Unbiased estimation of normalized scale-invariant indices under the gamma distribution

Pith reviewed 2026-06-26 09:29 UTC · model grok-4.3

The pith

A U-statistic based on sum-proportion independence yields an unbiased estimator for any normalized scale-invariant index when data follow a gamma distribution.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

When observations are drawn from a gamma distribution, the independence between the total sum and the associated Dirichlet proportions permits construction of a U-statistic that is unbiased for every normalized scale-invariant index generated by a homogeneous function.

What carries the argument

The U-statistic that exploits independence of the total sum and Dirichlet proportions under gamma populations.

If this is right

- The same estimator applies without modification to the Gini coefficient, generalized Gini indices, entropy-based measures, and variability indices.

- Closed-form expressions for the indices themselves exist under gamma populations.

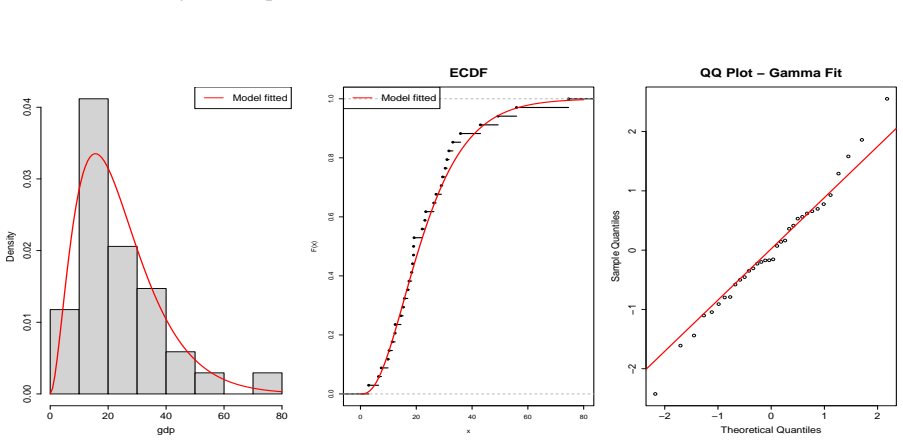

- Monte Carlo results show the estimator maintains low bias and stable variance across choices of index.

- The construction continues to perform well in simulations when the data follow a generalized gamma distribution.

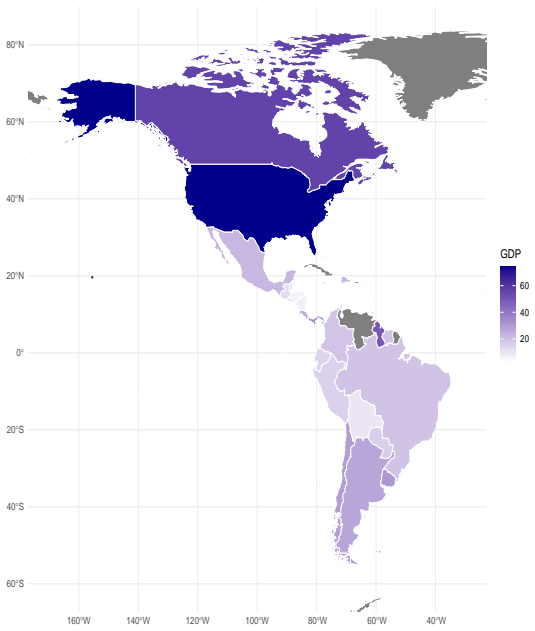

- The indices and their unbiased estimates can be computed directly on real datasets such as GDP per capita across countries.

Where Pith is reading between the lines

- If gamma is only an approximation, the estimator may still reduce finite-sample bias relative to plug-in methods that ignore the independence structure.

- The same independence device could be examined for other scale families where analogous decompositions hold approximately.

- Direct comparison of the U-statistic against the sample index on deliberately non-gamma data would measure how quickly unbiasedness degrades.

- The framework may extend to other economic or ecological indices that are homogeneous and scale-invariant.

Load-bearing premise

The data must be drawn from a gamma distribution so that the total sum and Dirichlet proportions are exactly independent.

What would settle it

Calculate the expected value of the proposed U-statistic on gamma-distributed samples and verify whether it equals the true index value for several different homogeneous functions.

Figures

read the original abstract

We introduce a broad class of normalized scale-invariant indices (NPRIs) generated by homogeneous functions and encompassing several well-known measures, including the Gini coefficient, generalized Gini indices, entropy-based measures, and variability indices. Explicit expressions are obtained for these indices under gamma populations. Exploiting the independence between the total sum and the associated Dirichlet proportions, we derive a simple unbiased estimator based on a U-statistic. The resulting estimator is shown to be unbiased for any NPRI when the underlying population follows a gamma distribution. Several examples are provided to illustrate the general theory. A Monte Carlo simulation study is carried out that shows the good performance of the unbiased estimator in several scenarios of index choices. We also present a simulation study that goes beyond the established theory by examining the estimator's applicability in settings characterized by a generalized gamma distribution. We evaluate the effectiveness of the NPRIs and their estimates in modeling a real-world dataset related to gross domestic product per capita in the Americas.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript defines a class of normalized scale-invariant indices (NPRIs) via homogeneous functions (encompassing Gini, generalized Gini, entropy, and variability measures), derives explicit expressions for these indices when the population is gamma, and constructs an unbiased U-statistic estimator that exploits the classical independence of the sample sum and the Dirichlet vector of proportions. The central result is that this estimator is unbiased for any NPRI under i.i.d. gamma sampling. The paper supplies examples, Monte Carlo illustrations under gamma and generalized gamma, and an application to GDP-per-capita data.

