Effects of analyst sentiment on volatility dynamics in financial market

Pith reviewed 2026-06-28 16:30 UTC · model grok-4.3

The pith

Pessimistic sentiment from analyst reports affects future volatility in the Chinese stock market, while optimistic sentiment does not.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

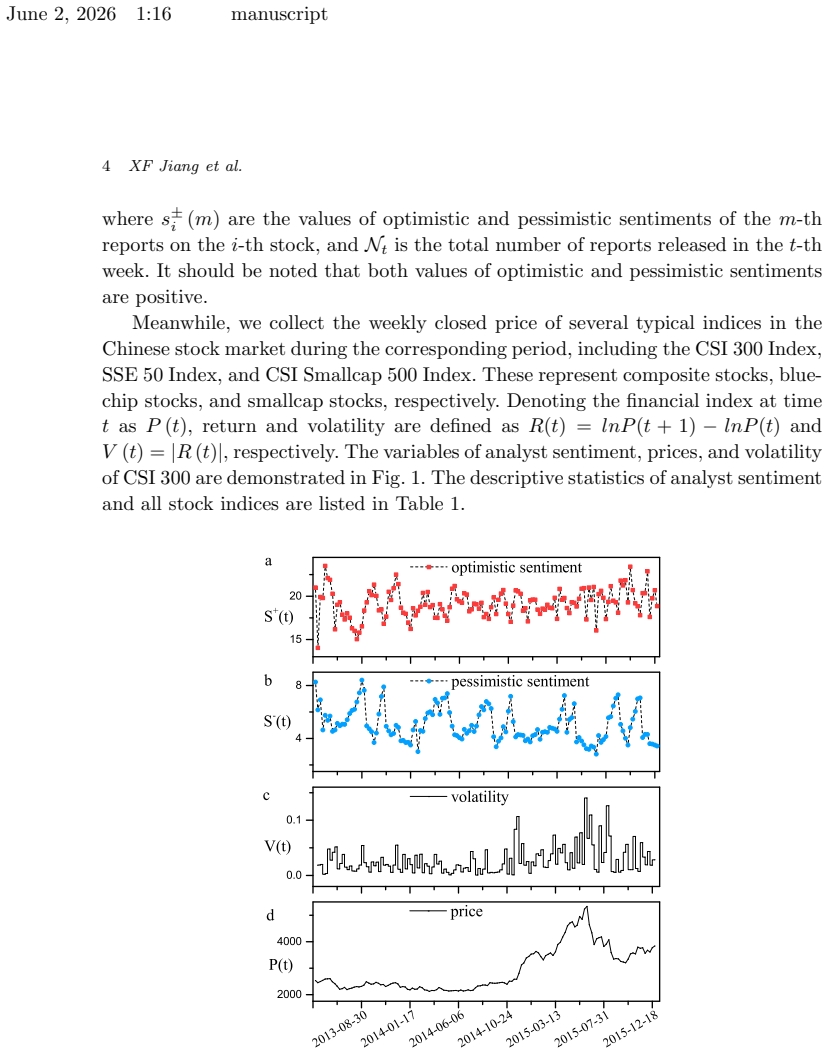

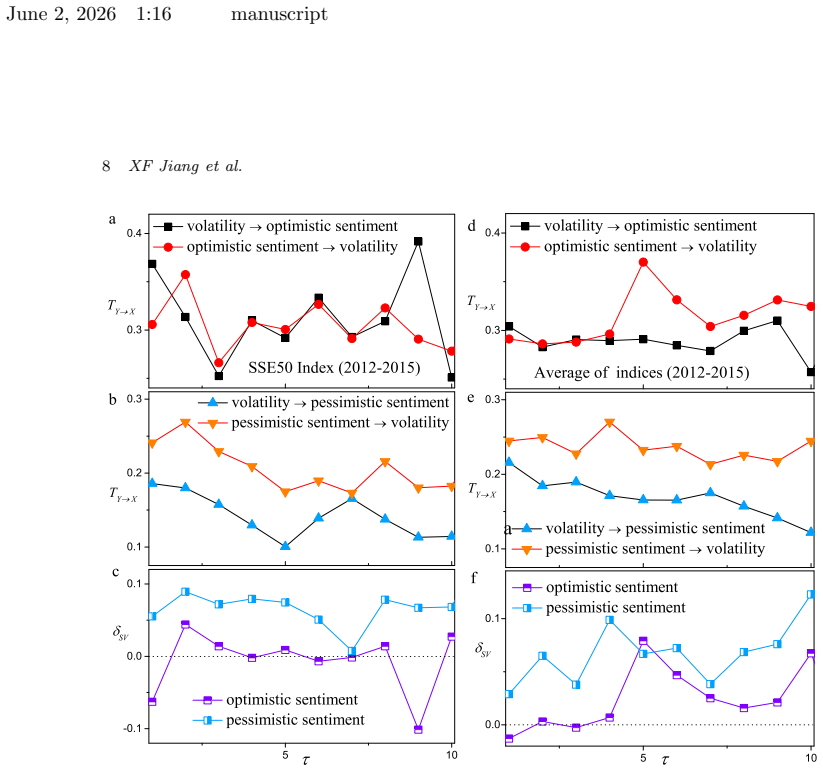

Text emotions are extracted using natural language processing technique on a substantial corpus of analyst reports on the Chinese stock market. Subsequently, the text-based analyst sentiment indices are constructed. It is observed that both optimistic and pessimistic sentiments represent short-range memory. Optimistic and pessimistic sentiments are correlated with volatility positively and negatively, respectively. The analysis of transfer entropy reveals that past pessimistic sentiment affects future volatility. Further, we model the driving effect of analyst sentiment on volatility using a GARCH model. The results show that pessimistic sentiment is an explanatory factor for volatility, whi

What carries the argument

Transfer entropy from pessimistic sentiment indices to volatility series, combined with a GARCH model that treats the sentiment indices as explanatory variables for volatility.

If this is right

- Past pessimistic sentiment affects future volatility.

- Pessimistic sentiment serves as an explanatory factor inside a GARCH volatility model.

- Optimistic sentiment shows no explanatory power for volatility.

- Both optimistic and pessimistic sentiment series exhibit only short-range memory.

Where Pith is reading between the lines

- Volatility forecasting models could gain accuracy by adding pessimistic sentiment as an input if the index construction holds up.

- The observed asymmetry implies that negative analyst information propagates to risk measures more readily than positive information.

- The same transfer-entropy test could be applied to analyst reports from other markets to check whether the pessimistic-only effect is general.

Load-bearing premise

The natural language processing method produces sentiment indices that accurately reflect true analyst sentiment without material bias from report selection or text processing choices.

What would settle it

