebuttal

We thank the referee for their positive summary of the manuscript and for recommending minor revision. The report correctly identifies the core contribution of the linear-algebra reduction that yields prices and Greeks for infinitely many strikes from a finite set of expectations, together with the explicit SABR convergence interval. No major comments were raised.

Circularity Check

No significant circularity; derivation is self-contained linear algebra

full rationale

The paper frames its core contribution as a matrix-based numerical method grounded in elementary linear algebra properties, allowing reuse of a finite set of expectations across infinitely many strikes within a derived convergence range (explicitly supplied for SABR). No load-bearing steps reduce by construction to fitted parameters, self-definitions, or self-citation chains; the abstract and description present the approach as independent of the target quantities and externally verifiable via the stated convergence interval and numerical examples for SABR and rough Bergomi. This qualifies as a normal non-finding of circularity.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Quantitative Finance , volume =

Elisa Alòs and Jim Gatheral and Radoš Radoičić , title =. Quantitative Finance , volume =. 2020 , publisher =

2020

-

[2]

Finance and Stochastics , volume =

Elisa Al. Finance and Stochastics , volume =. 2007 , publisher =

2007

-

[3]

arXiv preprint arXiv:2506.08067 , year=

Smile asymptotic for Bachelier Implied Volatility , author=. arXiv preprint arXiv:2506.08067 , year=

-

[4]

Malliavin Calculus in Finance: Theory and Practice , publisher =

Elisa Al. Malliavin Calculus in Finance: Theory and Practice , publisher =

-

[5]

Sato, Ken-Iti , journal=

-

[6]

Communications on Stochastic Analysis , volume =

Hossein Jafari and Josep Vives , title =. Communications on Stochastic Analysis , volume =

-

[7]

International Journal of Theoretical and Applied Finance , FJOURNAL =

Al\`os, Elisa and Nualart, Eulalia and Pravosud, Makar , TITLE =. International Journal of Theoretical and Applied Finance , FJOURNAL =. 2024 , NUMBER =. doi:10.1142/S0219024925500037 , URL =

-

[8]

Wilmott , volume =

Peter J. Wilmott , volume =. 2017 , publisher =

2017

-

[9]

Journal of Futures Markets , volume =

Choi, Jaehyuk and Kwak, Minsuk and Tee, Chyng Wen and Wang, Yumeng , title =. Journal of Futures Markets , volume =. doi:https://doi.org/10.1002/fut.22315 , url =

-

[10]

arXiv preprint arXiv:2211.10232 , year=

On the Bachelier implied volatility at extreme strikes , author=. arXiv preprint arXiv:2211.10232 , year=

-

[11]

Al\`os, Elisa and Bur\'. Short-. SIAM J. Financial Math. , FJOURNAL =. 2026 , NUMBER =. doi:10.1137/25M1776615 , URL =

-

[12]

Finance and Stochastics , volume=

A decomposition formula for option prices in the Heston model and applications to option pricing approximation , author=. Finance and Stochastics , volume=. 2012 , publisher=

2012

-

[13]

Finance and Stochastics , volume=

A generalization of the Hull and White formula with applications to option pricing approximation , author=. Finance and Stochastics , volume=. 2006 , publisher=

2006

-

[14]

Bachelier, L. , title =. Annales scientifiques de l'\'Ecole Normale Sup\'erieure , pages =. 1900 , publisher =. doi:10.24033/asens.476 , language =

-

[15]

Option Valuation Under Stochastic Volatility , publisher =

Lewis, Alan , year =. Option Valuation Under Stochastic Volatility , publisher =

-

[16]

Rama Cont and Peter Tankov , title =

-

[17]

Finance and Stochastics , volume =

Elisa Al. Finance and Stochastics , volume =. 2019 , publisher =

2019

-

[18]

2006 , edition =

David Nualart , title =. 2006 , edition =

2006

-

[19]

Risk Magazine , year =

Lorenzo Bergomi and Julien Guyon , title =. Risk Magazine , year =

-

[20]

Stochastic Processes and Their Applications , volume =

Jan Rosiński , title =. Stochastic Processes and Their Applications , volume =. 2007 , issn =. doi:10.1016/j.spa.2006.10.003 , url =

-

[21]

Barndorff-Nielsen , title =

Ole E. Barndorff-Nielsen , title =. Finance and Stochastics , volume =. 1997 , publisher =

1997

-

[22]

Generative adversarial networks for financial trading strategies fine-tuning and combination

Jean-Philippe Aguilar , title =. Quantitative Finance , volume =. 2021 , publisher =. doi:10.1080/14697688.2020.1856404 , url =

-

[23]

Journal of Futures Markets , volume =

Jaehyuk Choi and Minsuk Kwak and Chyng Wen Tee and Yumeng Wang , title =. Journal of Futures Markets , volume =. 2022 , publisher =

2022

-

[24]

2000 , publisher=

Derivatives in financial markets with stochastic volatility , author=. 2000 , publisher=

2000

-

[25]

