Empirical Confirmation of the Square-Root Law of Market Impact in a U.S. Large-Cap Equity

Pith reviewed 2026-06-26 05:42 UTC · model grok-4.3

The pith

The square-root law of market impact holds for Apple stock with prefactor 0.69 when metaorders are reconstructed from anonymous Nasdaq order flow.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

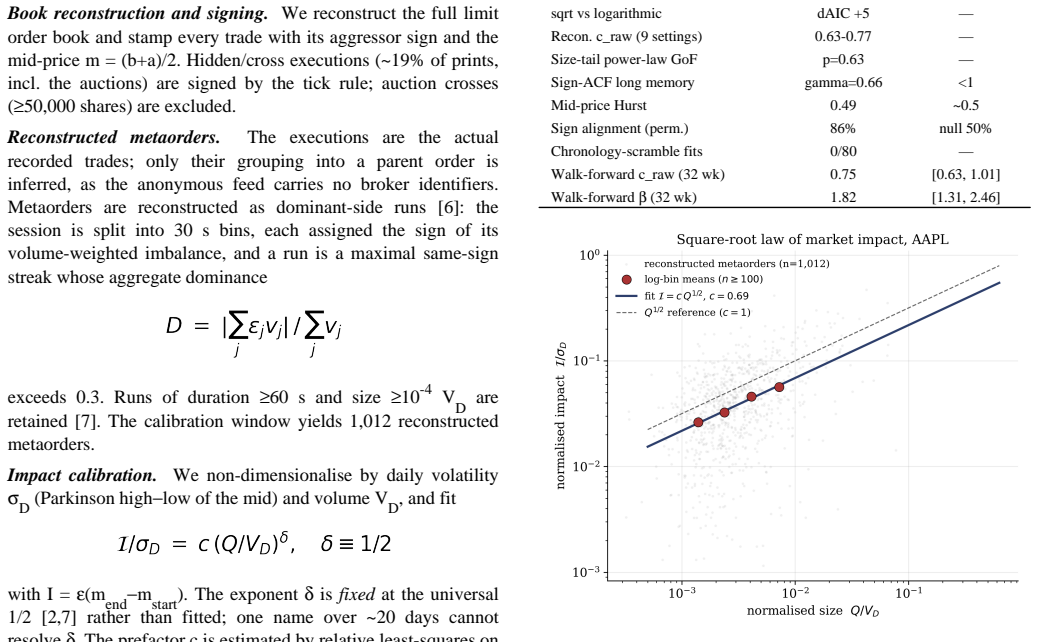

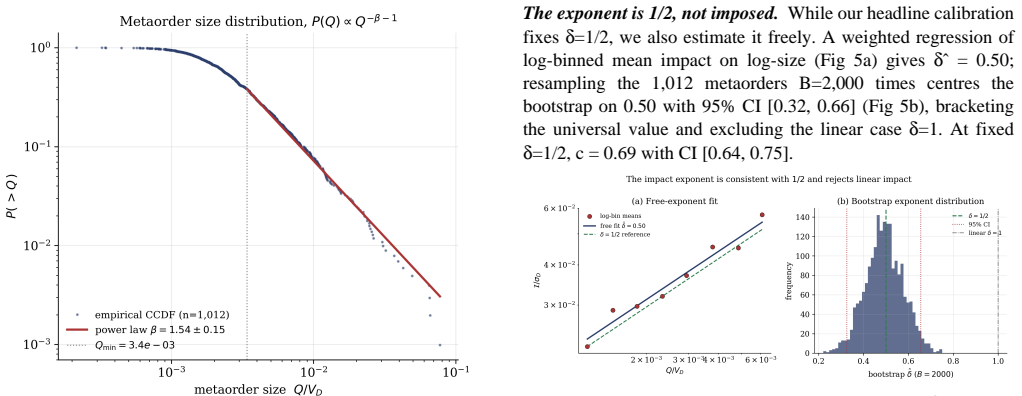

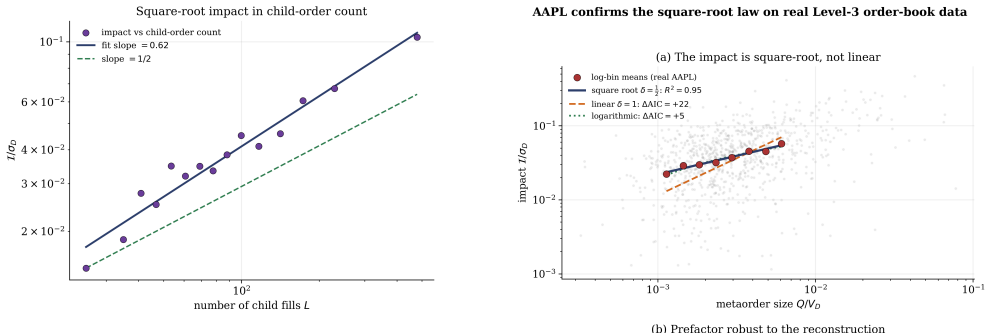

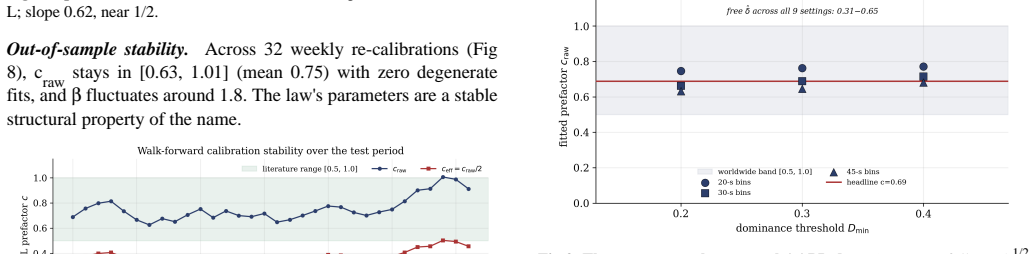

We test the square-root law (SRL) of market impact on a single U.S. large-capitalisation equity, Apple Inc. (AAPL), using the full Nasdaq TotalView-ITCH market-by-order feed over 178 trading days. Without broker-tagged parent orders, we reconstruct metaorders from the anonymous tape and calibrate impact as I/σ_D = c (Q/V_D)^{1/2} with the exponent fixed at