Estimator Averaging of Local Projection and VAR Impulse Responses

Reviewed by Pith T0 review T1 audit T2 compute T3 formal T4 kernel 2026-06-30 23:12 UTCgrok-4.3pith:DQ52YKTYrecord.jsonopen to challenge →

The pith

Averaging local projection and VAR impulse responses by minimizing their mean squared error yields consistent estimates with lower finite-sample risk.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

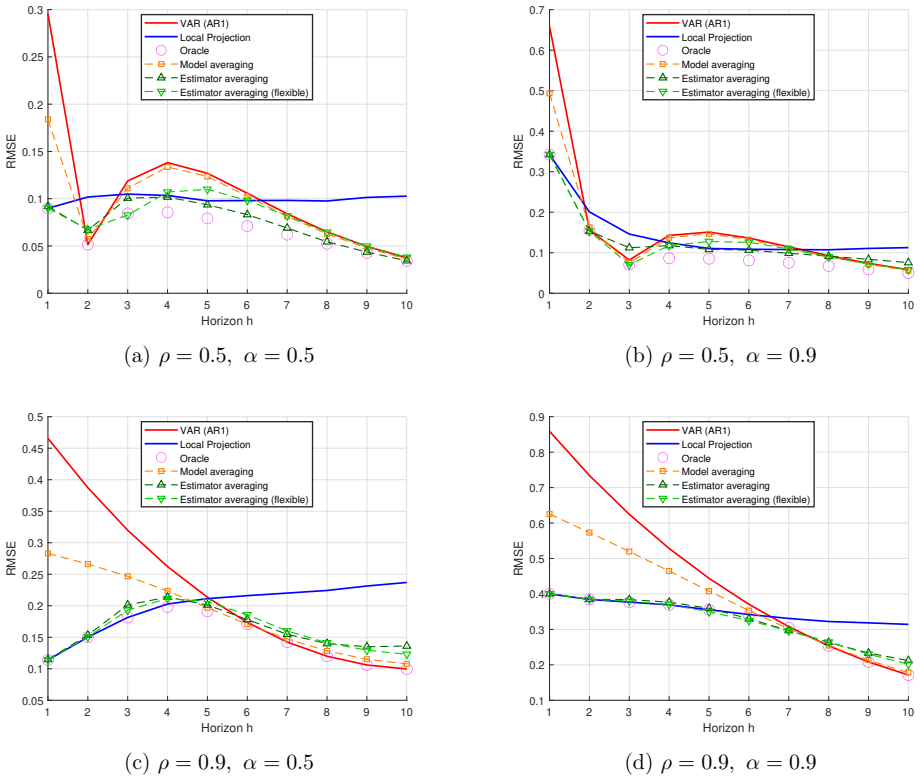

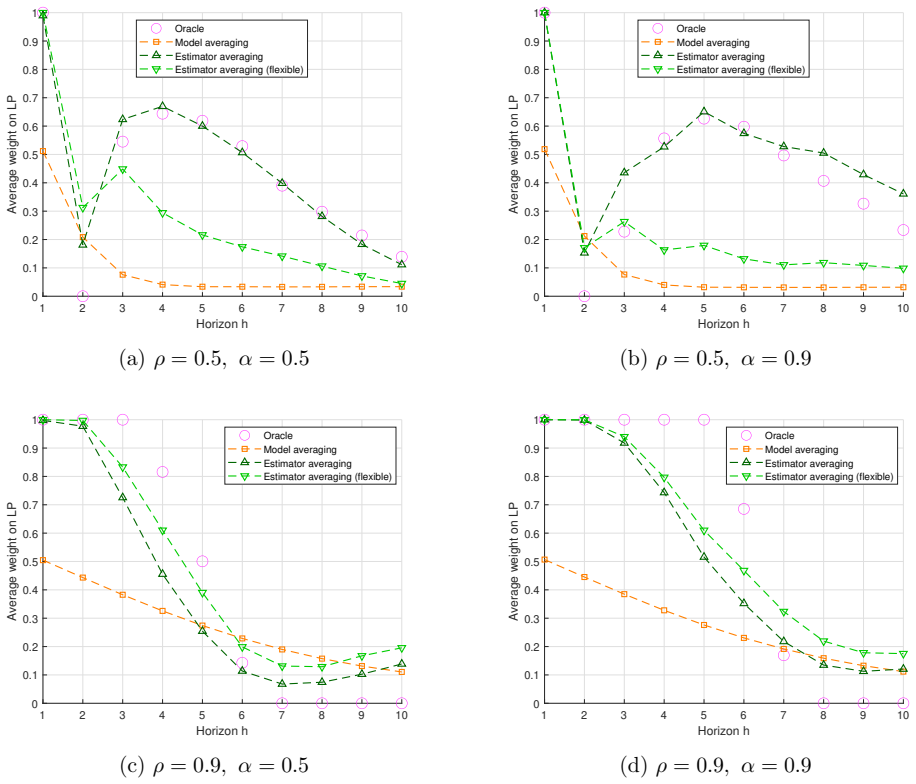

By deriving closed-form oracle weights that minimize the finite-sample mean squared error of the impulse response and approximating them with feasible AR-sieve-bootstrap procedures, the