Robust Hedging Valuation Adjustment under Liquidity--Demand Stress

Pith reviewed 2026-06-29 05:17 UTC · model grok-4.3

The pith

Robust HVA is the worst-case expected loss over relative-entropy neighborhoods of simulated loss distributions for each no-trade-band rule.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

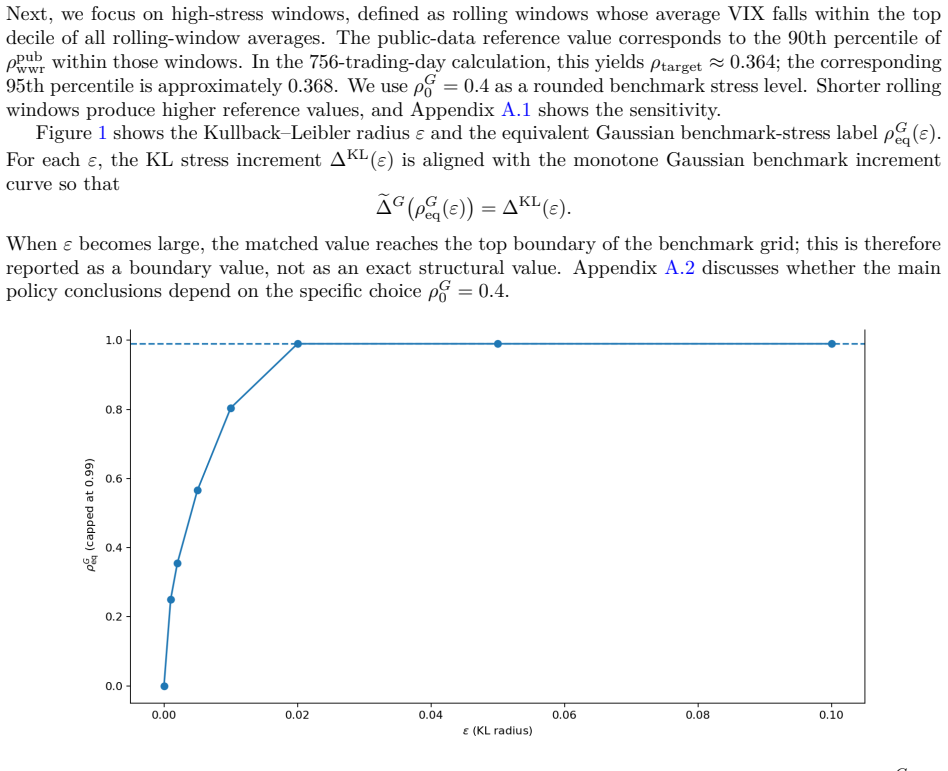

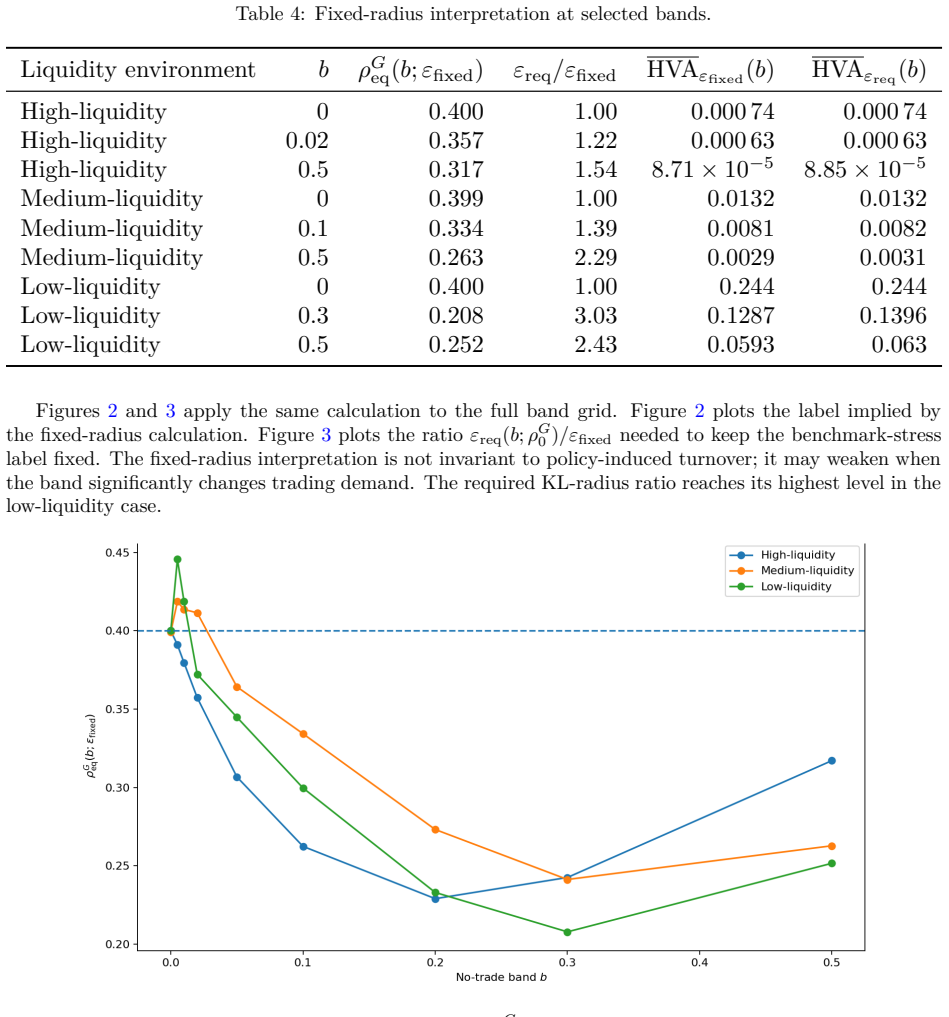

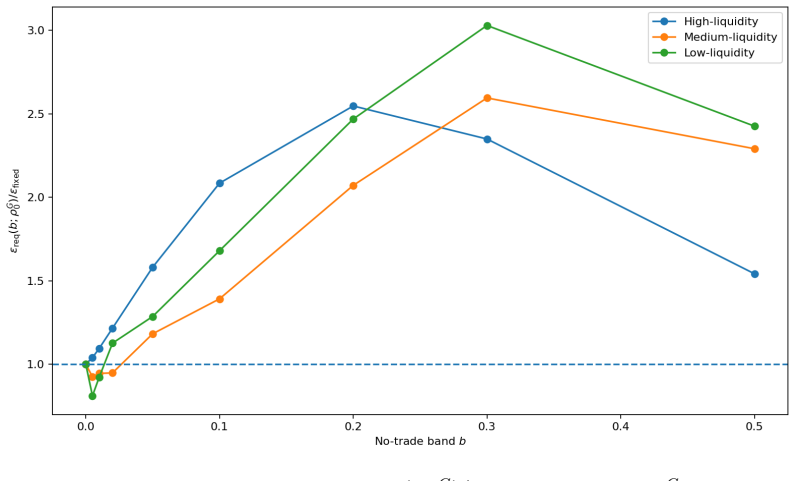

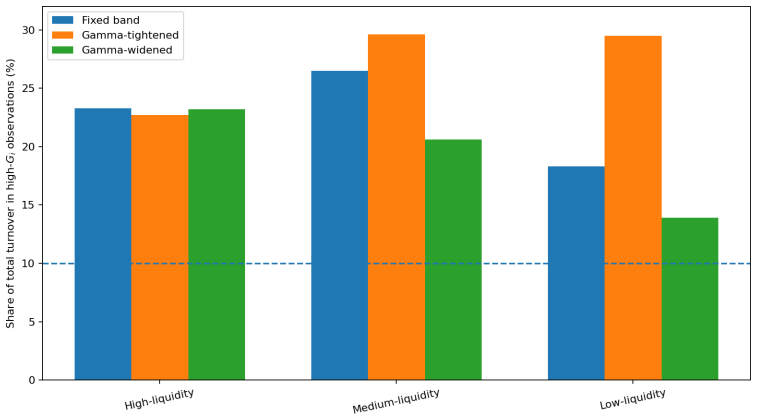

