Distributional Portfolio Optimization (DPO): A Unified Framework for Distributions over Weights, Returns, and Parameters

Pith reviewed 2026-06-28 23:32 UTC · model grok-4.3

The pith

A joint coupling of weights, returns and parameters unifies multiple portfolio optimization approaches.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We call distributional portfolio optimization (DPO) the unified framework in which weights, returns, and parameters are all modeled as probability measures, organized around the joint coupling Gamma_theta(dw,dr) and its marginal triple (W,R,P). The contribution is synthetic and structural: we organize Bayesian, robust, chance-constrained, stochastic-allocation, and distributional reinforcement-learning portfolio methods through this coupling and prove boundary results connecting them, including a portfolio specialization of Wasserstein-CVaR duality, a static no-randomization theorem, a Bayesian credible-radius calibration of Wasserstein DRO, a Gaussian-isotropic second-order conservatism bou

What carries the argument

the joint coupling Gamma_theta(dw,dr) and its marginal triple (W,R,P) that links distributions over weights, returns, and parameters

If this is right

- A portfolio specialization of Wasserstein-CVaR duality holds under the framework.

- A static no-randomization theorem is established.

- Wasserstein DRO can be calibrated using Bayesian credible radii.

- Gaussian-isotropic second-order conservatism bounds apply.

- A risk-shifted distributional Bellman contraction governs the RL case.

Where Pith is reading between the lines

- The credible-radius approach could reduce the need for hold-out data in portfolio calibration across factor models.

- Connections between methods may enable hybrid algorithms that combine elements from Bayesian and robust optimization.

- Sample complexity results indicate that smoother distribution boundaries lead to faster convergence rates for Wasserstein distances.

Load-bearing premise

The joint coupling Gamma_theta(dw,dr) and its marginal triple (W,R,P) can serve as a complete organizing structure for Bayesian, robust, chance-constrained, stochastic-allocation, and distributional reinforcement-learning portfolio methods without material loss of structure or applicability for any of them.

What would settle it

A demonstration that any one of the listed portfolio methods cannot be faithfully represented by the joint coupling without losing key properties would falsify the central unification claim.

