Granular Instrumental Variables in Large Panels: Identification and Inference Across Strong, Nearly Weak, and Weak GIV

Pith reviewed 2026-07-03 02:09 UTC · model grok-4.3

The pith

The GIV estimator is consistent and asymptotically normal at the √T rate when a few units dominate the aggregate, but only at slower rates or inconsistent when they do not.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

When a few units dominate the aggregate, the GIV estimator is consistent and asymptotically normal at the standard √T rate. When large units stand out but do not dominate, the estimator remains consistent and asymptotically normal at a slower rate. When units are comparable in size, the estimator is inconsistent with a non-standard distribution. Wald inference is reliable only outside the weak regime. When the instrument is weak, Anderson-Rubin confidence sets are recommended. The feasible estimator attains the same rate but its asymptotic variance includes an additional term from the first-stage estimation.

What carries the argument

Granular Instrumental Variables (GIV) whose strength is determined by the presence and degree of dominant units in the aggregate.

If this is right

- The parameter of interest remains recoverable in the nearly weak regime despite slower convergence than √T.

- Standard errors for the feasible GIV estimator must incorporate the extra variability from constructing the instrument in a first stage.

- Anderson-Rubin confidence sets maintain validity in the weak-instrument regime where Wald inference does not.

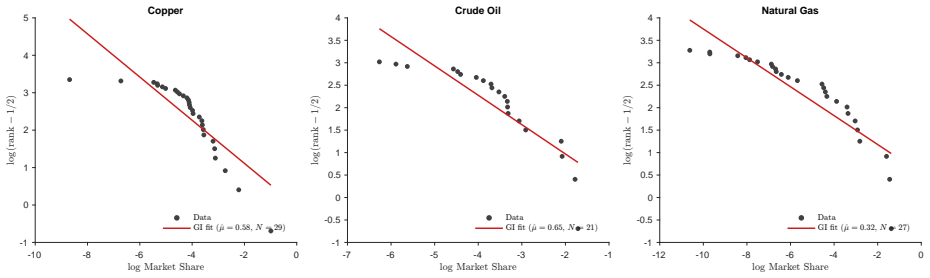

- The same three-regime analysis applies when recovering short-run demand elasticities for commodities such as refined copper, crude oil, and natural gas.

Where Pith is reading between the lines

- Dominance diagnostics could be used in practice to select between standard errors and Anderson-Rubin sets before estimation.

- The regime framework may extend to other aggregate instruments or to settings with time-varying dominance.

- Researchers studying cross-sectional dependence in macro panels could test for the presence of the nearly weak regime to interpret reported convergence rates.

Load-bearing premise

The classification of panels into strong, nearly weak, and weak regimes according to the relative sizes of units in the aggregate correctly governs the asymptotic behavior of the estimator.

What would settle it

A Monte Carlo experiment or empirical panel in which all units have comparable size, showing that the GIV point estimate fails to converge to the true parameter or that Wald intervals have incorrect coverage.

Figures

read the original abstract

I develop the asymptotic theory of instrument strength for Granular Instrumental Variables (GIV) in large panels with both $N$ and $T$ growing. The strength of the GIV depends on the presence of dominant units. I formalise what dominance means and characterise three regimes of instrument strength. When a few units dominate the aggregate, the instrument is strong. The GIV estimator is consistent and asymptotically normal at the standard $\sqrt{T}$ rate. When large units stand out but do not dominate, the instrument weakens. But I show that the parameter of interest remains recoverable. The GIV estimator remains consistent and asymptotically normal, now at a rate slower than $\sqrt{T}$. When units are comparable in size and none stands out, the instrument is weak in the standard sense. The GIV estimator is inconsistent and has a non-standard distribution. Wald inference is reliable only outside the weak regime. When the instrument is weak, I recommend Anderson-Rubin confidence sets. In practice, the instrument must be constructed in a first stage. I show that the feasible estimator attains the same rate, but its asymptotic variance picks up an additional term from the first-stage estimation. Valid inference must use standard errors that account for this term. I apply the GIV estimator with the correct standard errors to recover the short-run demand elasticities of three commodities: refined copper, crude oil, and natural gas.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops the asymptotic theory of Granular Instrumental Variables (GIV) in large N,T panels. It formalizes dominance of units in the aggregate and characterizes three regimes of instrument strength: strong (a few units dominate, yielding consistency and asymptotic normality at the √T rate), nearly weak (large units stand out but do not dominate, yielding consistency and asymptotic normality at a slower rate), and weak (units comparable in size, yielding inconsistency and a non-standard limiting distribution). The paper shows that Wald inference is reliable only outside the weak regime and recommends Anderson-Rubin confidence sets when the instrument is weak; it also derives the asymptotic behavior of the feasible two-step estimator that accounts for first-stage construction of the instrument and applies the corrected procedure to short-run demand elasticities for refined copper, crude oil, and natural gas.

