Anticipatory Portfolio Optimization

Pith reviewed 2026-06-28 06:57 UTC · model grok-4.3

The pith

Anticipatory portfolio optimization separates the control gap into an information trace plus one inverse-precision norm that expands to impact, forecast, and interaction terms.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The main result is a stacked finite-horizon LQG decomposition: information, forecast, and impact combine into an information trace plus one inverse-precision norm, whose expansion yields the impact term, forecast term, and signed forecast-impact interaction resolved by sharp angle bounds and an orthogonal nonnegative projection identity. For log utility under initial enlargement, value is the information-drift energy one-half E integral alpha_t squared dt, equivalently mutual information or relative entropy. In mean-variance form, signal value is one over two gamma times trace of Sigma inverse Omega. Permanent impact changes the price-taking allocation theta_na equals (Lambda plus gamma Sigm

What carries the argument

The stacked finite-horizon LQG decomposition that combines information, forecast, and impact into an information trace plus one inverse-precision norm whose expansion isolates the three channels.

If this is right

- Permanent impact replaces the naive allocation theta_na = (Lambda + gamma Sigma)^{-1} mu with the anticipatory allocation theta_an = (2 Lambda + gamma Sigma)^{-1} mu.

- Under initial enlargement with log utility the value of anticipation equals one-half E integral alpha_t^2 dt, equivalently mutual information.

- In mean-variance form the signal value equals one over two gamma times tr(Sigma^{-1} Omega).

- The stationary extension produces an infinite-horizon Lyapunov trace for impact anticipation once information covariance is endogenized via Kalman filtering.

- The penalty term one-half tr(H^{-1} Sigma_epsilon) is zero for vacuous anticipation and negative for misspecified anticipation.

Where Pith is reading between the lines

- The decomposition supplies an explicit way to compare the cost of using an incorrect model versus the benefit of using a richer one inside any LQG control problem.

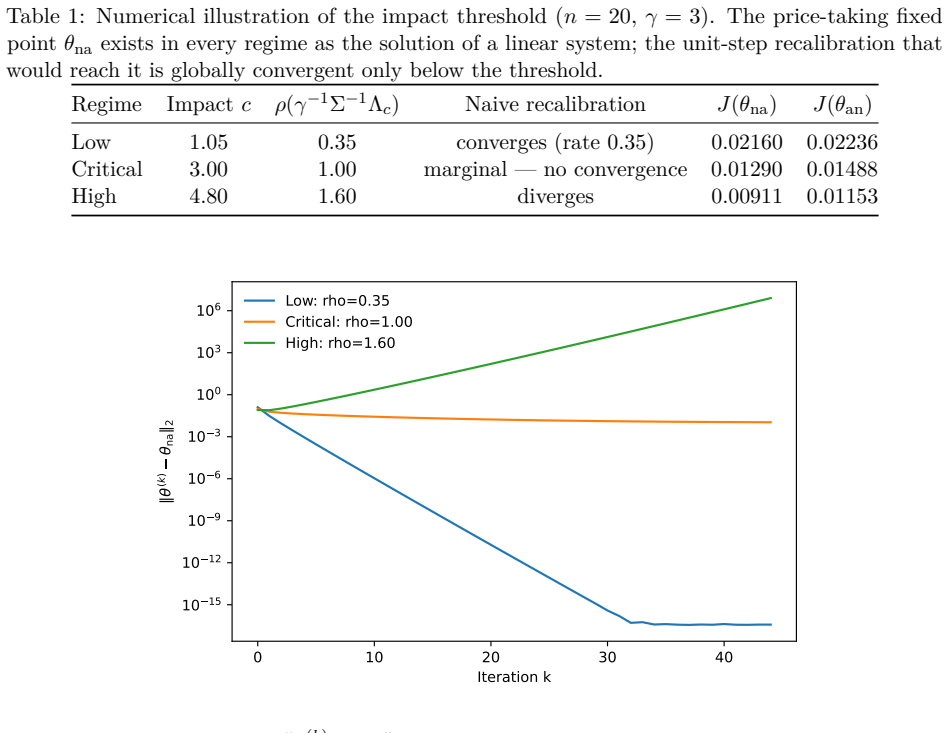

- The spectral phase transition identified for naive recalibration under impact suggests a threshold beyond which recalibration without anticipation becomes strictly dominated.

