Bayesian Joint Estimation of the Hurst Parameter and Volatility with Applications to Fractional Option Pricing

Pith reviewed 2026-06-30 01:14 UTC · model grok-4.3

The pith

A Bayesian framework jointly estimates the Hurst parameter and volatility to produce distributions of option prices that incorporate their uncertainty under the fractional Black-Scholes model.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

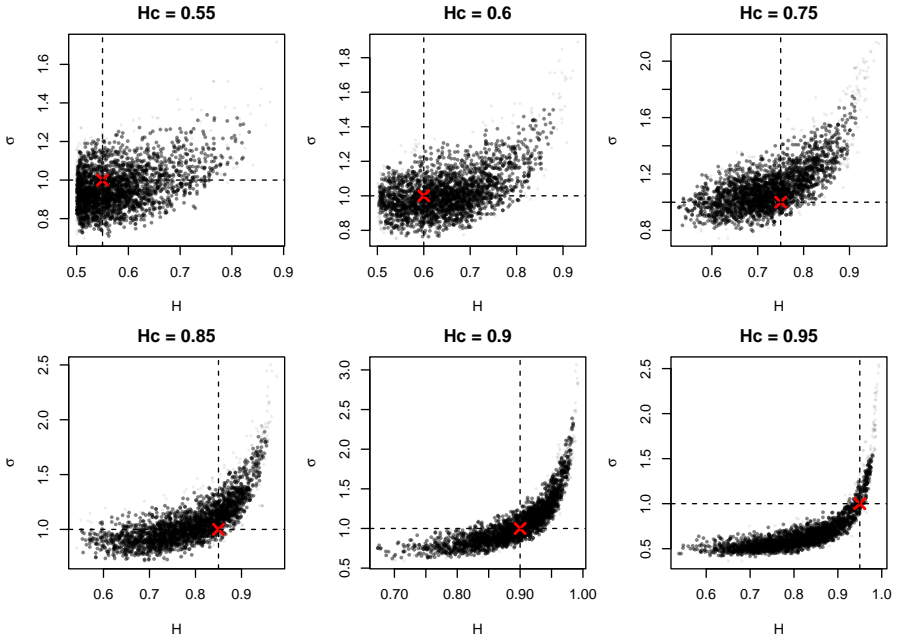

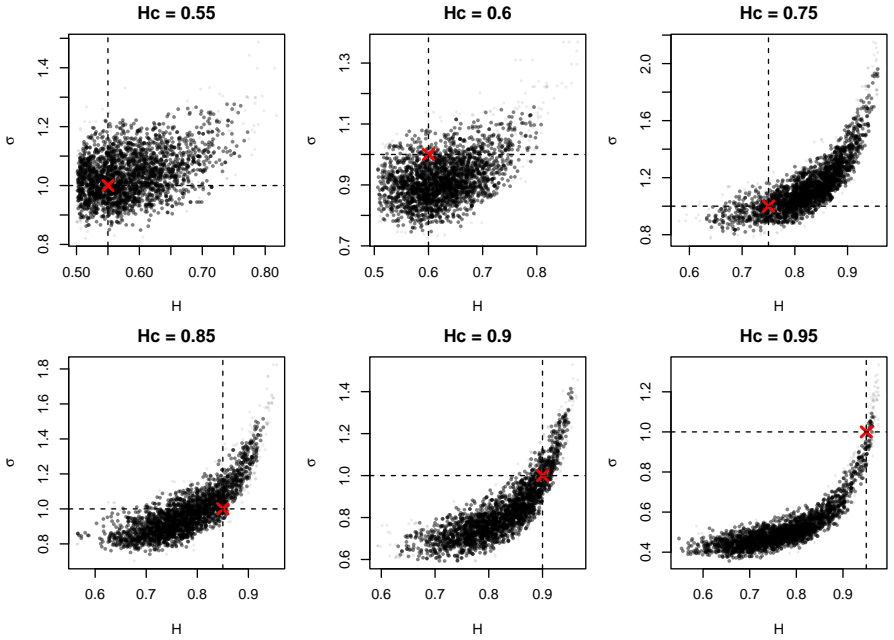

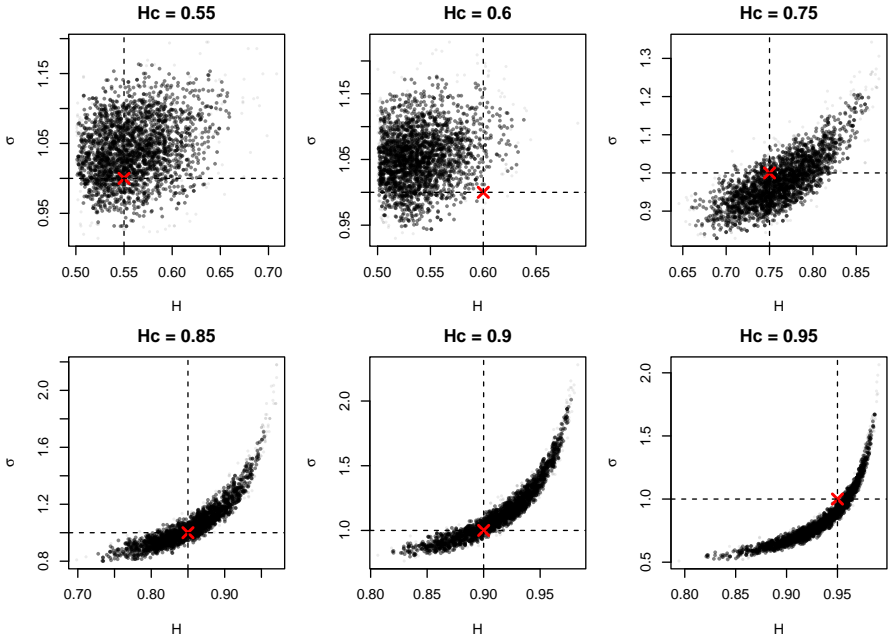

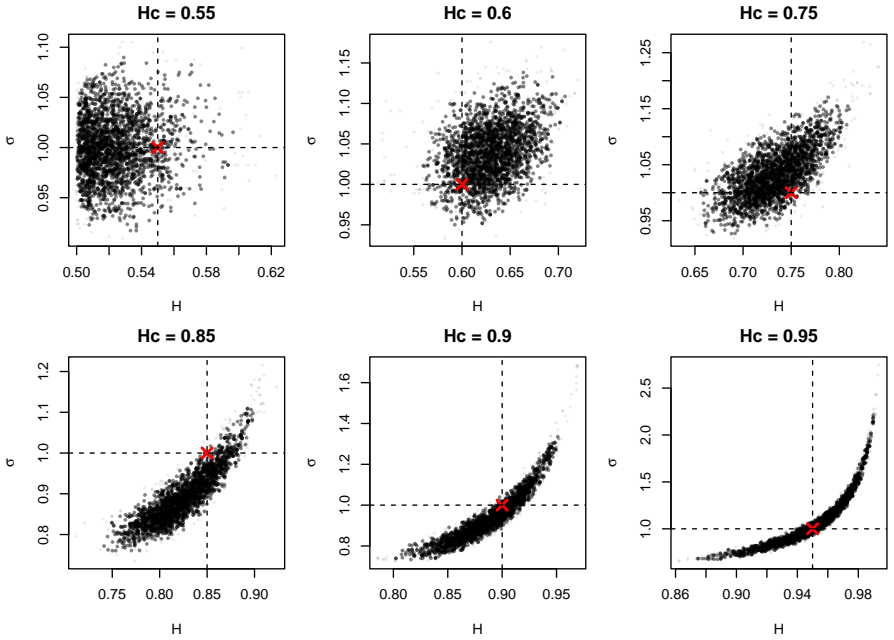

The proposed Bayesian joint inference on the Hurst parameter and volatility in fractional stochastic differential equation models allows direct propagation of posterior uncertainty into option pricing distributions under the fractional Black-Scholes model, as validated by simulations demonstrating stable inference and by empirical analysis of energy market data showing volatility-driven regime differences.

What carries the argument

The joint posterior distribution over the Hurst parameter and volatility, sampled via Bayesian methods and then used to compute a distribution of option prices by integrating the fractional Black-Scholes pricing function over the posterior.

