Innovative Extensions to Option Pricing: Asymmetric Brownian Motion and Random Walk Approaches

Pith reviewed 2026-06-26 09:51 UTC · model grok-4.3

The pith

The Geometric Asymmetric Brownian Motion model extends classical option pricing by using local time at the origin to generate skewness and state-dependent risk within the Bachelier-Black-Scholes-Merton framework.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

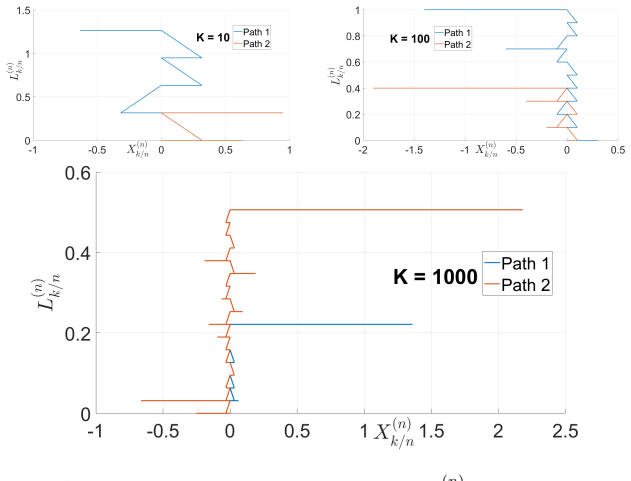

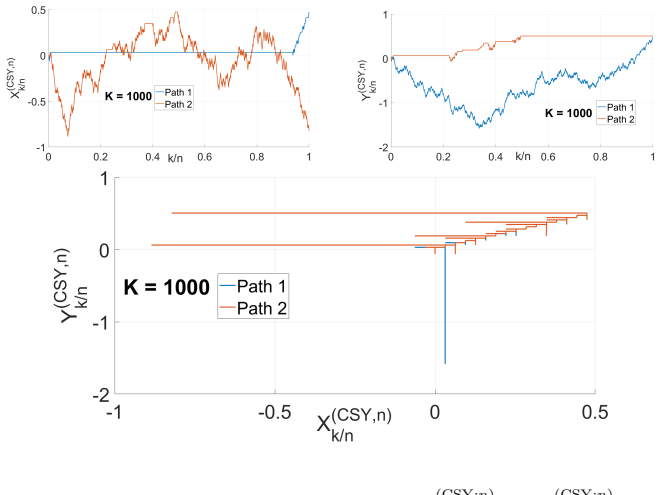

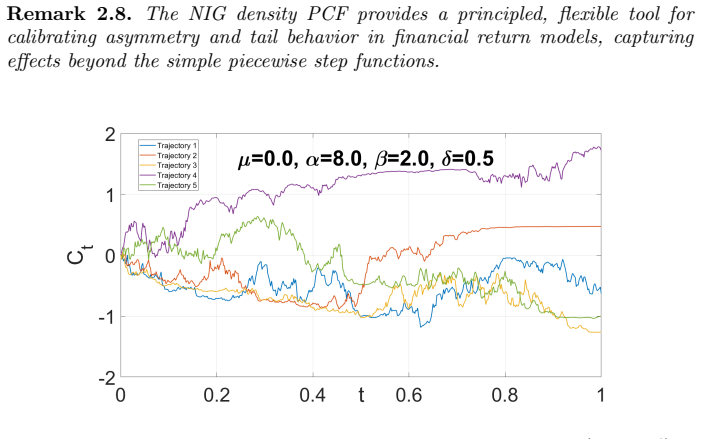

The GABM model unifies asymmetric Brownian motion and random walk methodologies within the Bachelier-Black-Scholes-Merton framework, harnesses the Cherny-Shiryaev-Yor invariance principle to define asymmetric random walk integrals where local time at the origin generates skewness and state-dependent risk, derives closed-form option pricing formulas, and constructs a discrete-time binomial tree algorithm shown to converge rigorously to the GABM limit, with a smoothed functional form based on the normal inverse Gaussian distribution allowing flexible state-dependent volatility calibration.

What carries the argument

The Cherny-Shiryaev-Yor invariance principle applied to asymmetric random walk integrals, where local time at the origin generates skewness and state-dependent risk.

If this is right

- Closed-form option pricing formulas become available for processes that incorporate skewness via local time.

- A discrete-time binomial tree can be used for computation and converges rigorously to the continuous GABM model.

- State-dependent volatility can be calibrated flexibly through a smoothed normal inverse Gaussian functional form.

