Stochastic Volatility in Mean Models with Heavy Tails: A Fast Approximate Bayesian Inference Using Hidden Markov Models

Pith reviewed 2026-06-26 09:14 UTC · model grok-4.3

The pith

Special functions enable fast approximate Bayesian inference for heavy-tailed stochastic volatility in mean models

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

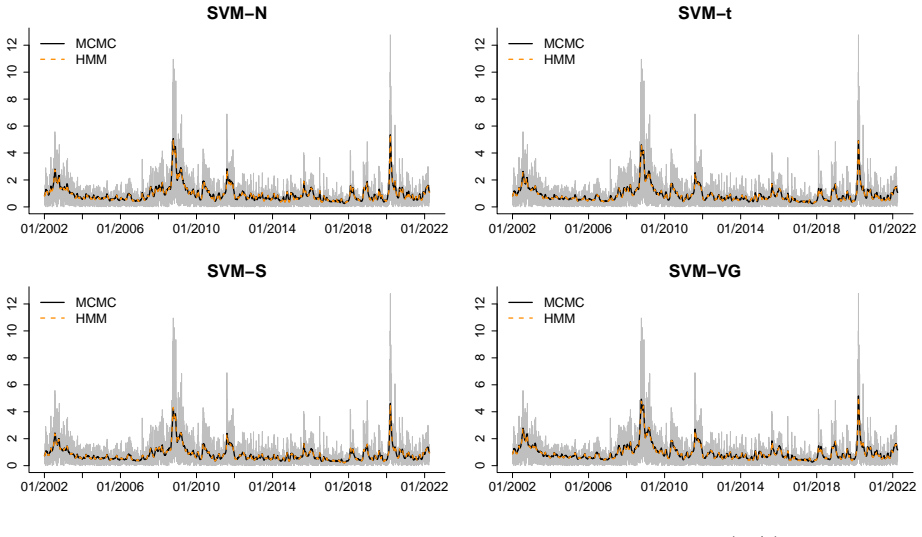

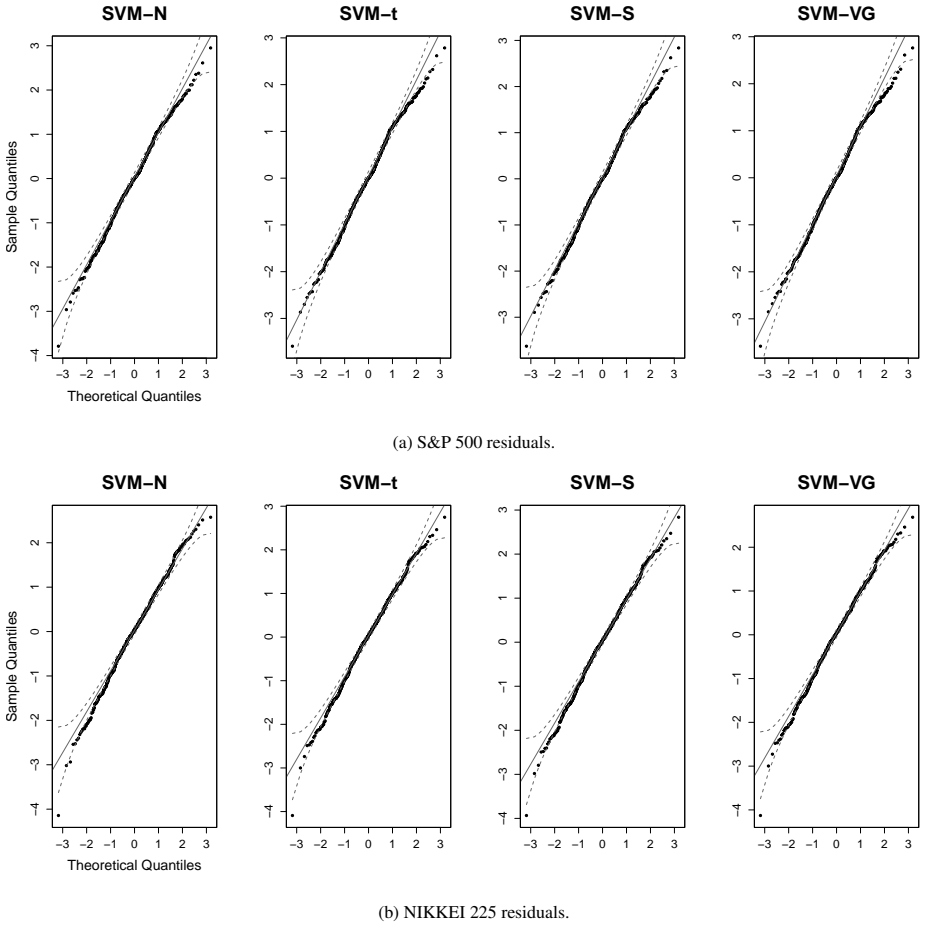