If this is right

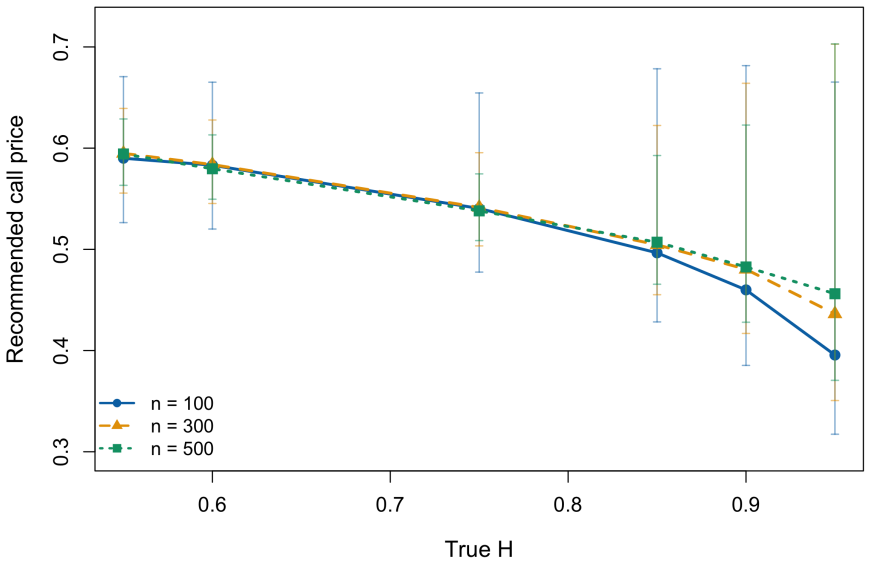

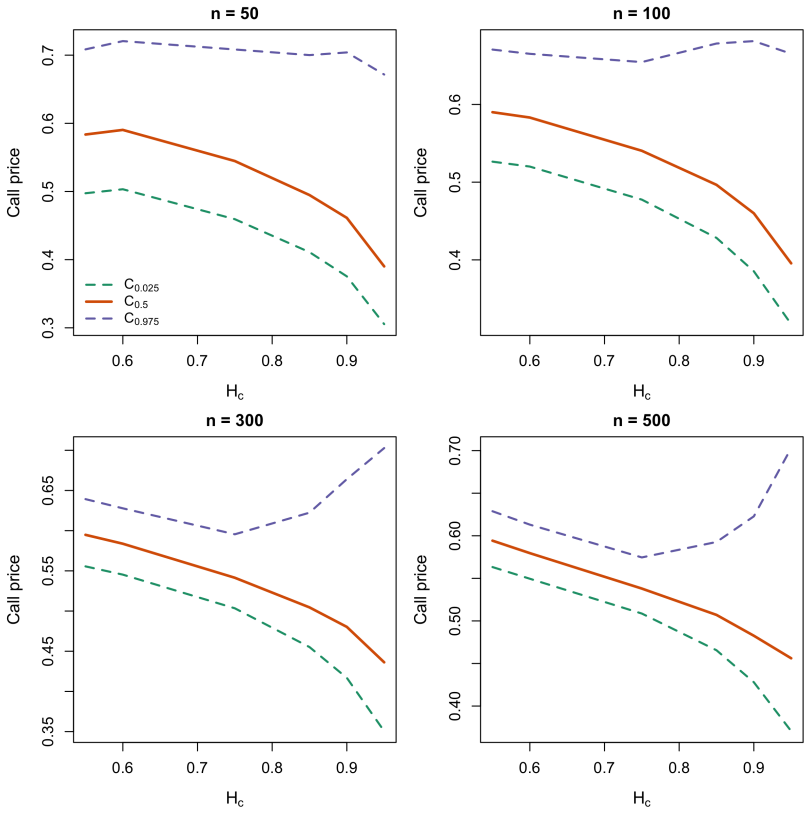

- Option prices are obtained as full posterior distributions rather than point values, reflecting parameter uncertainty.

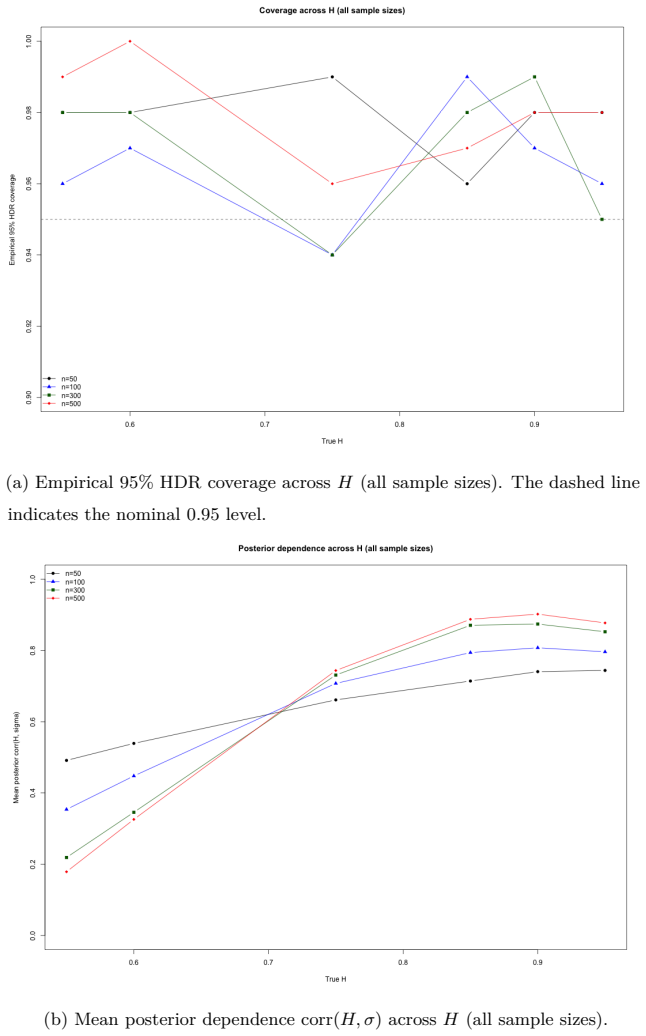

- Simulation studies confirm accurate recovery of the Hurst parameter and volatility with proper coverage of uncertainty intervals.