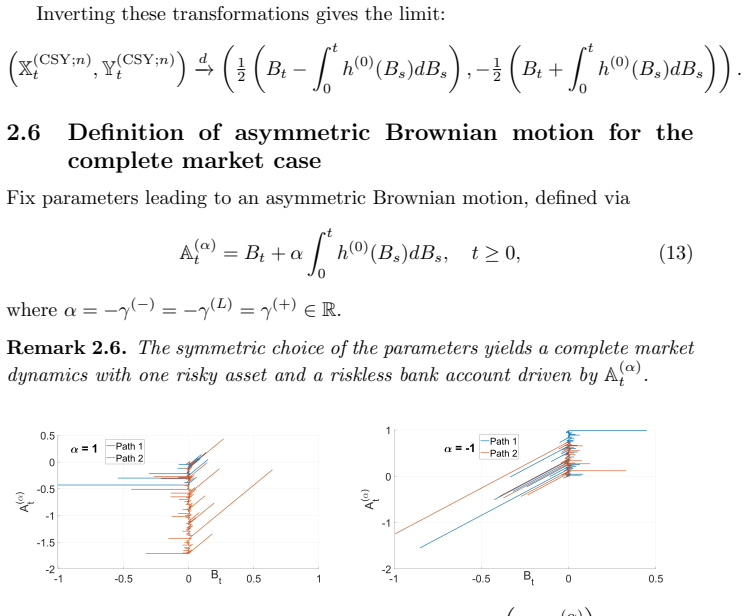

- The resulting prices and implied volatility surfaces reflect persistent market asymmetry and state-dependent risk.

Where Pith is reading between the lines

- The local-time mechanism could be tested by checking whether implied volatility surfaces from the model match those observed in equity options during periods of strong negative skewness.

- If the convergence result holds, the binomial tree offers a computationally tractable way to price path-dependent options under the GABM dynamics.

- Extensions to multi-factor or jump-augmented versions would follow naturally from the same invariance principle.

Load-bearing premise

The Cherny-Shiryaev-Yor invariance principle can be applied to define asymmetric random walk integrals in which local time at the origin generates skewness and state-dependent risk within the Bachelier-Black-Scholes-Merton framework.

What would settle it

Numerical simulations in which the discrete binomial tree algorithm fails to converge to the continuous GABM process as the time step approaches zero, or in which the closed-form prices deviate systematically from Monte Carlo benchmarks for the same process parameters.