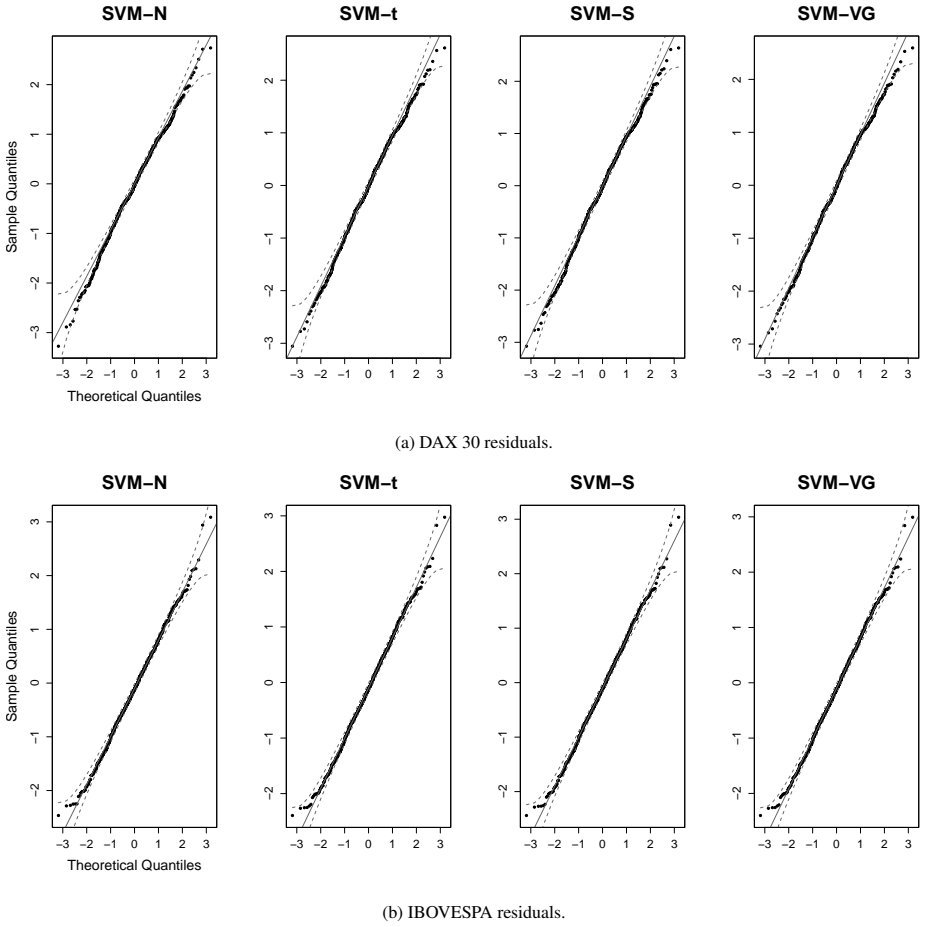

The authors develop a numerically stable estimation procedure for approximate Bayesian inference in SVM models with SMN heavy tails that exploits special functions to eliminate the need for direct numerical integration, incorporates parallel computing strategies, and delivers accurate inference at computational times approximately an order of magnitude smaller than those required by conventional MCMC methods.