Figures

read the original abstract

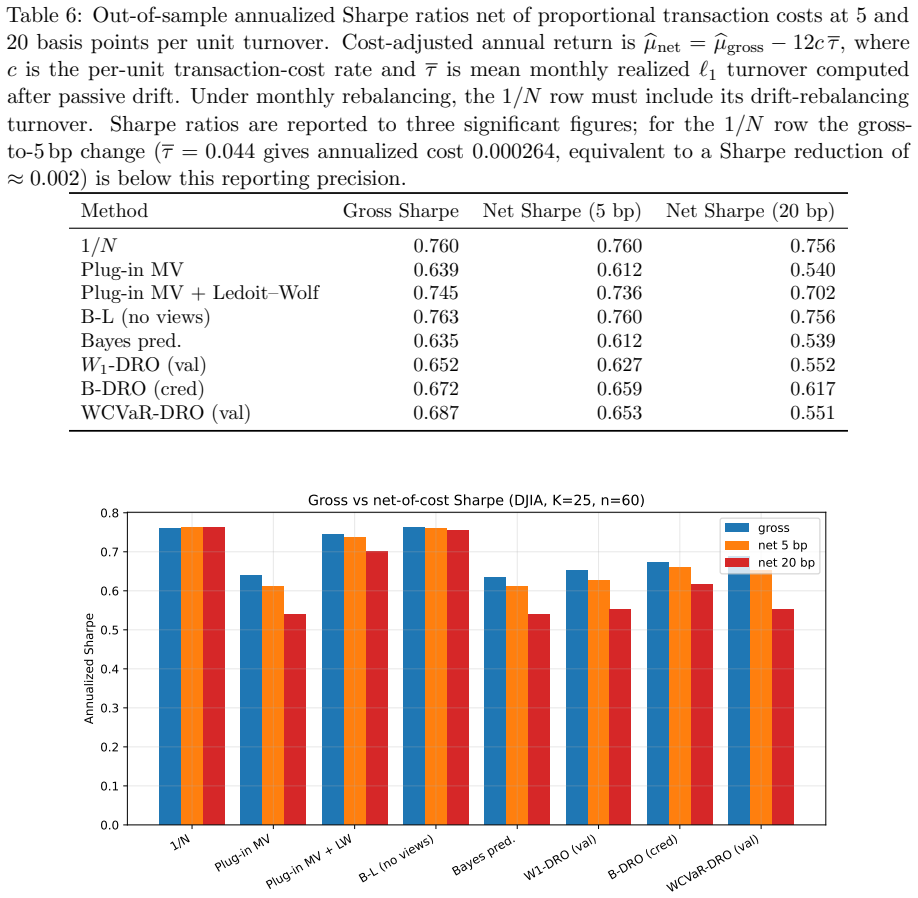

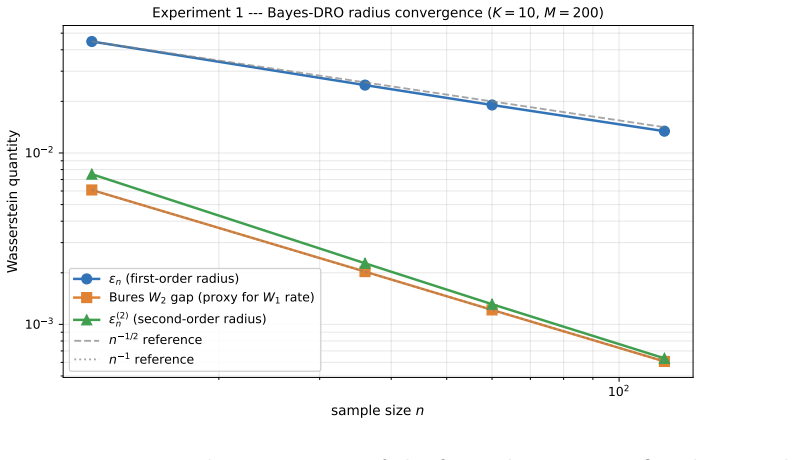

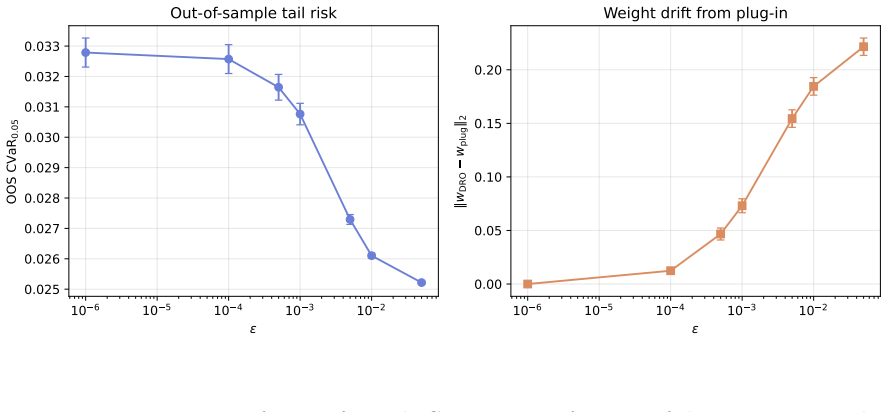

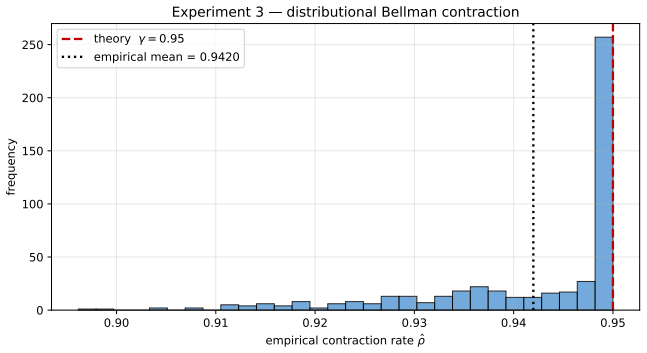

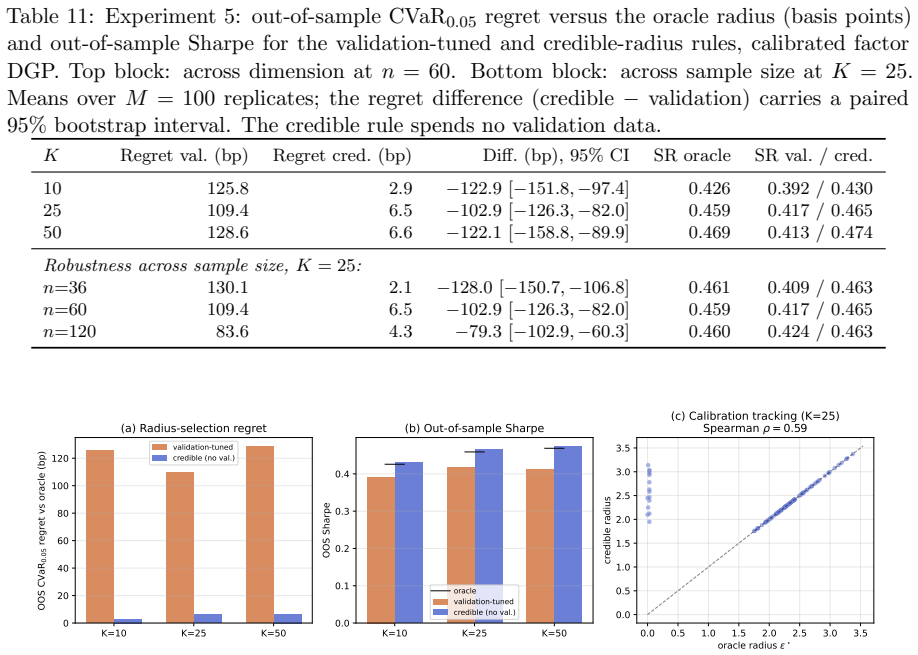

Classical portfolio optimization treats expected returns, covariances, and allocations as deterministic. Modern practice replaces at least one by a distribution: a posterior over parameters, a law of future returns, a stochastic allocation policy, or a distributional-robustness set. We call distributional portfolio optimization (DPO) the unified framework in which weights, returns, and parameters are all modeled as probability measures, organized around the joint coupling Gamma_theta(dw,dr) and its marginal triple (W,R,P). The contribution is synthetic and structural: we organize Bayesian, robust, chance-constrained, stochastic-allocation, and distributional reinforcement-learning portfolio methods through this coupling and prove boundary results connecting them, including a portfolio specialization of Wasserstein-CVaR duality, a static no-randomization theorem, a Bayesian credible-radius calibration of Wasserstein DRO, a Gaussian-isotropic second-order conservatism bound, a conditional two-sided rate W_1 = Theta(n^{-(1+alpha)/2}) governed by the local boundary Holder exponent alpha in [0,1], and a risk-shifted distributional Bellman contraction. A controlled experiment shows that across factor models at K in {10,25,50}, the credible-radius rule lands within 3-7 bp of the oracle out-of-sample tail risk and beats a 24-month validation-tuned radius while spending no validation data. On a K=25 DJIA backtest, equal-weight, no-view Black-Litterman, and Ledoit-Wolf shrinkage attain higher Sharpe than every distributional method; the operational claim is therefore confined to calibration-without-validation and turnover, not raw-return dominance.