Multivariate reconciliation for hierarchical time series

Pith reviewed 2026-05-20 01:25 UTC · model grok-4.3

The pith

A multivariate reconciliation method produces coherent hierarchical forecasts that improve accuracy by incorporating correlations among variables.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The proposed multivariate reconciliation methodology ensures coherent forecasts across a hierarchy of multiple time series by incorporating relationships among the variables rather than reconciling each variable independently.

What carries the argument

Multivariate reconciliation procedure that adjusts a vector of base forecasts to satisfy hierarchical aggregation constraints while using the covariance structure among the series.

If this is right

- Forecasts at every level of the hierarchy remain consistent for all variables simultaneously.

- Accuracy gains appear in both simulated hierarchies with varying correlation structures and in real employment data.

- Different base forecasting models can be plugged into the same reconciliation step and compared directly.

- The method generalizes the univariate reconciliation framework to the multivariate case without separate processing of each series.

Where Pith is reading between the lines

- The approach could be applied to joint forecasting of related economic indicators such as sales across product categories.

- Extensions might examine how the method behaves when some series in the hierarchy have missing observations.

- Scalability tests on very large hierarchies would show whether estimating the full cross-variable covariance remains practical.

Load-bearing premise

That correlations among the multiple variables can be reliably estimated from data and used to improve accuracy without breaking the hierarchical aggregation rules.

What would settle it

On a new collection of hierarchical series where the variables are known to be uncorrelated, the multivariate method should show no accuracy gain over separate univariate reconciliation while still preserving coherence.