- Because the projection identity resolves the signed interaction term, the same geometry may separate channels in other linear-quadratic problems that mix information and control.

- Endogenizing the information covariance via the Kalman filter opens a route to adaptive versions in which the filtration itself is learned from returns.

Load-bearing premise

The derivations assume linear-quadratic-Gaussian dynamics and either log or mean-variance utility so that the value functions remain quadratic and the control gap admits an exact trace decomposition.

What would settle it

A direct numerical check, under the stated LQG dynamics and quadratic utility, that the observed control gap between the anticipatory controller and the myopic estimator fails to equal the information trace plus inverse-precision norm.

Figures

read the original abstract

A portfolio is \emph{anticipatory} when its optimizer acts on a richer model than the myopic, price-taking estimator used to calibrate it. Enrichment may be informational, via enlarged filtrations; dynamic, via horizon forecasts; or performative, via the deployment law induced by market impact. We give a decision-theoretic definition for all three cases and measure anticipation by the realized control gap between enriched controller and restricted estimator. The same quadratic geometry separates information, planning value, impact correction, and overfitting. For log utility under initial enlargement, value is the information-drift energy $\frac12\mathbb{E} \int_0^T\alpha_t^2\,dt$, equivalently mutual information or relative entropy. In mean-variance form, signal value is $\frac{1}{2\gamma}{\rm tr}(\Sigma^{-1}\Omega)$. Dynamic forecast anticipation gives a finite-horizon quadratic premium in the forecast stack, while permanent impact changes the price-taking allocation $\theta_{\rm na} =(\Lambda+\gamma\Sigma)^{-1}\mu$ into $\theta_{\rm an} = (2\Lambda+\gamma\Sigma)^{-1}\mu$ and reveals a spectral phase transition for naive recalibration. The main result is a stacked finite-horizon LQG decomposition: information, forecast, and impact combine into an information trace plus one inverse-precision norm, whose expansion yields the impact term, forecast term, and signed forecast-impact interaction. Sharp angle bounds and an orthogonal nonnegative projection identity resolve the signed term. The stationary extension endogenizes information covariance as Kalman error reduction and carries impact anticipation to an infinite-horizon Lyapunov trace with transaction costs. Finally, the penalty $\frac{1}{2}{\rm tr}(H^{-1}\Sigma_\varepsilon)$ shows that correctly specified anticipation creates value, vacuous anticipation has zero value, and misspecified anticipation is harmful when estimated structure is optimized as true.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper defines anticipatory portfolios as those where the optimizer employs a richer model (informational via enlarged filtrations, dynamic via forecasts, or performative via market impact) than the myopic price-taking estimator. It measures anticipation via the control gap and claims that quadratic geometry separates the channels. For log utility the value is the information-drift energy ½E∫α_t² dt; for mean-variance it is (1/(2γ))tr(Σ^{-1}Ω). Explicit allocations are given as θ_na=(Λ+γΣ)^{-1}μ and θ_an=(2Λ+γΣ)^{-1}μ with a spectral phase transition under impact. The central claim is a stacked finite-horizon LQG decomposition into an information trace plus one inverse-precision norm, with the signed forecast-impact interaction resolved by sharp angle bounds and an orthogonal nonnegative projection identity. The stationary extension endogenizes covariance via Kalman filtering and yields a Lyapunov trace; the penalty ½tr(H^{-1}Σ_ε) is used to argue that correctly specified anticipation creates value while misspecified anticipation harms.

Significance. If the LQG decomposition and projection identity hold, the work supplies a unified geometric account of three anticipation channels with closed-form allocations and a phase-transition prediction. The explicit formulas θ_na and θ_an, the Kalman-Lyapunov stationary extension, and the separation into independent trace/norm terms are concrete strengths that could guide information-acquisition and impact-aware strategies. The paper is credited for deriving the allocations directly from the quadratic geometry and for endogenizing information covariance.

major comments (3)

- [Main result (stacked finite-horizon LQG decomposition)] Main result (stacked finite-horizon LQG decomposition): the additive separation into information trace plus inverse-precision norm, and the resolution of the signed interaction, rest on the control gap admitting an exact trace decomposition. This requires value functions to remain quadratic under the enriched anticipatory dynamics. The derivation of θ_an=(2Λ+γΣ)^{-1}μ from the impact model must be shown to preserve this quadratic structure; otherwise the claimed separation of the three channels does not follow.