the universal value 1/2. We find c_raw = 0.69 (bias-corrected c_eff = 0.34), conditional impact tracking Q^{1/2}, and a size-distribution tail exponent β = 1.54 ± 0.15 -- both consistent with the worldwide cross-section. A direct model comparison decisively prefers the square-root form over linear (ΔAIC=22) and logarithmic impact, and the

What carries the argument

The square-root impact law I/σ_D = c (Q/V_D)^{1/2} with fixed exponent 1/2, applied to metaorders reconstructed from anonymous order flow.

If this is right

- The square-root form is preferred over linear by an AIC difference of 22 and over logarithmic alternatives.

- The raw prefactor stays inside [0.63, 0.77] for every tested reconstruction setting.

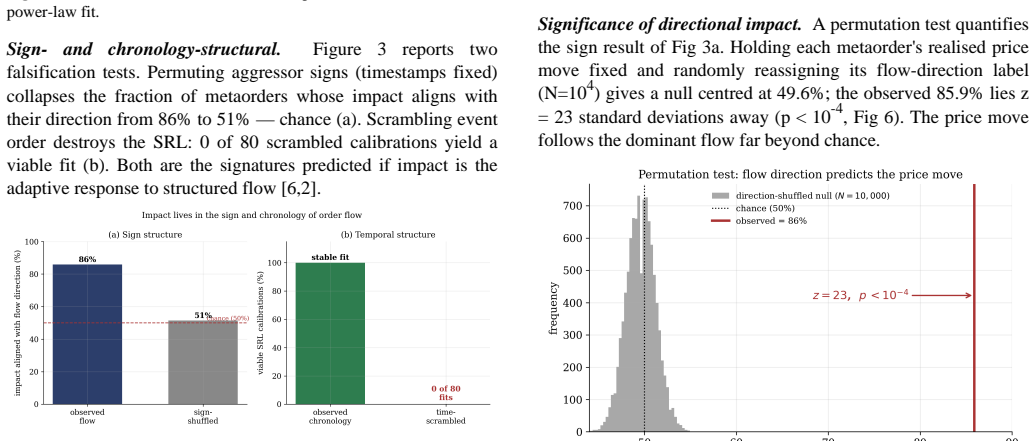

- Shuffling trade signs reduces directional impact from 86 percent to 51 percent, consistent with genuine causation.