Figures

read the original abstract

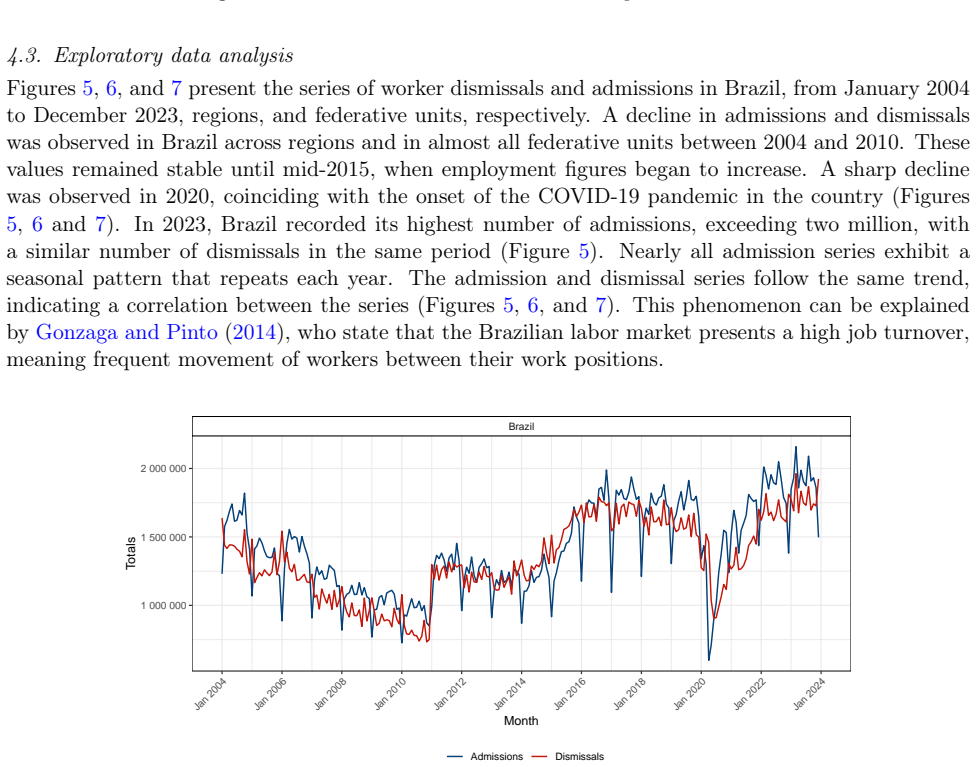

Some time series can be hierarchically organized into levels based on certain characteristics, such as geography or other attributes of interest. These series are referred to as hierarchical time series. Typically, forecasts are generated at all levels to ensure coherence, meaning that the forecasts should satisfy the same aggregation constraints as the observed data. Various approaches have been proposed to guarantee this coherence by using a set of base forecasts. The process through which these forecasts are adjusted to become coherent is known as forecast reconciliation. Similar to the univariate case, multivariate time series can also be structured hierarchically. However, all existing approaches are limited to a single variable. As a result, ensuring coherent forecasts requires reconciling each variable separately. However, this process does not account for correlations among multiple variables. To address this limitation, this paper proposes a multivariate reconciliation methodology that ensures coherent forecasts and incorporates relationships among variables. The proposed methodology was tested through numerical simulations, considering distinct scenarios within the series hierarchy and across multiple variables. Additionally, some base forecasting models were evaluated. The methodology was also applied to real employment data of admissions and dismissals in Brazil. The results demonstrated that multivariate reconciliation yielded more accurate outcomes than the other methods considered, both in simulated data and in practical applications.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a multivariate extension of forecast reconciliation for hierarchical time series. Unlike existing univariate approaches that reconcile each variable independently, the new method incorporates cross-variable correlations while enforcing the hierarchical aggregation constraints. The approach is evaluated via numerical simulations across different hierarchy scenarios and base forecasting models, and is applied to real Brazilian employment data on admissions and dismissals, where it is reported to produce more accurate forecasts than competing methods.

Significance. If the central claims hold, the work would constitute a natural and useful generalization of established reconciliation techniques such as MinT. By jointly modeling inter-variable dependence, it could improve accuracy in applications where multiple related series (e.g., economic or labor-market indicators) share a hierarchical structure, while still guaranteeing coherence.

major comments (2)

- [Abstract and §3] Abstract and §3 (methodology): the central claim of improved accuracy rests on the construction of a valid multivariate reconciliation matrix that respects both the aggregation constraints and the estimated joint covariance. No explicit matrix form, algorithm, or proof of positive-definiteness/stability is supplied in the visible text, making it impossible to verify that the estimator does not introduce bias or become ill-conditioned when correlations are estimated from finite samples.

- [§4] §4 (simulation study): the abstract states that multivariate reconciliation yields more accurate outcomes, yet no error metric (e.g., RMSE, MASE), no statistical test for significance of differences, and no description of how the correlation matrix is estimated or regularized are provided. Without these details the reported superiority cannot be assessed or reproduced.

minor comments (2)

- Clarify the notation for the multivariate base forecasts and the exact form of the reconciliation matrix (e.g., whether it is a direct extension of the MinT projection or a different optimization).

- Add a brief discussion of computational cost and scalability for large hierarchies or many variables.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments on our manuscript. We have carefully reviewed the major concerns and provide point-by-point responses below. We agree that additional details are needed for clarity and reproducibility, and we will incorporate the suggested improvements in the revised version.

read point-by-point responses

-

Referee: [Abstract and §3] Abstract and §3 (methodology): the central claim of improved accuracy rests on the construction of a valid multivariate reconciliation matrix that respects both the aggregation constraints and the estimated joint covariance. No explicit matrix form, algorithm, or proof of positive-definiteness/stability is supplied in the visible text, making it impossible to verify that the estimator does not introduce bias or become ill-conditioned when correlations are estimated from finite samples.