estimator averaging approach combines LP and VAR to achieve consistency and lower risk for a benchmark class of short-memory linear processes.

What carries the argument

Oracle weights minimizing the finite-sample mean squared error of the impulse response at each horizon, approximated by AR-sieve bootstrap.

If this is right

- The averaged estimator is consistent when both LP and VAR are consistent under the benchmark short-memory linear DGPs.

- The feasible averaged estimator possesses a well-defined limiting distribution.

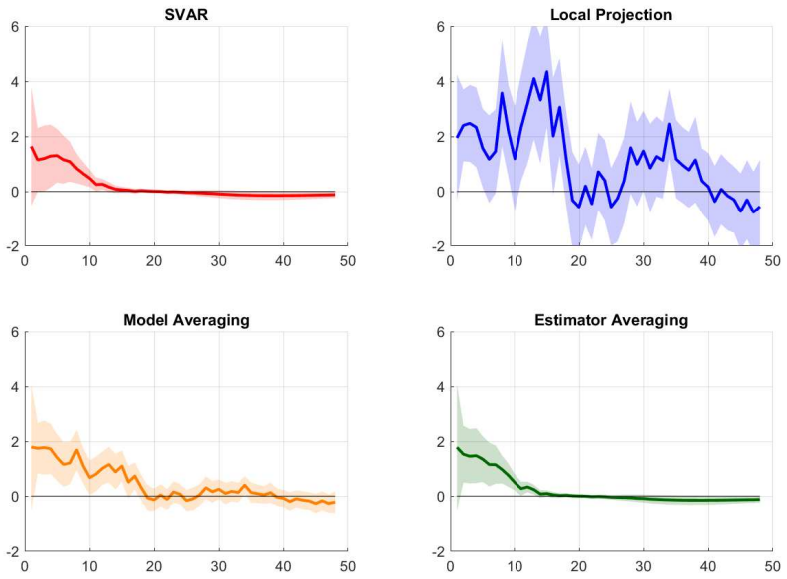

- Monte Carlo results establish meaningful finite-sample risk reductions relative to LP or VAR used separately.