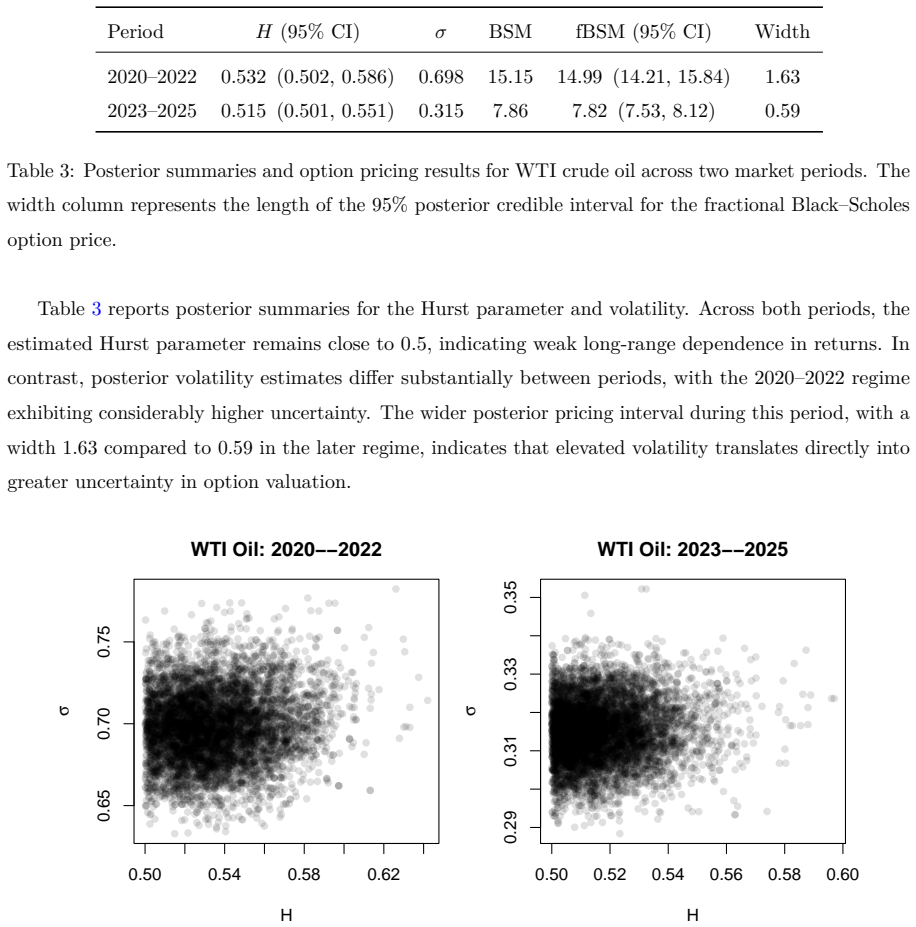

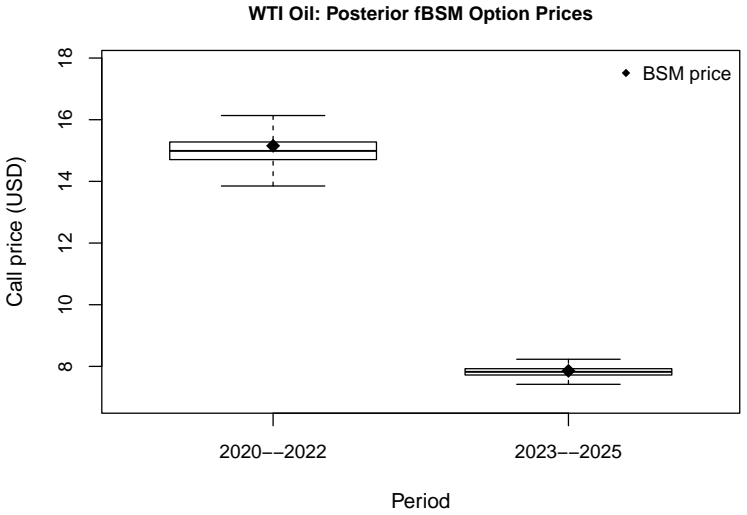

- Empirical results on WTI crude oil and natural gas suggest that differences across market regimes stem primarily from volatility changes rather than variations in long-range dependence.

