Hedging Maturity-Specific Risk in Forward Curve Derivatives under Stochastic Volatility

Pith reviewed 2026-06-30 08:35 UTC · model grok-4.3

The pith

The quadratic hedging error for forward-curve claims splits exactly into bucket, rank and residual components under infinite-rank stochastic volatility.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under Heath-Jarrow-Morton-Musiela dynamics modulated by an infinite-rank stochastic covariance, the variance-optimal hedge is the Galtchouk-Kunita-Watanabe projection with respect to the covariance-norm quotient; the quadratic hedging error then decomposes exactly into bucket, rank and residual risk, and the residual risk functions as a stochastic-volatility floor in enlarged filtrations for claims that depend on non-traded covariance noise.

What carries the argument

The Galtchouk-Kunita-Watanabe projection onto the covariance-norm quotient generated by the forward-curve martingale, applied to an infinite-rank stochastic covariance component in the HJMM SPDE.

If this is right

- Finite-maturity and delivery-window strategies are dense in the hedging space.

- Spectral finite-rank projections converge to the optimal hedge.

- The quadratic error decomposes exactly into bucket, rank and residual risk.

- Residual risk acts as a stochastic-volatility floor in enlarged filtrations for claims on non-traded covariance noise.

Where Pith is reading between the lines

- Traders could monitor bucket, rank and residual exposures separately when managing large forward-curve books.

- The decomposition suggests a natural way to allocate capital across different sources of unhedgeable risk in infinite-dimensional markets.

- Similar projections might be examined in other infinite-dimensional term-structure models that carry stochastic volatility.

Load-bearing premise

The forward curve follows a Heath-Jarrow-Morton-Musiela stochastic partial differential equation modulated by an infinite-rank stochastic covariance component that makes the Galtchouk-Kunita-Watanabe projection well-defined.

What would settle it

A concrete model in which the quadratic hedging error cannot be decomposed into the three stated components, or in which finite-maturity strategies fail to be dense, would falsify the central claims.

Figures

read the original abstract

We study the variance-optimal hedging of European contingent claims written on forwards. We assume that the dynamics of the underlying forward curves follow a Heath--Jarrow--Morton--Musiela stochastic partial differential equation modulated by an infinite-rank stochastic covariance component. The variance-optimal hedge is then given by the Galtchouk--Kunita--Watanabe projection with respect to some covariance-norm quotient generated by the forward curve martingale. We show density of finite-maturity and delivery-window strategies, convergence of spectral finite-rank hedge projections and an exact decomposition of the quadratic hedging error into bucket, rank and residual risk components. In enlarged filtrations, the residual risk is a stochastic-volatility floor for claims loading on non-traded covariance noise. We illustrate the hedging framework in affine stochastic covariance and multiplicative HJMM models, and give a concrete example of the decomposition in a CIR stochastic covariance model.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a variance-optimal hedging framework for European claims on forward curves whose dynamics are given by an HJMM-Musiela SPDE driven by an infinite-rank stochastic covariance process. The hedge is obtained via the Galtchouk-Kunita-Watanabe projection onto the covariance-norm quotient generated by the forward-curve martingale. The central results are the density of finite-maturity and delivery-window strategies, L2-convergence of spectral finite-rank projections, and an exact orthogonal decomposition of the quadratic hedging error into bucket, rank, and residual components; the residual is interpreted as a stochastic-volatility floor when the filtration is enlarged by non-traded covariance noise. The framework is illustrated in affine stochastic-covariance and multiplicative HJMM models, with a concrete CIR example.

Significance. If the operator-theoretic foundations are rigorously justified, the exact bucket/rank/residual decomposition supplies a transparent separation of hedgeable and unhedgeable risks in an infinite-dimensional stochastic-volatility setting. This is a substantive contribution to the mathematical-finance literature on curve hedging, as it moves beyond finite-factor approximations and quantifies the residual floor due to covariance noise. The model illustrations add concreteness without introducing free parameters.

major comments (2)

- [§2.2] §2.2, Definition 2.3 and Assumption 2.4: The existence of the Galtchouk-Kunita-Watanabe projection with respect to the covariance-norm quotient is asserted for an infinite-rank stochastic covariance operator on the Musiela space, yet no pathwise regularity (e.g., nuclear or Hilbert-Schmidt property of the covariance operator) or predictable-representation condition is supplied to guarantee that the quotient is a well-defined Hilbert space and that the projection exists. All subsequent claims on density, spectral convergence, and the exact decomposition rest on this step; without the missing operator conditions the results do not follow.

