Bitcoin's Power Law: Weak Structure, Strong Forecasts

Pith reviewed 2026-05-21 03:38 UTC · model grok-4.3

The pith

Bitcoin price follows a power law that lacks structural robustness yet delivers stronger 12-24 month forecasts than standard time-series models.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

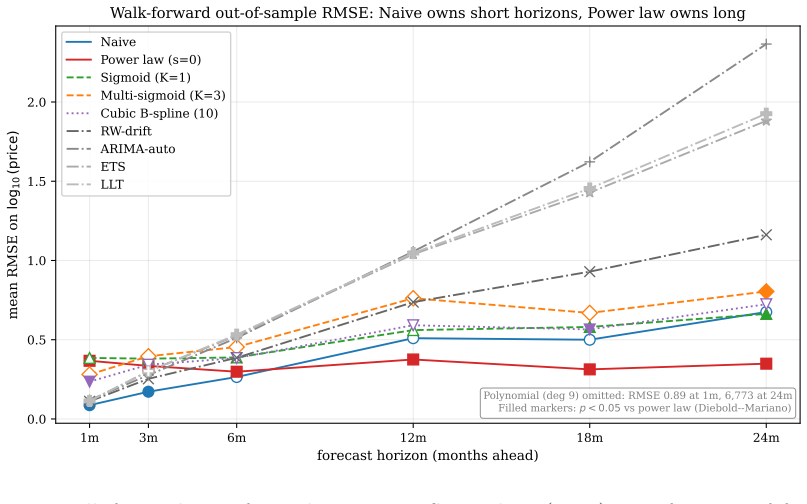

The central claim is that Bitcoin price exhibits no robust distributional or shift-invariant power-law structure and cannot be distinguished from multi-sigmoid growth by standard diagnostics, yet the simple power-law specification dominates 12-24 month forecasting horizons over random-walk-with-drift, auto-ARIMA, ETS, local-linear-trend and other baselines at p < 0.05, because it avoids committing to particular cycle shapes.

What carries the argument

The time-domain power-law model P(t) ~ t^β together with adapted Clauset-Shalizi-Newman protocols and walk-forward Diebold-Mariano comparisons against ten forecasting baselines.

If this is right

- The power law can serve as a reliable default for 12-24 month Bitcoin price projections without requiring wave-shape assumptions.

- Multi-sigmoid or other flexible in-sample models are likely to degrade on long horizons for the same series.

- Bitcoin remains the sole series among the nine tested where no single-component growth curve beats the power law in-sample.

- The quarterly K=3 wave-stability bootstrap signals that a PL+AR(1) combination is unstable for Bitcoin at the 15 percent threshold.

Where Pith is reading between the lines

- The forecasting edge may arise because the power law implicitly averages over irregular cycles that defeat more structured alternatives.

- The same simple-model advantage could be checked on other non-stationary series such as gold or equity indices.

- Practitioners might prefer power-law baselines for assets whose growth lacks repeatable wave patterns.

Load-bearing premise

The ten chosen baseline forecasters plus the multi-sigmoid alternative form a fair and exhaustive comparison set that reveals whether the power law's forecasting edge is genuine.

What would settle it

A new walk-forward evaluation on post-2024 Bitcoin prices in which the power law fails to outperform the standard baselines at p < 0.05 over 12-24 month horizons would refute the forecasting advantage.