What carries the argument

Hidden Markov model representation of the SVM-SMN model combined with special functions that remove direct numerical integration from the approximate Bayesian updates

Load-bearing premise

That the use of special functions to eliminate direct numerical integration preserves posterior accuracy without introducing material approximation bias or instability for the SMN family in the SVM setting

What would settle it

A simulation study in which the approximate posterior means, variances, or credible intervals for key parameters deviate substantially from those obtained by long MCMC runs on the identical SVM-SMN data set

Figures

read the original abstract

This paper extends the approximate Bayesian estimation framework for Stochastic Volatility in Mean (SVM) models to accommodate heavy-tailed distributions from the Scale Mixture of Normals (SMN) family. To overcome the computational challenges arising from these models, we propose a numerically stable estimation procedure that exploits special functions to eliminate the need for direct numerical integration. Furthermore, the implementation incorporates parallel computing strategies that substantially reduce computational costs. Simulation studies and empirical applications demonstrate that the proposed approach delivers accurate inference while achieving computational times that are approximately an order of magnitude smaller than those required by conventional Markov chain Monte Carlo (MCMC) methods.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript extends an approximate Bayesian estimation framework for stochastic volatility in mean (SVM) models to the scale mixture of normals (SMN) family. It replaces direct numerical integration with special functions for numerical stability and incorporates parallel computing to reduce runtime, claiming that simulation studies and empirical applications show accurate posterior inference at computational cost roughly an order of magnitude lower than standard MCMC.

Significance. If the special-function approximation is shown to introduce negligible bias relative to the target posterior, the method would supply a practical, scalable tool for Bayesian inference in heavy-tailed SVM models common in financial econometrics. The combination of analytic special-function substitutions with parallelization addresses a genuine computational bottleneck; however, the absence of reported error metrics or baseline comparisons in the provided description limits assessment of whether the accuracy claim holds.

major comments (1)

- [Simulation studies and empirical applications] The central claim that the special-function substitution preserves posterior accuracy (particularly for the volatility-in-mean coefficient) without material bias rests on unshown simulation evidence. No quantitative error metrics, comparison to exact integration or full MCMC, or sensitivity checks for the SMN family are described, leaving the weakest assumption untested.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback. Below we respond to the major comment.

read point-by-point responses

-

Referee: [Simulation studies and empirical applications] The central claim that the special-function substitution preserves posterior accuracy (particularly for the volatility-in-mean coefficient) without material bias rests on unshown simulation evidence. No quantitative error metrics, comparison to exact integration or full MCMC, or sensitivity checks for the SMN family are described, leaving the weakest assumption untested.

Authors: We agree that more explicit quantitative validation would strengthen the paper. Section 4 of the manuscript reports simulation results in which posterior means and intervals from the proposed method closely match those from MCMC for the volatility-in-mean coefficient under several SMN distributions. However, we acknowledge that tabulated error metrics (bias, RMSE, coverage rates) and direct comparisons against exact integration are not provided. In the revised manuscript we will add these metrics together with sensitivity checks across the SMN family. revision: yes

Circularity Check

No significant circularity; derivation self-contained against external benchmarks

full rationale

The paper extends an approximate Bayesian framework for SVM models to the SMN family by replacing numerical integration with special functions and adding parallelization. Claims of accurate inference and ~10x speedup are validated via simulation studies and empirical applications, which constitute independent external checks rather than reductions to fitted inputs or self-citations. No equations, derivations, or load-bearing steps in the provided text reduce by construction to the paper's own inputs. No self-citation chains, ansatzes smuggled via prior work, or uniqueness theorems are invoked in a manner that forces the central result. This is the common honest finding for a methods paper whose performance assertions rest on reproducible simulation design.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The SVM model with SMN errors admits an exact hidden Markov representation that enables the use of special functions in place of numerical integration.