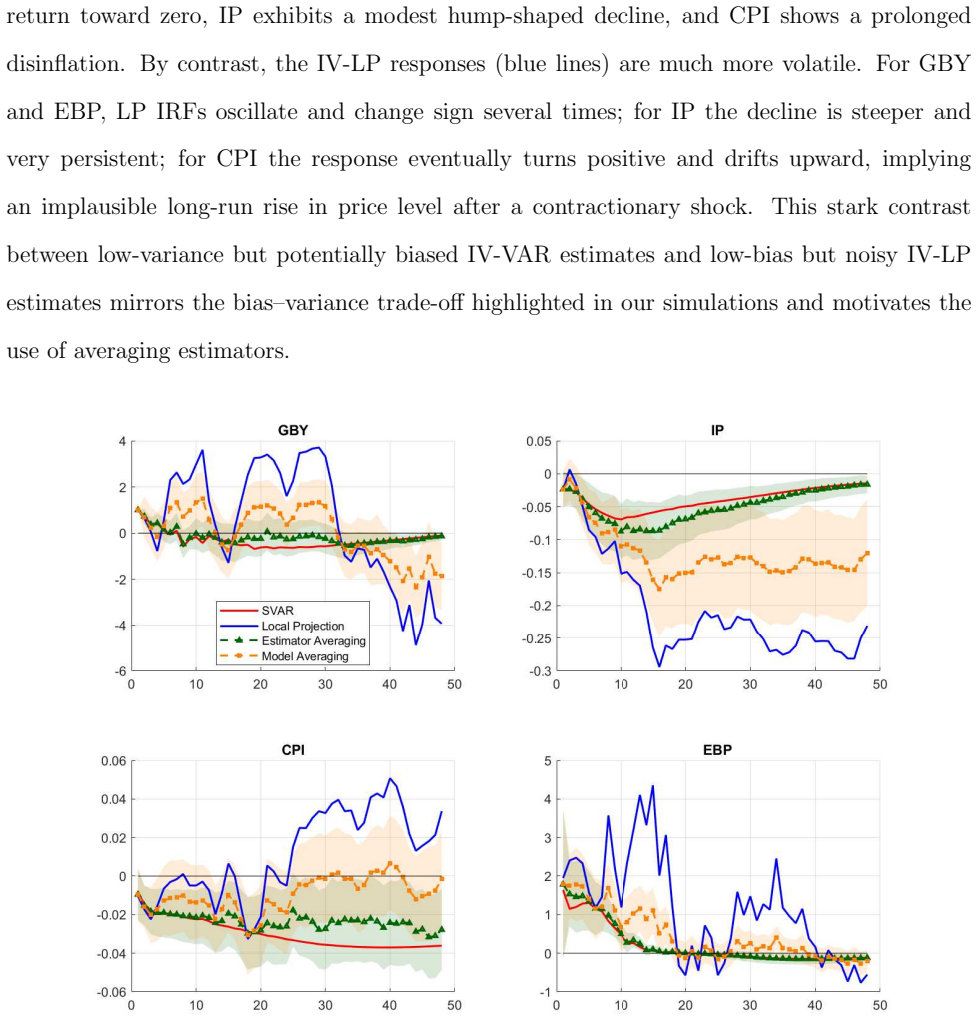

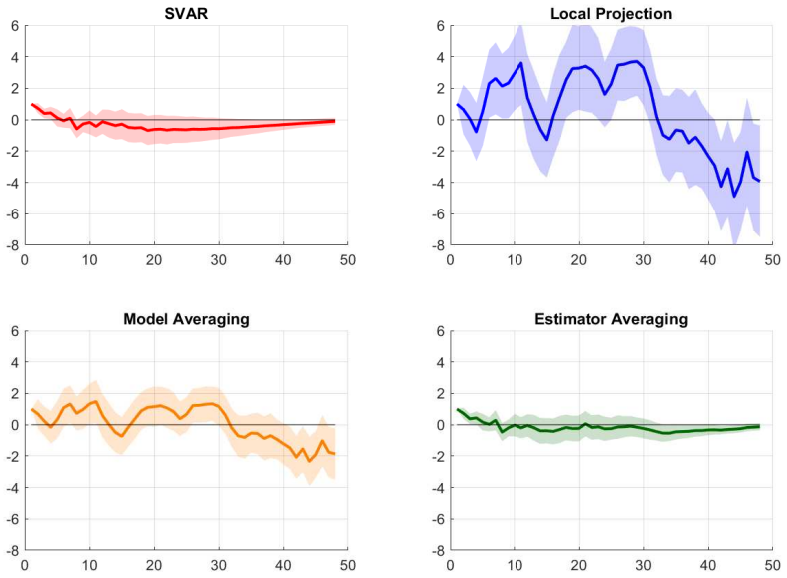

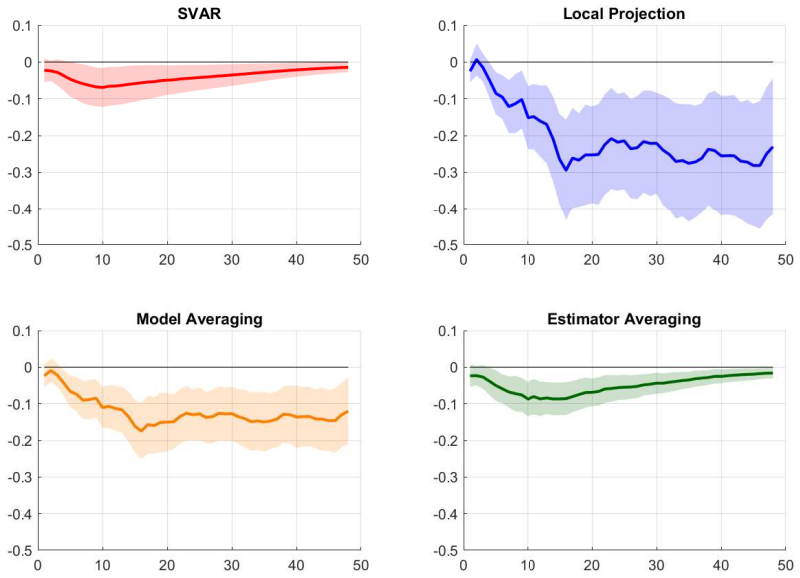

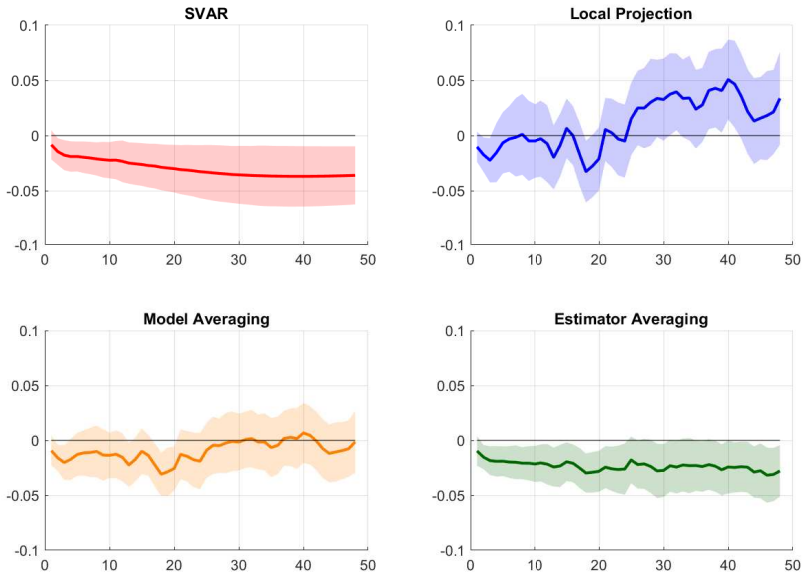

- The averaged estimates remain stable and economically interpretable in an application to monetary policy transmission.

Where Pith is reading between the lines

- The per-horizon weighting structure could be adapted to combine other pairs of estimators that trade bias against variance in impulse response settings.

- If the bootstrap approximation remains reliable outside short-memory linear cases, the method might extend to processes with longer memory or mild nonlinearity.

- Horizon-specific averaging suggests a route to tighter uncertainty bands for policy-relevant responses at longer horizons where volatility is typically high.

Load-bearing premise

The AR-sieve-bootstrap procedure accurately approximates the oracle weights that minimize finite-sample MSE without introducing additional bias or inconsistency.

What would settle it

A Monte Carlo experiment in which the bootstrap-derived weights produce higher MSE than the oracle weights or fail to reduce risk below the better of LP and VAR alone.