Significance. If the derivations hold, the paper supplies a practically relevant extension of IV asymptotics to the granular setting that is common in macro and industrial-organization panels. The explicit trichotomy of regimes, together with the feasible-estimator correction and the recommendation for Anderson-Rubin sets, gives applied researchers concrete guidance on when standard errors are valid and when they are not. The three-commodity application demonstrates that the corrected GIV procedure can be implemented on real data.

minor comments (3)

- [Abstract] The abstract states that the feasible estimator 'attains the same rate' as the infeasible one but does not restate the precise rate (e.g., T^{1/3} or T^{2/5}) that applies in the nearly-weak regime; adding this sentence would improve readability.

- [Section 2] Section 2 (or wherever the dominance measure is introduced) would benefit from an explicit statement of the normalization used for the size vector s_i so that readers can immediately verify whether the three regimes are exhaustive and mutually exclusive.

- [Empirical application] In the empirical application, the paper reports point estimates and standard errors but does not show the first-stage F-statistic or the estimated dominance measure for each commodity; adding these diagnostics would help readers assess which regime applies in practice.

Simulated Author's Rebuttal

We thank the referee for the careful and accurate summary of our manuscript, as well as for the positive assessment of its significance and practical relevance. The recommendation of minor revision is noted. No specific major comments were raised in the report.

Circularity Check

No significant circularity; derivation self-contained from stated assumptions

full rationale

The paper derives the trichotomy of instrument strength regimes (strong, nearly weak, weak) and the associated rates of consistency/asymptotic normality directly from formal definitions of dominance in large N,T panels and the construction of the GIV instrument. No step reduces a target parameter to a fitted quantity by construction, renames a known result, or relies on a load-bearing self-citation whose content is unverified. The central claims follow from the model's assumptions without circular reduction, consistent with the reader's assessment of score 2.0 as minor at most.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard panel data assumptions for identification and asymptotics of instrumental variables estimators, including relevance and exogeneity conditions adapted to the granular setting.

Reference graph

Works this paper leans on

-

[1]

Eigenvalue ratio test for the number of factors

Seung C Ahn and Alex R Horenstein. Eigenvalue ratio test for the number of factors . Econometrica, 81 0 (3): 0 1203--1227, 2013. ISSN 0012-9682

2013

-

[2]

The macro-financial effects of international bank lending on emerging markets

Iñaki Aldasoro, Paula Beltr \' a n, Federico Grinberg, and Tommaso Mancini-Griffoli. The macro-financial effects of international bank lending on emerging markets . Journal of International Economics, 142: 0 103733, 2023

2023

-

[3]

Estimators for the parameters of a single equation in a complete set of stochastic equations

T Anderson and H Rubin. Estimators for the parameters of a single equation in a complete set of stochastic equations . The Annals of Mathematical Statistics, 21: 0 570--582, 1949

1949

-

[4]

GMM with Nearly-Weak Identification

Bertille Antoine and Eric Renault. GMM with Nearly-Weak Identification . Econometrics and Statistics, 2021

2021

-

[5]

Large market asymptotics for differentiated product demand estimators with economic models of supply

Timothy B Armstrong. Large market asymptotics for differentiated product demand estimators with economic models of supply . Econometrica, 84 0 (5): 0 1961--1980, 2016. ISSN 0012-9682

1961

-

[6]

Natural gas price elasticities and optimal cost recovery under consumer heterogeneity: Evidence from 300 million natural gas bills

Maximilian Auffhammer and Edward Rubin. Natural gas price elasticities and optimal cost recovery under consumer heterogeneity: Evidence from 300 million natural gas bills . Technical report, 2018

2018

-

[7]

Robert L Axtell. Zipf Distribution of U.S. Firm Sizes . Science, 293 0 (5536): 0 1818--1820, 2001. ISSN 0036-8075, 1095-9203. doi:10.1126/science.1062081. URL https://www.science.org/doi/10.1126/science.1062081

-

[8]

Inferential Theory for Factor Models of Large Dimensions

Jushan Bai. Inferential Theory for Factor Models of Large Dimensions . Econometrica, 71 0 (1): 0 135--171, 2003. ISSN 0012-9682. doi:https://doi.org/10.1111/1468-0262.00392. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/1468-0262.00392

-

[9]