Figures

read the original abstract

Bitcoin's price has been described as following a power law (PL) in time, $P \sim t^{\beta}$ with $\hat\beta \approx 5.7$ over 2010-2026. We test this claim using the Clauset-Shalizi-Newman protocol applied to Bitcoin's tail-relevant distributional series, and develop three principled time-domain adaptations of the protocol. We find that (i) the distributional power law is rejected on UTXO balances and daily |returns|, with lognormal preferred decisively; (ii) the fitted time-domain exponent varies by nearly a factor of three across reasonable shifts of the time origin -- it is not specification-robust in the sense required for a shift-invariant structural reading; (iii) standard residual diagnostics and scale-invariance tests proposed in earlier work cannot distinguish a power law from a multi-component sigmoid stack fit to the same data; (iv) Bitcoin price stands apart in a cross-asset comparison spanning Bitcoin on-chain metrics and traditional asset classes: it is the only series in the nine-series in-sample test where no single-component growth curve improves on the power law, and the quarterly $K=3$ wave-stability bootstrap rejects the PL+AR(1) null on Bitcoin at $p = 0.015$ (strict 15% CV threshold) -- a clear cross-asset separation, although not a Bonferroni-robust rejection; and (v) walk-forward Diebold-Mariano evaluation against ten candidates -- including standard time-series baselines (RW with drift, auto-ARIMA, ETS, local-linear-trend) -- shows the in-sample winner (multi-sigmoid) is among the worst long-horizon forecasters, while the simple power law dominates 12-24 month horizons against every standard baseline at $p < 0.05$, precisely because it does not commit to specific wave shapes. The fit-prediction tradeoff is the practical counterpart of the descriptive findings.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript tests the power-law hypothesis for Bitcoin prices (P ~ t^β) using the Clauset-Shalizi-Newman protocol on distributional series and three new time-domain adaptations. It reports rejection of distributional power laws on UTXO balances and |returns| (lognormal preferred), factor-of-three variation in the time-domain exponent across time-origin shifts, failure of residual diagnostics to separate power laws from multi-sigmoid stacks, Bitcoin's uniqueness among nine cross-asset series (no single-component growth curve improves on PL; K=3 bootstrap rejects PL+AR(1) at p=0.015), and superior 12-24 month walk-forward Diebold-Mariano performance of the simple power law over ten baselines (RW-drift, auto-ARIMA, ETS, local-linear-trend, etc.) at p<0.05, attributed to its refusal to commit to wave shapes.

Significance. If the forecasting results are robust, the work provides evidence that parsimonious power-law extrapolations can outperform both standard time-series baselines and more flexible in-sample winners on long horizons for non-stationary assets. This would strengthen the case for simple structural models in volatile financial series where overfitting to transient patterns degrades out-of-sample accuracy.

major comments (2)

- [Finding (v)] Finding (v): The walk-forward Diebold-Mariano claim that the simple power law dominates 12-24 month horizons at p<0.05 rests on a single time-origin choice. Finding (ii) shows the fitted exponent varies by nearly a factor of three across reasonable origin shifts, which materially alters the extrapolated trajectory. The manuscript must demonstrate that the reported superiority survives re-running the full forecasting exercise under at least two additional plausible origins (e.g., 2009-01-03 and 2011-01-01).

- [Finding (iv)] Finding (iv): The quarterly K=3 wave-stability bootstrap rejects the PL+AR(1) null for Bitcoin at p=0.015 while no other series shows comparable separation. With only nine series and an explicit note that the result is not Bonferroni-robust, the cross-asset uniqueness claim requires either a pre-specified multiple-testing correction or an explicit statement that the test is exploratory rather than confirmatory.

minor comments (2)

- [Abstract] Abstract: The phrase 'strict 15% CV threshold' is ambiguous; expand to clarify whether CV denotes critical value, cross-validation, or another quantity and how the 15% level was chosen.

- [Methods] Methods: The three principled time-domain adaptations of the Clauset-Shalizi-Newman protocol are central but described only at high level; explicit algorithmic steps or pseudocode would improve reproducibility.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive suggestions. We address the two major comments below and will incorporate revisions to strengthen the robustness and interpretation of our results.

read point-by-point responses

-

Referee: Finding (v): The walk-forward Diebold-Mariano claim that the simple power law dominates 12-24 month horizons at p<0.05 rests on a single time-origin choice. Finding (ii) shows the fitted exponent varies by nearly a factor of three across reasonable origin shifts, which materially alters the extrapolated trajectory. The manuscript must demonstrate that the reported superiority survives re-running the full forecasting exercise under at least two additional plausible origins (e.g., 2009-01-03 and 2011-01-01).

Authors: We agree that the forecasting results should be checked for sensitivity to the choice of time origin, given the variation in the exponent documented in Finding (ii). We will re-run the complete walk-forward Diebold-Mariano evaluation using the two additional origins suggested (2009-01-03 and 2011-01-01) and report the updated p-values and rankings in the revised manuscript. revision: yes

-

Referee: Finding (iv): The quarterly K=3 wave-stability bootstrap rejects the PL+AR(1) null for Bitcoin at p=0.015 while no other series shows comparable separation. With only nine series and an explicit note that the result is not Bonferroni-robust, the cross-asset uniqueness claim requires either a pre-specified multiple-testing correction or an explicit statement that the test is exploratory rather than confirmatory.

