(In)Efficient Market States and Rough Volatility Detected via Grunwald-Letnikov Fractional Derivative

Pith reviewed 2026-06-29 02:12 UTC · model grok-4.3

The pith

The Grünwald-Letnikov fractional derivative filter restores a usable Kolmogorov-Smirnov limit for testing self-similarity in long-range dependent processes from single trajectories.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

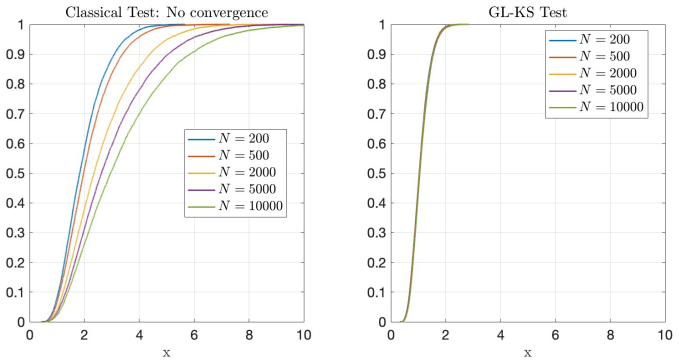

The discrete Grünwald-Letnikov fractional derivative removes the low-frequency long-memory singularity while preserving the finite-dimensional H-self-similarity, which permits derivation of the filtered empirical-process limit and consistent estimation of the Hurst exponent even when the classical Kolmogorov-Smirnov statistic undergoes a phase transition for H greater than one half.

What carries the argument

The discrete Grünwald-Letnikov fractional derivative used as a pre-filter on the observed time series.

If this is right

- Derivation of the filtered empirical process limit under the new framework.

- Proof of consistency and local asymptotic behavior for the resulting Hurst estimator.

- Detection of rough volatility in realized volatility series.

- Identification of persistent, anti-persistent, or efficient market states in equity index prices.

Where Pith is reading between the lines

- The filter might improve Hurst estimation in other fields exhibiting long memory, such as hydrology or network traffic.

- Real-time application could track changes in market efficiency over short windows.

- Extensions to multivariate series could reveal cross-asset dependencies in roughness.

Load-bearing premise

Applying the discrete Grünwald-Letnikov fractional derivative to a single observed trajectory isolates the self-similarity properties without introducing finite-sample distortions that would invalidate the Kolmogorov-Smirnov limit or the Hurst estimation.

What would settle it

A Monte Carlo experiment or real-data check in which the filtered statistic fails to recover the known Hurst value for series with H greater than one half would falsify the claim that the method restores reliable estimation.

Figures

read the original abstract

Testing self-similarity in fractional processes from a single observed trajectory is difficult under long-range dependence, because the associated Kolmogorov--Smirnov (KS) statistic undergoes a phase transition when $H>1/2$. In this regime, the classical limit collapses to a non-functional absolute Gaussian law and finite-sample convergence becomes severely distorted. This paper introduces a regime-adaptive KS/GL--KS framework based on the discrete Gr\"{u}nwald--Letnikov (GL) fractional derivative. The GL filter removes the low-frequency long-memory singularity while preserving the finite-dimensional $H$-self-similarity needed for distributional identification. We derive the filtered empirical-process limit, prove consistency and local asymptotic behavior of the resulting Hurst estimator, and validate the method through Monte Carlo simulations. Financial applications to realized volatility and equity index prices show how the procedure detects rough volatility and persistent, anti-persistent, or efficient market states.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a regime-adaptive KS/GL-KS framework that applies the discrete Grünwald-Letnikov fractional derivative to a single observed trajectory of a fractional process. The GL filter is claimed to remove the low-frequency long-memory singularity while preserving finite-dimensional H-self-similarity, enabling derivation of the filtered empirical-process limit, consistency and local asymptotic normality of the resulting Hurst estimator, Monte Carlo validation, and detection of rough volatility together with persistent/anti-persistent/efficient market states in realized volatility and equity index data.

Significance. If the filtered limit and consistency results hold, the procedure would supply a practical, single-trajectory method for Hurst estimation under long-range dependence that avoids the classical KS phase transition for H>1/2, with direct applicability to rough-volatility modeling and market-state classification in quantitative finance.

major comments (2)

- [Abstract / §3] Abstract and §3 (presumably the derivation section): the central claim that the discrete GL operator exactly removes the low-frequency singularity while leaving finite-dimensional H-self-similarity intact is load-bearing for the subsequent KS-limit derivation and consistency proof. The discrete GL formula is a truncated binomial-weighted difference; for H>1/2 the weights decay only polynomially, so any fixed truncation or discretization step produces a remainder whose effect on the covariance structure of the finite-dimensional distributions is not shown to be negligible. Without an explicit bound on this remainder that is uniform in the sample size, the claimed convergence of the filtered empirical process to the stated limit does not follow.