Figures

read the original abstract

Local projections (LP) and vector autoregressions (VAR) are the two standard tools for impulse response analysis, but they often display a finite-sample trade-off: LP is typically less biased but more volatile, while VAR is more precise but can be biased under misspecification. We propose an easy-to-implement estimator-averaging approach that combines LP and VAR at each horizon by minimizing the mean squared error of the impulse response itself, rather than in-sample fit. We derive closed-form oracle weights for this finite-sample risk problem, develop feasible AR-sieve-bootstrap procedures, and compare them against an Rsquare-based model-averaging benchmark. For a benchmark class of short-memory linear data generating processes in which LP and VAR are both consistent, we establish the consistency and limiting distribution of the feasible averaged estimator. Monte Carlo results show meaningful risk reductions relative to LP and VAR alone. In an empirical application revisiting Bauer and Swanson (2023), estimator averaging delivers stable and economically intuitive responses for yields, activity, prices, and credit spreads.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes an estimator-averaging method that combines local projection (LP) and VAR impulse responses at each horizon by minimizing the finite-sample mean squared error of the impulse response itself. Closed-form oracle weights are derived for this risk objective; feasible versions are implemented via AR-sieve bootstrap; consistency and a limiting distribution are established for the feasible averaged estimator under short-memory linear DGPs in which both LP and VAR are consistent; Monte Carlo experiments show risk reductions relative to the individual estimators; and an empirical application to Bauer and Swanson (2023) is presented.

Significance. If the bootstrap step is valid, the approach would supply a practical, MSE-optimal way to exploit the bias-variance trade-off between LP and VAR without model selection, yielding more reliable impulse-response estimates in macroeconometric applications.

major comments (1)

- [Feasible AR-sieve-bootstrap procedure and limiting-distribution theorem] The consistency and limiting-distribution claim for the feasible averaged estimator (abstract) rests on the AR-sieve bootstrap recovering the n-dependent oracle weights sufficiently accurately that the weight-estimation error does not change the asymptotic behavior. The manuscript states that such procedures are developed and the result proved, yet the provided materials give no explicit conditions, rate requirements, or proof outline for bootstrap consistency in this oracle-MSE setting; this step is load-bearing and requires additional verification.

Simulated Author's Rebuttal

We thank the referee for the careful reading and for identifying the need for greater transparency on the bootstrap step. We address the single major comment below.

read point-by-point responses

-

Referee: [Feasible AR-sieve-bootstrap procedure and limiting-distribution theorem] The consistency and limiting-distribution claim for the feasible averaged estimator (abstract) rests on the AR-sieve bootstrap recovering the n-dependent oracle weights sufficiently accurately that the weight-estimation error does not change the asymptotic behavior. The manuscript states that such procedures are developed and the result proved, yet the provided materials give no explicit conditions, rate requirements, or proof outline for bootstrap consistency in this oracle-MSE setting; this step is load-bearing and requires additional verification.

Authors: We agree that the bootstrap consistency argument is load-bearing and that the current draft does not supply sufficient detail. In the revision we will add an appendix subsection that states the precise conditions on the AR-sieve order (growing with sample size at a controlled rate), the moment and mixing assumptions needed for the bootstrap to replicate the finite-sample MSE objective, and the rate requirements ensuring that the estimation error in the feasible weights is o_p(1) relative to the oracle weights. We will also include a proof outline showing that this error does not alter the limiting distribution of the averaged estimator. These additions will make the claim fully verifiable. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper derives closed-form oracle weights explicitly from an external finite-sample MSE objective for the impulse response (distinct from the LP/VAR estimators themselves), then constructs a separate AR-sieve-bootstrap procedure to approximate those weights. It proves consistency and limiting distribution of the resulting feasible averaged estimator under stated short-memory linear DGP assumptions where both LP and VAR are already consistent. No step reduces by construction to a fitted parameter, self-citation chain, or definitional loop; the bootstrap step is presented as an independent approximation whose validity is established separately rather than assumed via the target result.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Both LP and VAR estimators are consistent for the impulse responses under the benchmark class of short-memory linear data generating processes.

