Valuation Reveals Uncertainty

Pith reviewed 2026-06-30 01:30 UTC · model grok-4.3

The pith

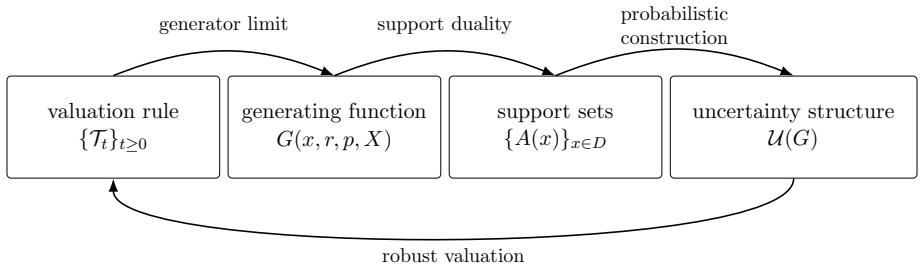

Dynamic sublinear valuation rules contain enough information to identify and recover the latent uncertainty structures that generate them.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

A robust valuation rule induced by worst-case expectations over a set of models allows the underlying uncertainty structure to be identified explicitly from the observed dynamic sublinear valuation rule, with all time-consistent uncertainty structures representing the rule fully characterized and recoverable via nonparametric estimation from valuation data.

What carries the argument

Dynamic sublinear valuation rule as the functional induced by robust worst-case expectations over a set of models.

Load-bearing premise

The observed valuation rules are dynamic sublinear functionals induced by robust worst-case expectations over a set of models.

What would settle it

A dynamic sublinear valuation rule for which no uncertainty structure reproduces the valuations exactly or for which the nonparametric estimator fails to recover a structure that matches the original worst-case expectations on held-out payoffs.

Figures

read the original abstract

This paper studies the recovery of uncertainty from dynamic sublinear valuation rules. A robust valuation assigns each payoff its worst-case expected value across plausible models under uncertainty and induces a dynamic sublinear valuation rule. While valuation rules are observable in practice, the underlying uncertainty structure is latent. First, we show that the latent uncertainty structure can be identified from an observed valuation rule and provide an explicit procedure for recovering it. Second, we develop the notion of time consistency for uncertainty structures as the uncertainty-side counterpart of time consistency in valuation. Third, we characterize all time-consistent uncertainty structures that represent a given valuation rule. Finally, we develop nonparametric estimators for recovering uncertainty from limited valuation data. These results overturn the traditional Knightian view that uncertainty is inherently non-measurable. Indeed, valuation contains sufficient information to identify, characterize, and statistically recover the uncertainty structures that generate it.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that dynamic sublinear valuation rules (observable in practice) induced by robust worst-case expectations over a set of models suffice to identify the latent uncertainty structure, characterize all time-consistent uncertainty structures compatible with a given valuation, and recover it via nonparametric estimators from limited data. This is positioned as overturning the Knightian view that uncertainty is inherently non-measurable.

Significance. If the explicit identification procedures, time-consistency characterization, and estimator constructions hold under the maintained robust-representation hypothesis, the result is significant for mathematical finance: it supplies concrete, non-circular maps from observable valuations to recoverable sets of models, resting on standard dual representations of sublinear functionals and dynamic risk measures. The nonparametric estimators follow directly from the identification map, providing falsifiable recovery tools that could be tested in pricing and risk applications.

minor comments (2)

- The abstract states that the steps from observed valuation to recovered set of models are spelled out without hidden circularity, but the full manuscript should include an explicit statement of the measurability assumptions required for the dual representation to yield a unique recovered set (e.g., in the section developing the identification procedure).

- Notation for the time-consistent uncertainty structures should be cross-referenced to the corresponding dynamic valuation functional to improve readability when moving between the uncertainty-side and valuation-side characterizations.

Simulated Author's Rebuttal

We thank the referee for the positive summary, significance assessment, and recommendation of minor revision. The recognition that our identification procedures, time-consistency characterization, and nonparametric estimators could supply concrete maps from observable valuations to recoverable model sets is appreciated.

Circularity Check

No significant circularity

full rationale

The manuscript derives identification of uncertainty structures from observed dynamic sublinear valuations via explicit procedures grounded in standard dual representations of sublinear functionals and dynamic risk measures. The characterization of time-consistent uncertainty structures, the recovery map, and the nonparametric estimators are constructed directly from these representations without any reduction to self-definitional loops, fitted inputs renamed as predictions, or load-bearing self-citations whose content is itself unverified. All steps remain self-contained against external benchmarks in the robust-valuation literature, so the claim that valuation data suffice for recovery does not collapse into its own inputs by construction.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Alvarez, L., Guichard, F., Lions, P.-L., and Morel, J.-M. (1993). Axioms and fundamental equations of image processing. Archive for rational mechanics and analysis , 123(3):199--257

1993

-

[2]

W., Hansen, L

Anderson, E. W., Hansen, L. P., and Sargent, T. J. (2003). A quartet of semigroups for model specification, robustness, prices of risk, and model detection. Journal of the European Economic Association , 1(1):68--123

2003

-

[3]

Cellina, A. (1969). Approximation of set valued functions and fixed point theorems. Annali di matem \'a tica pura ed applicata , 82(1):17--24

1969

-

[4]

and Epstein, L

Chen, Z. and Epstein, L. G. (2002). Ambiguity, risk, and asset returns in continuous time. Econometrica , 70(4):1403--1443

2002

-

[5]

