Sticky CIR process with potential: invariant measure and exact sampling

Pith reviewed 2026-05-20 20:45 UTC · model grok-4.3

The pith

For δ in (1,2) the sticky CIR process is well-posed with a unique invariant measure that mixes a point mass at zero with a weighted gamma density and admits exact sampling from its resolvent Green's function.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The sticky CIR process with sticky boundary condition at zero is well-posed for δ ∈ (1,2). Its unique invariant measure is a mixture of a Dirac point mass at the origin and a weighted gamma-type density on (0,∞). The explicit Green's function of the resolvent, expressed in confluent hypergeometric functions, allows construction of an exact sampler for this invariant measure when the potential is zero. For a non-zero potential G satisfying suitable regularity, a Girsanov change of measure establishes existence and uniqueness of the tilted invariant measure, and supports two sampling methods: a Metropolis-Hastings algorithm that targets the measure exactly and an unadjusted Langevin algorithm.

What carries the argument

The explicit Green's function for the resolvent of the infinitesimal generator, expressed via confluent hypergeometric functions, which encodes the transition structure and directly yields the exact sampling procedure for the invariant measure.

If this is right

- The sticky CIR process admits a unique invariant measure that is a mixture of a point mass at zero and a gamma-type density for every δ in (1,2).

- An exact sampler for the invariant measure can be built directly from the closed-form Green's function without time discretization.

- Existence and uniqueness of the tilted invariant measure hold for non-zero potentials via the Girsanov transformation.

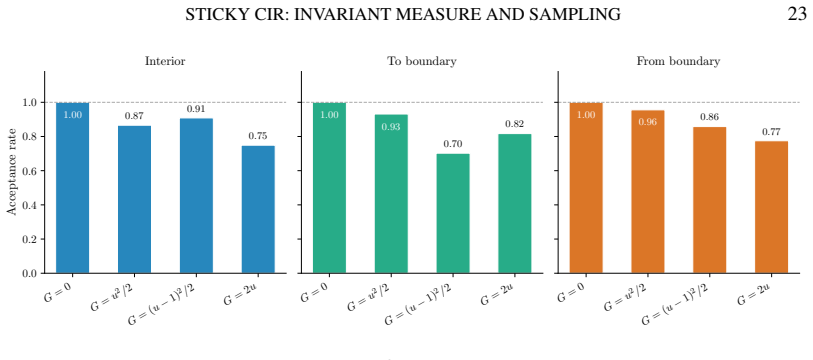

- The Metropolis-Hastings sampler targets the invariant measure exactly at every step size while the unadjusted Langevin algorithm carries an O(h) bias.

Where Pith is reading between the lines

- The exact sampling procedure may be directly useful inside the sparse Bayesian inference setting that originally motivated the sticky CIR process as a marginal.

- The hypergeometric representation of the Green's function could permit closed-form expressions for moments or tail probabilities of the invariant measure.

- The same resolvent analysis might extend to other one-dimensional diffusions that combine sticky boundaries with drift and diffusion coefficients of similar functional form.

Load-bearing premise

The Girsanov change of measure used to obtain the tilted invariant measure remains valid under the regularity conditions imposed on the non-zero potential G.

What would settle it

Generate long trajectories of the sticky CIR process for a concrete δ in (1,2) and test whether the empirical occupation measure converges to the predicted mixture consisting of a point mass at zero plus the explicit weighted gamma density on the positive reals.