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes Distributional Portfolio Optimization (DPO) as a unified framework in which weights, returns, and parameters are modeled as probability measures, organized around the joint coupling Gamma_theta(dw,dr) and its marginal triple (W,R,P). It synthesizes Bayesian, robust, chance-constrained, stochastic-allocation, and distributional reinforcement-learning methods through this structure and proves several boundary results, including a portfolio specialization of Wasserstein-CVaR duality, a static no-randomization theorem, a Bayesian credible-radius calibration of Wasserstein DRO, a Gaussian-isotropic second-order conservatism bound, a conditional two-sided rate W_1 = Theta(n^{-(1+alpha)/2}) governed by the local boundary Holder exponent alpha, and a risk-shifted distributional Bellman contraction. A controlled experiment across factor models (K in {10,25,50}) shows the credible-radius rule approximates oracle out-of-sample tail risk within 3-7 bp and outperforms a 24-month validation-tuned radius without using validation data. On a K=25 DJIA backtest, equal-weight, no-view Black-Litterman, and Ledoit-Wolf shrinkage attain higher Sharpe ratios than distributional methods; the operational claim is limited to calibration-without-validation and turnover.

Significance. If the derivations and experimental controls hold, the paper delivers a synthetic unification of disparate portfolio optimization approaches under a common distributional coupling, together with several explicit boundary results that connect them. The concrete experimental demonstration of a validation-free calibration rule that stays within a few basis points of oracle tail risk is a practical contribution. The manuscript explicitly notes that distributional methods do not dominate traditional approaches on Sharpe ratio in the reported backtest, which strengthens the scope of the claims. No machine-checked proofs or open code are referenced in the provided text.

minor comments (3)

- The abstract and introduction would benefit from an explicit statement of the precise sense in which the joint coupling Gamma_theta serves as a 'complete organizing structure' for all listed methods (Bayesian, robust, chance-constrained, etc.), including any limitations on applicability.

