Universal Value-at-Risk superadditivity

Pith reviewed 2026-06-26 02:02 UTC · model grok-4.3

The pith

For portfolios satisfying weighted universal VaR superadditivity, every distortion risk measure is superadditive and optimal allocation concentrates on one asset.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

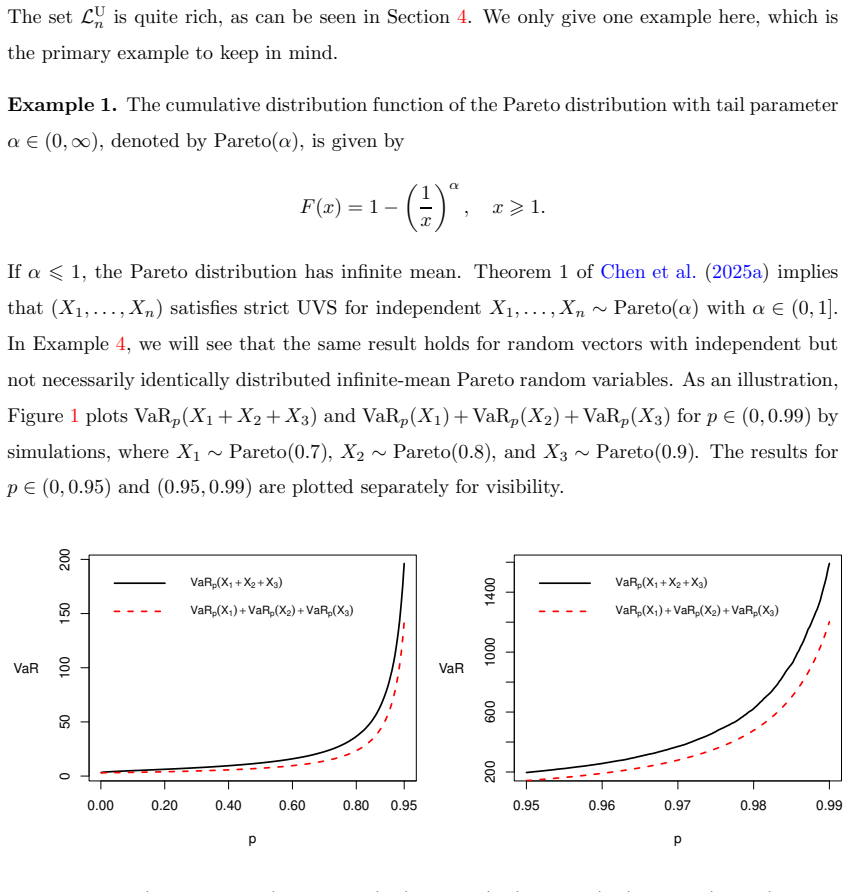

Universal value-at-risk superadditivity (UVS) holds when VaR_alpha(X + Y) >= VaR_alpha(X) + VaR_alpha(Y) for all alpha in (0,1), with the weighted version WUVS strengthening this uniformity across levels; except for trivial cases UVS requires infinite means, and the paper establishes both properties for several large families of non-iid risks while showing they survive listed operations and yield superadditivity of every distortion risk measure.

What carries the argument

Universal VaR superadditivity (UVS) and weighted UVS (WUVS) as properties of the joint distribution of a random vector, requiring superadditivity of VaR at every level and implying superadditivity for all distortion risk measures.

If this is right

- Every distortion risk measure is superadditive on any portfolio satisfying WUVS.

- An optimal allocation for such a portfolio concentrates on a single asset.

- Diversification is never beneficial under WUVS.

- Strict versions of UVS and WUVS produce stronger decision-theoretic conclusions than the non-strict versions.

Where Pith is reading between the lines

- The uniform-over-all-levels character of UVS supplies a stronger prohibition on diversification than the asymptotic superadditivity already known from extreme-value theory.

- Because the properties are stated for random vectors rather than marginals, they can be checked or imposed directly on portfolio dependence structures.

- The preservation results under mixtures and weak convergence allow UVS to be verified for limits or averaged versions of the base families.