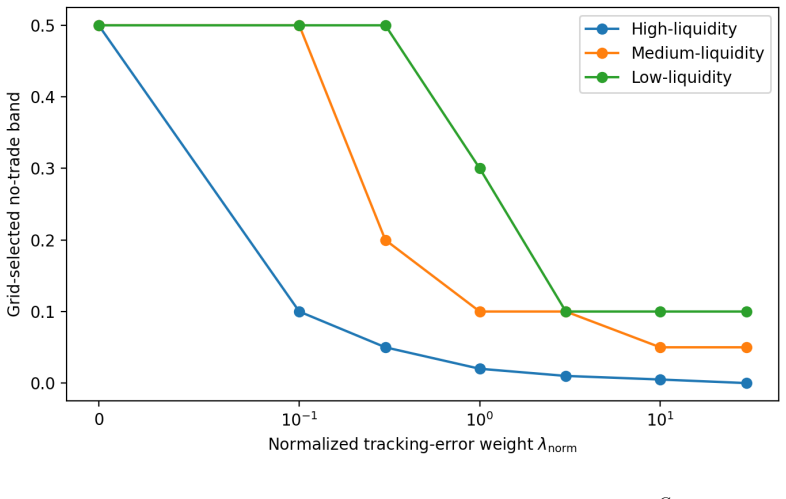

Simulated rebalancing and maturity-unwind trades generate a loss distribution for each no-trade-band rule, and robust HVA is defined as the worst-case expected loss over a relative-entropy neighborhood of that distribution. Because band width affects turnover, the same relative-entropy radius applied to different bands can imply different levels of demand-liquidity stress. Wider no-trade bands lower rebalancing costs but raise hedge-error risk.