- [Abstract] Abstract: the Monte Carlo validation and financial applications rest on the same filtered series whose limiting behavior is asserted. If the truncation remainder alters the finite-dimensional distributions even mildly, both the reported consistency rates and the phase-transition analysis cease to apply to the actual estimator used in the simulations and data examples.

minor comments (1)

- [Abstract] Notation: the abstract alternates between “Grunwald-Letnikov” and “Grünwald--Letnikov”; standardize the spelling and supply the precise discrete formula (including truncation order) at first use.

Simulated Author's Rebuttal

We thank the referee for the careful reading and for identifying the need for greater explicitness in the justification of the filtered limit. We respond to each major comment below and will revise the manuscript to incorporate the requested clarifications.

read point-by-point responses

-

Referee: [Abstract / §3] Abstract and §3 (presumably the derivation section): the central claim that the discrete GL operator exactly removes the low-frequency singularity while leaving finite-dimensional H-self-similarity intact is load-bearing for the subsequent KS-limit derivation and consistency proof. The discrete GL formula is a truncated binomial-weighted difference; for H>1/2 the weights decay only polynomially, so any fixed truncation or discretization step produces a remainder whose effect on the covariance structure of the finite-dimensional distributions is not shown to be negligible. Without an explicit bound on this remainder that is uniform in the sample size, the claimed convergence of the filtered empirical process to the stated limit does not follow.

Authors: We agree that an explicit uniform bound on the truncation remainder is required to complete the argument. Section 3 derives the filtered limit by showing that the GL operator annihilates the long-memory component while the finite-dimensional distributions retain H-self-similarity; however, the manuscript would be strengthened by a dedicated lemma that quantifies the remainder uniformly in sample size. We will add this lemma in the revision, thereby confirming that the convergence of the filtered empirical process holds as stated. revision: yes

-

Referee: [Abstract] Abstract: the Monte Carlo validation and financial applications rest on the same filtered series whose limiting behavior is asserted. If the truncation remainder alters the finite-dimensional distributions even mildly, both the reported consistency rates and the phase-transition analysis cease to apply to the actual estimator used in the simulations and data examples.

Authors: The Monte Carlo experiments and empirical illustrations use precisely the discrete GL filter analyzed in the theoretical sections. Once the uniform remainder bound is supplied, the consistency, local asymptotic normality, and phase-transition results apply directly to the implemented procedure. In the revision we will cross-reference the new lemma from the abstract and §3 and, where appropriate, add finite-sample diagnostics confirming that the observed distributions align with the theoretical limits. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The abstract and provided text describe a mathematical derivation of the filtered empirical-process limit under the discrete Grünwald-Letnikov operator, followed by proofs of consistency and local asymptotics for the Hurst estimator. No quoted equations or claims reduce any prediction, limit, or estimator to a fitted parameter, self-citation chain, or definitional tautology. The GL filter is introduced as an external operator whose properties are analyzed rather than presupposed, and the KS phase-transition handling follows from standard empirical-process theory applied to the filtered path. This satisfies the default expectation of a non-circular paper whose central results rest on independent asymptotic arguments.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Angelini and S

D. Angelini and S. Bianchi. Kolmogorov–Smirnov estimation of self-similarity in long-range dependent fractional processes.Physica D: Nonlinear Phenomena, 476:134697, 2025

2025

-

[2]

M.A. Arcones. Limit theorems for nonlinear functionals of a stationary Gaussian sequence of vectors.Annals of Probability, 22(4):2242–2274, 1994

1994

-

[3]

S. Bianchi. A new distribution-based test of self-similarity.Fractals, 12(03):331–346, 2004

2004

-

[4]

Bianchi and A

S. Bianchi and A. Pianese. Time-varying Hurst–H¨ older exponents and the dynamics of (in)efficiency in stock markets.Chaos, Solitons & Fractals, 109:64–75, 2018

2018

-

[5]

Brandi and T

G. Brandi and T. Di Matteo. Multiscaling and rough volatility: An empirical investigation. International Review of Financial Analysis, 84:102324, 2022

2022

-

[6]

Breuer and P

P. Breuer and P. Major. Central limit theorems for non-linear functionals of Gaussian fields. Journal of Multivariate Analysis, 13(3):425–441, 1983

1983

-

[7]

Brockwell and R.A

P.J. Brockwell and R.A. Davis.Time series: Theory and methods. Springer science & business media, 2009

2009

-

[8]