- [Resolution of the signed forecast-impact interaction] Resolution of the signed forecast-impact interaction: the orthogonal nonnegative projection identity invoked to separate the signed term is load-bearing for the additive decomposition. The manuscript must state this identity explicitly and verify that it is independent of the model parameters rather than constructed from them, as the latter would render the separation tautological.

- [Penalty term ½tr(H^{-1}Σ_ε)] Penalty term ½tr(H^{-1}Σ_ε): the claim that this term demonstrates harm from misspecified anticipation is presented as an independent result. It is unclear whether the term is derived from first principles or follows directly once the estimated structure is optimized as if true; a self-contained derivation or counter-example is needed to establish that the harm is not definitional.

minor comments (1)

- [Allocation formulas] The transition from the myopic allocation θ_na to the anticipatory allocation θ_an would benefit from a one-sentence reminder of the linear permanent-impact assumption that produces the coefficient 2.

Simulated Author's Rebuttal

We thank the referee for the thorough review and insightful comments on the manuscript. We address each major comment below with clarifications and indicate revisions where appropriate to strengthen the exposition of the derivations.

read point-by-point responses

-

Referee: Main result (stacked finite-horizon LQG decomposition): the additive separation into information trace plus inverse-precision norm, and the resolution of the signed interaction, rest on the control gap admitting an exact trace decomposition. This requires value functions to remain quadratic under the enriched anticipatory dynamics. The derivation of θ_an=(2Λ+γΣ)^{-1}μ from the impact model must be shown to preserve this quadratic structure; otherwise the claimed separation of the three channels does not follow.

Authors: The anticipatory problem remains an LQG control problem because the market impact enters linearly in the dynamics and the objective remains quadratic; the value function is therefore quadratic by the standard Riccati theory for linear-quadratic problems. The allocation θ_an is obtained by completing the square in the enriched Hamiltonian, which directly yields the stated inverse and preserves the quadratic form. We will add an explicit paragraph verifying that the value function stays quadratic under the impact-augmented dynamics and that the trace decomposition follows from the same Riccati solution. revision: yes

-

Referee: Resolution of the signed forecast-impact interaction: the orthogonal nonnegative projection identity invoked to separate the signed term is load-bearing for the additive decomposition. The manuscript must state this identity explicitly and verify that it is independent of the model parameters rather than constructed from them, as the latter would render the separation tautological.

Authors: The identity is the standard orthogonal decomposition ||v||^2 = ||Pv||^2 + ||(I-P)v||^2 for any orthogonal projection P onto a subspace; it holds for the Euclidean inner product on the stacked forecast-impact vector and is therefore independent of all model parameters (Λ, Σ, γ, etc.). We will state the identity verbatim in the revised text, together with a one-line proof that it relies only on the inner-product axioms, and note that the nonnegativity of the projection term follows immediately. revision: yes

-

Referee: Penalty term ½tr(H^{-1}Σ_ε): the claim that this term demonstrates harm from misspecified anticipation is presented as an independent result. It is unclear whether the term is derived from first principles or follows directly once the estimated structure is optimized as if true; a self-contained derivation or counter-example is needed to establish that the harm is not definitional.

Authors: The term is obtained by subtracting the value function evaluated at the allocation that is optimal for the estimated covariance H from the value function evaluated at the allocation that is optimal for the true covariance Σ; after algebraic expansion of the quadratic forms the difference reduces exactly to ½tr(H^{-1}Σ_ε) plus a nonnegative term that vanishes only when H=Σ. We will supply this short derivation in a new appendix subsection, showing it is not merely definitional but follows from the difference of two quadratic value functions. revision: yes

Circularity Check

No circularity: derivations follow from standard LQG assumptions without self-referential reduction.

full rationale

The paper's central decomposition is derived under the explicit assumption of linear-quadratic-Gaussian dynamics with log or mean-variance utility, under which value functions are quadratic by standard control theory and the control gap therefore admits an exact trace decomposition. This is an input modeling choice, not a self-definition or fitted prediction. The information trace, inverse-precision norm, impact/forecast terms, and projection identity are presented as consequences of that quadratic geometry rather than presupposed by it. The penalty term ½ tr(H^{-1} Σ_ε) is likewise a direct model consequence measuring misspecification under the same assumptions. No self-citations, ansatzes smuggled via prior work, or renaming of known results are invoked as load-bearing steps in the provided text. The derivation chain is therefore self-contained against external LQG benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- γ

- Λ

axioms (2)

- domain assumption Dynamics are linear-quadratic-Gaussian so that value functions remain quadratic and admit exact trace decompositions.