- Posterior option price distributions exhibit substantial variation in pricing uncertainty depending on the market regime.

Where Pith is reading between the lines

- Risk assessment in fractional models could incorporate the full price distribution width to set capital buffers.

- The method could be tested on equity or FX data to check whether volatility dominance over Hurst effects appears in other asset classes.

- Multi-period extensions might allow the Hurst parameter itself to evolve while retaining joint Bayesian updating.

Load-bearing premise

The asset price dynamics are accurately described by a fractional Brownian motion driven by a single constant Hurst parameter across the observed period.

What would settle it

If repeated simulations show that the credible intervals for the Hurst parameter fail to contain the true value at the expected frequency, or if real-world option market prices fall consistently outside the predicted posterior distributions.

Figures

read the original abstract

Fractional Brownian motion has been widely used in financial modeling to capture long-range dependence and persistent behavior observed in asset dynamics. In the fractional Black--Scholes framework, accurate estimation of the Hurst parameter is essential, since estimation uncertainty can directly affect option pricing results. In this paper, we propose a Bayesian framework for joint inference on the Hurst parameter and volatility in fractional stochastic differential equation models. In contrast to approaches based solely on point estimation, the proposed method propagates posterior uncertainty directly into option pricing distributions under the fractional Black--Scholes model. Simulation studies are conducted across multiple values of the Hurst parameter and sample sizes to evaluate estimation accuracy, posterior coverage, and pricing uncertainty. The results demonstrate stable posterior inference and coherent uncertainty quantification for both model parameters and option prices. The methodology is further illustrated using WTI crude oil and natural gas data under different market regimes. The empirical analysis indicates that differences in market behavior are driven primarily by changes in volatility rather than strong long-range dependence, while posterior option price distributions reflect substantial variation in pricing uncertainty across regimes. These findings highlight the importance of incorporating joint parameter uncertainty in fractional financial models and demonstrate the practical value of Bayesian methods for option pricing applications.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a Bayesian framework for the joint posterior estimation of the Hurst parameter H and volatility in fractional SDE models driven by fractional Brownian motion. Posterior draws of (H, σ) are propagated through the fractional Black-Scholes formula to obtain distributions of option prices that incorporate parameter uncertainty. Simulation experiments across different H values and sample sizes are used to assess estimation accuracy, posterior coverage, and pricing uncertainty; the method is then applied to WTI crude oil and natural gas price series under different regimes, with the conclusion that regime differences are driven primarily by volatility rather than long-range dependence.