Load-bearing premise

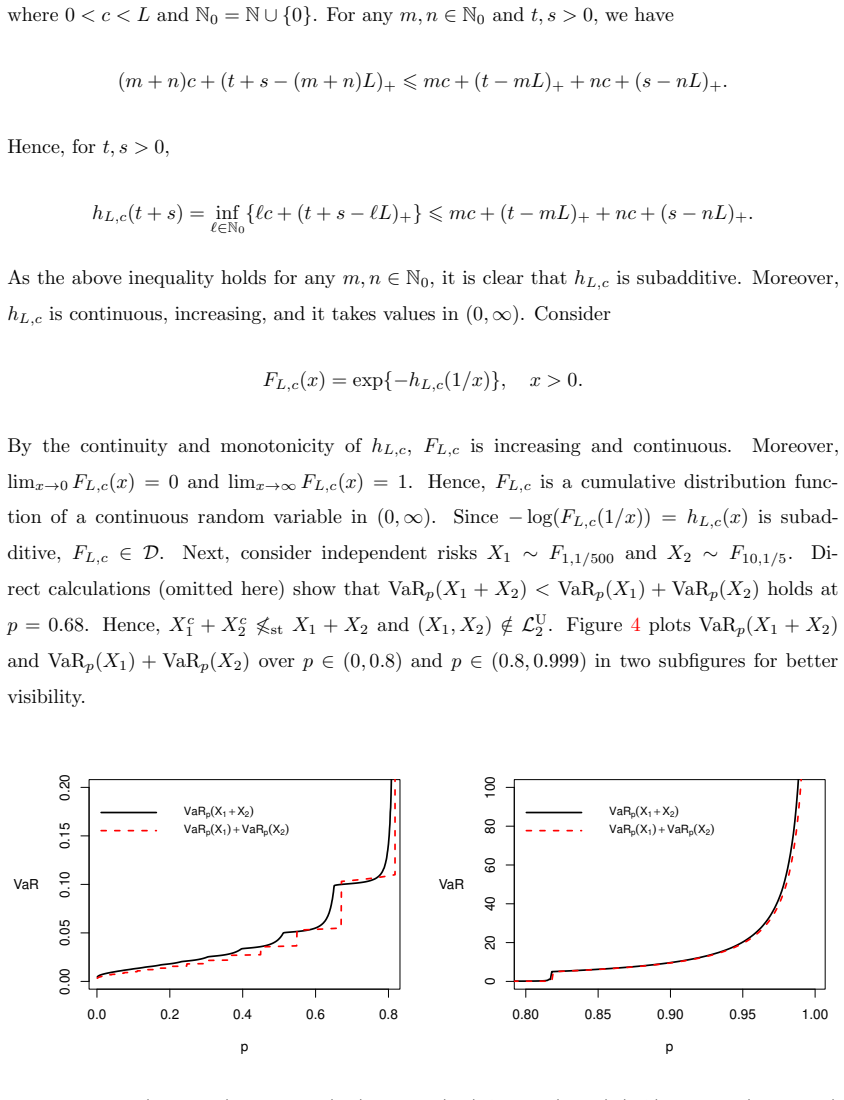

The risks must belong to the listed families that carry the required infinite-mean structure and preserve UVS and WUVS under the stated operations.

What would settle it

A counter-example random vector inside one of the families (completely subscalable, super-Cauchy, or inverted subadditive) for which VaR_alpha of the sum falls below the sum of separate VaRs at some alpha would falsify the preservation and the resulting superadditivity claims.