Carbone, G

A. Carbone, G. Castelli, and H.E. Stanley. Time-dependent Hurst exponent in financial time series.Physica A: Statistical Mechanics and its Applications, 344(1-2):267–271, 2004. 31

2004

-

[9]

Cheridito, H

P. Cheridito, H. Kawaguchi, and M. Maejima. Fractional Ornstein-Uhlenbeck processes.Elec- tronic Journal of Probability [electronic only], 8, 2003

2003

-

[10]

Comte and E

F. Comte and E. Renault. Long memory in continuous-time stochastic volatility models.Math- ematical Finance, 8(4):291–323, 1998

1998

-

[11]

Dehling and M.S

H. Dehling and M.S. Taqqu. The empirical process of some long-range dependent sequences with an application to U-statistics.Annals of Statistics, 17(4):1767–1783, 1989

1989

-

[12]

Di Matteo

T. Di Matteo. Multi-scaling in finance.Quantitative finance, 7(1):21–36, 2007

2007

-

[13]

Dobrushin and P

R.L. Dobrushin and P. Major. Non-central limit theorems for non-linear functional of Gaussian fields.Zeitschrift f¨ ur Wahrscheinlichkeitstheorie und verwandte Gebiete, 50(1):27–52, 1979

1979

-

[14]

E.F. Fama. Efficient capital markets: a review of theory and empirical work.The Journal of Finance, 25(2):383–417, 1970

1970

-

[15]

Gatheral, T

J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough.Quantitative Finance, 18(6):933– 949, 2018

2018

-

[16]

Giraitis, H.L

L. Giraitis, H.L. Koul, and D. Surgailis.Large sample inference for long memory processes. World Scientific, 2012

2012

-

[17]

Kantelhardt, E

J.W. Kantelhardt, E. Koscielny-Bunde, H.H.A. Rego, S. Havlin, and A. Bunde. Detecting long- range correlations with detrended fluctuation analysis.Physica A: Statistical Mechanics and its Applications, 295:441–454, 2001

2001

-

[18]

Kolmogorov

A.N. Kolmogorov. Wienershe spiralen und einige andere interessante kurven im hilbertishen raum.DAS of the URSS (Nat. Sciences), 26:115–118, 1940

1940

-

[19]

Mandelbrot and J.W

B.B. Mandelbrot and J.W. Van Ness. Fractional Brownian motions, fractional noises and appli- cations.SIAM Review, 10(4):422–437, 1968

1968

-

[20]

Mantegna and H.E

R.N. Mantegna and H.E. Stanley.An Introduction to Econophysics. Correlations and Complexity in Finance. Cambridge University Press, 2004

2004

-

[21]

Ouannas, I.M

A. Ouannas, I.M. Batiha, and V.-T. Pham.Fractional Discrete Chaos. World Scientific, 2023

2023

-

[22]

Podlubny.Fractional Differential Equations, volume 198

I. Podlubny.Fractional Differential Equations, volume 198. Elsevier, 1998

1998

-

[23]

M.S. Taqqu. Weak convergence to fractional Brownian motion and to the Rosenblatt process. Advances in Applied Probability, 7(2):249–249, 1975

1975

-

[24]

Taqqu, V

M.S. Taqqu, V. Teverovsky, and W. Willinger. Estimators for long-range dependence: An em- pirical study.Fractals, 3(4):785–798, 1995

1995

-

[25]

Teverovsky and M

V. Teverovsky and M. Taqqu. Testing for long-range dependence in the presence of shifting means or a slowly declining trend, using a variance-type estimator.Journal of Time Series Analysis, 18(3):279–304, 1997

1997

-

[26]

X. Wang, W. Xiao, and J. Yu. Modeling and forecasting realized volatility with the fractional Ornstein–Uhlenbeck process.Journal of Econometrics, 232(2):389–415, 2023

2023

-

[27]

R. Weron. Estimating long-range dependence: Finite sample properties and confidence intervals. Physica A: Statistical Mechanics and its Applications, 312(1–2):285–299, 2002. 32

2002

-

[28]

Wood and G

A.T.A. Wood and G. Chan. Simulation of stationary Gaussian processes in [0,1] d.Journal of Computational and Graphical Statistics, 3(4):409–432, 1994. A Proof of the short-memory benchmark We prove Proposition 2.2 in the balanced regimen,m→∞,n m→1.Let ξi(x) :=1{Xi≤x}−Φ(x), ηj(x) :=1{Yj≤x}−Φ(x), so that Fn(x)−Gm(x) = 1 n n∑ i=1 ξi(x)−1 m m∑ j=1 ηj(x). Defi...

1994

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.