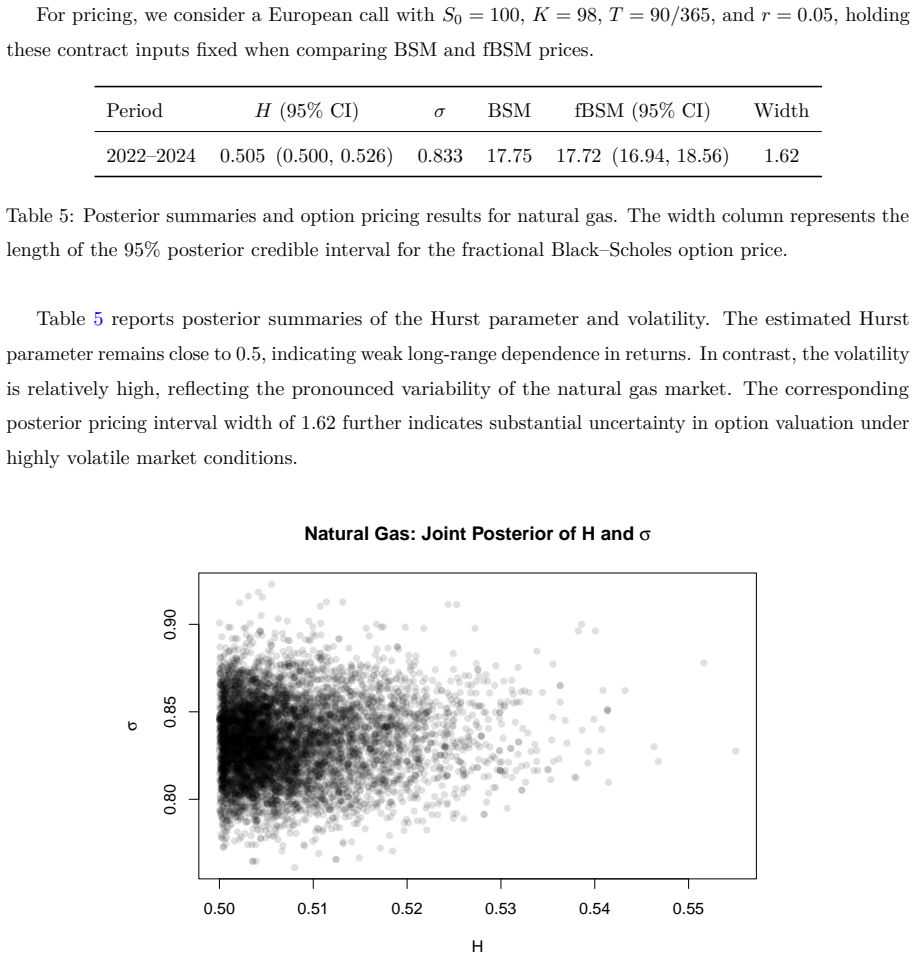

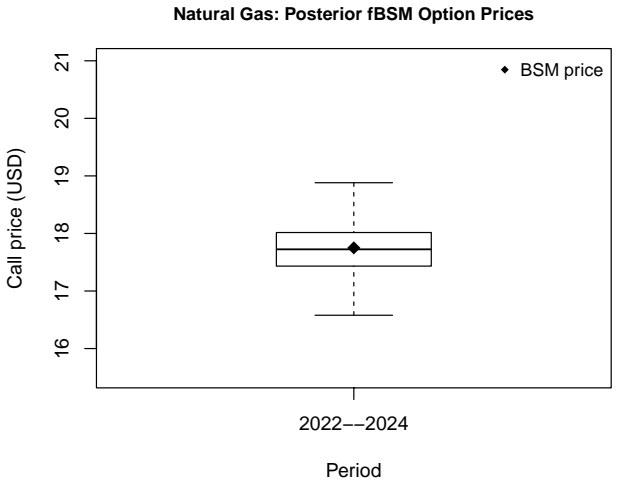

Significance. If the maintained assumption that asset dynamics are exactly described by a single-Hurst fBM holds, the direct propagation of joint posterior uncertainty into option-price distributions supplies a coherent quantification of estimation risk that is absent from point-estimate approaches. The empirical finding that volatility shifts dominate Hurst effects in the energy data would be a useful practical observation for fractional pricing applications.

major comments (2)

- The central claim that the propagated price distributions are reliable rests on the untested assumption that the data-generating process is exactly a fractional SDE with one fixed Hurst parameter. The manuscript provides no diagnostics, robustness checks, or comparisons against multifractal, locally self-similar, or regime-switching alternatives; if this assumption is violated, both the joint posterior and the resulting option-price distributions are computed under a misspecified measure even if the MCMC sampler mixes correctly.

- [Abstract] The abstract states that 'simulation studies demonstrate stable posterior inference and coherent uncertainty quantification' yet supplies no quantitative results (bias, coverage rates, interval widths, or RMSE for H and σ, or calibration checks for the price distributions). Without these metrics or the precise prior and sampling specifications, it is impossible to verify the performance claims that underwrite the method's practical value.

minor comments (1)

- Notation for the fractional SDE and the precise form of the fractional Black-Scholes pricing formula should be stated explicitly in the main text rather than assumed from the literature.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. We address the major comments below and outline the revisions we plan to make.

read point-by-point responses

-

Referee: The central claim that the propagated price distributions are reliable rests on the untested assumption that the data-generating process is exactly a fractional SDE with one fixed Hurst parameter. The manuscript provides no diagnostics, robustness checks, or comparisons against multifractal, locally self-similar, or regime-switching alternatives; if this assumption is violated, both the joint posterior and the resulting option-price distributions are computed under a misspecified measure even if the MCMC sampler mixes correctly.

Authors: We agree that the reliability of the price distributions is conditional on the correctness of the single-Hurst fractional SDE assumption. Our simulation experiments are designed to assess performance under correct specification, and the empirical application is presented as an illustration under this model. To address this concern, we will add a dedicated subsection in the discussion that explicitly states the maintained assumption, notes the absence of robustness checks against multifractal or regime-switching models, and suggests this as an avenue for future research. This will clarify the scope of the current contribution without altering the core methodology. revision: yes

-

Referee: [Abstract] The abstract states that 'simulation studies demonstrate stable posterior inference and coherent uncertainty quantification' yet supplies no quantitative results (bias, coverage rates, interval widths, or RMSE for H and σ, or calibration checks for the price distributions). Without these metrics or the precise prior and sampling specifications, it is impossible to verify the performance claims that underwrite the method's practical value.