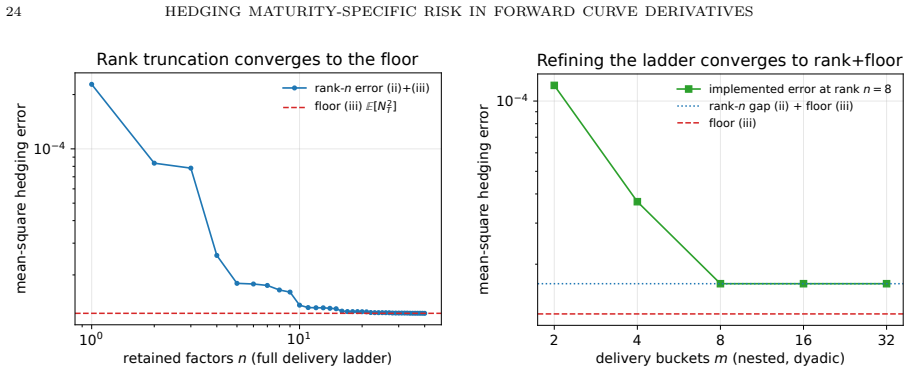

- [§4.1] §4.1, Theorem 4.2: The claimed L2-convergence of the spectral finite-rank hedge projections is stated without an explicit rate or error bound that would control the tail of the infinite-rank covariance; the proof sketch appears to rely on the same unverified quotient-space construction.

minor comments (2)

- [Eq. (3.7)] The distinction between the bucket-risk and rank-risk components in the decomposition (Eq. (3.7)) would be clearer if the orthogonal projection onto the finite-maturity subspace were written explicitly rather than left implicit.

- [§2] Notation for the Musiela parametrization and the covariance-norm quotient is introduced in §2 but reused with slight variations in §5; a single consolidated table of symbols would improve readability.

Simulated Author's Rebuttal

We thank the referee for the thorough review and valuable comments on the operator-theoretic foundations of our framework. We agree that the manuscript requires additional assumptions to rigorously establish the Galtchouk-Kunita-Watanabe projection in the infinite-dimensional setting. We will revise the paper to include the necessary regularity conditions and error bounds. Below we address each major comment.

read point-by-point responses

-

Referee: [§2.2] §2.2, Definition 2.3 and Assumption 2.4: The existence of the Galtchouk-Kunita-Watanabe projection with respect to the covariance-norm quotient is asserted for an infinite-rank stochastic covariance operator on the Musiela space, yet no pathwise regularity (e.g., nuclear or Hilbert-Schmidt property of the covariance operator) or predictable-representation condition is supplied to guarantee that the quotient is a well-defined Hilbert space and that the projection exists. All subsequent claims on density, spectral convergence, and the exact decomposition rest on this step; without the missing operator conditions the results do not follow.

Authors: We acknowledge this gap in the current version. To address it, we will introduce a new assumption (Assumption 2.5) requiring that the stochastic covariance operator process is predictable and takes values in the Hilbert-Schmidt operators on the Musiela space almost surely. This ensures the covariance-norm quotient is a separable Hilbert space, allowing the application of the Galtchouk-Kunita-Watanabe decomposition theorem in Hilbert spaces. With this, the projection exists uniquely, and the subsequent density results, spectral convergence, and orthogonal decomposition follow directly from the projection properties and the spectral theorem for compact operators. We will also add a remark on the predictable representation property holding under the affine model assumptions used in the illustrations. revision: yes

-

Referee: [§4.1] §4.1, Theorem 4.2: The claimed L2-convergence of the spectral finite-rank hedge projections is stated without an explicit rate or error bound that would control the tail of the infinite-rank covariance; the proof sketch appears to rely on the same unverified quotient-space construction.