Figures

read the original abstract

We study the sticky Cox-Ingersoll-Ross (CIR) process in one dimension, a diffusion on $[0,\infty)$ with a sticky boundary condition at the origin, arising as the marginal process in a sparse Bayesian inference framework based on Hadamard-Langevin dynamics. For the parameter range $\delta\in(1,2)$, in which the origin is accessible but not absorbing, we prove well-posedness of the process and uniqueness of its invariant measure, which is a mixture of a point mass at zero and a weighted gamma-type density on the interior. We derive an explicit Green's function for the resolvent in terms of confluent hypergeometric functions, and use this to construct an exact sampler for the invariant measure in the zero-potential case. For a non-trivial potential $G$, we establish existence and uniqueness of the tilted invariant measure via a Girsanov change of measure, and develop two sampling algorithms: a Metropolis-Hastings corrected sampler that targets the invariant measure exactly, and an unadjusted Langevin algorithm (ULA) that is cheaper per step but introduces an $O(h)$ bias. Numerical experiments confirm the predicted behaviour: the Metropolis-Hastings sampler achieves the target invariant measure at all step sizes, while the ULA exhibits the expected $O(h)$ bias.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies the sticky CIR process on [0, ∞) with sticky boundary at the origin for δ ∈ (1,2). It proves well-posedness and uniqueness of the invariant measure (a mixture of a point mass at zero and a weighted gamma-type density), derives an explicit Green's function for the resolvent in confluent hypergeometric functions to construct an exact sampler in the zero-potential case, and for non-zero potential G uses a Girsanov change of measure to establish the tilted invariant measure together with an exact Metropolis-Hastings sampler and a biased ULA with O(h) bias, supported by numerical experiments confirming the predicted behavior.

Significance. If the results hold, this work supplies rigorous foundations and explicit constructions for sampling the invariant measure of sticky diffusions arising in sparse Bayesian inference via Hadamard-Langevin dynamics. Strengths include the explicit Green's function derivation, the use of classical stochastic calculus and Girsanov without ad-hoc fitting, and numerical experiments that reproduce the theoretical O(h) bias for ULA and exactness for MH.

major comments (1)

- Section on existence and uniqueness via Girsanov: the claim that the Girsanov change of measure yields the tilted invariant measure for non-zero G rests on regularity conditions on G, but does not explicitly verify that the local-time coefficient in the semimartingale decomposition (or the domain of the generator) remains unaffected, so that the resulting process stays within the class of sticky diffusions. Standard Girsanov theorems for Itô processes do not automatically guarantee preservation of the sticky boundary; this step is load-bearing for uniqueness of the tilted measure.

minor comments (2)

- The abstract and introduction could more explicitly contrast the zero-potential exact sampler with the two algorithms for non-zero G to improve readability.

- Numerical experiments section: the plots confirming O(h) bias would benefit from tabulated error values across a wider range of h to make the rate visually clearer.

Simulated Author's Rebuttal

We thank the referee for their careful reading of the manuscript and for identifying this important technical point concerning the Girsanov argument. We address the comment in detail below and will incorporate a clarification in the revised version.

read point-by-point responses

-

Referee: Section on existence and uniqueness via Girsanov: the claim that the Girsanov change of measure yields the tilted invariant measure for non-zero G rests on regularity conditions on G, but does not explicitly verify that the local-time coefficient in the semimartingale decomposition (or the domain of the generator) remains unaffected, so that the resulting process stays within the class of sticky diffusions. Standard Girsanov theorems for Itô processes do not automatically guarantee preservation of the sticky boundary; this step is load-bearing for uniqueness of the tilted measure.

Authors: We agree that the preservation of the sticky boundary under Girsanov requires explicit verification and is not automatic from standard Itô-process results. In the manuscript the change of measure is constructed from the potential G via the usual exponential martingale, which modifies only the drift on (0,∞) while leaving the diffusion coefficient and the sticky parameter unchanged. Because the local-time term in the semimartingale decomposition of the sticky CIR process is a continuous additive functional whose coefficient depends solely on the diffusion coefficient and the stickiness parameter (both invariant under the absolutely continuous change of measure), the boundary behavior is preserved. Under the regularity assumed on G the Girsanov density is a true martingale, so the measures are equivalent on the path space and null sets (including paths that spend positive Lebesgue time at zero) are preserved. Nevertheless, we acknowledge that this reasoning is only sketched and should be stated more explicitly. In the revised manuscript we will insert a short paragraph immediately after the statement of the Girsanov theorem, recalling the semimartingale decomposition of the sticky process and noting that the local-time coefficient is unaffected by drift changes; we will also cite the relevant result on preservation of additive functionals under equivalent measures. This addition will make the argument for uniqueness of the tilted invariant measure fully rigorous. revision: yes

Circularity Check

No circularity: derivations rest on classical generator analysis and Girsanov theorem

full rationale

The paper derives well-posedness, uniqueness of the invariant measure, and the explicit Green's function directly from the infinitesimal generator with sticky boundary conditions at zero, then applies the Girsanov theorem under stated regularity assumptions on the potential G to obtain the tilted measure. These steps invoke standard results from stochastic calculus and do not reduce to self-definition, fitted parameters renamed as predictions, or load-bearing self-citations; the central claims remain independent of the target quantities and are externally verifiable via the resolvent equation and change-of-measure martingale properties.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Existence and uniqueness of solutions to the sticky SDE for δ∈(1,2)