Authors: We acknowledge that the explicit closed-form expression for the multivariate reconciliation matrix, the associated algorithm, and a formal discussion of its properties were not presented with sufficient detail in the submitted version. In the revision we will add the matrix form W = (S' V^{-1} S)^{-1} S' V^{-1}, where V denotes the estimated joint covariance of the base forecasts and S is the aggregation matrix, together with a step-by-step computational algorithm. We will also include a brief argument establishing that the reconciled forecasts remain unbiased under the usual linear constraints and that positive-definiteness of V is preserved when a shrinkage estimator is used; the same shrinkage step will be shown to guarantee numerical stability for finite-sample correlation estimates. revision: yes

-

Referee: [§4] §4 (simulation study): the abstract states that multivariate reconciliation yields more accurate outcomes, yet no error metric (e.g., RMSE, MASE), no statistical test for significance of differences, and no description of how the correlation matrix is estimated or regularized are provided. Without these details the reported superiority cannot be assessed or reproduced.

Authors: We agree that the simulation results lack the quantitative detail required for assessment and reproduction. In the revised manuscript we will report both RMSE and MASE for all methods and scenarios, include Diebold-Mariano tests (or paired t-tests where appropriate) to evaluate the statistical significance of accuracy differences, and describe the correlation-matrix estimator explicitly, including the use of the sample covariance with Ledoit-Wolf shrinkage regularization to mitigate ill-conditioning in finite samples. revision: yes

Circularity Check

No significant circularity detected

full rationale

The paper introduces a multivariate forecast reconciliation method for hierarchical time series that extends existing univariate approaches by incorporating cross-variable correlations while enforcing aggregation constraints. The derivation is presented as a direct generalization, with the central claims supported by performance comparisons on independently generated simulation scenarios (varying hierarchy structures and variable counts) and an external real-world dataset of Brazilian employment admissions and dismissals. No equations or steps reduce by construction to fitted parameters, self-definitions, or self-citation chains; the accuracy results are evaluated against baselines using held-out test data, rendering the methodology self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

vec(eYT+h|T) = S*[S'*W_h^{-1}S*]^{-1}S'*W_h^{-1} vec(bYT+h|T) (eq. 10); multivariate coherence constraint C* vec(Yt)=0

-

IndisputableMonolith/Foundation/ArithmeticFromLogic.leanLogicNat recovery unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

nine simulation scenarios using V and Sigma correlation matrices; ARIMA/ETS/VAR base forecasts

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

- [1]

-

[2]

Athanasopoulos, George and Ahmed, Roman A and Hyndman, Rob J , journal =. Hierarchical forecasts for

-

[3]

Forecasting with temporal hierarchies , volume =

Athanasopoulos, George and Hyndman, Rob J and Kourentzes, Nikolaos and Petropoulos, Fotios , journal =. Forecasting with temporal hierarchies , volume =

-

[4]

Athanasopoulos, George and Hyndman, Rob J and Kourentzes, Nikolaos and Panagiotelis, Anastasios , journal =. Forecast reconciliation:

-

[5]

Time series analysis: forecasting and control , year =

Box, George EP and Jenkins, Gwilym M and Reinsel, Gregory C and Ljung, Greta M , publisher =. Time series analysis: forecasting and control , year =

-

[6]

Brown, Robert Goodell , title =

-

[7]

Large air quality and public health impacts due to

Butt, Edward W and Conibear, Luke and Knote, Christoph and Spracklen, Dominick V , journal =. Large air quality and public health impacts due to

-

[8]

Corseuil, Carlos Henrique and Foguel, Miguel and Gonzaga, Gustavo and Ribeiro, Eduardo Pontual , booktitle =. Youth labor market in

-

[9]

Redes neurais artificiais na previs

Vigan. Redes neurais artificiais na previs. Revista Brasileira de Geografia F

-

[10]

da Silva, G.B.S. and Fasiaben, M. and Nogueira, S.F. and Grego, C.R. and Moraes, A.S. and Almeida, M.M.T.B. and de Oliveira, O.C. and Eusebio, G.S. and Lopes, W.M.O. , journal =. M

-

[11]

Dangerfield, Byron J and Morris, John S , journal =. Top-down or bottom-up:

-

[12]

Davydenko, Andrey and Fildes, Robert , journal =. Measuring forecasting accuracy: The case of judgmental adjustments to SKU-level demand forecasts , volume =