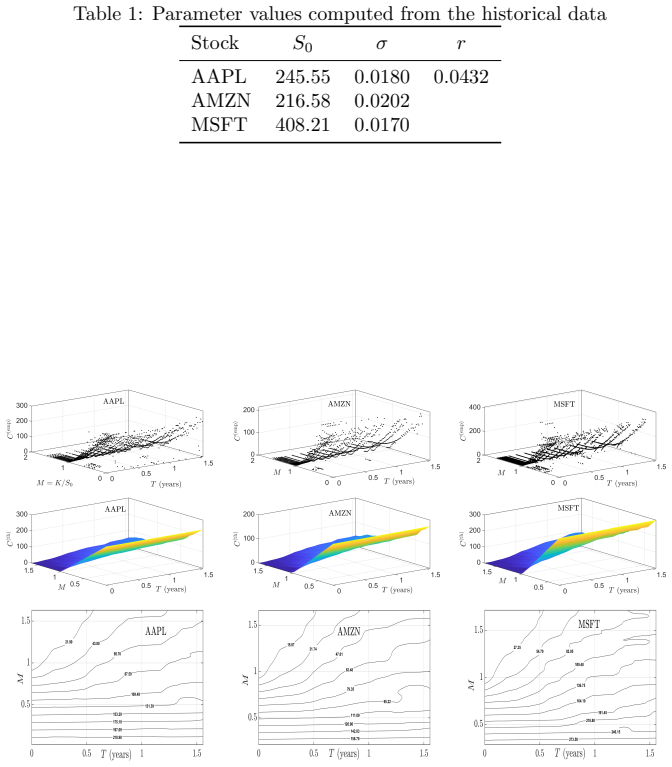

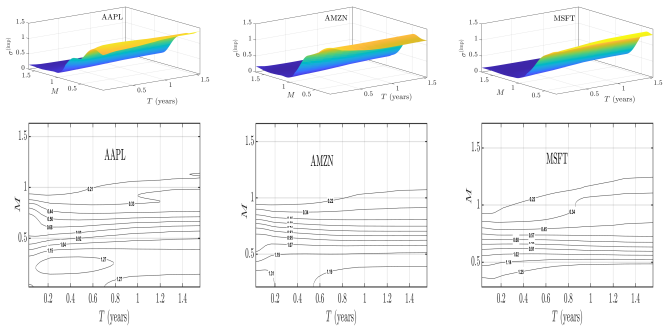

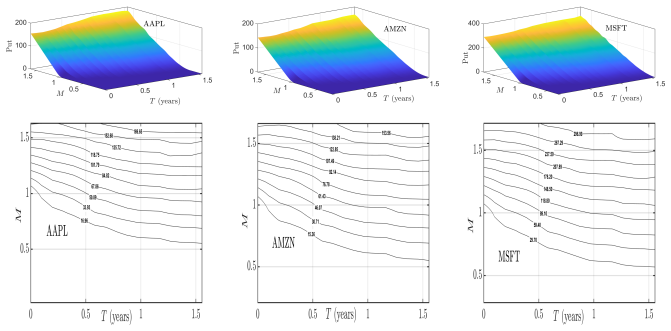

Figures

read the original abstract

Classical option pricing models, such as Bachelier and Black--Scholes--Merton, postulate symmetric Brownian diffusion, which limits their capacity to reflect empirical phenomena including return skewness, heavy tails, and volatility asymmetry. This paper develops an innovative extension: the Geometric Asymmetric Brownian Motion (GABM), unifying asymmetric Brownian motion and random walk methodologies within the Bachelier--Black--Scholes--Merton framework. The approach harnesses the Cherny--Shiryaev--Yor invariance principle (CSYIP) to define asymmetric random walk integrals, where local time at the origin generates skewness and state-dependent risk. Closed-form option pricing formulas are derived, and a discrete-time binomial tree algorithm is constructed and shown to converge rigorously to the GABM limit. By incorporating a smoothed functional form based on the normal inverse Gaussian distribution, the model allows for flexible, state-dependent volatility calibration. Numerical experiments demonstrate the resulting option price and implied volatility surfaces, highlighting the framework's enhanced ability to capture persistent market asymmetry and complex risk behaviors observed in empirical data.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops the Geometric Asymmetric Brownian Motion (GABM) model as an extension within the Bachelier-Black-Scholes-Merton framework. It unifies asymmetric Brownian motion and random walk approaches by applying the Cherny-Shiryaev-Yor invariance principle to asymmetric random walk integrals, where local time at the origin is used to generate skewness and state-dependent risk. The manuscript claims to derive closed-form option pricing formulas, construct a discrete-time binomial tree algorithm with rigorous convergence to the GABM limit, and employ a normal inverse Gaussian (NIG) smoothed functional form for flexible state-dependent volatility calibration. Numerical experiments are presented to illustrate resulting option price and implied volatility surfaces that capture market asymmetry.

Significance. If the claimed closed-form derivations and convergence proof hold, the GABM construction could offer a mathematically unified way to incorporate empirical skewness and volatility asymmetry into a familiar pricing framework, with the binomial tree providing a practical computational tool. The explicit use of local time for state-dependent effects is a potentially interesting technical feature. However, the NIG-based calibration step introduces a data-fitting component that may limit the extent to which the model generates independent predictions rather than descriptive fits.

major comments (2)

- [Abstract, model development section] Abstract and model development section: The central claim that closed-form option pricing formulas are derived and that the binomial tree converges rigorously to the GABM limit is asserted without any displayed equations, proofs, or error bounds. This absence makes it impossible to verify whether the CSYIP application to asymmetric random walk integrals correctly produces the stated skewness and state-dependent risk without internal inconsistencies.

- [Calibration and numerical experiments section] Calibration and numerical experiments section: The smoothed NIG functional form for state-dependent volatility is described as allowing flexible calibration, yet the abstract and reader's description indicate that parameters are fitted to empirical data. This creates a potential circularity for the central claim that the model captures 'persistent market asymmetry,' because the option prices and surfaces may be tuned to the same asymmetry they purport to predict, rather than emerging parameter-free from the GABM construction.

minor comments (1)

- [Abstract] The abstract refers to 'rigorous convergence' of the binomial tree but provides no statement of the norm or rate; a minor clarification of the convergence statement would improve readability.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. We address the two major comments point by point below, indicating the revisions we will make to strengthen the manuscript.

read point-by-point responses

-

Referee: [Abstract, model development section] Abstract and model development section: The central claim that closed-form option pricing formulas are derived and that the binomial tree converges rigorously to the GABM limit is asserted without any displayed equations, proofs, or error bounds. This absence makes it impossible to verify whether the CSYIP application to asymmetric random walk integrals correctly produces the stated skewness and state-dependent risk without internal inconsistencies.