Determining the Number of Factors in Approximate Factor Models

Jushan Bai and Serena Ng. Determining the Number of Factors in Approximate Factor Models . Econometrica, 70 0 (1): 0 191--221, 2002. ISSN 0012-9682. doi:https://doi.org/10.1111/1468-0262.00273. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/1468-0262.00273

-

[10]

Inferential Theory for Granular Instrumental Variables in High Dimensions

Saman Banafti and Tae-Hwy Lee. Inferential Theory for Granular Instrumental Variables in High Dimensions . arXiv preprint arXiv:2201.06605, 2022

-

[11]

Christiane Baumeister and James D Hamilton. Structural Interpretation of Vector Autoregressions with Incomplete Identification: Revisiting the Role of Oil Supply and Demand Shocks . American Economic Review, 109 0 (5): 0 1873--1910, 5 2019. doi:10.1257/aer.20151569. URL https://www.aeaweb.org/articles?id=10.1257/aer.20151569

-

[12]

A Full-Information Approach to Granular Instrumental Variables

Christiane Baumeister and James D Hamilton. A Full-Information Approach to Granular Instrumental Variables . Technical report, Working Paper, UCSD, 2023

2023

-

[13]

Asset insulators

Gabriel Chodorow-Reich, Andra Ghent, and Valentin Haddad. Asset insulators . The Review of Financial Studies, 34 0 (3): 0 1509--1539, 2021. ISSN 0893-9454

2021

-

[14]

Subexponentiality of the product of independent random variables

D B H Cline and G Samorodnitsky. Subexponentiality of the product of independent random variables . Stochastic Processes and their Applications, 49 0 (1): 0 75--98, 1994. ISSN 0304-4149. doi:https://doi.org/10.1016/0304-4149(94)90113-9. URL https://www.sciencedirect.com/science/article/pii/0304414994901139

-

[15]

On a Theorem of Breiman and a Class of Random Difference Equations

Denis Denisov and Bert Zwart. On a Theorem of Breiman and a Class of Random Difference Equations . Journal of Applied Probability, 44 0 (4): 0 1031--1046, 2007. ISSN 00219002. URL http://www.jstor.org/stable/27595905

-

[16]

Probability: theory and examples

Richard Durrett. Probability: theory and examples . Duxbury Press, Belmont, Calif, 2nd ed edition, 1996. ISBN 9780534243180

1996

-

[17]

Matrix theory

Joel N Franklin. Matrix theory . Courier Corporation, 2012

2012

-

[18]

Power Laws in Economics and Finance

Xavier Gabaix. Power Laws in Economics and Finance . Annual Review of Economics, 1 0 (1): 0 255--294, 2009. doi:10.1146/annurev.economics.050708.142940. URL https://www.annualreviews.org/doi/abs/10.1146/annurev.economics.050708.142940

-

[19]

The Granular Origins of Aggregate Fluctuations

Xavier Gabaix. The Granular Origins of Aggregate Fluctuations . Econometrica, 79 0 (3): 0 733--772, 2011. ISSN 0012-9682. doi:10.3982/ECTA8769

-

[20]

Rank — 1/2: A Simple Way to Improve the OLS Estimation of Tail Exponents

Xavier Gabaix and Rustam Ibragimov. Rank — 1/2: A Simple Way to Improve the OLS Estimation of Tail Exponents . Journal of Business & Economic Statistics , 29 0 (1): 0 24--39, 2011. ISSN 07350015. URL http://www.jstor.org/stable/25800776

-

[21]

Granular Instrumental Variables

Xavier Gabaix and Ralph S J Koijen. Granular Instrumental Variables . Journal of Political Economy, 132 0 (7): 0 728743, 7 2024. ISSN 0022-3808, 1537-534X. doi:10.1086/728743. URL https://www.journals.uchicago.edu/doi/10.1086/728743

-

[22]

Granular Credit Risk

Sigurd Galaasen, Rustam Jamilov, Ragnar Juelsrud, and Hélène Rey. Granular Credit Risk . Technical Report w27994, National Bureau of Economic Research, Cambridge, MA, 10 2020. URL http://www.nber.org/papers/w27994.pdf

2020

-

[23]

Global Portfolio Rebalancing and Exchange Rates

H Hau, H Rey, and N Camahno Neto. Global Portfolio Rebalancing and Exchange Rates . Review of Financial Studies, 2022. ISSN 0893-9454

2022

-

[24]

Granular shocks to corporate leverage and the macroeconomic transmission of monetary policy

Fédéric Holm-Hadulla and Claire Th \" u rw \" a chter. Granular shocks to corporate leverage and the macroeconomic transmission of monetary policy . 2024

2024

-

[25]