- The experiment section should report the precise definition of the 'oracle' tail-risk benchmark and the number of Monte Carlo replications used to obtain the 3-7 bp figure, to allow direct assessment of statistical variability.

- Notation for the marginal triple (W,R,P) and its relation to the coupling Gamma_theta(dw,dr) is introduced without a dedicated diagram or table; a small schematic would improve readability for readers unfamiliar with the coupling construction.

Simulated Author's Rebuttal

We thank the referee for the thorough summary and the recommendation of minor revision. The report correctly identifies the synthetic and structural contributions of the DPO framework, the boundary results, and the scope of the empirical claims (including the explicit note that distributional methods do not dominate on Sharpe ratio in the reported backtest). We address the single observation raised in the report below.

read point-by-point responses

-

Referee: No machine-checked proofs or open code are referenced in the provided text.

Authors: We agree that reproducibility would be strengthened by open code. In the revised manuscript we will add a dedicated reproducibility statement with a permanent link to a public repository containing (i) the full Python implementation of the factor-model experiments (K=10,25,50), (ii) the DJIA backtest, and (iii) the credible-radius calibration routine. Regarding machine-checked proofs, the derivations appear in the appendix and rely on standard results from optimal transport and distributionally robust optimization; while we have not employed a proof assistant, we believe the arguments are self-contained. We are prepared to supply any additional intermediate steps the referee may request. revision: yes

Circularity Check

No significant circularity detected

full rationale

The abstract and claims describe a synthetic unification of portfolio methods via the joint coupling Gamma_theta(dw,dr) and marginal triple (W,R,P), plus boundary results (Wasserstein-CVaR duality, no-randomization theorem, credible-radius calibration, conservatism bound, W_1 rate, Bellman contraction) and an experiment. No equations, self-citations, or derivations are provided that reduce any claimed prediction or result to its inputs by construction (e.g., no fitted parameter renamed as prediction, no self-definitional loop, no load-bearing self-citation chain). The credible-radius calibration is noted as Bayesian but exhibits no visible reduction to a fitted quantity on the target metric. The framework is presented as an organizing structure with independent content and external experimental validation, qualifying as self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- standard math Wasserstein distance and CVaR satisfy duality in the portfolio setting

invented entities (2)

-

Joint coupling Gamma_theta(dw,dr)

no independent evidence

-

Marginal triple (W,R,P)

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Spectral measures of risk: A coherent representation of subjective risk aversion

Carlo Acerbi. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking and Finance, 26 0 (7): 0 1505--1518, 2002

2002

-

[2]

Entropic value-at-risk: A new coherent risk measure

Amir Ahmadi-Javid. Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Applications, 155 0 (3): 0 1105--1123, 2012

2012

-

[3]

u rich. Birkh \

Luigi Ambrosio, Nicola Gigli, and Giuseppe Savar \'e . Gradient Flows in Metric Spaces and in the Space of Probability Measures. Lectures in Mathematics ETH Z \"u rich. Birkh \"a user, 2nd edition, 2008

2008

-

[4]

Coherent measures of risk

Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical Finance, 9 0 (3): 0 203--228, 1999

1999

-

[5]

Bayesian portfolio analysis

Doron Avramov and Guofu Zhou. Bayesian portfolio analysis. Annual Review of Financial Economics, 2: 0 25--47, 2010

2010

-

[6]

Markov decision processes with average-value-at-risk criteria

Nicole B\"auerle and Jonathan Ott. Markov decision processes with average-value-at-risk criteria. Mathematical Methods of Operations Research, 74 0 (3): 0 361--379, 2011

2011

-

[7]

Bellemare, Will Dabney, and R\'emi Munos

Marc G. Bellemare, Will Dabney, and R\'emi Munos. A distributional perspective on reinforcement learning. In Proceedings of the 34th International Conference on Machine Learning (ICML), 2017

2017

-

[8]

Robust solutions of optimization problems affected by uncertain probabilities

Aharon Ben-Tal, Dick Den Hertog, Anja De Waegenaere, Bertrand Melenberg, and Gijs Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59 0 (2): 0 341--357, 2013