Authors: We agree that providing an explicit convergence rate would improve the result. In the revised manuscript, we will strengthen Theorem 4.2 by deriving an error bound: the L2-distance between the infinite-rank and N-rank projections is bounded by the square root of the sum of the tail eigenvalues of the covariance operator, i.e., ||P - P_N|| <= (sum_{k>N} lambda_k)^{1/2}, where lambda_k are the eigenvalues. This bound follows from the Hilbert-Schmidt property and controls the tail under the assumption that the covariance is trace-class. The proof will be updated to explicitly use the new Assumption 2.5. revision: yes

Circularity Check

No circularity; derivation self-contained under standard stochastic assumptions

full rationale

The paper assumes HJMM-Musiela SPDE dynamics with infinite-rank stochastic covariance and posits existence of the GKW projection in the induced covariance-norm quotient; all subsequent claims (density of strategies, spectral convergence, bucket/rank/residual decomposition) are derived from this setup via standard stochastic calculus without any reduction of outputs to fitted inputs, self-definitional loops, or load-bearing self-citations. No equations or steps in the provided abstract or description equate a claimed result to its own construction by renaming or fitting.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Forward curve dynamics follow a Heath-Jarrow-Morton-Musiela SPDE modulated by an infinite-rank stochastic covariance component

- domain assumption The Galtchouk-Kunita-Watanabe projection exists with respect to the covariance-norm quotient generated by the forward curve martingale

Reference graph

Works this paper leans on

-

[1]

Andresen, S

A. Andresen, S. Koekebakker, and S. Westgaard. Modeling electricity forward prices using the multivariate normal inverse gaussian distribution.Journal of Energy Markets, 3(3):3–25, sep 2010

2010

-

[2]

Bátkai, B

A. Bátkai, B. Farkas, P. Csomós, and A. Ostermann. Operator semigroups for numerical analysis. Lecture notes for the 15th Internet Seminar, 2011/12, 2012. Accessed: 2024-08-13

2011

-

[3]

F. E. Benth and H. Eyjolfsson. Robustness of Hilbert space-valued stochastic volatility models. Finance and Stochastics, 28(4):1117–1146, 2024

2024

-

[4]

F. E. Benth and S. Koekebakker. Stochastic modeling of financial electricity contracts.Energy Economics, 30(3):1116–1157, 2008

2008

-

[5]

F. E. Benth and P. Krühner. Representation of infinite-dimensional forward price models in com- modity markets.Communications in Mathematics and Statistics, 2(1):47–106, 2014

2014

-

[6]

F. E. Benth, B. Rüdiger, and A. Süss. Ornstein–Uhlenbeck processes in Hilbert space with non- Gaussian stochastic volatility.Stochastic Processes and their Applications, 128(2):461–486, 2018

2018

-

[7]

F. E. Benth, J. Šaltyt˙ e Benth, and S. Koekebakker.Stochastic Modeling of Electricity and Related Markets. World Scientific Publishing Co. Pte. Ltd., 2008

2008

-

[8]

F. E. Benth and I. C. Simonsen. The Heston stochastic volatility model in Hilbert space.Stochastic Analysis and Applications, 36(4):733–750, 2018

2018

-

[9]

Björk, G

T. Björk, G. Di Masi, Y. Kabanov, and W. Runggaldier. Towards a general theory of bond markets. Finance and Stochastics, 1(2):141–174, 1997

1997

-

[10]

Borak and R

S. Borak and R. Weron. A semiparametric factor model for electricity forward curve dynamics. Journal of Energy Markets, 1(3):3–16, 2008

2008

-

[11]

R. A. Carmona.HJM: A Unified Approach to Dynamic Models for Fixed Income, Credit and Equity Markets, pages 1–50. Springer Berlin Heidelberg, Berlin, Heidelberg, 2007

2007

-

[12]

R. A. Carmona and M. R. Tehranchi.Interest rate models: an infinite dimensional stochastic analysis perspective. Berlin: Springer, 2006

2006

-

[13]

Chatziandreou and S

K. Chatziandreou and S. Karbach. Semi-static variance-optimal hedging of covariance risk in multi- asset derivatives, 2026

2026

-

[14]

R. Cont. Modeling term structure dynamics: an infinite dimensional approach.International Journal of Theoretical and Applied Finance, 8(3):357–380, 2005

2005

-

[15]

S. Cox, S. Karbach, and A. Khedher. An infinite-dimensional affine stochastic volatility model. Mathematical Finance, 32(3):878–906, 2022

2022

-

[16]

GeneralizedFellerprocessesandMarkovianliftsofstochasticVolterra processes: the affine case.J

C.CuchieroandJ.Teichmann. GeneralizedFellerprocessesandMarkovianliftsofstochasticVolterra processes: the affine case.J. Evol. Equ., 20(4):1301–1348, 2020

2020

-

[17]