Figures

read the original abstract

Value-at-Risk (VaR) is a standard regulatory risk measure, and its failure of subadditivity is well known. Much less appreciated is that for sufficiently heavy-tailed losses, VaR can be superadditive uniformly across all probability levels, a phenomenon strictly stronger than the asymptotic superadditivity studied in extreme value theory. We call this property universal VaR superadditivity (UVS). We study UVS and its stronger weighted version (WUVS) as properties of random vectors rather than of marginal distributions. This perspective unifies and extends a recent line of work on iid infinite-mean models. UVS, except for trivial cases, imposes an infinite-mean structure. We establish preservation properties of UVS and WUVS under increasing and convex transformations, weak convergence, and certain distributional mixtures, and use these tools to prove UVS and WUVS for non-identically distributed risks in several large families including completely subscalable, super-Cauchy, and inverted subadditive risks, extending results previously available only in the iid case. In many results, we also establish strict versions of UVS and WUVS, which lead to stronger decision-theoretic implications. As a consequence, for any portfolio satisfying WUVS, every distortion risk measure is superadditive, so an optimal allocation concentrates on a single asset, and diversification is never beneficial.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper defines universal VaR superadditivity (UVS) and its weighted version (WUVS) as properties of random vectors (not merely marginals). It shows that UVS/WUVS, except in trivial cases, require an infinite-mean structure. Preservation of these properties is established under increasing convex transformations, weak convergence, and certain distributional mixtures. These tools are then used to prove UVS and WUVS (including strict versions) for non-identically distributed risks belonging to the families of completely subscalable, super-Cauchy, and inverted subadditive risks, extending prior iid results. The central consequence is that any portfolio satisfying WUVS makes every distortion risk measure superadditive, so optimal allocation concentrates on a single asset and diversification is never beneficial.

Significance. If the derivations hold, the work supplies a coherent unification and extension of the infinite-mean literature from the iid to the non-iid setting, with explicit preservation results that enable application across several large families. The link from WUVS to superadditivity of all distortion risk measures yields a sharp decision-theoretic implication with direct relevance to portfolio construction under heavy tails. The establishment of strict versions of UVS/WUVS strengthens the conclusions beyond the asymptotic superadditivity familiar from extreme-value theory.

major comments (1)

- [Abstract (and the section containing the mixture-preservation theorem)] The abstract states that preservation under 'certain distributional mixtures' is used to obtain the non-iid results for the listed families; the precise conditions on the mixing measure (and whether they are automatically satisfied by the target families) must be stated explicitly, as this step is load-bearing for the extension beyond the iid case.

minor comments (2)

- The introduction should include a short comparison table or explicit list of which prior iid results are recovered as special cases and which are genuinely new for the non-iid setting.

- Notation for the weighting function in WUVS should be introduced once and used consistently; currently the distinction between UVS and WUVS is clear in the abstract but may require an early displayed definition for readers.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation and the constructive comment on clarifying the mixture-preservation step. We address the single major comment below and will incorporate the requested clarification.

read point-by-point responses

-

Referee: [Abstract (and the section containing the mixture-preservation theorem)] The abstract states that preservation under 'certain distributional mixtures' is used to obtain the non-iid results for the listed families; the precise conditions on the mixing measure (and whether they are automatically satisfied by the target families) must be stated explicitly, as this step is load-bearing for the extension beyond the iid case.

Authors: We agree that the abstract and the mixture-preservation section should state the precise conditions on the mixing measure explicitly. In the revision we will add the required support, integrability, and independence conditions on the mixing measure, together with a short verification that these conditions hold for the completely subscalable, super-Cauchy, and inverted subadditive families. This will make transparent how the preservation result yields the non-iid statements. revision: yes

Circularity Check

No significant circularity

full rationale

The derivation defines UVS/WUVS on random vectors, proves preservation under increasing convex maps, weak convergence and mixtures, then applies the properties to families (completely subscalable, super-Cauchy, inverted subadditive) via explicit constructions that do not reduce to self-definition or fitted inputs. All load-bearing steps are external mathematical arguments or extensions of prior non-self-referential literature on infinite-mean models; no equation equates a claimed prediction to its own fitted parameter, and no uniqueness theorem is imported solely via author self-citation.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math VaR is the left-continuous quantile function of a loss random variable

- domain assumption Distortion risk measures are obtained by integrating the quantile function against a distortion function

invented entities (2)

-

Universal VaR superadditivity (UVS)

no independent evidence

-

Weighted universal VaR superadditivity (WUVS)

no independent evidence

Reference graph

Works this paper leans on

-

[1]

and Oliveira, P

Arab, I., Lando, T. and Oliveira, P. E. (2025). Convex combinations of random variables stochas- tically dominate the parent for a new class of heavy tailed distribution s. Electronic Commu- nications in Probability , 30:1–11

2025

-

[2]

and Heath, D

Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999). Coher ent measures of risk. Mathe- matical Finance, 9(3):203–228

1999

-

[3]