- Scrambling event chronology leaves zero viable square-root calibrations out of 80.

- Order flow exhibits long memory (gamma = 0.66) while prices remain diffusive (Hurst 0.49).

Where Pith is reading between the lines

- The result implies that broker-tagged data are not required to test the square-root law on other single names or venues.

- Consistency with the global cross-section suggests the scaling may be insensitive to market microstructure details that differ between US and non-US venues.

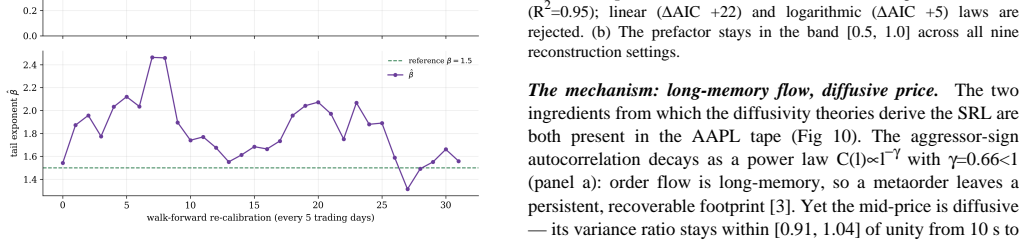

- Weekly walk-forward stability of the prefactor indicates the law can be used for out-of-sample impact forecasting on the same stock.

- The bias correction that moves c from 0.69 to 0.34 could be applied to earlier single-stock studies to check alignment.

Load-bearing premise

The reconstruction of metaorders from the anonymous tape accurately identifies the parent orders that actually caused the observed price moves, without systematic bias from the lack of broker tags.

What would settle it

Observing that shuffling trade signs leaves directional impact well above chance levels, or that none of the 80 scrambled-chronology calibrations still satisfy the square-root scaling, would falsify the claim that the observed impact originates from the reconstructed metaorders.