Significance. If the derivation holds, the work supplies a parameter-free, unbiased estimator for an entire family of scale-invariant functionals under the gamma model by direct application of the gamma-Dirichlet independence and U-statistic theory. This is a clean methodological contribution that avoids plug-in estimation of shape or scale parameters and directly yields unbiasedness for the listed indices once the homogeneous-function representation is verified.

minor comments (2)

- The Monte Carlo section examines performance under the generalized gamma distribution, which lies outside the gamma theory; a short paragraph explaining the motivation for this extension (e.g., robustness check) would improve readability.

- Notation for the homogeneous-function class and the associated kernel of the U-statistic could be introduced with one additional displayed equation in the general-theory section to make the transition from the abstract definition to the estimator fully explicit.

Simulated Author's Rebuttal

We thank the referee for the positive assessment of the manuscript, the accurate summary of its contributions, and the recommendation for minor revision. No specific major comments were listed in the report.

Circularity Check

No significant circularity detected

full rationale

The paper's central derivation establishes an unbiased U-statistic estimator for any NPRI (defined via homogeneous functions) under i.i.d. gamma sampling by invoking the standard gamma property that the total sum is independent of the Dirichlet vector of proportions; this independence directly implies that the expectation of any scale-invariant functional of the proportions equals the expectation of a symmetric kernel, so the U-statistic is unbiased by the usual U-statistic theory. No step reduces to a fitted parameter renamed as prediction, a self-definitional loop, or a load-bearing self-citation; the gamma independence is an external, well-known fact independent of the present work, and the Monte Carlo and data sections are presented only as illustrations. The logical chain (homogeneous function → scale invariance → Dirichlet representation → U-statistic kernel) is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Observations are i.i.d. from a gamma distribution, enabling independence of total sum and Dirichlet proportions.

- domain assumption The indices are generated by homogeneous functions of a certain degree.

Reference graph

Works this paper leans on

-

[1]

A. B. Atkinson, On the measurement of inequality, Journal of Economic Theory, 2(3):244--263, 1970

1970

-

[2]

P. S. Bullen, Handbook of Means and Their Inequalities, Springer, Dordrecht, 2003

2003

-

[3]

T. M. Cover and J. A. Thomas, Elements of Information Theory, 2nd ed., Wiley, Hoboken, 2006

2006

-

[4]

F. A. Cowell. Measuring Inequality. 3rd ed., Oxford University Press, Oxford, 2011

2011

-

[5]

H. A. David and H. N. Nagaraja, Order Statistics, 3rd ed., Wiley, Hoboken, 2003

2003

-

[6]

J. M. Gavilan-Ruiz, \'A. Ruiz-G\'andara, F.J. Ortega-Irizo and L. Gonzalez-Abril, Some Notes on the Gini Index and New Inequality Measures: The nth Gini Index. Stats , 7:1354--1365, 2024

2024

-

[7]

Gini, Variabilit\`a e mutabilit\`a, Studi Economico-Giuridici della R

C. Gini, Variabilit\`a e mutabilit\`a, Studi Economico-Giuridici della R. Universit\`a di Cagliari, 1912

1912

-

[8]

C. Gini. On the measure of concentration with special reference to income and statistics. Colorado College Publication, General Series, 208 , 73--79, 1936

1936

-

[9]

N. Henze. Asymptotic Stochastics: An Introduction with a View towards Statistics. Springer Berlin, Heidelberg, 2024

2024

-

[10]

Hoeffding

W. Hoeffding. A class of statistics with asymptotically normal distribution. Annals of Mathematical Statistics , 19, 293–325, 1948

1948

-

[11]

A. J. Lee. U-Statistics. Marcel Dekker, New York, 1990

1990

-

[12]

A. W. Marshall, I. Olkin and B. C. Arnold, Inequalities: Theory of Majorization and Its Applications, 2nd ed., Springer, New York, 2011

2011

-

[13]

J. E. Mosimann, On the Compound Multinomial Distribution, the Multivariate Beta-Distribution, and Correlations among Proportions. Biometrika , 49:65--82, 1962

1962

-

[14]

Shaked and J

M. Shaked and J. G. Shanthikumar, Stochastic Orders, Springer, New York, 2007

2007

-

[15]

C. E. Shannon, A mathematical theory of communication, Bell System Technical Journal, 27:379--423, 623--656, 1948

1948

-

[16]

R. Vila and H. Saulo, The mth Gini index estimator: Unbiasedness for gamma populations. The Journal of Economic Inequality , 2026. https://doi.org/10.1007/s10888-025-09715-3

-

[17]

Vila and H

R. Vila and H. Saulo, An unbiased estimator of a novel extended mth Gini index for gamma distributed populations. Journal of Computational and Applied Mathematics , 482:117320, 2026

2026

-

[18]

R. Vila and H. Saulo, Bias analysis of a linear order-statistic inequality index estimator: Unbiasedness under gamma populations. Preprint , 2026. https://arxiv.org/abs/2602.14861

Pith/arXiv arXiv 2026

-

[19]

Yitzhaki and E

S. Yitzhaki and E. Schechtman, The Gini Methodology: A Primer on a Statistical Methodology, Springer, New York, 2013

2013

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.