Reference graph

Works this paper leans on

-

[1]

Stegun , year =

M Abramowitz and N. Stegun , year =. Handbook of Mathematical Functions , address =

-

[2]

Marwala , year =

T. Marwala , year =. Condition monitoring using computational intelligence method , address =

-

[3]

D. F. Andrews and P. J. Bickel and F. R. Hampel and P. J. Huber and W. H. Rogers and J.W. Tukey , year =. Robust Estimates of Location:

-

[4]

Zucchini and I

W. Zucchini and I. L. MacDonald and R. Langrock , year =. Hidden Markov Models for Time Series: An Introduction Using R , edition=

-

[5]

Leimkuhler and S

B. Leimkuhler and S. Reich , year =. Simulating Hamiltonian Dynamics , address =

-

[6]

B. D. Ripley , year =. Stochastic Simulation , address =

-

[7]

1986 , publisher=

Modelling Financial Time Series , author=. 1986 , publisher=

1986

-

[8]

Zucchini and I

W. Zucchini and I. L. MacDonald , publisher =. Hidden Markov Models for Time Series: An Introduction Using R , year =

-

[9]

Chib , year =

S. Chib , year =. Markov chain. Handbook of

-

[10]

Bollerslev and R

T. Bollerslev and R. F. Engle and D. B. Nelson , year =. Handbook of

-

[11]

Ghysels and A

E. Ghysels and A. C. Harvey and E. Renault , year =. Stochastic volatility , editor =. Handbook of

-

[12]

N. G. Shephard , year =. Statistical aspects of. Time Series Models in Econometrics, Finance and Other Fields, Monographs on Statistics and Applied Probability 65 , address =

-

[13]

F. X. Diebold and J. A. Lopes , year =. Modeling volatility dynamics , editor =. In Macreoconometrics: Developments, Tensions and Prospects , address =

-

[14]

M Neal , year =

R. M Neal , year =. MCMC using Hamiltonian dynamics , editor =. Handbook of Markov Chain Monte Carlo , address =

-

[15]

Geweke , year =

J. Geweke , year =. Evaluating the accuracy of sampling-based approaches to the calculation of posterior moments , editor =

-

[16]

Taylor , year =

S.J. Taylor , year =. Financial returns modelled by the product of two stochastic processes-a study of the daily sugar prices 1961-75 , editor =. Time

1961

-

[17]

C. A. Abanto-Valle and Gabriel Rodr\'iguez and H. B. Garrafa-Arag\'on , title =. 2021 , journal =

2021

-

[18]

P. H. Kupiec , year =. Techniques for verifying the accuracy of risk measurement models , journal =

-

[19]

Embrechts and R

P. Embrechts and R. Kaufmann and P. Patie , year =. Strategic Long-term Financial Risks: Single Risk Factors , journal =

-

[20]

C. A. Abanto-Valle and R. Langrock and M.-H. Chen and M. V. Cardoso , year =. Maximum likelihood estimation for stochastic volatility in mean models with heavy-tailed distributions , journal =

-

[21]

F. X. Diebold and A. Inoue , year =. Long memory and regime switching , journal =

-

[22]

Perron and Z

P. Perron and Z. Qu , year =. Long-memory and level shifts in the volatility of stock market return indices , journal =

-

[23]

G. Rodr. The North American Journal of Economics and Finance , volume =. 2017 , title =

2017

-

[24]

J. C. Chan , year =. The stochastic volatility in mean model with time-varying parameters: An application to inflation modeling , journal =

-

[25]

C. A. Abanto-Valle and H. S. Migon and V. H. Lachos , year =. Stochastic volatility in mean models with heavy-tailed distributions , journal =

-

[26]

C. A. Abanto-Valle and D. Bandyopadhyay and V. H. Lachos and I. Enriquez , year =. Robust Bayesian analysis of heavy-tailed stochastic volatility models using scale mixtures of normal distributions , journal =

-

[27]

C. A. Abanto-Valle and H. S. Migon and V. H. Lachos , year =. Stochastic volatility in mean models with scale mixtures of normal distributions and correlated errors: A Bayesian approach , journal =

-

[28]

Aas and I

K. Aas and I. H. Haff , title =. Journal of Financial Econometrics , volume =. 2006 , pages =

2006

-

[29]

Shephard and M

N. Shephard and M. Pitt , year =. Likelihood analysis of non-Gaussian measurements time series , journal=

-

[30]