Authors: We will revise the abstract to incorporate specific quantitative metrics from our simulation studies, including average posterior bias, coverage probabilities, and RMSE for the Hurst parameter and volatility across different H values and sample sizes. The precise prior distributions and MCMC sampling details are already provided in Section 3 of the manuscript; we will ensure the abstract references these for completeness. These changes will make the performance claims more verifiable while maintaining the abstract's brevity. revision: yes

Circularity Check

No circularity: Bayesian posterior propagation is data-driven and does not reduce to input by construction

full rationale

The paper describes a standard Bayesian joint posterior for (H, σ) under an fSDE model, followed by forward propagation of draws into fractional Black-Scholes prices. No derivation step equates a claimed prediction or uniqueness result to a fitted parameter or self-citation; the abstract and described workflow rely on external likelihood evaluation and MCMC sampling whose validity is independent of the target price distributions. The maintained modeling assumption (single-H fBM) is an external modeling choice, not a definitional tautology inside the estimation procedure itself. This is the normal non-circular case for a statistical estimation paper.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Abry, P., & Veitch, D. (1998). Wavelet analysis of long-range dependent traffic. IEEE Transactions on Information Theory, 44(1), 2--15. https://doi.org/10.1109/18.650984

-

[2]

M., Lang, G., Moulines, E., & Soulier, P

Bardet, J. M., Lang, G., Moulines, E., & Soulier, P. (2000). Wavelet estimator of long-range dependent processes. Statistical Inference for Stochastic Processes, 3(1), 85--99. https://doi.org/10.1023/A:1009953000763

-

[3]

Bennedsen, M., Lunde, A., & Pakkanen, M. S. (2022). Decoupling the short- and long-term behavior of stochastic volatility. Journal of Financial Econometrics, 20(5), 961--1006. https://doi.org/10.1093/jjfinec/nbaa049

-

[4]

Beran, J. (1994). Statistics for Long-Memory Processes. Chapman & Hall, New York

1994

-

[5]

Beskos, A., Dureau, J., & Kalogeropoulos, K. (2015). Bayesian inference for partially observed stochastic differential equations driven by fractional Brownian motion. Biometrika, 102(4), 809--827. https://doi.org/10.1093/biomet/asv051

-

[6]

Biagini, F., Hu, Y., ksendal, B., & Zhang, T. (2008). Stochastic calculus for fractional Brownian motion and applications. Springer. https://doi.org/10.1007/978-1-84628-797-8

-

[7]

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637--654. https://doi.org/10.1086/260062

-

[8]

Chen, C.-Y., Shafie, K., & Lin, Y.-K. (2017). Bayesian estimation of the Hurst parameter of fractional Brownian motion. Communications in Statistics -- Simulation and Computation, 46(6), 4760--4766. https://doi.org/10.1080/03610918.2015.1130835

-

[9]

Chopin, N., & Papaspiliopoulos, O. (2020). An Introduction to Sequential Monte Carlo. Springer. https://doi.org/10.1007/978-3-030-47845-2

-

[10]

Comte, F., & Renault, E. (1998). Long memory in continuous-time stochastic volatility models. Mathematical Finance, 8(4), 291--323. https://doi.org/10.1111/1467-9965.00057

-

[11]

Dlask, M., Kukal, J., & Vyšata, O. (2017). Bayesian approach to Hurst exponent estimation. Methodology and Computing in Applied Probability, 19(3), 973--983. https://doi.org/10.1007/s11009-017-9543-x

-

[12]

Doukhan, P., Oppenheim, G., & Taqqu, M. S. (Eds.). (2003). Theory and Applications of Long-Range Dependence. Boston, MA: Birkh\"auser

2003

-

[13]

Embrechts, P., & Maejima, M. (2002). Selfsimilar Processes. Princeton, NJ: Princeton University Press

2002

-

[14]

Gatheral, J., Jaisson, T., & Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18(6), 933--949. https://doi.org/10.1080/14697688.2017.1393551

-

[15]

H., & Van Loan, C

Golub, G. H., & Van Loan, C. F. (2013). Matrix Computations (4th ed.). Baltimore, MD: Johns Hopkins University Press

2013

-

[16]

Hu, Y., & ksendal, B. (2003). Fractional white noise calculus and applications to finance. Infinite Dimensional Analysis, Quantum Probability and Related Topics, 6(1), 1--32. https://doi.org/10.1142/S0219025703001110

-

[17]

Hurvich, C. M., Deo, R., & Brodsky, J. (1998). The mean squared error of Geweke and Porter-Hudak's estimator. Journal of Time Series Analysis, 19(1), 19--46. https://doi.org/10.1111/1467-9892.00075

-

[18]