Authors: The referee correctly notes that the abstract and model development section state the existence of closed-form formulas and a rigorous convergence result without displaying the supporting equations or proof details. In the revised manuscript we will insert the key CSYIP-derived integral expressions for the asymmetric random walk, the resulting closed-form option pricing formulas, and the statement of the convergence theorem together with the error-bound argument into the main text of the model development section (with full proofs retained in an appendix for completeness). This will allow direct verification of the local-time mechanism and the absence of internal inconsistencies. revision: yes

-

Referee: [Calibration and numerical experiments section] Calibration and numerical experiments section: The smoothed NIG functional form for state-dependent volatility is described as allowing flexible calibration, yet the abstract and reader's description indicate that parameters are fitted to empirical data. This creates a potential circularity for the central claim that the model captures 'persistent market asymmetry,' because the option prices and surfaces may be tuned to the same asymmetry they purport to predict, rather than emerging parameter-free from the GABM construction.

Authors: We agree that the NIG smoothing is a calibration device and that the numerical surfaces are therefore descriptive fits. However, the skewness and state-dependent risk in the GABM arise directly from the local-time term generated by the CSYIP applied to the asymmetric random walk; this structural feature is independent of the particular functional form chosen for volatility. The NIG component only modulates the volatility surface while preserving the asymmetry mechanism. In the revision we will add an explicit paragraph separating the model-derived asymmetry (parameter-free once the random-walk asymmetry parameter is fixed) from the subsequent NIG calibration step, thereby clarifying that the core asymmetry is not an artifact of fitting. revision: partial

Circularity Check

No significant circularity identified

full rationale

The derivation chain rests on applying the external Cherny-Shiryaev-Yor invariance principle to construct asymmetric random walk integrals, deriving closed-form pricing formulas, and rigorously proving binomial-tree convergence to the GABM limit. These steps are independent of the subsequent NIG-smoothed calibration choice, which is presented only as a flexible fitting device for state-dependent volatility and does not retroactively define or force the closed-form expressions or convergence result. No self-definitional equations, fitted inputs relabeled as predictions, or load-bearing self-citations appear in the provided claims.

Axiom & Free-Parameter Ledger

free parameters (2)

- asymmetry factor

- NIG smoothing parameters

axioms (2)

- domain assumption Cherny-Shiryaev-Yor invariance principle applies to asymmetric random walk integrals with local time generating skewness

- domain assumption Binomial tree converges rigorously to the continuous GABM limit

invented entities (2)

-

Geometric Asymmetric Brownian Motion (GABM)

no independent evidence

-

local time at origin as generator of skewness

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Bachelier, Louis , booktitle=. Th

-

[2]

The Review of Financial Studies , volume=

Stock return characteristics, skew laws, and the differential pricing of individual equity options , author=. The Review of Financial Studies , volume=. 2003 , publisher=

2003

-

[3]

Journal of financial economics , volume=

A model of investor sentiment , author=. Journal of financial economics , volume=. 1998 , publisher=

1998

-

[4]

Finance and stochastics , volume=

Processes of normal inverse Gaussian type , author=. Finance and stochastics , volume=. 1997 , publisher=

1997

-

[5]

Journal of political economy , volume=

The pricing of options and corporate liabilities , author=. Journal of political economy , volume=. 1973 , publisher=

1973

-

[6]

The Journal of Finance , volume=

Noise , author=. The Journal of Finance , volume=. 1986 , publisher=

1986

-

[7]

Quantitative finance , volume=

A non-Gaussian option pricing model with skew , author=. Quantitative finance , volume=. 2004 , publisher=

2004

-

[8]

Applied Stochastic Models in Business and Industry , volume=

Forecasting portfolio returns with skew-geometric Brownian motions , author=. Applied Stochastic Models in Business and Industry , volume=. 2022 , publisher=

2022

-

[9]

Journal of computational finance , volume=

Option valuation using the fast Fourier transform , author=. Journal of computational finance , volume=

-

[10]

horizontal-vertical

Limit behavior of the" horizontal-vertical" random walk and some extensions of the Donsker-Prokhorov invariance principle , author=. Theory of Probability & Its Applications , volume=. 2003 , publisher=

2003

-

[11]

The Review of Financial Studies , volume=

Capturing option anomalies with a variance-dependent pricing kernel , author=. The Review of Financial Studies , volume=. 2013 , publisher=