Authors: The manuscript already states that the result is not Bonferroni-robust. We will add an explicit sentence clarifying that the cross-asset uniqueness finding and the Bitcoin-specific rejection are exploratory in nature, given the small number of series examined and the lack of a pre-specified multiple-testing correction. revision: yes

Circularity Check

No significant circularity in empirical testing chain

full rationale

The paper's core claims rest on direct application of the Clauset-Shalizi-Newman protocol to Bitcoin data, cross-asset comparisons, residual diagnostics, and walk-forward Diebold-Mariano tests against ten external baselines (RW with drift, auto-ARIMA, ETS, local-linear-trend, multi-sigmoid). No equation or result is shown to reduce by construction to a fitted parameter that is then relabeled as a prediction; the reported exponent variation, distributional rejections, and long-horizon dominance are outputs of independent statistical procedures rather than self-referential definitions. The analysis is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

doi: 10.1109/TAC.1974.1100705. David H. Bailey, Jonathan M. Borwein, Marcos López de Prado, and Qiji Jim Zhu. Pseudo- mathematics and financial charlatanism: The effects of backtest overfitting on out-of-sample performance.Notices of the American Mathematical Society, 61(5):458–471,

-

[2]

doi: 10.1287/mnsc.15.5.215. T. S. Breusch and A. R. Pagan. A simple test for heteroscedasticity and random coefficient variation.Econometrica, 47(5):1287–1294,

-

[3]

doi: 10.2307/1911963. Anna D. Broido and Aaron Clauset. Scale-free networks are rare.Nature Communications, 10 (1):1017,

-

[4]

Leopoldo Catania, Stefano Grassi, and Francesco Ravazzolo

doi: 10.1038/s41467-019-08746-5. Leopoldo Catania, Stefano Grassi, and Francesco Ravazzolo. Forecasting cryptocurrencies under model and parameter instability.International Journal of Forecasting, 35(2):485–501,

-

[5]

doi: 10.1016/j.ijforecast.2018.09.005. 42 Gregory C. Chow. Tests of equality between sets of coefficients in two linear regressions.Econo- metrica, 28(3):591–605,

-

[6]

Tests of Equality Between Sets of Coefficients in Two Linear Regressions

doi: 10.2307/1910133. Aaron Clauset, Cosma Rohilla Shalizi, and M. E. J. Newman. Power-law distributions in empirical data.SIAM Review, 51(4):661–703,

-

[7]

doi: 10.1137/070710111. David A. Dickey and Wayne A. Fuller. Distribution of the estimators for autoregressive time series with a unit root.Journal of the American Statistical Association, 74(366):427–431,

-

[8]

FrancisX.DieboldandRobertoS.Mariano

doi: 10.2307/2286348. FrancisX.DieboldandRobertoS.Mariano. Comparingpredictiveaccuracy.Journal of Business & Economic Statistics, 13(3):253–263,

-

[9]

Parisa Foroutan and Salim Lahmiri

doi: 10.1080/07350015.1995.10524599. Parisa Foroutan and Salim Lahmiri. Bitcoin price regime shifts: A Bayesian MCMC and hidden Markov model analysis of macroeconomic influence.Mathematics, 13(10):1577,

-

[10]

Nikola Gradojevic, Dragan Kukolj, Robert Adcock, and Vladimir Djakovic

doi: 10.3390/math13101577. Nikola Gradojevic, Dragan Kukolj, Robert Adcock, and Vladimir Djakovic. Forecasting Bitcoin with technical analysis: A not-so-random forest?International Journal of Forecasting, 39(1): 1–17,

-

[11]

doi: 10.1016/j.ijforecast.2021.08.001. C. W. J. Granger. Investigating causal relations by econometric models and cross-spectral methods.Econometrica, 37(3):424–438,

-

[12]

doi: 10.2307/1912791. C. W. J. Granger and P. Newbold. Spurious regressions in econometrics.Journal of Economet- rics, 2(2):111–120,

-

[13]