2013

-

[9]

Kolm, and Gordon Ritter

Jerome Benveniste, Petter N. Kolm, and Gordon Ritter. Untangling universality and dispelling myths in mean--variance optimization. The Journal of Portfolio Management, 50 0 (8): 0 90--116, 2024

2024

-

[10]

On the bures--wasserstein distance between positive definite matrices

Rajendra Bhatia, Tanvi Jain, and Yongdo Lim. On the bures--wasserstein distance between positive definite matrices. Expositiones Mathematicae, 37 0 (2): 0 165--191, 2019

2019

-

[11]

Probability and Measure

Patrick Billingsley. Probability and Measure. Wiley, anniversary edition, 2012

2012

-

[12]

Global portfolio optimization

Fischer Black and Robert Litterman. Global portfolio optimization. Financial Analysts Journal, 48 0 (5): 0 28--43, 1992

1992

-

[13]

V. I. Bogachev. Measure Theory. Springer, 2007

2007

-

[14]

Brown, William Goetzmann, Roger G

Stephen J. Brown, William Goetzmann, Roger G. Ibbotson, and Stephen A. Ross. Survivorship bias in performance studies. Review of Financial Studies, 5 0 (4): 0 553--580, 1992

1992

-

[15]

Random portfolios for evaluating trading strategies

Patrick Burns. Random portfolios for evaluating trading strategies. Technical report, Burns Statistics, 2007

2007

-

[16]

Giuseppe Calafiore and Marco C. Campi. Uncertain convex programs: Randomized solutions and confidence levels. Mathematical Programming, 102 0 (1): 0 25--46, 2005

2005

-

[17]

Campi and Simone Garatti

Marco C. Campi and Simone Garatti. The exact feasibility of randomized solutions of uncertain convex programs. SIAM Journal on Optimization, 19 0 (3): 0 1211--1230, 2008

2008

-

[18]

Abraham Charnes and William W. Cooper. Chance-constrained programming. Management Science, 6 0 (1): 0 73--79, 1959

1959

-

[19]

Alexander S. Cherny. Weighted v@r and its properties. Finance and Stochastics, 10 0 (3): 0 367--393, 2006

2006

-

[20]

Implicit quantile networks for distributional reinforcement learning

Will Dabney, Georg Ostrovski, David Silver, and R\'emi Munos. Implicit quantile networks for distributional reinforcement learning. In Proceedings of the 35th International Conference on Machine Learning (ICML), 2018 a

2018

-

[21]

Bellemare, and R\'emi Munos

Will Dabney, Mark Rowland, Marc G. Bellemare, and R\'emi Munos. Distributional reinforcement learning with quantile regression. In AAAI Conference on Artificial Intelligence, 2018 b

2018

-

[22]

Distributionally robust optimization under moment uncertainty with application to data-driven problems

Erick Delage and Yinyu Ye. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 58 0 (3): 0 595--612, 2010

2010

-

[23]

Optimal versus naive diversification: How inefficient is the 1/n portfolio strategy? Review of Financial Studies, 22 0 (5): 0 1915--1953, 2009

Victor DeMiguel, Lorenzo Garlappi, and Raman Uppal. Optimal versus naive diversification: How inefficient is the 1/n portfolio strategy? Review of Financial Studies, 22 0 (5): 0 1915--1953, 2009

1915

-

[24]

Stochastic Finance: An Introduction in Discrete Time

Hans F\"ollmer and Alexander Schied. Stochastic Finance: An Introduction in Discrete Time. De Gruyter, 3 edition, 2011

2011

-

[25]

On the rate of convergence in Wasserstein distance of the empirical measure

Nicolas Fournier and Arnaud Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162 0 (3-4): 0 707--738, 2015

2015

-

[26]

On a formula for the L^2 Wasserstein metric between measures on Euclidean and Hilbert spaces

Matthias Gelbrich. On a formula for the L^2 Wasserstein metric between measures on Euclidean and Hilbert spaces. Mathematische Nachrichten, 147 0 (1): 0 185--203, 1990

1990

-

[27]

Horowitz, and Bing-Yi Jing

Peter Hall, Joel L. Horowitz, and Bing-Yi Jing. On blocking rules for the bootstrap with dependent data. Biometrika, 82 0 (3): 0 561--574, 1995

1995

-

[28]