- domain assumption Utility is either log or mean-variance.

Reference graph

Works this paper leans on

-

[1]

Journal of Risk , volume =

Almgren, Robert and Chriss, Neil , title =. Journal of Risk , volume =

-

[2]

Additional Logarithmic Utility of an Insider , journal =

Amendinger, J. Additional Logarithmic Utility of an Insider , journal =

-

[3]

A General Stochastic Calculus Approach to Insider Trading , journal =

Biagini, Francesca and. A General Stochastic Calculus Approach to Insider Trading , journal =

-

[4]

Mathematics of Operations Research , volume =

Blanchet, Jose and Murthy, Karthyek , title =. Mathematics of Operations Research , volume =

-

[5]

and Koh, Kwangmoo and Nystrup, Peter and Speth, Jan , title =

Boyd, Stephen and Busseti, Enzo and Diamond, Steven and Kahn, Ronald N. and Koh, Kwangmoo and Nystrup, Peter and Speth, Jan , title =. Foundations and Trends in Optimization , volume =

-

[6]

A Probabilistic Weak Formulation of Mean Field Games and Applications , journal =

Carmona, Ren. A Probabilistic Weak Formulation of Mean Field Games and Applications , journal =

-

[7]

and Thomas, Joy A

Cover, Thomas M. and Thomas, Joy A. , title =

-

[8]

Malliavin Calculus for L

Di Nunno, Giulia and. Malliavin Calculus for L

-

[9]

Zico , title =

Donti, Priya and Amos, Brandon and Kolter, J. Zico , title =. Advances in Neural Information Processing Systems , volume =

-

[10]

Mathematical Programming , volume =

Mohajerin Esfahani, Peyman and Kuhn, Daniel , title =. Mathematical Programming , volume =

-

[11]

and Grigas, Paul , title =

Elmachtoub, Adam N. and Grigas, Paul , title =. Management Science , volume =

-

[12]

Dynamic Trading with Predictable Returns and Transaction Costs , journal =

G. Dynamic Trading with Predictable Returns and Transaction Costs , journal =

-

[13]

Quantitative Finance , volume =

Gatheral, Jim , title =. Quantitative Finance , volume =

-

[14]

Journal of Mathematical Economics , volume =

Gilboa, Itzhak and Schmeidler, David , title =. Journal of Mathematical Economics , volume =

-

[15]

and Stiglitz, Joseph E

Grossman, Sanford J. and Stiglitz, Joseph E. , title =. American Economic Review , volume =

-

[16]

Grossissements de Filtrations: Exemples et Applications , series =

Jacod, Jean , title =. Grossissements de Filtrations: Exemples et Applications , series =

-

[17]

Grossissements de Filtrations: Exemples et Applications , series =

-

[18]

, title =

Karatzas, Ioannis and Shreve, Steven E. , title =

-

[19]

, title =

Kyle, Albert S. , title =. Econometrica , volume =

-

[20]

and Wang, Jiang , title =

Obizhaeva, Anna A. and Wang, Jiang , title =. Journal of Financial Markets , volume =

-

[21]

and Zrnic, Tijana and Mendler-D

Perdomo, Juan C. and Zrnic, Tijana and Mendler-D. Performative Prediction , booktitle =

-

[22]

Advances in Applied Probability , volume =

Pikovsky, Igor and Karatzas, Ioannis , title =. Advances in Applied Probability , volume =

-

[23]

Tyrrell and Uryasev, Stanislav , title =

Rockafellar, R. Tyrrell and Uryasev, Stanislav , title =. Journal of Risk , volume =

-

[24]

Lancaster, Peter and Rodman, Leiba , title =

-

[25]

Journal of Financial and Quantitative Analysis , volume =

Jorion, Philippe , title =. Journal of Financial and Quantitative Analysis , volume =

-

[26]

Financial Analysts Journal , volume =

Black, Fischer and Litterman, Robert , title =. Financial Analysts Journal , volume =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.