Cheridito, P., Delbaen, F., and Kupper, M. (2006). Dynamic monetary risk measures for bounded discrete-time processes. Electronic Journal of Probability

2006

-

[6]

G., Ishii, H., and Lions, P.-L

Crandall, M. G., Ishii, H., and Lions, P.-L. (1992). User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American mathematical society , 27(1):1--67

1992

-

[7]

G., Kocan, M., and \'S wiech, A

Crandall, M. G., Kocan, M., and \'S wiech, A. (2000). L^p -theory for fully nonlinear uniformly parabolic equations: Parabolic equations. Communications in Partial Differential Equations , 25(11-12):1997--2053

2000

-

[8]

Criens, D. and Kupper, M. (2025). Representation theorems for convex expectations and semigroups on path space. arXiv preprint arXiv:2503.10572

-

[9]

and Niemann, L

Criens, D. and Niemann, L. (2025). A stochastic representation theorem for sublinear semigroups with non-local generators. Electronic Journal of Probability , 30:1--36

2025

-

[10]

and Martini, C

Denis, L. and Martini, C. (2006). A theoretical framework for the pricing of contingent claims in the presence of model uncertainty. Annals of Applied Probability

2006

-

[11]

and Zaj \'i c ek, L

Duda, J. and Zaj \'i c ek, L. (2009). Semiconvex functions: R epresentations as suprema of smooth functions and extensions. Journal of Convex Analysis , 16(1):239--260

2009

-

[12]

Epstein, L. G. and Ji, S. (2013). Ambiguous volatility and asset pricing in continuous time. The Review of Financial Studies , 26(7):1740--1786

2013

-

[13]

Epstein, L. G. and Schneider, M. (2003). Recursive multiple-priors. Journal of Economic Theory , 113(1):1--31

2003

-

[14]

and Schied, A

F \"o llmer, H. and Schied, A. (2011). Stochastic finance: An introduction in discrete time . Walter de Gruyter

2011

-

[15]

Goldys, B., Nendel, M., and R \"o ckner, M. (2024). Operator semigroups in the mixed topology and the infinitesimal description of M arkov processes. Journal of Differential Equations , 412:23--86

2024

-

[16]

Hansen, L. P. (2007). Beliefs, doubts and learning: Valuing macroeconomic risk. American Economic Review , 97(2):1--30

2007

-

[17]

Hansen, L. P. and Sargent, T. J. (2001). Robust control and model uncertainty. American Economic Review , 91(2):60--66

2001

-

[18]

P., Sargent, T

Hansen, L. P., Sargent, T. J., Turmuhambetova, G. A., and Williams, N. (2006). Robust control and model misspecification. Journal of Economic Theory , 128(1):45--90

2006

-

[19]

Hollender, J. (2016). L \'e vy-Type Processes under Uncertainty and Related Nonlocal Equations . Ph.D. dissertation, Technische Universit \"a t Dresden, Dresden, Germany

2016

-

[20]

and Shiryaev, A

Jacod, J. and Shiryaev, A. (2013). Limit theorems for stochastic processes , volume 288. Springer Science & Business Media

2013

-

[21]

Knight, F. H. (1921). Risk, uncertainty and profit , volume 31. Houghton Mifflin

1921

-

[22]

K \"u hn, F. (2021). On infinitesimal generators of sublinear M arkov semigroups. Osaka Journal of Mathematics , 58(3):487--508

2021

-

[23]

Maccheroni, F., Marinacci, M., and Rustichini, A. (2006a). Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica , 74(6):1447--1498

-

[24]

Maccheroni, F., Marinacci, M., and Rustichini, A. (2006b). Dynamic variational preferences. Journal of Economic Theory , 128(1):4--44

-

[25]

Maenhout, P. J. (2004). Robust portfolio rules and asset pricing. Review of financial studies , 17(4):951--983

2004

-

[26]

Nendel, M. (2025). Lower semicontinuity of monotone functionals in the mixed topology on C_b . Finance and Stochastics , 29(1):261--287

2025

-

[27]

and Nutz, M

Neufeld, A. and Nutz, M. (2017). Nonlinear L \'e vy processes and their characteristics. Transactions of the American Mathematical Society , 369(1):69--95

2017

-

[28]

Nutz, M. (2012). A quasi-sure approach to the control of non- M arkovian stochastic differential equations. Electronic Journal of Probability , 17(23):1--23

2012

-

[29]

Nutz, M. (2013). Random G -expectations. The Annals of Applied Probability , 23(5):1755--1777

2013

-

[30]

and Soner, H

Nutz, M. and Soner, H. M. (2012). Superhedging and dynamic risk measures under volatility uncertainty. SIAM Journal on Control and Optimization , 50(4):2065--2089

2012

-

[31]

and Van Handel, R

Nutz, M. and Van Handel, R. (2013). Constructing sublinear expectations on path space. Stochastic processes and their applications , 123(8):3100--3121

2013

-

[32]

Peng, S. (2007). G -expectation, G - B rownian motion and related stochastic calculus of I t \^o type. In Stochastic Analysis and Applications: The Abel Symposium 2005 , pages 541--567. Springer

2007

-

[33]

Pinsky, R. G. (1995). Positive harmonic functions and diffusion , volume 45. Cambridge university press

1995

-

[34]

Rockafellar, R. T. (2015). Convex analysis:(pms-28) . Princeton university press

2015

-

[35]

Rockafellar, R. T. and Wets, R. J. (1998). Variational analysis . Springer

1998

-

[36]

Stroock, D. W. and Varadhan, S. S. (1997). Multidimensional diffusion processes , volume 233. Springer Science & Business Media

1997

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.