Hyndman, R. J. (1996). Computing and graphing highest density regions. The American Statistician, 50(2), 120--126. https://doi.org/10.1080/00031305.1996.10474359

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1080/00031305.1996.10474359 1996

-

[19]

Jacquier, E., Polson, N. G., & Rossi, P. E. (1994). Bayesian analysis of stochastic volatility models. Journal of Business & Economic Statistics, 12(4), 371--389. https://doi.org/10.1080/07350015.1994.10524553

-

[20]

Makarava, N., & Holschneider, M. (2012). Estimation of the Hurst exponent from noisy data: A Bayesian approach. The European Physical Journal B, 85, 379. https://doi.org/10.1140/epjb/e2012-30221-1

-

[21]

Mandelbrot, B. B. (1971). When can price be arbitraged efficiently? A limit to the validity of the random walk and martingale models. The Review of Economics and Statistics, 53(3), 225--236. https://www.jstor.org/stable/1937966

arXiv 1971

-

[22]

Mandelbrot, B., & Van Ness, J. (1968). Fractional Brownian motions, fractional noises and applications. SIAM Review, 10(4), 422--437. https://doi.org/10.1137/1010093

-

[23]

Mangalam, M., & Likens, A. D. (2025). Precision in Brief: The Bayesian Hurst--Kolmogorov Method for the Assessment of Long-Range Temporal Correlations in Short Behavioral Time Series. Entropy, 27(5), 500. https://doi.org/10.3390/e27050500

-

[24]

Mangalam, M., Wilson, T. J., Sommerfeld, J. H., & Likens, A. D. (2025). Optimizing a Bayesian method for estimating the Hurst exponent in behavioral sciences. Axioms, 14(6), 421. https://doi.org/10.3390/axioms14060421

-

[25]

Merton, R. C. (1973). Theory of rational option pricing. Bell Journal of Economics, 4(1), 141--183. https://doi.org/10.2307/3003143

-

[26]

Murphy, K. P. (2012). Machine learning: A probabilistic perspective. MIT Press. https://mitpress.mit.edu/9780262018029

arXiv 2012

-

[27]

Njomen Njomen, D. A., & Djeutcha, E. (2019). Solving Black--Scholes equation using standard fractional Brownian motion. Journal of Mathematics Research, 11(2), 142--149. https://doi.org/10.5539/jmr.v11n2p142

-

[28]

Necula, C. (2002). Option Pricing in a Fractional Brownian Motion Environment. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1286833

-

[29]

Pramanik, P., Boone, E. L., & Ghanam, R. A. (2024). Parametric estimation in fractional stochastic differential equation. Stats, 7(3), 745--760. https://doi.org/10.3390/stats7030045

-

[30]

Rogers, L. C. G. (1997). Arbitrage with fractional Brownian motion. Mathematical Finance, 7(1), 95--105. https://doi.org/10.1111/1467-9965.00025

-

[31]

Robinson, P. M. (1995). Gaussian semiparametric estimation of long range dependence. Annals of Statistics, 23(5), 1630--1661. https://doi.org/10.1214/aos/1176324317

-

[32]

Sagor, H., Boone, E. L., & Ghanam, R. A. (2025). Bias-corrected method of moments estimation of the Hurst parameter for improved option pricing under the fractional Black--Scholes model. Journal of Risk and Financial Management, 18(10), 588. https://doi.org/10.3390/jrfm18100588

-

[33]

Samorodnitsky, G., & Taqqu, M. S. (1994). Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. New York, NY: Chapman & Hall. https://doi.org/10.1201/9780203738818

-

[34]

S., Teverovsky, V., & Willinger, W

Taqqu, M. S., Teverovsky, V., & Willinger, W. (1995). Estimators for long-range dependence: An empirical study. Fractals, 3(4), 785--798. https://doi.org/10.1142/S0218348X95000692

-

[35]

Tsionas, M. G. (2021). Bayesian analysis of static and dynamic Hurst parameters under stochastic volatility. Physica A: Statistical Mechanics and its Applications, 567, 125647. https://doi.org/10.1016/j.physa.2020.125647

-

[36]

Weron, R. (2002). Estimating long-range dependence: Finite sample properties and confidence intervals. Physica A: Statistical Mechanics and its Applications, 312(1--2), 285--299. https://doi.org/10.1016/S0378-4371(02)00961-5

-

[37]

Zhang, H.-Y., Feng, Z.-Q., Feng, S.-Y., & Zhou, Y. (2024). Typical algorithms for estimating Hurst exponent of time sequence: A comprehensive review with pseudo-code implementations. IEEE Access, 12, 185528--185556. https://doi.org/10.1109/ACCESS.2024.3512542

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.