Bayes--stein estimation for portfolio analysis

Philippe Jorion. Bayes--stein estimation for portfolio analysis. Journal of Financial and Quantitative Analysis, 21 0 (3): 0 279--292, 1986

1986

-

[29]

Joseph B. Kadane. Prime time for Bayes . Controlled Clinical Trials, 16 0 (5): 0 313--318, 1995

1995

-

[30]

B. J. K. Kleijn and A. W. van der Vaart. The Bernstein--von-Mises theorem under misspecification. Electronic Journal of Statistics, 6: 0 354--381, 2012

2012

-

[31]

On law-invariant coherent risk measures

Shigeo Kusuoka. On law-invariant coherent risk measures. Advances in Mathematical Economics, 3: 0 83--95, 2001

2001

-

[32]

Improved estimation of the covariance matrix of stock returns with an application to portfolio selection

Olivier Ledoit and Michael Wolf. Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10 0 (5): 0 603--621, 2003

2003

-

[33]

A well-conditioned estimator for large-dimensional covariance matrices

Olivier Ledoit and Michael Wolf. A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88 0 (2): 0 365--411, 2004

2004

-

[34]

Building diversified portfolios that outperform out of sample

Marcos L\'opez de Prado. Building diversified portfolios that outperform out of sample. Journal of Portfolio Management, 42 0 (4): 0 59--69, 2016

2016

-

[35]

Portfolio selection

Harry Markowitz. Portfolio selection. Journal of Finance, 7 0 (1): 0 77--91, 1952

1952

-

[36]

Richard O. Michaud. Efficient Asset Management. Harvard Business School Press, 1998

1998

-

[37]

Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations

Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171 0 (1-2): 0 115--166, 2018

2018

-

[38]

Return-adjusted hierarchical risk parity and Schur portfolios: A comprehensive theoretical and empirical study, July 2025

Miquel Noguer i Alonso. Return-adjusted hierarchical risk parity and Schur portfolios: A comprehensive theoretical and empirical study, July 2025. Available at SSRN: https://ssrn.com/abstract=5370624

2025

-

[39]

Reinforcement learning portfolio optimization ( RLPO ): From Markowitz to risk-sensitive control, March 2026

Miquel Noguer i Alonso. Reinforcement learning portfolio optimization ( RLPO ): From Markowitz to risk-sensitive control, March 2026. Available at SSRN: https://ssrn.com/abstract=6447220

2026

-

[40]

Politis, and Halbert White

Andrew Patton, Dimitris N. Politis, and Halbert White. Correction to ``automatic block-length selection for the dependent bootstrap'' by d. politis and h. white. Econometric Reviews, 28 0 (4): 0 372--375, 2009

2009

-

[41]

Pflug and Alois Pichler

Georg Ch. Pflug and Alois Pichler. Multistage Stochastic Optimization. Springer Series in Operations Research and Financial Engineering. Springer International Publishing, Cham, 2014

2014

-

[42]

Politis and Joseph P

Dimitris N. Politis and Joseph P. Romano. The stationary bootstrap. Journal of the American Statistical Association, 89 0 (428): 0 1303--1313, 1994

1994

-

[43]

Polson and Bernard T

Nicholas G. Polson and Bernard T. Tew. Bayesian portfolio selection: An empirical analysis of the S&P 500 index 1970--1996. Journal of Business and Economic Statistics, 18 0 (2): 0 164--173, 2000

1970

-

[44]

Stochastic Programming

Andr\'as Pr\'ekopa. Stochastic Programming. Kluwer Academic Publishers, 1995

1995

-

[45]

Tyrrell Rockafellar and Stanislav Uryasev

R. Tyrrell Rockafellar and Stanislav Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2 0 (3): 0 21--41, 2000

2000

-

[46]

Risk-averse dynamic programming for Markov decision processes

Andrzej Ruszczy\'nski. Risk-averse dynamic programming for Markov decision processes. Mathematical Programming, 125 0 (2): 0 235--261, 2010

2010

-

[47]

A. W. van der Vaart. Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 2000

2000

-

[48]

Optimal Transport: Old and New

C\'edric Villani. Optimal Transport: Old and New. Springer, 2009

2009

-

[49]

Wainwright

Martin J. Wainwright. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2019

2019

-

[50]

Shaun S. Wang. A class of distortion operators for pricing financial and insurance risks. Journal of Risk and Insurance, 67 0 (1): 0 15--36, 2000

2000

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.