An independent dataset of analyst reports in which transfer entropy from the pessimistic index to volatility is statistically insignificant and the GARCH coefficient on pessimistic sentiment is zero would falsify the central claim.

Figures

read the original abstract

Text emotions are extracted using natural language processing technique on a substantial corpus of analyst reports on the Chinese stock market. Subsequently, the text-based analyst sentiment indices are constructed. It is observed that both optimistic and pessimistic sentiments represent short-range memory. Optimistic and pessimistic sentiments are correlated with volatility positively and negatively, respectively. The analysis of transfer entropy reveals that past pessimistic sentiment affects future volatility. Further, we model the driving effect of analyst sentiment on volatility using a GARCH model. The results show that pessimistic sentiment is an explanatory factor for volatility, while optimistic sentiment is not.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper applies NLP to a corpus of analyst reports on the Chinese stock market to construct optimistic and pessimistic sentiment indices. Both indices exhibit short-range memory; optimistic sentiment correlates positively and pessimistic sentiment correlates negatively with volatility. Transfer entropy analysis indicates that past pessimistic sentiment influences future volatility, while a GARCH model identifies pessimistic sentiment as an explanatory variable for volatility but finds no such role for optimistic sentiment.

Significance. If the sentiment indices are shown to be valid and the statistical results survive robustness and out-of-sample checks, the work would add to the behavioral-finance literature by providing directional evidence that analyst pessimism affects volatility in an emerging market, with potential implications for volatility forecasting and market-microstructure models.

major comments (3)

- [Abstract / Methods] Abstract and Methods: the construction of the sentiment indices via NLP is described only at a high level; no inter-annotator agreement, correlation with human-coded subsample, or robustness to alternative lexica or report-selection criteria is reported. Because both the transfer-entropy directionality and the GARCH coefficients rest on these indices, the absence of validation is load-bearing for the central claim.