Fouque, J. P. and Papanicolaou, G. and Sircar, R. and Solna, K. , title =. SIAM Journal on Applied Mathematics , volume =. 2003 , doi =

2003

-

[26]

Electronic Journal of Probability , number =

Masaaki Fukasawa , title =. Electronic Journal of Probability , number =. 2011 , doi =

2011

-

[27]

The Best of Wilmott , volume=

Managing smile risk , author=. The Best of Wilmott , volume=

-

[28]

Bates , title =

David S. Bates , title =. The Review of Financial Studies , volume =. 1996 , publisher =

1996

-

[29]

Finance and Stochastics , volume =

Figueroa-L. Finance and Stochastics , volume =. 2016 , publisher =

2016

-

[30]

Finance and Stochastics , volume=

Figueroa-L. Finance and Stochastics , volume=. 2015 , publisher=

2015

-

[31]

Oldham, Keith and Myland, Jan and Spanier, Jerome , TITLE =. 2009 , PAGES =. doi:10.1007/978-0-387-48807-3 , URL =

-

[32]

Frontiers of Mathematical Finance , volume =

Andrey Itkin , keywords =. Frontiers of Mathematical Finance , volume =. 2024 , issn =. doi:10.3934/fmf.2024005 , url =

-

[33]

2011 , publisher=

Fukasawa, Masaaki , journal=. 2011 , publisher=

2011

-

[34]

International Journal of Stochastic Analysis , volume=

Al. International Journal of Stochastic Analysis , volume=. 2008 , publisher=

2008

-

[35]

Applied Mathematical Finance , volume=

Gerhold, Stefan and G. Applied Mathematical Finance , volume=. 2016 , publisher=

2016

-

[36]

2016 , publisher=

Bayer, Christian and Friz, Peter and Gatheral, Jim , journal=. 2016 , publisher=

2016

-

[37]

International Journal of Theoretical and Applied Finance , volume =

JAFARI, HOSSEIN and BUR\'. International Journal of Theoretical and Applied Finance , volume =. 0 , doi =. https://doi.org/10.1142/S0219024925500062 , abstract =

-

[38]

Elisa Alòs and Òscar Burés and Josep Vives , year=. 2503.22282 , archivePrefix=

-

[39]

Kadelburg, Zoran and Marjanovic, M , journal=

-

[40]

Schachermayer, Walter and Teichmann, Josef , TITLE =. Math. Finance , FJOURNAL =. 2008 , NUMBER =. doi:10.1111/j.1467-9965.2007.00326.x , URL =

-

[41]

Lewis and Dan Pirjol , title =

Alan L. Lewis and Dan Pirjol , title =. Quantitative Finance , volume =. 2022 , publisher =

2022

-

[42]

, TITLE =

Lewis, Alan L. , TITLE =. 2016 , PAGES =

2016

-

[43]

Al\`os, Elisa , TITLE =. Finance Stoch. , FJOURNAL =. 2006 , NUMBER =. doi:10.1007/s00780-006-0013-5 , URL =

-

[44]

Antonelli, Fabio and Scarlatti, Sergio , TITLE =. Finance Stoch. , FJOURNAL =. 2009 , NUMBER =. doi:10.1007/s00780-008-0086-4 , URL =

-

[45]

Exponentiation of conditional expectations under stochastic volatility , JOURNAL =

Al\`os, Elisa and Gatheral, Jim and Radoi. Exponentiation of conditional expectations under stochastic volatility , JOURNAL =. 2020 , NUMBER =. doi:10.1080/14697688.2019.1642506 , URL =

-

[46]

Entropy , volume=

Analytic Approximation for Bachelier Option Prices and Applications , author=. Entropy , volume=. 2026 , publisher=

2026

-

[47]

Yor, Marc , TITLE =. Adv. in Appl. Probab. , FJOURNAL =. 1992 , NUMBER =. doi:10.2307/1427477 , URL =

-

[48]

Hartman, Philip and Watson, Geoffrey S. , TITLE =. Ann. Probability , FJOURNAL =. 1974 , PAGES =. doi:10.1214/aop/1176996606 , URL =

-

[49]

Cai, Ning and Song, Yingda and Chen, Nan , TITLE =. Oper. Res. , FJOURNAL =. 2017 , NUMBER =. doi:10.1287/opre.2017.1617 , URL =

-

[50]

Pirjol, Dan , TITLE =. Methodol. Comput. Appl. Probab. , FJOURNAL =. 2021 , NUMBER =. doi:10.1007/s11009-020-09827-5 , URL =

-

[51]

Pirjol, Dan , TITLE =. Appl. Math. Comput. , FJOURNAL =. 2026 , PAGES =. doi:10.1016/j.amc.2026.130144 , URL =

-

[52]

SIAM Journal on Scientific and Statistical Computing , volume =

Greengard, Leslie and Strain, John , title =. SIAM Journal on Scientific and Statistical Computing , volume =. 1991 , doi =. https://doi.org/10.1137/0912004 , abstract =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.