Watanabe and Y

T. Watanabe and Y. Omori , year =. A multi-move sampler for estimate non-Gaussian time series model: Comments on Shepard and Pitt (1997) , journal =

1997

-

[31]

Watanabe , year =

S. Watanabe , year =. Asymtotic equivalence of Bayes crross validation and widely applicable information criterion in singular learning theory , journal =

-

[32]

Spiegelhalter, D. J. and Best, N. G. and Carlin, B. P. and van. Journal of the Royal Statistical Society, Series. 2002 , title =

2002

-

[33]

Watanabe , year =

S. Watanabe , year =. A widely applicable Bayesian information criterion , journal =

-

[34]

Nakajima , year =

J. Nakajima , year =. Stochastic volatility model with regime-switching skewness in heavy-tailed errors for exchange rate returns , journal =

-

[35]

Chen and L

M.-H. Chen and L. Huan and J.G. Ibrahim and S. Kim , year =. Bayesian Variable Selection and Computation for Generalized Linear Models with Conjugate Priors , journal =

-

[36]

Geweke , journal =

J. Geweke , journal =. Bayesian Inference in Econometric Models Using Monte Carlo Integration , volume =. 1989 , note=

1989

-

[37]

D. B. Nugroho and T. Morimoto , year =. Estimation of realized stochastic volatility models using Hamiltonian Monte Carlo-Based methods , journal =

-

[38]

M. A. Carnero and D. Pe. Journal of Financial Econometrics , volume=. 2004 , title =

2004

-

[39]

Abanto-Valle and Caifeng Wang and Xiaojing Wang and Fei-Xing Wang and Ming-Hui Chen , year =

Carlos A. Abanto-Valle and Caifeng Wang and Xiaojing Wang and Fei-Xing Wang and Ming-Hui Chen , year =. Bayesian Inference for Stochastic Volatility Models Using the Generalized Skew-t Distribution with Applications to the Shenzhen Stock Exchange Returns , journal=

-

[40]

W. L. Le. Statistics and its Interface , volume=. 2017 , title =

2017

-

[41]

Bollerslev and R

T. Bollerslev and R. Y. Chou and K. F. Kroner , year =. Journal of Econometrics , volume=

-

[42]

Duane and A

S. Duane and A. D. Kennedy and B. J. Pendleton and D. Roweth , year =. Hybrid Monte Carlo , journal=

-

[43]

Bekaert and G

G. Bekaert and G. Wu , year =. Asymmetric Volatility and Risk in Equity Markets , journal =

-

[44]

G. Wu. The Determinats of Asymmetric Volatility. Review of Financial Studies. 2001

2001

-

[45]

D. Nelson. Conditional Heteroskedasticity in Asset Returns: a New Approach. Econometrica. 1991

1991

-

[46]

L. R. Glosten and R. Jagannathan and D. E. Runkle. On the Relation Between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. Jorunal of Finance. 1993

1993

-

[47]

R. F. Engle and V. Ng. Measuring and testing the impact of news in volatility. Jorunal of Finance. 1993

1993

-

[48]

Black , year =

F. Black , year =. Studies of stock price volatility changes , journal =

-

[49]

J. Y. Campbell and L. Hentschel , year =. No News is Good News: An Asymmetric Model of Changing Volatility in Stock Returns , journal =

-

[50]

K. R. French and W. G. Schert and R. F. Stambugh , year =. Expected Stock Return and Volatility , journal =

-

[51]

S. J. Koopman and E. H. Uspensky , year =. The stochastic volatility in mean model: empirical evidence from international tock markets , journal =

-

[52]

G. W. Schwert , year =. Why does stock market volatility change over time? , journal =

-

[53]

M. A. Tanner and W. H. Wong , year =. The calculation of posterior distributions by data augmentation , journal =

-

[54]

C. K. Carter and R. Kohn , year =. On. Biometrika , volume =

-

[55]

Cathy W. S. Chen and F. C. Liu and Mike K. P. So , year =. Heavy-tailed-distributed threshold stochastic volatility models in financial time series , journal =