Figures

read the original abstract

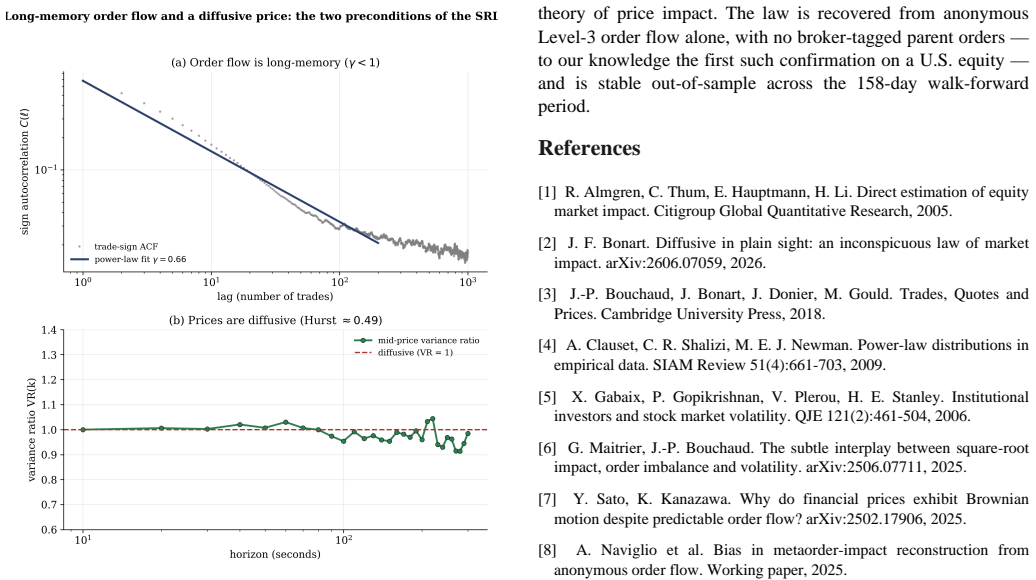

We test the square-root law (SRL) of market impact on a single U.S. large-capitalisation equity, Apple Inc. (AAPL), using the full Nasdaq TotalView-ITCH market-by-order feed over 178 trading days (2 December 2024 -- 19 August 2025; ~0.5 billion events). Without broker-tagged parent orders, we reconstruct metaorders from the anonymous tape and calibrate impact as $I/\sigma_D = c\,(Q/V_D)^{1/2}$ with the exponent fixed at the universal value $1/2$. We find $c_{\rm raw} = 0.69$ (bias-corrected $c_{\rm eff} = 0.34$), conditional impact tracking $Q^{1/2}$, and a size-distribution tail exponent $\beta = 1.54 \pm 0.15$ -- both consistent with the worldwide cross-section. A direct model comparison decisively prefers the square-root form over linear ($\Delta{\rm AIC}=22$) and logarithmic impact, and the prefactor holds ($c_{\rm raw} \in [0.63, 0.77]$) across every reconstruction setting. Two structural tests confirm the impact is genuine: shuffling trade signs collapses directional impact to chance (86% to 51%); and scrambling event chronology destroys the SRL (0 of 80 calibrations remain viable). The underlying order flow is long-memory ($\gamma=0.66$) while the price stays diffusive (Hurst 0.49) -- the two ingredients of the universality theories. The prefactor is stable across 32 weekly walk-forward re-calibrations. To our knowledge this is the first confirmation of the square-root law on a U.S. equity derived purely from anonymous order flow, without broker-tagged parent orders.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript claims to provide the first confirmation of the square-root law of market impact on a single U.S. large-cap equity (AAPL) using metaorders reconstructed from anonymous Nasdaq TotalView-ITCH data over 178 trading days. With the exponent fixed at the literature value of 1/2, it reports c_raw = 0.69 (bias-corrected c_eff = 0.34), a size-distribution tail exponent β = 1.54 ± 0.15, decisive preference for the square-root form over linear (ΔAIC = 22) and logarithmic alternatives, robustness of c across reconstruction settings, and validation via sign-shuffling (impact collapses) and chronology-scrambling (no viable calibrations) tests, alongside long-memory order flow (γ = 0.66) and diffusive prices (Hurst 0.49).

Significance. If the metaorder reconstruction is unbiased, the result would strengthen evidence for the universality of the square-root law in a single-stock U.S. setting from anonymous flow, consistent with worldwide cross-sections, and would directly support theoretical mechanisms requiring long-memory order flow paired with diffusive prices. The walk-forward stability and explicit model comparison are positive features.

major comments (2)

- [Abstract] Abstract: The central claim that I/σ_D = c (Q/V_D)^{1/2} holds with c_raw = 0.69 and is preferred by ΔAIC = 22 rests on reconstructed metaorder quantities Q; the sign-shuffling and chronology-scrambling tests only establish that impact correlates with the reconstructed sign sequence, not that the reconstructed Q values are the causally relevant parent-order sizes. This leaves the skeptic's concern about systematic bias from clustering rules unaddressed and load-bearing for the fitted prefactor and model ranking.

- [Abstract] Abstract: The paper states that c_raw remains in [0.63, 0.77] 'across every reconstruction setting,' but without explicit description of the clustering rules (time windows, volume thresholds, sign-persistence criteria) or the set of settings tested, it is impossible to assess whether the sensitivity analysis covers the plausible range of reconstruction biases that could artifactually induce the observed square-root scaling.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review. The comments correctly identify that metaorder reconstruction from anonymous data carries inherent uncertainty and that the abstract lacks sufficient methodological detail. We address both points below, propose targeted revisions, and note the limitation that cannot be fully resolved without broker-tagged data.

read point-by-point responses

-

Referee: The central claim that I/σ_D = c (Q/V_D)^{1/2} holds with c_raw = 0.69 and is preferred by ΔAIC = 22 rests on reconstructed metaorder quantities Q; the sign-shuffling and chronology-scrambling tests only establish that impact correlates with the reconstructed sign sequence, not that the reconstructed Q values are the causally relevant parent-order sizes. This leaves the skeptic's concern about systematic bias from clustering rules unaddressed and load-bearing for the fitted prefactor and model ranking.