2013

-

[12]

1990 , publisher=

Introduction to stochastic integration , author=. 1990 , publisher=

1990

-

[13]

Corns, T Richard A and Satchell, Stephen E , journal=. Skew. 2007 , publisher=

2007

-

[14]

Quantitative finance , volume=

Empirical properties of asset returns: stylized facts and statistical issues , author=. Quantitative finance , volume=. 2001 , publisher=

2001

-

[15]

2001 , publisher=

Dynamic asset pricing theory , author=. 2001 , publisher=

2001

-

[16]

Bernoulli , pages=

Hyperbolic distributions in finance , author=. Bernoulli , pages=. 1995 , publisher=

1995

-

[17]

Journal of finance , volume=

Efficient capital markets , author=. Journal of finance , volume=

-

[18]

Journal of Risk and Financial Management , volume=

Hedging via Perpetual Derivatives: Trinomial Option Pricing and Implied Parameter Surface Analysis , author=. Journal of Risk and Financial Management , volume=. 2025 , publisher=

2025

-

[19]

The review of financial studies , volume=

A closed-form solution for options with stochastic volatility with applications to bond and currency options , author=. The review of financial studies , volume=. 1993 , publisher=

1993

-

[20]

International Journal of Theoretical and Applied Finance , volume=

Option pricing in markets with informed traders , author=. International Journal of Theoretical and Applied Finance , volume=. 2020 , publisher=

2020

-

[21]

Journal of Risk and Financial Management , volume=

Option pricing incorporating factor dynamics in complete markets , author=. Journal of Risk and Financial Management , volume=. 2020 , publisher=

2020

-

[22]

Market complete option valuation using a

Hu, Yuan and Lindquist, W Brent and Rachev, Svetlozar T and Shirvani, Abootaleb and Fabozzi, Frank J , journal=. Market complete option valuation using a. 2022 , publisher=

2022

-

[23]

Journal of Risk and Financial Management , volume=

Option Pricing Using a Skew Random Walk Binary Tree , author=. Journal of Risk and Financial Management , volume=. 2024 , publisher=

2024

-

[24]

The Review of Financial Studies , volume=

Recovering risk aversion from option prices and realized returns , author=. The Review of Financial Studies , volume=. 2000 , publisher=

2000

-

[25]

Journal of Futures Markets , volume=

A random walk down the options market , author=. Journal of Futures Markets , volume=. 2012 , publisher=

2012

-

[26]

1999 , publisher=

A random walk down Wall Street: including a life-cycle guide to personal investing , author=. 1999 , publisher=

1999

-

[27]

Econometrica: Journal of the Econometric Society , pages=

An intertemporal capital asset pricing model , author=. Econometrica: Journal of the Econometric Society , pages=. 1973 , publisher=

1973

-

[28]

A simple European option pricing formula with a skew

Pasricha, Puneet and He, Xin-Jiang , journal=. A simple European option pricing formula with a skew

-

[29]

1999 , school =

The Generalized Hyperbolic Model: Estimation, Financial Derivatives, and Risk Measures , author =. 1999 , school =

1999

-

[30]

Bachelier’s market model for

Rachev, Svetlozar and Asare Nyarko, Nancy and Omotade, Blessing and Yegon, Peter , journal=. Bachelier’s market model for. 2024 , publisher=

2024

-

[31]

International Journal of Theoretical and Applied Finance , volume=

Financial markets with no riskless (safe) asset , author=. International Journal of Theoretical and Applied Finance , volume=. 2017 , publisher=

2017

-

[32]

Stochastic processes and their applications , volume=

Tempering stable processes , author=. Stochastic processes and their applications , volume=. 2007 , publisher=

2007

-

[33]

The normal inverse Gaussian L

Rydberg, Tina Hviid , journal=. The normal inverse Gaussian L. 1997 , publisher=

1997

-

[34]

Industrial Management Review , volume =

Proof that properly anticipated prices fluctuate randomly , author=. Industrial Management Review , volume =. 1965 , publisher=

1965

-

[35]

1981 , publisher=

Do stock prices move too much to be justified by subsequent changes in dividends? , author=. 1981 , publisher=

1981

-

[36]

Valuation of spread options under correlated skew

Song, Shiyu and Wang, Xingchun and Zhang, Xiaowen , journal=. Valuation of spread options under correlated skew. 2024 , publisher=

2024

-

[37]

Zhu, S. P. and He, X. J. , title =. The European Journal of Finance , year =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.