A Kernel Score Perspective on Forecast Disagreement and the Linear Pool

Pith reviewed 2026-05-23 07:09 UTC · model grok-4.3

The pith

Forecast disagreement among component distributions affects linear pool performance under any kernel scoring rule, with a new condition for optimal equal weights.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Several results on linear pooling generalize from squared error loss to all kernel scores. Forecast disagreement measured as the average pairwise divergence of component distributions has important implications for the linear pool's performance. The results are useful for understanding and designing linear pools in general combination settings. In particular, they motivate using the linear pool as opposed to other combination formulas and yield a novel condition under which equal combination weights are optimal under a given kernel scoring rule.

What carries the argument

Kernel scoring rules, the family that generalizes squared error loss and includes the Continuous Ranked Probability Score and Energy Score, together with the measure of forecast disagreement defined as average pairwise divergence of component distributions.

If this is right

- The linear pool is motivated over other combination formulas when kernel scores are used.

- Equal combination weights are optimal under the novel condition derived for any given kernel scoring rule.

- Disagreement among component forecasts can be used to assess and improve the performance of linear pools.

- The generalizations apply uniformly to point and distribution forecasts in all listed dimensions and data types.

Where Pith is reading between the lines

- Forecasters could compute disagreement in advance to decide whether linear pooling will improve accuracy under a chosen kernel score.

- The condition for equal weights might be checked empirically in applications such as macroeconomic or ensemble forecasting.

- Similar disagreement measures could be tested with scoring rules outside the kernel family to see whether the optimality results carry over.

Load-bearing premise

The mathematical properties that allow results on linear pooling under squared error loss extend without additional restrictions to the entire family of kernel scores across univariate, multivariate, discrete, and continuous settings.

What would settle it

A specific kernel score or forecast setting, such as a multivariate discrete case, in which the linear pooling results fail to generalize or the stated condition for equal weights does not produce the optimal score value.