- [GARCH model] GARCH section: sentiment enters the conditional-variance equation as a fitted regressor on the same volatility series used for estimation. Without explicit out-of-sample tests or parameter-free validation, the reported explanatory power of pessimistic sentiment risks being an in-sample artifact rather than evidence of a genuine driving effect.

- [Transfer entropy analysis] Transfer-entropy and correlation results: the manuscript supplies no sample sizes, standard errors, or robustness checks (e.g., alternative lag choices, subsample stability, or controls for contemporaneous market tone). These omissions prevent assessment of whether the reported directional effect of pessimistic sentiment is statistically reliable.

minor comments (1)

- [Abstract] The abstract states that optimistic sentiment is 'correlated with volatility positively' and pessimistic sentiment 'negatively,' but does not specify the precise correlation measure or lag structure; a short clarification would improve readability.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback, which highlights important areas for improving the transparency and robustness of our results. We address each major comment below and will incorporate revisions to strengthen the manuscript.

read point-by-point responses

-

Referee: [Abstract / Methods] Abstract and Methods: the construction of the sentiment indices via NLP is described only at a high level; no inter-annotator agreement, correlation with human-coded subsample, or robustness to alternative lexica or report-selection criteria is reported. Because both the transfer-entropy directionality and the GARCH coefficients rest on these indices, the absence of validation is load-bearing for the central claim.

Authors: We agree that the Methods section provides only a high-level overview of the NLP-based sentiment construction. The revised manuscript will expand this description to specify the exact NLP technique and lexicon employed, report inter-annotator agreement where applicable, and include correlation results with a human-coded subsample. We will also add robustness checks using alternative lexica and variations in report-selection criteria to better support the validity of the indices underlying the transfer entropy and GARCH results. revision: yes

-

Referee: [GARCH model] GARCH section: sentiment enters the conditional-variance equation as a fitted regressor on the same volatility series used for estimation. Without explicit out-of-sample tests or parameter-free validation, the reported explanatory power of pessimistic sentiment risks being an in-sample artifact rather than evidence of a genuine driving effect.

Authors: The referee correctly identifies that the current GARCH specification relies on in-sample fitting. To address this concern, the revised manuscript will incorporate explicit out-of-sample tests, including rolling-window forecasts and parameter-free validation approaches, to evaluate whether the explanatory role of pessimistic sentiment holds beyond the estimation sample. revision: yes

-

Referee: [Transfer entropy analysis] Transfer-entropy and correlation results: the manuscript supplies no sample sizes, standard errors, or robustness checks (e.g., alternative lag choices, subsample stability, or controls for contemporaneous market tone). These omissions prevent assessment of whether the reported directional effect of pessimistic sentiment is statistically reliable.

Authors: We acknowledge the need for greater statistical transparency in the transfer entropy and correlation analyses. The revised version will report sample sizes and standard errors for the transfer entropy estimates. We will also add robustness checks covering alternative lag selections, subsample stability, and controls for contemporaneous market tone to allow readers to assess the reliability of the directional influence from pessimistic sentiment. revision: yes

Circularity Check

No circularity in derivation chain

full rationale

The paper constructs sentiment indices via NLP, computes correlations and transfer entropy on the resulting time series, and fits a GARCH model with sentiment as regressor. All steps are standard empirical computations on observed data; none reduce by construction to the inputs via self-definition, fitted parameters renamed as predictions, or self-citation chains. The transfer-entropy directionality and GARCH coefficient significance are direct statistical outputs rather than tautological restatements. No load-bearing uniqueness theorems or ansatzes imported from prior author work appear.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Ramnath, S

S. Ramnath, S. Rock, P. Shane, The financial analyst foreca sting literature: A taxonomy with suggestions for further research, International Jour nal of Forecasting 24, 34–75 (2008)

2008

-

[2]

K. L. Womack, Do brokerage analysts’ recommendations hav e investment value?, The Journal of Finance 51, 137–167 (1996)

1996

-

[3]

Givoly, J

D. Givoly, J. Lakonishok, The information content of finan cial analysts’ forecasts of earnings: Some evidence on semi-strong inefficiency, Journa l of Accounting and Eco- nomics 1, 165–185 (1979)

1979

-

[4]

T. Lys, S. Sohn, The association between revisions of finan cial analysts’ earnings fore- casts and security-price changes, Journal of Accounting an d Economics 13, 341–363 (1990)

1990

-

[5]