Forward citations

Cited by 1 Pith paper

-

Approximate Minimax Estimation of a Bounded Normal Mean via Stochastic Mirror Ascent

Stochastic mirror ascent provably finds an approximately least-favorable distribution and minimax estimator for the Bounded Normal Mean problem, yielding 6–18% risk improvements over the minimax linear estimator.

Reference graph

Works this paper leans on

-

[1]

Before proving the lemma, we clarify the role of the AR-sieve pseudo -truth. Under the short-memory Wold assumptions and the AR-sieve lag-or der condition, with pT → ∞ sufficiently slowly relative to T , the AR-sieve approximation targets the same population impulse response in the benchmark setting where LP and V AR are bot h consistent. This motivates the...

-

[2]

Then ˆwh = ¯G ( G( ˆAT,h , ˆDT,h , ˆFT,h ) ) and w⋆ h = ¯G(G(Ah, D h, F h))

Define G(A, D, F ) = ( D− F )/ (A+D− 2F ), and let ¯G(x) = min {1, max{0, x }} denote clipping. Then ˆwh = ¯G ( G( ˆAT,h , ˆDT,h , ˆFT,h ) ) and w⋆ h = ¯G(G(Ah, D h, F h)). By Lemma 2, ( ˆAT,h , ˆDT,h , ˆFT,h ) p − →(Ah, D h, F h). (B.1) Assumption 5 implies Ah + Dh − 2Fh ≥ c > 0. Therefore, G is continuous in a neighborhood of ( Ah, D h, F h). Since the l...

-

[3]

31 0 . 75 0 . 25 − 0. 12 2 . 08 0 . 23 − 0. 23 0 . 56 1 . 75 , A 2 = − 0. 52 − 1. 06 − 0. 35

-

[4]

32 − 0. 78 − 1. 12 , A3 =

-

[5]

04 0 . 48 0 . 16 − 0. 08 0 . 53 0 . 15 − 0. 14 0 . 35 0 . 31 , A 4 =

-

[6]

02 − 0. 05 − 0. 03 . The structural impact matrix M0 is: M0 =

-

[7]

6 − 0. 6 1 . 7 44 SV ARMA(4,1) Specification The autoregressive coefficients A1, . . . , A 4 are: A1 =

-

[8]

24 − 0. 04 − 0. 03 − 0. 58 1 . 77 0 . 32 − 0. 78 0 . 76 1 . 63 , A 2 = − 0. 52 0 . 02 0 . 06

-

[9]

04 − 0. 98 − 1. 02 , A3 =

-

[10]

08 0 . 00 − 0. 03 − 0. 30 0 . 39 0 . 16 − 0. 44 0 . 41 0 . 29 , A 4 = − 0. 01 0 . 00 0 . 00

-

[11]

06 − 0. 05 − 0. 03 . The moving average matrix M1 is: M1 = − 0. 30 0 . 10 − 0. 40 − 0. 20 0 . 20 − 1. 00 − 0. 30 0 . 07 0 . 20 The structural impact matrix M0 is: M0 =

-

[12]