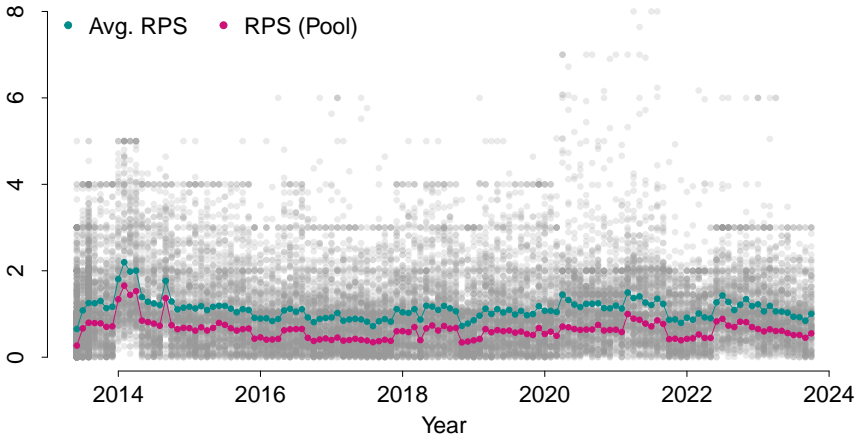

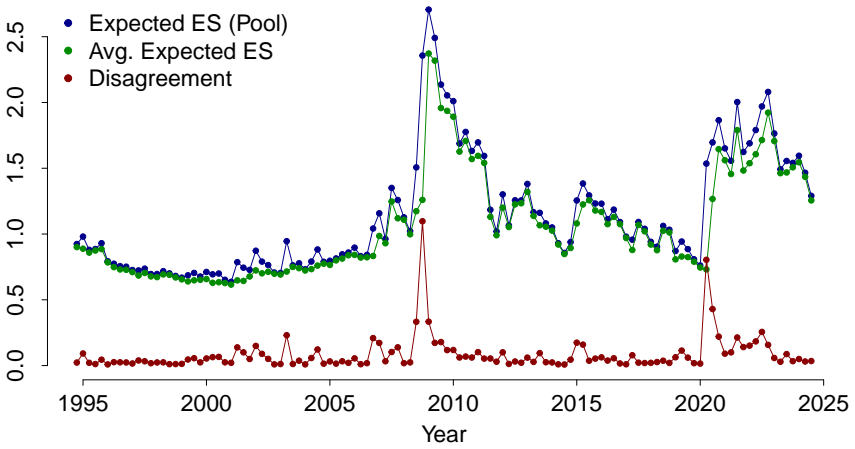

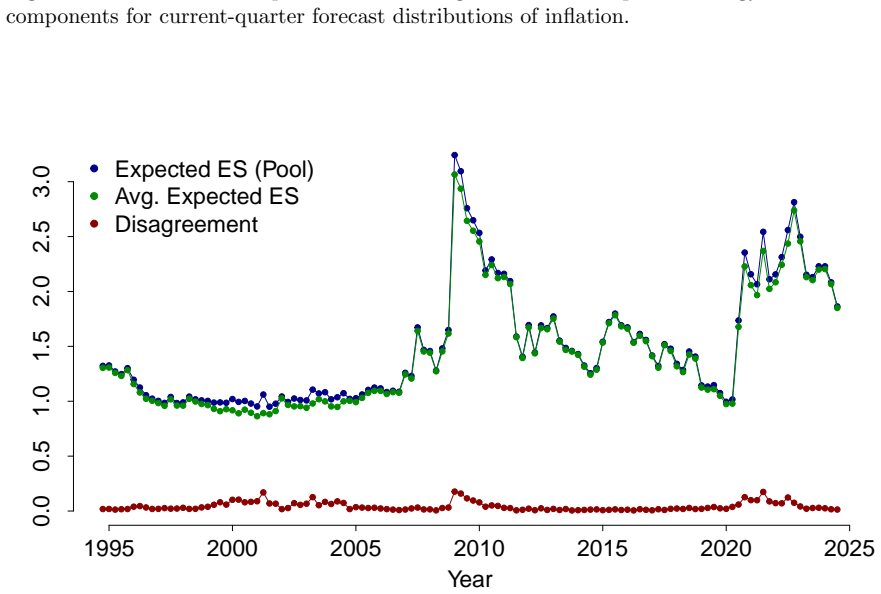

Figures

read the original abstract

This paper generalizes several results on linear pooling from squared error loss to all kernel scores. The latter are a rich family of scoring rules that covers point and distribution forecasts for univariate and multivariate, discrete and continuous settings. Its members include the Continuous Ranked Probability Score for univariate distribution forecasting and the Energy Score for multivariate distribution forecasting. Our results indicate that forecast disagreement (measured as the average pairwise divergence of all component distributions) has important implications for the linear pool's performance. The results are useful for understanding and designing linear pools in general combination settings. In particular, they motivate using the linear pool (as opposed to other combination formulas) and yield a novel condition under which equal combination weights are optimal under a given kernel scoring rule.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper generalizes several results on linear pooling of forecasts from squared error loss to the family of kernel scores. These include the CRPS for univariate distribution forecasts and the Energy Score for multivariate cases, covering point and distribution forecasts in univariate/multivariate and discrete/continuous settings. It shows that forecast disagreement (average pairwise divergence of component distributions) affects linear pool performance and derives a novel condition under which equal weights are optimal for a given kernel score.

Significance. If the generalization holds, the work supplies a unified framework for linear forecast combination under a broad class of proper scoring rules. The extension relies on shared integral representations and properness properties of kernel scores to carry over decompositions and optimality conditions from squared error without further restrictions, yielding practical implications for when linear pools are preferable and when equal weights are optimal.

minor comments (1)

- [Abstract] Abstract: the claim that results 'extend without additional restrictions' is stated but the abstract provides no preview of the specific properties (e.g., integral representation) used to establish this; a one-sentence indication would improve readability.

Simulated Author's Rebuttal

We thank the referee for the supportive summary and recommendation of minor revision. No specific major comments or requested changes were provided in the report.

Circularity Check

No significant circularity

full rationale

The paper generalizes known results on linear pooling under squared error loss to the family of kernel scores by invoking shared integral representations and properness properties that hold across the family. These properties are external to the target results on disagreement and equal-weight optimality; no equation reduces a claimed prediction or optimality condition to a fitted parameter, self-definition, or load-bearing self-citation. The derivation chain remains self-contained against the stated assumptions on kernel scores.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Kernel scores are proper scoring rules that generalize squared error loss across the listed forecast settings.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.