A. Brav, R. Lehavy, An empirical analysis of analysts’ tar get prices: Short-term infor- mativeness and long-term dynamics, The Journal of Finance 5 8, 1933–1967 (2003)

1933

-

[6]

Asquith, M

P. Asquith, M. B. Mikhail, A. S. Au, Information content of equity analyst reports, Journal of Financial Economics 75, 245–282 (2005)

2005

-

[7]

Givoly, C

D. Givoly, C. Hayn, R. Lehavy, The quality of analysts’ cas h flow forecasts, The Ac- counting Review 84, 1877–1911 (2009)

1911

-

[8]

A. C. Call, S. Chen, Y. H. Tong, Are analysts’ cash flow forec asts na ¨ ıve extensions of their own earnings forecasts?, Contemporary Accounting Re search 30, 438–465 (2013)

2013

-

[9]

Ertimur, J

Y. Ertimur, J. Livnat, M. Martikainen, Differential marke t reactions to revenue and expense surprises, Review of Accounting Studies 8, 185–211 (2003)

2003

-

[10]

A. H. Huang, A. Y. Zang, R. Zheng, Evidence on the informat ion content of text in analyst reports, The Accounting Review 89, 2151–2180 (2014 )

2014

-

[11]

Jiang, L

X.-F. Jiang, L. Xiong, T. Cen, L. Bai, N. Zhao, J. Zhang, C. -J. Zheng, T.-Y. Jiang, Analyst sentiment and earning forecast bias in financial mar kets, Physica A: Statistical Mechanics and its Applications 589, 126601 (2022)

2022

-

[12]

A. K. Davis, J. M. Piger, L. M. Sedor, Beyond the numbers: M easuring the information content of earnings press release language, Contemporary A ccounting Research 29, 845– 868 (2012)

2012

-

[13]

Feldman, S

R. Feldman, S. Govindaraj, J. Livnat, B. Segal, Manageme nt?s tone change, post earnings announcement drift and accruals, Review of Accoun ting Studies 15, 915–953 (2010)

2010

-

[14]

Loughran, B

T. Loughran, B. McDonald, When is a liability not a liabil ity? textual analysis, dic- tionaries, and 10-ks, The Journal of Finance 66, 35–65 (2011 )

2011

-

[15]

Twedt, L

B. Twedt, L. Rees, Reading between the lines: An empirica l examination of qualitative attributes of financial analysts’ reports, Journal of Accou nting and Public Policy 31, 1–21 (2012)

2012

-

[16]

B. J. Bushee, M. J. Jung, G. S. Miller, Conference present ations and the disclosure milieu, Journal of Accounting Research 49, 1163–1192 (2011 )

2011

-

[17]

Lemmon, E

M. Lemmon, E. Portniaguina, Consumer Confidence and Asse t Prices: Some Empirical Evidence, The Review of Financial Studies 19 , 1499–1529 (20 06)

-

[18]

L. Qiu, I. Welch, Investor sentiment measures, Tech. rep ., National Bureau of Eco- June 2, 2026 1:16 manuscript 12 XF Jiang et al. nomic Research (2004)

2026

-

[19]

K. L. Fisher, M. Statman, Investor sentiment and stock re turns, Financial Analysts Journal 56, 16–23 (2000)

2000

-

[20]

S. J. Brown, W. N. Goetzmann, T. Hiraki, N. Shirishi, M. Wa tanabe, Investor sen- timent in Japanese and US daily mutual fund flows, Tech. Rep., National Bureau of Economic Research (2003)

2003

-

[21]

Baker, J

M. Baker, J. C. Stein, Market liquidity as a sentiment ind icator, Journal of Financial Markets 7, 271–299 (2004)

2004

-

[22]

Baker, J

M. Baker, J. Wurgler, A catering theory of dividends, The Journal of Finance 59, 1125–1165 (2004)

2004

-

[23]

Baker, J

M. Baker, J. Wurgler, Appearing and disappearing divide nds: The link to catering incentives, Journal of Financial Economics 73, 271–288 (20 04)

-

[24]

R. Neal, S. M. Wheatley, Do measures of investor sentimen t predict returns?, Journal of Financial and Quantitative Analysis 33, 523–547 (1998)

1998

-

[25]

R. E. Whaley, The investor fear gauge, The Journal of Port folio Management 26, 12–17 (2000)

2000

-

[26]