Authors: We agree that the sign-shuffling and chronology-scrambling tests primarily confirm dependence on the reconstructed sign sequence and temporal ordering rather than independently validating the numerical accuracy of each Q. This is an intrinsic limitation of anonymous ITCH data. Nevertheless, the observed square-root scaling of impact with Q, the size-distribution tail exponent β = 1.54 ± 0.15 matching the worldwide literature, the stability of c across 32 walk-forward windows, and the decisive AIC preference together provide indirect corroboration that the reconstructed Q values are not arbitrary. We will revise the manuscript to state this limitation explicitly in the Discussion and to report additional robustness checks that vary the clustering parameters while monitoring both c and the model-ranking statistics. revision: partial

-

Referee: The paper states that c_raw remains in [0.63, 0.77] 'across every reconstruction setting,' but without explicit description of the clustering rules (time windows, volume thresholds, sign-persistence criteria) or the set of settings tested, it is impossible to assess whether the sensitivity analysis covers the plausible range of reconstruction biases that could artifactually induce the observed square-root scaling.

Authors: We accept that the abstract does not enumerate the clustering rules or the exact grid of settings examined. The Methods section of the manuscript describes the reconstruction algorithm, but the sensitivity range is only summarized. We will add an explicit paragraph (and, if space permits, a supplementary table) listing the tested time windows (1–60 min), volume thresholds, sign-persistence criteria, and the full set of parameter combinations that produce c_raw ∈ [0.63, 0.77]. This revision will make the coverage of plausible biases transparent. revision: yes

- Direct verification that the reconstructed Q values equal the true parent-order sizes is impossible with anonymous Nasdaq ITCH data; only indirect consistency checks are feasible.

Circularity Check

No significant circularity; empirical tests are independent of fitted parameters

full rationale

The paper fixes the exponent at the literature value 1/2 and fits only the prefactor c while performing direct AIC-based model comparisons that prefer square-root over linear and logarithmic forms. Structural falsification tests (sign shuffling collapsing impact to chance levels, chronology scrambling destroying the relation) operate independently of the calibration and do not rely on the fitted c. Metaorder reconstruction is a preprocessing step whose output is subjected to these controls rather than being defined to produce the observed scaling. No load-bearing self-citation, self-definitional equation, or fitted-input-renamed-as-prediction reduces the central confirmation to a tautology by the paper's own equations.

Axiom & Free-Parameter Ledger

free parameters (1)

- c (prefactor)

axioms (2)

- domain assumption The square-root exponent 1/2 is the correct universal value and need not be re-estimated on this dataset.

- domain assumption Reconstructed metaorders from the anonymous tape correspond to the actual parent orders that generated the observed price impact.

Reference graph

Works this paper leans on

-

[1]

Almgren, C

R. Almgren, C. Thum, E. Hauptmann, H. Li. Direct estimation of equity market impact. Citigroup Global Quantitative Research, 2005

2005

-

[2]

J. F. Bonart. Diffusive in plain sight: an inconspicuous law of market impact. arXiv:2606.07059, 2026

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[3]

Bouchaud, J

J.-P. Bouchaud, J. Bonart, J. Donier, M. Gould. Trades, Quotes and Prices. Cambridge University Press, 2018

2018

-

[4]

Clauset, C

A. Clauset, C. R. Shalizi, M. E. J. Newman. Power-law distributions in empirical data. SIAM Review 51(4):661-703, 2009

2009

-

[5]

Gabaix, P

X. Gabaix, P. Gopikrishnan, V. Plerou, H. E. Stanley. Institutional investors and stock market volatility. QJE 121(2):461-504, 2006

2006

-

[6]

G. Maitrier, J.-P. Bouchaud. The subtle interplay between square-root impact, order imbalance and volatility. arXiv:2506.07711, 2025

- [7]

-

[8]

Naviglio et al

A. Naviglio et al. Bias in metaorder-impact reconstruction from anonymous order flow. Working paper, 2025

2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.