Matrix analysis

Roger A Horn and Charles R Johnson. Matrix analysis . Cambridge University Press, Cambridge ; New York, 2nd ed. edition, 2012. ISBN 9781139776004

2012

-

[26]

Limit theorems for network dependent random variables

Denis Kojevnikov, Vadim Marmer, and Kyungchul Song. Limit theorems for network dependent random variables . Journal of Econometrics, 222 0 (2): 0 882--908, 2021. ISSN 0304-4076. doi:https://doi.org/10.1016/j.jeconom.2020.05.019. URL https://www.sciencedirect.com/science/article/pii/S0304407620302402

-

[27]

A meta-analysis on the price elasticity of energy demand

Xavier Labandeira, José M Labeaga, and Xiral L \' o pez-Otero. A meta-analysis on the price elasticity of energy demand . Energy Policy, 102: 0 549--568, 2017. ISSN 0301-4215. doi:https://doi.org/10.1016/j.enpol.2017.01.002. URL https://www.sciencedirect.com/science/article/pii/S0301421517300022

-

[28]

Subglobal climate agreements and energy‐intensive activities: an evaluation of carbon leakage in the copper industry

Bruno Lanz, Thomas F Rutherford, and John E Tilton. Subglobal climate agreements and energy‐intensive activities: an evaluation of carbon leakage in the copper industry . The World Economy, 36 0 (3): 0 254--279, 2013. ISSN 0378-5920

2013

-

[29]

HAR inference: Recommendations for practice

Eben Lazarus, Daniel J Lewis, James H Stock, and Mark W Watson. HAR inference: Recommendations for practice . Journal of Business & Economic Statistics , 36 0 (4): 0 541--559, 2018. ISSN 0735-0015

2018

-

[30]

Nonparametric econometrics: theory and practice

Qi Li and Jeffrey Scott Racine. Nonparametric econometrics: theory and practice . Princeton University Press, Princeton, N.J, 2007. ISBN 9780691121611

2007

-

[31]

Expectations and bank lending

Yueran Ma, Teodora Paligorova, and José-Luis Peydro. Expectations and bank lending . University of Chicago, Unpublished Working Paper, 2021

2021

-

[32]

The two-parameter Poisson-Dirichlet distribution derived from a stable subordinator

Jim Pitman and Marc Yor. The two-parameter Poisson-Dirichlet distribution derived from a stable subordinator . The Annals of Probability, pages 855--900, 1997. ISSN 0091-1798

1997

-

[33]

Heterogeneity-robust granular instruments

Eric Qian. Heterogeneity-robust granular instruments . arXiv preprint arXiv:2304.01273, 2023

work page internal anchor Pith review Pith/arXiv arXiv 2023

-

[34]

On the subspaces of L p (p> 2) spanned by sequences of independent random variables

Haskell P Rosenthal. On the subspaces of L p (p> 2) spanned by sequences of independent random variables . Israel Journal of Mathematics, 8 0 (3): 0 273--303, 1970. ISSN 0021-2172

1970

-

[35]

Understanding Market Sensitivity: Estimation of Supply and Demand Elasticities for Non-Fuel Minerals

Elina Shojaeddini, Elisa Alonso, Nedal T Nassar, David Pineault, Shayla M Allen, Joshua L Brainard, David M McCaffrey, Timothy M O'Brien, Arturo J Padilla, and James W Ryter. Understanding Market Sensitivity: Estimation of Supply and Demand Elasticities for Non-Fuel Minerals . Mineral Economics, 38: 0 985--996, 2025. doi:10.1007/s13563-025-00537-3

-

[36]

Instrumental Variables Regression with Weak Instruments

Douglas Staiger and James H Stock. Instrumental Variables Regression with Weak Instruments . Econometrica, 65 0 (3): 0 557--586, 1997. ISSN 00129682, 14680262. doi:10.2307/2171753. URL http://www.jstor.org/stable/2171753

-

[37]

Forecasting using principal components from a large number of predictors

James H Stock and Mark W Watson. Forecasting using principal components from a large number of predictors . Journal of the American statistical association, 97 0 (460): 0 1167--1179, 2002

2002

-

[38]

A survey of weak instruments and weak identification in generalized method of moments

James H Stock, Jonathan H Wright, and Motohiro Yogo. A survey of weak instruments and weak identification in generalized method of moments . Journal of business & economic statistics , 20 0 (4): 0 518--529, 2002. ISSN 0735-0015

2002

-

[39]

Asymptotic theory for econometricians

Halbert White. Asymptotic theory for econometricians . Emerald, Bingley, rev. ed edition, 2001. ISBN 9780127466521

2001

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.