What carries the argument

The relative-entropy neighborhood of the simulated loss distribution for a chosen no-trade-band rule, which supplies the set of stressed scenarios whose worst-case expected loss defines robust HVA.

If this is right

- Wider no-trade bands reduce rebalancing costs at the expense of higher hedge-error risk under the robust measure.

- A fixed benchmark-stress convention normalizes the entropy radius differently for each band width than a fixed-radius convention.

- The robust HVA value for any given band rule is determined once the loss distribution and the chosen convention are fixed.

- The same relative-entropy radius maps to stronger or weaker liquidity stress depending on the turnover induced by the band.

Where Pith is reading between the lines

- Traders could choose band width by minimizing robust HVA under a fixed convention for a target liquidity-stress level.

- The framework could be applied to other dynamic-hedging parameters such as rebalancing triggers or unwind thresholds.

- Calibration of the entropy radius might be performed by matching the neighborhood to observed liquidity-demand statistics from past stress periods.

Load-bearing premise

The simulated loss distributions from the chosen rebalancing and unwind rules are representative of true losses under liquidity-demand stress, and the relative-entropy neighborhood correctly captures the relevant stress scenarios.

What would settle it

Compare realized hedging losses observed during an actual episode of elevated liquidity demand against the worst-case bound given by the robust HVA for the matching band rule and radius.

Figures

read the original abstract

This paper develops a robust hedging valuation adjustment (HVA) measure for dynamic hedging. Simulated rebalancing and maturity-unwind trades generate a loss distribution for each no-trade-band rule, and we define robust HVA as the worst-case expected loss over a relative-entropy neighborhood of that distribution. Because band width affects turnover, the same relative-entropy radius applied to different bands can imply different levels of demand-liquidity stress. We distinguish a fixed-radius convention from a fixed benchmark-stress convention and show that wider no-trade bands lower rebalancing costs but raise hedge-error risk.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a robust hedging valuation adjustment (HVA) for dynamic hedging under liquidity-demand stress. Simulated rebalancing and maturity-unwind trades generate a loss distribution for each no-trade-band rule; robust HVA is then defined as the worst-case expected loss over a relative-entropy neighborhood of that distribution. The authors distinguish a fixed-radius convention from a fixed-benchmark-stress convention and conclude that wider no-trade bands lower rebalancing costs but raise hedge-error risk.

Significance. If the relative-entropy construction is shown to capture liquidity-driven stress, the framework supplies a quantitative tool for evaluating the cost-risk trade-off across hedging rules under distributional ambiguity. The explicit comparison of the two conventions for the ambiguity set is a clear contribution that could guide practical implementation in risk-management settings.

major comments (1)

- [Abstract, paragraph 2] Abstract, paragraph 2 (definition of robust HVA): the construction takes a base loss distribution P generated by a chosen rebalancing/unwind rule and defines robust HVA as the worst-case expectation under Q with D(Q||P) ≤ radius. Liquidity-demand stress acts on primitives (market-impact coefficients, bid-ask spreads, unwind liquidity) that alter the loss law in a directed, low-dimensional manner. An unstructured relative-entropy ball admits arbitrary deviations unrelated to these primitives, and the manuscript provides neither a derivation linking the radius to plausible changes in those primitives nor numerical checks that the worst-case value remains stable or interpretable under such directed perturbations. This modeling choice is load-bearing for the claimed trade-off between band width and robust HVA.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The single major comment concerns the modeling choice of an unstructured relative-entropy ball around the simulated loss distribution. We address this point directly below.

read point-by-point responses

-

Referee: [Abstract, paragraph 2] Abstract, paragraph 2 (definition of robust HVA): the construction takes a base loss distribution P generated by a chosen rebalancing/unwind rule and defines robust HVA as the worst-case expectation under Q with D(Q||P) ≤ radius. Liquidity-demand stress acts on primitives (market-impact coefficients, bid-ask spreads, unwind liquidity) that alter the loss law in a directed, low-dimensional manner. An unstructured relative-entropy ball admits arbitrary deviations unrelated to these primitives, and the manuscript provides neither a derivation linking the radius to plausible changes in those primitives nor numerical checks that the worst-case value remains stable or interpretable under such directed perturbations. This modeling choice is load-bearing for the claimed trade-off between band width and robust HVA.