Vincent Gurgul, Stefan Lessmann, and Wolfgang Karl Härdle

doi: 10.1016/0304-4076(74)90034-7. Vincent Gurgul, Stefan Lessmann, and Wolfgang Karl Härdle. Deep learning and NLP in cryp- tocurrency forecasting: Integrating financial, blockchain, and social media data.International Journal of Forecasting, 41(4):1666–1695,

-

[14]

doi: 10.1016/j.ijforecast.2025.02.007. Andrew C. Harvey and James Durbin. The effects of seat belt legislation on British road casualties: A case study in structural time series modelling.Journal of the Royal Statistical Society, Series A, 149(3):187–210,

-

[15]

doi: 10.2307/2981553. Rob J. Hyndman and Yeasmin Khandakar. Automatic time series forecasting: The forecast package for R.Journal of Statistical Software, 27(3):1–22,

-

[16]

doi: 10.18637/jss.v027.i03. Carlos M. Jarque and Anil K. Bera. Efficient tests for normality, homoscedasticity and serial independence of regression residuals.Economics Letters, 6(3):255–259,

-

[17]

doi: 10.1093/biomet/65.2.297. Nicolás F. Magner and Nicolás Hardy. Cryptocurrency forecasting: More evidence of the Meese– Rogoff puzzle.Mathematics, 10(13):2338,

-

[18]

doi: 10.3390/math10132338. Richard A. Meese and Kenneth Rogoff. Empirical exchange rate models of the seventies: Do they fit out of sample?Journal of International Economics, 14(1–2):3–24,

-

[19]

1016/0022-1996(83)90017-X. Michael Mitzenmacher. A brief history of generative models for power law and lognormal dis- tributions.Internet Mathematics, 1(2):226–251,

work page 1996

-

[20]

doi: 10.1080/15427951.2004.10129088. Whitney K. Newey and Kenneth D. West. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix.Econometrica, 55(3):703–708,

-

[21]

43 Simona-Vasilica Oprea and Adela Bâra

doi: 10.2307/1913610. 43 Simona-Vasilica Oprea and Adela Bâra. Regime-aware adaptive forecasting framework for Bit- coin prices using probabilistic generative models.Computational Economics,

-

[22]

doi: 10.1007/s10614-026-11338-3. forthcoming. Filippo Puoti, Fabrizio Pittorino, and Manuel Roveri. Quantifying cryptocurrency unpre- dictability: A comprehensive study of complexity and forecasting. InProceedings of AIML- Systems

-

[23]

doi: 10.3390/jrfm18020066. Said E. Said and David A. Dickey. Testing for unit roots in autoregressive-moving average models of unknown order.Biometrika, 71(3):599–607,

-

[24]

Giovanni Santostasi and Stephen Perrenod

doi: 10.1093/biomet/71.3.599. Giovanni Santostasi and Stephen Perrenod. A mechanistic derivation of the Bitcoin price power law: Network adoption dynamics and generalised Metcalfe scaling. Preprint, Scientific Bitcoin Institute,

-

[25]

doi: 10.2307/2333709. Austin Shelton. Bitcoin return prediction: Is it possible via stock-to-flow, Metcalfe’s law, technical analysis, or market sentiment?Journal of Risk and Financial Management, 17(10): 443,

-

[26]

doi: 10.3390/jrfm17100443. Leonard J. Tashman. Out-of-sample tests of forecasting accuracy: an analysis and review.Inter- national Journal of Forecasting, 16(4):437–450,

-

[27]

doi: 10.1016/S0169-2070(00)00065-0. Bilgehan Tekin. Structural breaks and co-movements of Bitcoin and Ethereum: Evidence from the COVID-19 pandemic period.Journal of Central Banking Theory and Practice, 13(2): 41–70,

-

[28]

doi: 10.2478/jcbtp-2024-0012. Quang H. Vuong. Likelihood ratio tests for model selection and non-nested hypotheses.Econo- metrica, 57(2):307–333,

-

[29]

doi: 10.2307/1912557. Spencer Wheatley, Didier Sornette, Tobias Huber, Max Reppen, and Robert N. Gantner. Are Bitcoin bubbles predictable? Combining a generalized Metcalfe’s Law and the Log-Periodic Power Law Singularity model.Royal Society Open Science, 6(6):180538,

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.