-

[56]

Chib and E

S. Chib and E. Greenberg , year =. Understanding the. The American Statistician , volume =

-

[57]

Chib , year =

S. Chib , year =. Estimation and Comparison of Multiple Change-Point Models , journal =

-

[58]

Markov chain Monte Carlo methods for stochastic volatility models , volume =

Siddhartha Chib and Federico Nardari and Neil Shephard , journal =. Markov chain Monte Carlo methods for stochastic volatility models , volume =

-

[59]

S. T. Boris Choy and Jennifer S. K. Chan , year =. Scale mixtures distributions in statistical modelling , journal =

-

[60]

A. A. Christie , year =. The stochastic behavior of common stock variances:. Journal of Financial Economics , volume =

-

[61]

A. E. Clements and S. Hurn and S. I. White , journal =. Mixture distribution-based forecasting using stochastic volatility model , volume =

-

[62]

Biometrika , volume =

Piet de. Biometrika , volume =. 1995 , title =

1995

-

[63]

Delatola and J

E-I. Delatola and J. E. Griffin , year =. Bayesian Nonparametric Modelling of the Return Distribution with Stochastic Volatility , journal =

-

[64]

Fama , year =

E. Fama , year =. Portfolio analysis in a stable paretian market , journal =

-

[65]

Threshold Stochastic Volatility Models with Heavy Tails: A Bayesian Approach , author=. Econom

-

[66]

Fridman and L

M. Fridman and L. Harris , journal =. A maximum likelihood approach for non-Gaussian stochastic volatility models , volume =

-

[67]

T. C. O. Fonseca and M. A. R. Ferreira and H. S. Migon , year =. Objective. Biometrika , volume =

-

[68]

Gneiting and A

T. Gneiting and A. E. Raftery , issue =. Strictly proper scoring rules, prediction and estimation , volume =. Journal of the American Statistical Association , pages =

-

[69]

I. J. Good , year =. Rational Decisions , journal =

-

[70]

Ju\'arez and M

Miguel A. Ju\'arez and M. F. J. Steel , year =. Strategic Long-term Financial Risks: Single Risk Factors , journal =

-

[71]

Polson and Peter E

Eric Jacquier and Nicholas G. Polson and Peter E. Rossi , journal =. Bayesian analysis of stochastic volatility models with fat-tails and correlated errors , volume =. 2004 , note=

2004

-

[72]

Kim and Neil Shepard and S

S. Kim and Neil Shepard and S. Chib , year =. Stochastic volatility: likelihood inference and comparison with. Review of Economic Studies , volume =

-

[73]

Girolami and Ben Calderhead , journal =

M. Girolami and Ben Calderhead , journal =. Riemann manifold Langevin and Hamiltonian Monte Carlo methods , volume =. 2011 , pages =

2011

-

[74]

The Quarterly Review of Economics and Finance , title =

Patricia. The Quarterly Review of Economics and Finance , title =. 2018 , pages =

2018

-

[75]

K. L. Lange and J. S. Sinsheimer , year =. Normal/independent distributions and their applications in robust regression , journal =

-

[76]

Langrock , title =

R. Langrock , title =. 2011 , journal =

2011

-

[77]

Langrock and I

R. Langrock and I. L. MacDonald and W. Zucchini , year =. Some nonstandard stochastic volatility models and their estimation using structured hidden Markov models , journal =

-

[78]

Ataurima

M. Ataurima. Empirical Modeling of High-Income and Emerging Stock and Forex Market Return Volatility using Markov-Switching GARCH Models , volume =. The North American Journal of Economics and Finance , pages =

-

[79]

Alanya and G

W. Alanya and G. Rodr\'iguez , journal =. Asymmetries in Volatility: An Empirical Study for the Peruvian Stock and Forex Returns , volume =. 2019 , note=

2019

-

[80]

Rodr\'iguez , journal =

G. Rodr\'iguez , journal =. Selecting Between Autoregressive Conditional Heterocedasticidity Models: An Empirical Application to the Volatility of Stock Returns in Peru , volume =. 2017 , note=

2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.