-

[13]

de Andrade Baltar, Paulo Eduardo , journal =. Estagna

-

[14]

Di Fonzo, Tommaso and Girolimetto, Daniele , journal =. Cross-temporal forecast reconciliation: Optimal combination method and heuristic alternatives , volume =

-

[15]

fable: Forecasting Models for Tidy Time Series , url =

Mitchell O'Hara-Wild and Rob J Hyndman and Earo Wang , note =. fable: Forecasting Models for Tidy Time Series , url =

-

[16]

fable.prophet: Prophet Modelling Interface for ``fable'' , url =

Mitchell O'Hara-Wild , note =. fable.prophet: Prophet Modelling Interface for ``fable'' , url =

-

[17]

Exponential smoothing: The state of the art , volume =

Gardner Jr, Everette S , journal =. Exponential smoothing: The state of the art , volume =

-

[18]

Forecasting trends in time series , volume =

Gardner Jr, Everette S and McKenzie, ED , journal =. Forecasting trends in time series , volume =

-

[19]

Gawe. Global and Local Approaches for Forecasting of Long-Term Natural Gas Consumption in Poland Based on Hierarchical Short Time Series , volume =. Energies , number =

-

[20]

Girolimetto, Daniele and Di Fonzo, Tommaso , journal =. Point and probabilistic forecast reconciliation for general linearly constrained multiple time series , volume =

-

[21]

Rotatividade do trabalho e incentivos da legisla

Gustavo Gonzaga and Rafael Cayres Pinto , copyright =. Rotatividade do trabalho e incentivos da legisla

-

[22]

Rotatividade e qualidade do emprego no

Gonzaga, Gustavo , journal =. Rotatividade e qualidade do emprego no

-

[23]

Disaggregation methods to expedite product line forecasting , volume =

Gross, Charles W and Sohl, Jeffrey E , journal =. Disaggregation methods to expedite product line forecasting , volume =

-

[24]

Understanding forecast reconciliation , volume =

Hollyman, Ross and Petropoulos, Fotios and Tipping, Michael E , journal =. Understanding forecast reconciliation , volume =

-

[25]

Forecasting trends and seasonals by exponentially weighted moving averages , volume =

Holt, Charles C , journal =. Forecasting trends and seasonals by exponentially weighted moving averages , volume =

-

[26]

A state space framework for automatic forecasting using exponential smoothing methods , volume =

Hyndman, Rob J and Koehler, Anne B and Snyder, Ralph D and Grose, Simone , journal =. A state space framework for automatic forecasting using exponential smoothing methods , volume =

-

[27]

Another look at measures of forecast accuracy , volume =

Hyndman, Rob J and Koehler, Anne B , journal =. Another look at measures of forecast accuracy , volume =

-

[28]

Automatic time series forecasting: the forecast package for

Hyndman, Rob J and Khandakar, Yeasmin , journal =. Automatic time series forecasting: the forecast package for

-

[29]

Forecasting with exponential smoothing: the state space approach , year =

Hyndman, Rob J and Koehler, Anne B and Ord, J Keith and Snyder, Ralph D , publisher =. Forecasting with exponential smoothing: the state space approach , year =

-

[30]

Optimal combination forecasts for hierarchical time series , volume =

Hyndman, Rob J and Ahmed, Roman A and Athanasopoulos, George and Shang, Han Lin , journal =. Optimal combination forecasts for hierarchical time series , volume =

-

[31]

Fast computation of reconciled forecasts for hierarchical and grouped time series , volume =

Hyndman, Rob J and Lee, Alan J and Wang, Earo , journal =. Fast computation of reconciled forecasts for hierarchical and grouped time series , volume =

-

[32]

Forecasting: Principles and Practice , url =

Hyndman, Rob J and Athanasopoulos, George , edition =. Forecasting: Principles and Practice , url =

-

[33]

Rob J Hyndman and G. Athanasopoulos , edition =. Forecasting: Principles and Practice , url =

- [34]

-

[35]

