Goal-based portfolio selection with mental accounting

Pith reviewed 2026-05-19 11:43 UTC · model grok-4.3

The pith

Goal-based investors maintain separate portfolios penalized by mental costs, and their value function is the unique constrained viscosity solution to a coupled HJB system.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

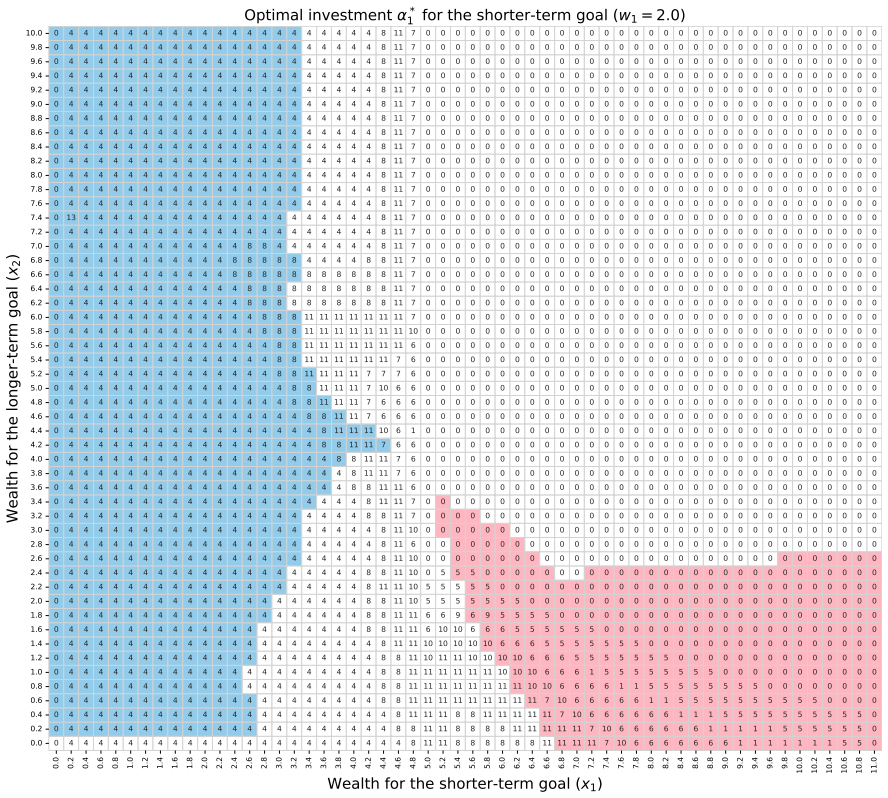

By modeling mental costs as a continuous-time penalty process for fund transfers between goal-specific portfolios, the framework leads to a system of HJB equations whose unique constrained viscosity solution is the value function, established through stochastic Perron's method. Numerical analysis reveals complex free boundaries with bulges and notches, dependence of strategies on other portfolios' wealth, diversification across stocks and portfolios, and delayed reallocation of surplus.

What carries the argument

Stochastic Perron's method applied to a system of Hamilton-Jacobi-Bellman equations whose running cost includes explicit penalties for transfers between goal-specific portfolios.

If this is right

- Optimal stock holdings chosen for one goal depend on the current wealth held in every other goal's portfolio.

- Investors spread risk both among individual stocks and across the different goal-specific portfolios.

- Surplus wealth in an important goal may be optimally retained there until its deadline draws near rather than being moved immediately.

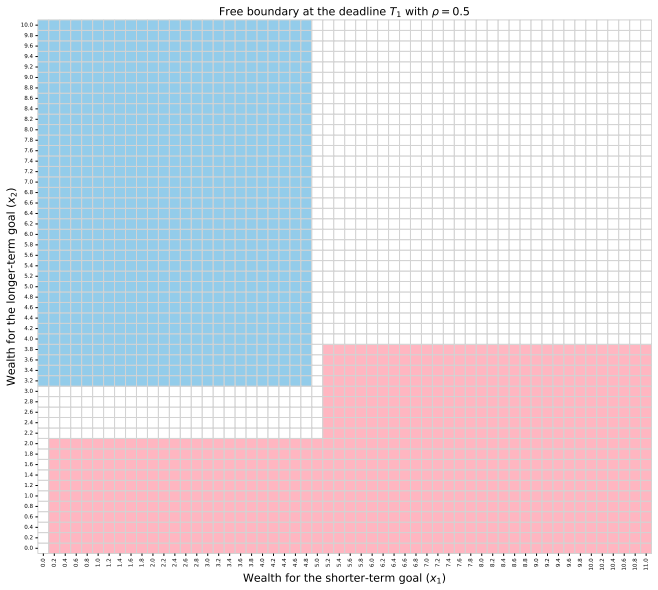

- The free boundaries that separate regions of different investment behavior take non-convex shapes containing bulges and notches.