Baker, J

M. Baker, J. Wurgler, Investor sentiment and the cross-s ection of stock returns, The Journal of Finance 61, 1645–1680 (2006)

2006

-

[27]

Black, Noise, The Journal of Finance 41, 528–543 (1986 )

F. Black, Noise, The Journal of Finance 41, 528–543 (1986 )

1986

-

[28]

Chung, J.-P

H. Chung, J.-P. Laforte, D. Reifschneider, J. C. William s, Have we underestimated the likelihood and severity of zero lower bound events?, Jou rnal of Money, Credit and Banking 44, 47–82 (2012)

2012

-

[29]

J. B. De Long, A. Shleifer, L. H. Summers, R. J. Waldmann, N oise trader risk in financial markets, Journal of Political Economy 98, 703–738 (1990)

1990

-

[30]

Mehra, R

R. Mehra, R. Sah, Mood fluctuations, projection bias, and volatility of equity prices, Journal of Economic Dynamics and Control 26, 869–887 (2002)

2002

-

[31]

W. Y. Lee, C. X. Jiang, D. C. Indro, Stock market volatilit y, excess returns, and the role of investor sentiment, Journal of Banking & Finance 26, 2277–2299 (2002)

2002

-

[32]

Mendel, A

B. Mendel, A. Shleifer, Chasing noise, Journal of Financ ial Economics 104, 303–320 (2012)

2012

-

[33]

T.-T. Chen, B. Zheng, Y. Li, X.-F. Jiang, New approaches i n agent-based modeling of complex financial systems, Front. Phys. 12, 128905 (2017)

2017

-

[34]

T.-T. Chen, B. Zheng, Y. Li, X.-F. Jiang, Information dri ving force and its application in agent-based modeling, Physica A 496, 593–601 (2018)

2018

-

[35]

Jiang, T.T

X.F. Jiang, T.T. Chen and B. Zheng, Time-reversal asymme try in financial systems, Physica A 392, 5369 (2013)

2013

-

[36]

Zhang, B

J. Zhang, B. Zheng, L.-F. Jin, Y. Li, X.-F. Jiang, Non-sta tionary temporal-spatio correlation analysis of information-driven complex financ ial dynamics, Chinese Journal of Physics 88, 756–767 (2024)

2024

-

[37]

L.-F. Jin, B. Zheng, J.-H. Ma, J. Zhang, and L. Xiong, X.-F . Jiang, J.-C. Li, Empirical study and model simulation of global stock market dynamics d uring COVID-19, Chaos, Solitons & Fractals 159, 112138 (2022)

2022

-

[38]

Y.-Y. Zhao, B. Qin, T. Liu, Sentiment analysis, Journal o f Software 21, 1834–1848 (2010)

2010

-

[39]

Kahneman, Maps of bounded rationality: Psychology fo r behavioral economics, American Economic Review 93, 1449–1475 (2003)

D. Kahneman, Maps of bounded rationality: Psychology fo r behavioral economics, American Economic Review 93, 1449–1475 (2003)

2003

-

[40]

T. Qiu, B. Zheng, F. Ren, and S. Trimper, Return-volatili ty correlation in financial dynamics, Phys. Rev. E 73, 065103 (2006)

2006

-

[41]

Jiang, B

X.-F. Jiang, B. Zheng, F. Ren, T. Qiu, Localized motion in random matrix decomposi- tion of complex financial systems, Physica A: Statistical Me chanics and its Applications June 2, 2026 1:16 manuscript Effects of analyst sentiment on volatility dynamics in financ ial market 13 471, 154–161 (2017)

2026

-

[42]

G. W. Brown, M. T. Cliff, Investor sentiment and the near-t erm stock market, Journal of Empirical Finance 11, 1–27 (2004)

2004

-

[43]

Bollerslev, Generalized autoregressive conditiona l heteroskedasticity, Journal of Econometrics 31, 307–327 (1986)

T. Bollerslev, Generalized autoregressive conditiona l heteroskedasticity, Journal of Econometrics 31, 307–327 (1986)

1986

-

[44]

R. F. Engle, T. Bollerslev, Modelling the persistence of conditional variances, Econo- metric Reviews 5, 1–50 (1986)

1986

-

[45]

P. C. O’BRIEN, M. F. McNichols, L. Hsiou-Wei, Analyst imp artiality and investment banking relationships, Journal of Accounting Research 43, 623–650 (2005)

2005

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.