Lila, Maur. Forecasting unemployment in Brazil: A robust reconciliation approach using hierarchical data , volume =. Socio-Economic Planning Sciences , pages =

-

[36]

Mattei, Lauro and Heinen, Vicente Loeblein , journal =. Impactos da crise da

-

[37]

Mesquita Lopes Cabreira, Marlon and Leite Coelho da Silva, Felipe and da Silva Cordeiro, Josiane and Serrano Hern. A Hybrid Approach for Hierarchical Forecasting of Industrial Electricity Consumption in Brazil , volume =. Energies , number =

-

[38]

Forecasting hierarchical time series in supply chains: an empirical investigation , volume =

Mircetic, Dejan and Rostami-Tabar, Bahman and Nikolicic, Svetlana and Maslaric, Marinko , journal =. Forecasting hierarchical time series in supply chains: an empirical investigation , volume =

-

[39]

Predicting fires for policy making:

Morello, Thiago Fonseca and Ramos, Rossano Marchetti and Anderson, Liana O and Owen, Nathan and Rosan, Thais Michele and Steil, Lara , journal =. Predicting fires for policy making:

-

[40]

Morettin, Pedro A and Toloi, Cl. An. An

- [41]

-

[42]

Bayesian spatio-temporal modeling of the Brazilian fire spots between 2011 and 2022 , volume =

Pimentel, Jonatha Sousa and Bulh. Bayesian spatio-temporal modeling of the Brazilian fire spots between 2011 and 2022 , volume =. Scientific Reports , number =

work page 2011

-

[43]

Hierarchical Time Series Forecasting of Fire Spots in Brazil: A Comprehensive Approach , volume =

Pinheiro, Ana Caroline and Rodrigues, Paulo Canas , journal =. Hierarchical Time Series Forecasting of Fire Spots in Brazil: A Comprehensive Approach , volume =

-

[44]

Pivello, V. Understanding. Perspectives in Ecology and Conservation , number =

-

[45]

R: A Language and Environment for Statistical Computing , url =

- [46]

-

[47]

Rocha, Rudi and Sant’Anna, Andr. Winds of fire and smoke:. World Development , pages =

-

[48]

Santos, Juliana Ferreira and Soares, Ronaldo Viana and Batista, Antonio Carlos , journal =. Perfil dos inc

-

[49]

Sch. A shrinkage approach to large-scale covariance matrix estimation and implications for functional genomics , volume =. Statistical Applications in Genetics and Molecular Biology , number =

-

[50]

Macroeconomics and reality , year =

Sims, Christopher A , journal =. Macroeconomics and reality , year =

-

[51]

Soares, Ronaldo Viana and Santos, Juliana Ferreira , journal =. Perfil dos inc

-

[52]

Further analysis of the data by Akaike's information criterion and the finite corrections , volume =

Sugiura, Nariaki , journal =. Further analysis of the data by Akaike's information criterion and the finite corrections , volume =

-

[53]

Sulandari, Winita and Suhartono and Subanar and Rodrigues, Paulo Canas , journal =. Exponential smoothing on modeling and forecasting multiple seasonal time series: An overview , volume =

-

[54]

Forecasting at scale , volume =

Taylor, Sean J and Letham, Benjamin , journal =. Forecasting at scale , volume =

-

[55]

Torres, Fillipe Tamiozzo Pereira and Lima, Gumercindo Souza and Costa, A das G and F. Perfil dos inc. Floresta, Curitiba , number =

-

[56]

Prediction and modeling of forest fires in the

Vigan. Prediction and modeling of forest fires in the. Revista Brasileira de Meteorologia , number =

-

[57]

Wickramasuriya, Shanika L and Athanasopoulos, George and Hyndman, Rob J , journal =. Optimal forecast reconciliation for hierarchical and grouped time series through trace minimization , volume =

-

[58]

Forecasting sales by exponentially weighted moving averages , volume =

Winters, Peter R , journal =. Forecasting sales by exponentially weighted moving averages , volume =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.