Where Pith is reading between the lines

- Real-world investors who practice mental accounting may exhibit portfolio choices that appear inefficient when viewed from a single integrated account.

- Advisory tools could be built to recommend goal-specific allocations while explicitly charging modeled transfer costs.

- The predicted dependence of one portfolio's strategy on other goals' wealth levels could be tested with panel data on individual account holdings.

- Adding stochastic labor income or random goal deadlines would be a direct next step that preserves the same viscosity-solution structure.

Load-bearing premise

Investors maintain strictly separate portfolios for each goal and incur explicit continuous-time penalties whenever funds are transferred between them.

What would settle it

A numerical or empirical test in which optimal stock allocation in one goal's portfolio remains unchanged when wealth levels in other goal portfolios are varied over a wide range.

Figures

read the original abstract

We present a continuous-time portfolio selection framework that reflects goal-based investment principles and mental accounting behavior. In this framework, an investor with multiple investment goals constructs separate portfolios, each corresponding to a specific goal, with penalties imposed on fund transfers between these goals, referred to as mental costs. By applying the stochastic Perron's method, we demonstrate that the value function is the unique constrained viscosity solution of a Hamilton-Jacobi-Bellman equation system. Numerical analysis reveals several key features: the free boundaries exhibit complex shapes with bulges and notches; the optimal strategy for one portfolio depends on the wealth level of another; investors must diversify both among stocks and across portfolios; and they may postpone reallocating surplus from an important goal to a less important one until the former's deadline approaches.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper presents a continuous-time portfolio selection framework that incorporates goal-based investing and mental accounting behavior. Investors maintain strictly separate portfolios for each goal, with explicit mental costs imposed as penalties on fund transfers between goals. The central theoretical result applies stochastic Perron's method to establish that the value function is the unique constrained viscosity solution to the associated system of Hamilton-Jacobi-Bellman equations. Numerical experiments illustrate complex free-boundary shapes, cross-portfolio dependence in optimal controls, diversification across assets and goals, and delayed reallocation of surplus wealth.

Significance. If the uniqueness result is rigorously established, the framework supplies a mathematically grounded extension of classical Merton-style problems to behavioral multi-goal settings with frictions. The numerical observations on free-boundary geometry and strategy interdependence could inform practical goal-based allocation rules, provided the model primitives (mental costs, deadlines, utilities) are calibrated appropriately.

major comments (1)

- [Theoretical analysis / stochastic Perron's method] Application of stochastic Perron's method (central theoretical section): the uniqueness of the constrained viscosity solution requires an explicit verification that the comparison principle continues to hold once the mental-cost transfer process is introduced. This process adds cross terms to the Hamiltonian across the multi-dimensional wealth coordinates; the manuscript should confirm that the requisite monotonicity, growth, or Lipschitz conditions remain satisfied under these dynamics, or supply a tailored argument. Without this check the uniqueness claim is not yet load-bearing.

minor comments (2)

- [Model formulation] Model setup: the precise functional form of the mental cost process (running penalty rate, dependence on transfer size and goal pair) should be stated explicitly with an equation number for clarity.

- [Numerical analysis] Numerical section: figure captions for free-boundary plots should list the exact parameter values, grid resolution, and time-stepping scheme employed so that the reported shapes can be reproduced.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. The major comment raises an important point about the rigor of the uniqueness result, which we address directly below.

read point-by-point responses

-

Referee: Application of stochastic Perron's method (central theoretical section): the uniqueness of the constrained viscosity solution requires an explicit verification that the comparison principle continues to hold once the mental-cost transfer process is introduced. This process adds cross terms to the Hamiltonian across the multi-dimensional wealth coordinates; the manuscript should confirm that the requisite monotonicity, growth, or Lipschitz conditions remain satisfied under these dynamics, or supply a tailored argument. Without this check the uniqueness claim is not yet load-bearing.