W., Savits, T

Block, H. W., Savits, T. H. and Shaked, M. (1982). Some concepts o f negative dependence. Annals of Probability , 10(3):765–772

1982

-

[4]

Chen, Y., Hu, T., Shneer, S. and Zou, Z. (2025c). Stochastic domin ance for linear combinations 31 of infinite-mean risks. arXiv:2505.01739

-

[5]

and Shneer, S

Chen, Y. and Shneer, S. (2026). Risk aggregation and stochastic dominance for a class of heavy- tailed distributions. ASTIN Bulletin , 56(1):206–219

2026

-

[6]

and Wang, R

Chen, Y. and Wang, R. (2025). Infinite-mean models in risk managem ent: Discussions and recent advances. Risk Sciences, 1:100003

2025

-

[7]

and Scandolo, G

Cont, R., Deguest, R. and Scandolo, G. (2010). Robustness and s ensitivity analysis of risk measurement procedures. Quantitative Finance , 10(6):593–606

2010

-

[8]

and Mikosch, T

Embrechts, P., Kl¨ uppelberg, C. and Mikosch, T. (1997).Modelling Extremal Events for Insurance and Finance. Springer, Heidelberg

1997

-

[9]

and W¨ uthrich, M

Embrechts, P., Lambrigger, D. and W¨ uthrich, M. (2009). Multivar iate extremes and the aggre- gation of dependent risks: examples and counter-examples. Extremes, 12(2):107–127

2009

-

[10]

and Wang, R

Embrechts, P., Liu, H. and Wang, R. (2018). Quantile-based risk sh aring. Operations Research, 66(4):936–949

2018

-

[11]

and Beler aj, A

Embrechts, P., Puccetti, G., R¨ uschendorf, L., Wang, R. and Beler aj, A. (2014). An academic response to Basel 3.5. Risks, 2(1):25–48

2014

-

[12]

Ibragimov, R. (2009). Portfolio diversification and value at risk und er thick-tailedness. Quanti- tative Finance , 9(5):565–580

2009

-

[13]

and Kato, T

Imamura, Y. and Kato, T. (2026). A note on subadditivity of value a t risks (VaRs): A new connection to comonotonicity. Journal of Applied Probability , 63:91–95

2026

-

[14]

and R¨ uschendorf, L

Mainik, G. and R¨ uschendorf, L. (2010). On optimal portfolio diver sification with respect to extreme risks. Finance and Stochastics , 14:593–623

2010

-

[15]

J., Frey, R

McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised Edition. Princeton, NJ: Princeton University Press

2015

-

[16]

Mohammed, N. (2025). VaR at its extremes: Impossibilities and cond itions for one-sided random variables. arXiv:2512.07787. M¨ uller, A. (2025). Some remarks on the effect of risk sharing and d iversification for infinite mean risks. ASTIN Bulletin , 55(3):747–756. M¨ uller, A. and Stoyan, D. (2002). Comparison Methods for Stochastic Models and Risks . Wiley...

Pith/arXiv arXiv 2025

-

[17]

Samorodnitsky, G. (2017). Stable Non-Gaussian Random Processes: Stochastic Models w ith Infinite Variance. Routledge

2017

-

[18]

Schmeidler, D. (1986). Integral representation without additivit y. Proceedings of the American 32 Mathematical Society, 97(2):255–261

1986

-

[19]

and Shanthikumar, J

Shaked, M. and Shanthikumar, J. G. (2007). Stochastic Orders. Springer, New York

2007

-

[20]

Vincent, L. (2025). Diversification and stochastic dominance: Whe n all eggs are better put in one basket. arXiv:2507.16265

arXiv 2025

-

[21]

and Wei, Y

Wang, Q., Wang, R. and Wei, Y. (2020). Distortion riskmetrics on gen eral spaces. ASTIN Bulletin, 50(4):827–851

2020

-

[22]

and Zitikis, R

Wang, R. and Zitikis, R. (2021). An axiomatic foundation for the Exp ected Shortfall. Manage- ment Science , 67:1413–1429

2021

-

[23]

Zeng, K., Zou, Z., Su, Y. and Hu, T. (2025). Further developments on stochastic dominance for different classes of infinite-mean distributions. arXiv:2511.00764. 33

Pith/arXiv arXiv 2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.