Da Prato and J

G. Da Prato and J. Zabczyk.Stochastic Equations in Infinite Dimensions, volume 152 ofEncyclo- pedia of Mathematics and its Applications. Cambridge University Press, Cambridge, second edition, 2014

2014

-

[18]

De Donno, P

M. De Donno, P. Guasoni, and M. Pratelli. Super-replication and utility maximization in large financial markets.Stochastic Processes and their Applications, 115(12):2006–2022, 2005

2006

-

[19]

De Donno and M

M. De Donno and M. Pratelli. A theory of stochastic integration for bond markets.The Annals of Applied Probability, 15(4):2773–2791, 2005

2005

-

[20]

Detering and S

N. Detering and S. Lavagnini. A class of locally state-dependent models for forward curves, 2025

2025

-

[21]

R. Douady. Yield curve smoothing and residual variance of fixed income positions. In Y. Kabanov, M. Rutkowski, and T. Zariphopoulou, editors,Inspired by Finance: The Musiela Festschrift, pages 221–256. Springer International Publishing, Cham, 2014

2014

-

[22]

Ekeland and E

I. Ekeland and E. Taflin. A theory of bond portfolios.The Annals of Applied Probability, 15(2):1260– 1305, 2005

2005

-

[23]

Filipović.Consistency problems for Heath-Jarrow-Morton interest rate models, volume 1760

D. Filipović.Consistency problems for Heath-Jarrow-Morton interest rate models, volume 1760. Berlin: Springer, 2001

2001

-

[24]

D. Frestad. Common and unique factors influencing daily swap returns in the nordic electricity market, 1997-2005.Energy Economics, 30(3):1081–1097, May 2008

1997

-

[25]

Friesen and S

M. Friesen and S. Karbach. Stationary covariance regime for affine stochastic covariance models in Hilbert spaces.Finance Stoch., 28(4):1077–1116, 2024

2024

-

[26]

J. He, S. Karbach, and A. Khedher. Pricing Options on Forwards in Function-Valued Affine Sto- chastic Volatility Models. Preprint, arXiv:2508.14813 [q-fin.MF] (2025), 2025

work page internal anchor Pith review Pith/arXiv arXiv 2025

-

[27]

Kallsen and A

J. Kallsen and A. Pauwels. Variance-optimal hedging in general affine stochastic volatility models. Advances in Applied Probability, 42(1):83–105, 2010

2010

-

[28]

S. Karbach. Heat modulated affine stochastic volatility models for forward curve dynamics.arXiv preprint arXiv:2409.13070, 2024. HEDGING MATURITY-SPECIFIC RISK IN FOR W ARD CUR VE DERIV ATIVES 27

work page internal anchor Pith review arXiv 2024

-

[29]

S. Karbach. Finite-rank approximation of affine processes on positive Hilbert-Schmidt operators.J. Math. Anal. Appl., 553(2):35, 2026. Id/No 129852

2026

-

[30]

Koekebakker and F

S. Koekebakker and F. Ollmar. Forward curve dynamics in the nordic electricity market.Managerial Finance, 31:73–94, 2005

2005

-

[31]

J. Y. Ouvrard. Représentation de martingales vectorielles de carré intégrable à valeurs dans des espaces de hilbert réels séparables.Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 33:195–208, 1975

1975

-

[32]

Peszat and J

S. Peszat and J. Zabczyk.Stochastic Partial Differential Equations with Lévy Noise. An Evolution Equation Approach, volume 113 ofEncyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 2007

2007

-

[33]

H. Pham. On quadratic hedging in continuous time.Mathematical Methods of Operations Research, 51(2):315–339, 2000

2000

-

[34]

Schweizer

M. Schweizer. A guided tour through quadratic hedging approaches. In E. Jouini, J. Cvitanic, and M. Musiela, editors,Option Pricing, Interest Rates and Risk Management, Handbooks in Mathe- matical Finance, page 538–574. Cambridge University Press, 2001

2001

-

[35]

E. Taflin. Bond market completeness and attainable contingent claims.Finance and Stochastics, 9(3):429–452, 2005

2005

-

[36]

S. Tappe. Compact embeddings for spaces of forward rate curves.Abstr. Appl. Anal., 2013:Article ID 709505, 6 pages, 2013

2013

-

[37]

Černý and J

A. Černý and J. Kallsen. On the structure of general mean-variance hedging strategies.The Annals of Probability, 35(4):1479–1531, 2007

2007

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.