Authors: We agree that an explicit verification is required to ensure the comparison principle holds with the mental-cost transfers. In the revised manuscript we add a dedicated paragraph in Section 3.3 that confirms the Hamiltonian remains monotone and satisfies the necessary growth and Lipschitz conditions. The cross terms generated by the transfer penalties are controlled by the non-negativity of the mental-cost function and the linear structure of the wealth dynamics; the standard estimates in the stochastic Perron method therefore carry over without modification. We have also included a brief remark on how the multi-dimensional state space does not alter the viscosity comparison argument. revision: yes

Circularity Check

No circularity: uniqueness via stochastic Perron's method is independent of inputs

full rationale

The paper defines the value function directly from the optimization objective that includes mental-cost penalties on transfers between goal-specific wealth processes. It then applies the stochastic Perron's method to establish that this value function satisfies the dynamic programming principle and is the unique constrained viscosity solution to the resulting HJB system whose coefficients are explicitly constructed from the model primitives (utilities, deadlines, mental cost functions, and multi-dimensional wealth dynamics). No equation reduces the claimed uniqueness to a fitted quantity, a self-referential definition, or a load-bearing self-citation whose own justification is unverified; the comparison principle is invoked for the specific Hamiltonian arising from the penalized transfers. The numerical illustrations of free boundaries and cross-portfolio dependence are presented as consequences rather than inputs. The derivation chain is therefore self-contained against the model primitives.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The value function satisfies a system of Hamilton-Jacobi-Bellman equations with constraints induced by the mental-cost penalties and goal deadlines.

invented entities (1)

-

mental cost process

no independent evidence

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

By applying the stochastic Perron's method, we demonstrate that the value function is the unique constrained viscosity solution of a Hamilton-Jacobi-Bellman equation system.

-

IndisputableMonolith/Foundation/AbsoluteFloorClosure.leanabsolute_floor_iff_bare_distinguishability unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

penalties imposed on fund transfers between these goals, referred to as mental costs

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Forward citations

Cited by 1 Pith paper

-

Analytical Approach to Continuous-Time Causal Optimal Transport

Causal optimal transport value between finite-state Markov source and diffusion target is characterized by a nonlinear parabolic master equation on enlarged state space and shown equivalent to Kushner-Stratonovich fil...

Reference graph

Works this paper leans on

-

[1]

Azimzadeh, P. (2017). Impulse Control in Finance: Numerical Methods and Viscosity Solutions . PhD thesis, University of Waterloo. Barberis, N. and Huang, M. (2001). Mental accounting, loss aversion, and individual stock returns. Journal of Finance , 56(4):1247–1292. Bayraktar, E., Belak, C., Christensen, S., and Seifried, F. T. (2022). Convergence of opti...

work page 2017

-

[2]

Bayraktar, E. and Li, J. (2016a). Stochastic Perron for stochastic target games. The Annals of Applied Probability, pages 1082–1110. Bayraktar, E. and Li, J. (2016b). Stochastic Perron for stochastic target problems. Journal of Optimization Theory and Applications , 170:1026–1054. Bayraktar, E. and Sirbu, M. (2012). Stochastic Perron’s method and verifica...

work page 2012

-

[3]

Springer Science & Business Media. Rokhlin, D. B. (2014). Stochastic Perron’s method for optimal control problems with state con- straints. Electronic Communications in Probability,

work page 2014

-

[4]

Shreve, S. E. and Soner, H. M. (1994). Optimal investment and consumption with transaction costs. The Annals of Applied Probability , pages 609–692. Sirbu, M. (2014). Stochastic Perron’s method and elementary strategies for zero-sum differential games. SIAM Journal on Control and Optimization , 52(3):1693–1711. Thaler, R. (1985). Mental accounting and con...

work page 1994

-

[5]

By a modification of the proof in Bayraktar and Sirbu (2013, Theorem 3.1), it follows that vK+1,+ in v+ satisfies the terminal condition (3.15) at T . Step

work page 2013

-

[6]

The viscosity subsolution property in Definition 3.1 (3), when t ∈ [Tk, T): Similarly, it follows from the proof of Bayraktar and Sirbu (2013, Theorem 3.1). Step

work page 2013

-

[7]

As vK+1,+ is USC, there exists a small ε > 0 such that vK,+(TK, ¯xK:K+1, ¯y) ≥ wK(GK − xK)+ + vK+1,+(TK, xK+1, y) + ε on the compact set B(¯xK:K+1, ¯y, ε), the closure of B(¯xK:K+1, ¯y, ε) := {(xK:K+1, y) : |(xK:K+1, y) − (¯xK:K+1, ¯y)| < ε}. (A.3) Since (¯xK:K+1, ¯y) is in the interior SK and ε is small enough, we can choose B(¯xK:K+1, ¯y, ε) ⊂ SK. By Ba...