- domain assumption Validity of Girsanov change of measure under the regularity assumed on G

Reference graph

Works this paper leans on

-

[1]

BORODIN, A. N. and SALMINEN, P. (2002).Handbook of Brownian Motion: Facts and Formulae, 2nd ed. Probability and Its Applications. Birkhäuser, Basel. https://doi.org/10.1007/978-3-0348-8163-0

-

[2]

Hadamard Langevin dynamics for sampling the l1-prior

CHELTSOV, I., CORNALBA, F., POON, C. and SHARDLOW, T. (2026). Hadamard–Langevin dynamics for sampling the l1-prior.Bernoulli. To appear. https://doi.org/10.48550/arXiv.2411.11403

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.2411.11403 2026

-

[3]

COX, J. C., INGERSOLL, J. E. and ROSS, S. A. (1985). A Theory of the Term Structure of Interest Rates. Econometrica53385–407. https://doi.org/10.2307/1911242

-

[4]

GEORGE, E. I. and MCCULLOCH, R. E. (1993). Variable Selection via Gibbs Sampling.Journal of the American Statistical Association88881–889. https://doi.org/10.1080/01621459.1993.10476353 GÖING-JAESCHKE, A. and YOR, M. (2003). A Survey and Some Generalizations of Bessel Processes.Bernoulli 9313–349. https://doi.org/10.3150/bj/1068128980

-

[5]

HAIRER, M. and MATTINGLY, J. C. (2011). Yet another look at Harris’ ergodic theorem for Markov chains. InSeminar on Stochastic Analysis, Random Fields and Applications VI.Progress in Probability63109–117. Birkhäuser/Springer Basel AG, Basel. https://doi.org/10.1007/978-3-0348-0021-1_7 ITÔ, K. and MCKEAN, H. P. (1965).Diffusion Processes and Their Sample P...

-

[6]

KARLIN, S. and TAYLOR, H. M. (1981).A Second Course in Stochastic Processes, 1st ed. Academic Press, New York

work page 1981

-

[7]

seaborn: statistical data visualization

KUMAR, R., CARROLL, C., HARTIKAINEN, A. and MARTIN, O. (2019). ArviZ a unified library for exploratory analysis of Bayesian models in Python.Journal of Open Source Software41143. https://doi.org/10.21105/joss. 01143

-

[8]

MEYN, S. P. and TWEEDIE, R. L. (1993).Markov Chains and Stochastic Stability.Communications and Control Engineering. Springer. https://doi.org/10.1007/978-1-4471-3267-7

-

[9]

MITCHELL, T. J. and BEAUCHAMP, J. J. (1988). Bayesian Variable Selection in Linear Regression.Journal of the American Statistical Association831023–1032. https://doi.org/10.1080/01621459.1988.10478694

-

[10]

OLVER, F. W. J., LOZIER, D. W., BOISVERT, R. F. and CLARK, C. W., eds. (2010).NIST Handbook of Mathematical Functions. Cambridge University Press, New York. Also available as the NIST Digital Library of Mathematical Functions at https://dlmf.nist.gov

work page 2010

-

[11]

PESKIR, G. (2022). Sticky Bessel Diffusions.Stochastic Processes and Their Applications1501015–1036. https://doi.org/10.1016/j.spa.2022.05.003

-

[12]

REVUZ, D. and YOR, M. (1999).Continuous Martingales and Brownian Motion, 3rd ed.Grundlehren der mathematischen Wissenschaften293. Springer. https://doi.org/10.1007/978-3-662-06400-9

-

[13]

ROGERS, L. C. G. and WILLIAMS, D. (2000).Diffusions, Markov Processes, and Martingales2, 2nd ed. Cambridge University Press. https://doi.org/10.1017/CBO9781107590120

-

[14]

VOLKONSKII, V. A. (1958). Random substitution of time in strong Markov processes.Theory of Probability and Its Applications3310–326. https://doi.org/10.1137/1103025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.