Authors: The loss distribution P is obtained by Monte-Carlo simulation of rebalancing and unwind trades under explicit liquidity primitives (market-impact coefficients, bid-ask spreads, and unwind liquidity). Thus P already encodes the directed effect of those primitives for each no-trade-band rule. The relative-entropy ball is then placed around this P to capture residual distributional ambiguity. The manuscript explicitly distinguishes the fixed-radius convention from the fixed-benchmark-stress convention precisely to handle the fact that the same radius can correspond to different effective stress levels when turnover (and hence liquidity demand) changes with band width. Under the fixed-benchmark-stress convention the radius is calibrated so that the worst-case expectation equals a pre-specified stress level for a benchmark rule; this calibration provides an implicit link between the ambiguity set and the liquidity primitives via the benchmark. We acknowledge, however, that the manuscript does not supply an explicit analytic derivation mapping infinitesimal changes in the primitives to the radius, nor does it report numerical experiments that replace the unstructured ball with directed perturbations of the primitives. We will add a clarifying paragraph in the revised introduction and methodology section explaining the role of the two conventions and the modeling choice. If the referee can suggest concrete directed perturbations, we are prepared to include a sensitivity study in a revised version. revision: partial

Circularity Check

No significant circularity in derivation chain

full rationale

The paper generates loss distributions via simulation of rebalancing and unwind rules for each no-trade band, then defines robust HVA explicitly as the worst-case expectation under a relative-entropy ball around that distribution. No equations, parameters, or self-citations reduce the HVA value or the band-width trade-off back to fitted inputs or prior results by construction. The central claims rest on external simulation outputs and the explicit definition of the ambiguity set, rendering the derivation self-contained.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

10 Cyril Bénézet and Stéphane Crépey

doi: 10.1016/S1386-4181(01)00024-6. 10 Cyril Bénézet and Stéphane Crépey. Handling model risk with xvas.Frontiers of Mathematical Finance, 3 (4):490–519,

-

[2]

Cyril Bénézet, Stéphane Crépey, and Dounia Essaket

doi: 10.3934/fmf.2024016. Cyril Bénézet, Stéphane Crépey, and Dounia Essaket. The recalibration conundrum: Hedging Valuation Adjustment for callable claims,

-

[3]

Fischer Black and Myron Scholes

arXiv:2304.02479. Fischer Black and Myron Scholes. The pricing of options and corporate liabilities.Journal of Political Economy, 81(3):637–654,

-

[4]

doi: 10.1086/260062. Benedict Burnett. Hedging valuation adjustment: Fact and friction. Technical report, SSRN, October

-

[5]

Retrieved March 24, 2026, fromhttps://fred.stlouisfed.org/series/VIXCLS. Mark H. A. Davis, Vassilios G. Panas, and Thaleia Zariphopoulou. European option pricing with transaction costs.SIAM Journal on Control and Optimization, 31(2):470–493,

2026

-

[6]

doi: 10.1137/0331022. Paul Glasserman and Xingbo Xu. Robust risk measurement and model risk.Quantitative Finance, 14(1): 29–58,

-

[7]

doi: 10.1080/14697688.2013.822989. J. S. Kennedy, P. A. Forsyth, and K. R. Vetzal. Dynamic hedging under jump diffusion with transaction costs.Operations Research, 57(3):541–559,

-

[8]

doi: 10.1287/opre.1080.0598. Hayne E. Leland. Option pricing and replication with transactions costs.The Journal of Finance, 40(5): 1283–1301,

-

[9]

The disposition to sell winners too early and ride losers too long: T heory and evidence

doi: 10.1111/j.1540-6261.1985.tb02383.x. Robert C. Merton. Theory of rational option pricing.The Bell Journal of Economics and Management Science, 4(1):141–183,

-

[10]

doi: 10.2307/3003143. Robert C. Merton. Option pricing when underlying stock returns are discontinuous.Journal of Financial Economics, 3(1–2):125–144,

-

[11]

doi: 10.1016/0304-405X(76)90015-2. Artur Sepp. An approximate distribution of delta-hedging errors in a jump-diffusion model with discrete trading and transaction costs.Quantitative Finance, 12(7):1119–1141,

-

[12]

doi: 10.1080/14697688.2010. 494613. H. Mete Soner, Steven E. Shreve, and Jakša Cvitanić. There is no nontrivial hedging portfolio for option pricing with transaction costs.The Annals of Applied Probability, 5(2):327–355,

-

[13]

doi: 10.1111/1467-9965.00034. 11 A Supplementary numerical analyses A.1 Window sensitivity Table 7 summarizes the window sensitivity. With 126-day windows, the stress targetρG target ranges from 0.459 to 0.550 andεcalib ranges from 0.0035 to 0.0048. With 252-day windows, the target is 0.472–0.482. With 756-day windows, the target range falls to about 0.36...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.