work page 2012

-

[8]

The proof is similar to the Case (2) with the counterpart inequality to (A.28)

This suggests transferring from xK to xK+1. The proof is similar to the Case (2) with the counterpart inequality to (A.28). The control when A ∩ {τ 1 = TK} happens should be modified as follows. Denote (NK(xK), NK+1(xK+1), y) as the intersection of the ray{(xK −h, xK+1+h, y) : h ≥ 0} and ∂B(¯xK:K+1, ¯y, ε/2). Let U 2 := {(α2 K:K+1(t), L2 K(t), M2 K(t))}t∈...

work page 2013

-

[9]

A.2 Results of the stochastic subsolution Proof of Lemma 6.3

Then the claim (5.8) follows. A.2 Results of the stochastic subsolution Proof of Lemma 6.3. By definition of the value function J without mental accounting, we have Γk(t, 0, y) ≤ K+1X i=k wie−β(Ti−t)Gi, ∀ t ∈ [0, T], y ∈ Rm, k = 1, . . . , K+ 1, (A.36) ΓK+1(T, xK+1, y) ≤ (GK+1 − xK+1)+, ∀ (xK+1, y) ∈ S K+1. (A.37) Next, we prove that (Γ 1, . . . ,Γk, . . ...

work page 2024

-

[10]

By a modification of the step 3 in Bayraktar and Sirbu (2013, Theorem 4.1), it follows that vK+1,− in v− satisfies the terminal condition (3.21) at T . Step

work page 2013

-

[11]

The viscosity supersolution property in Definition 3.2 (3), when t ∈ [Tk, T): Similarly, it follows from the proof of Bayraktar and Sirbu (2013, Theorem 4.1). Step 3 . The viscosity supersolution property in Definition 3.2 (2), when t = TK: Let (¯xK:K+1, ¯y) ∈ S o K = {[0, ∞)2\{0}} × Rm and φ(xK:K+1, y) ∈ C2(S o K) be a test function such 46 that vK,−(TK,...

work page 2013

-

[12]

Similar to Bayraktar and Sirbu (2013, Theorem 4.1) and the step 3 in Proposition 5.5, we introduce a function h(δ) := inf TK −δ≤t≤TK , (xK:K+1,y)∈SK and ε 2 ≤|(xK:K+1,y)−(¯xK:K+1,¯y)|≤ε vK,−(t, xK:K+1, y) − φ(xK:K+1, y) , 0 < δ < δ 0, with some small δ0 >

work page 2013

-

[13]

Consider a stopping time ρ ∈ [τ, T ]

Let U := ( αK:K+1, LK, MK) ∈ U (τ, ξK:K+1, ξy). Consider a stopping time ρ ∈ [τ, T ]. Define the event A :={(τ, ξK:K+1, ξy) ∈ (TK − δ/2, TK] × B ¯S(¯xK:K+1, ¯y, ε/2)} ∩ {φp,η(τ, ξK:K+1, ξy) > v n K(τ, ξK:K+1, ξy)}. Then A ∈ F τ. Let τ 1 := inf n t ∈ [τ, TK] (t, (XK:K+1, Y )(t; τ, ξK:K+1, ξy, U)) /∈ (TK − δ/2, TK] × B ¯S(¯xK:K+1, ¯y, ε/2) o . Denote ξ1 := ...

work page 2015

-

[14]

Under Ac, the submartingale property of vn K with the random initial condition ( τ, ξK:K+1, ξy) and the control U leads to E h 1Ac∩{ρ<τ 1}e−β(ρ−τ)vn K(ρ, (XK:K+1, Y )(ρ; τ, ξK:K+1, ξy, U)) + 1Ac∩{ρ≥τ 1}∩{τ 1<TK }e−β(τ 1−τ)vn K(τ 1, ξ1 K:K+1, ξ1 y) + 1Ac∩{ρ≥τ 1}∩{τ 1=TK }e−β(TK −τ) wK(GK − ξ1 K)+ + vn K+1(TK, ξ1 K+1, ξ1 y) + 1Ac λK Z ρ∧τ 1 τ e−β(s−τ)dLK(s)...

work page 2015

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.