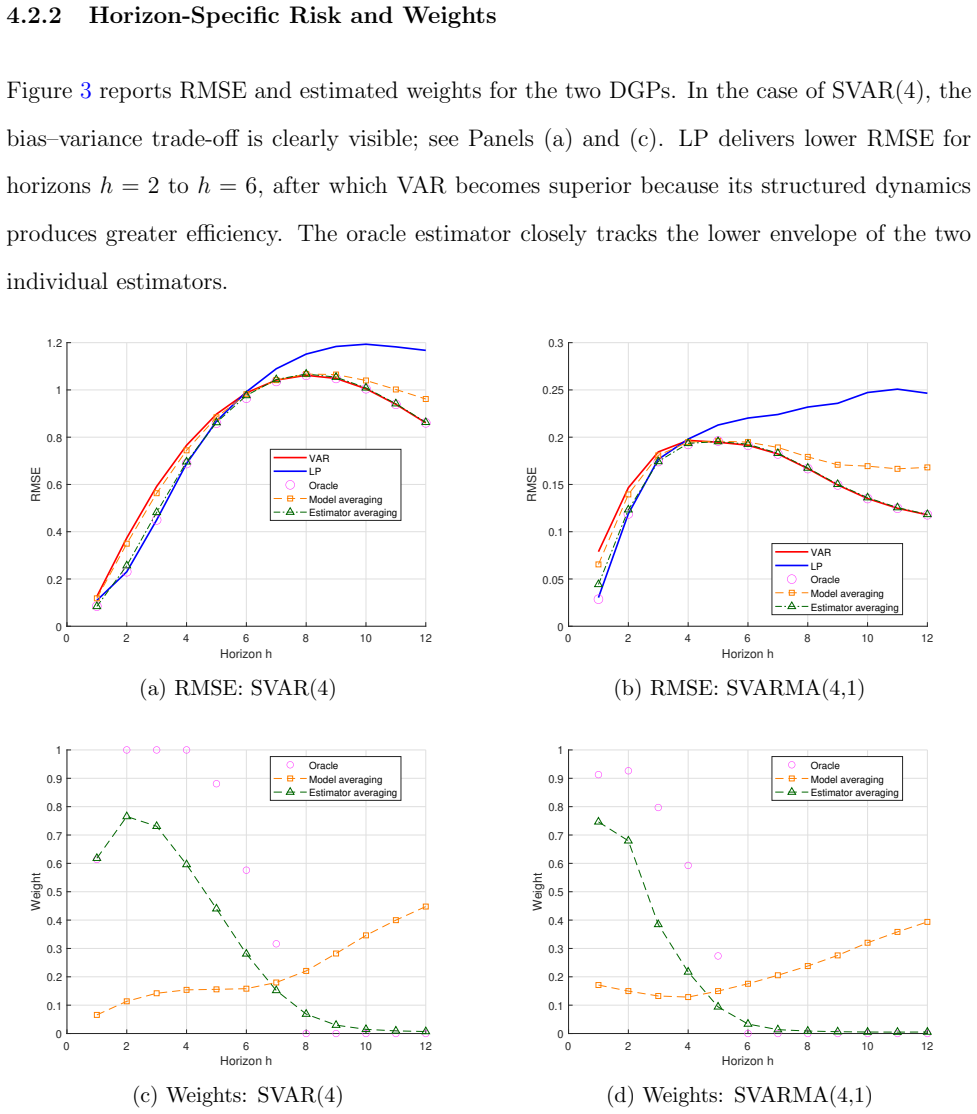

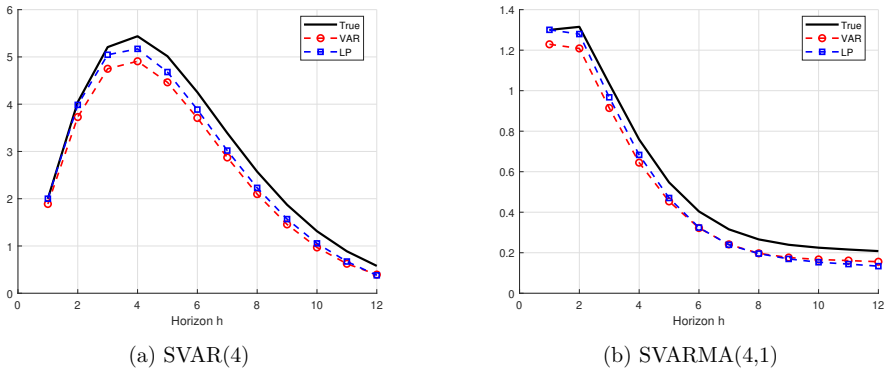

30 0 . 40 0 . 10 − 0. 02 0 . 05 2 . 00 − 0. 08 − 1. 70 0 . 80 Figure 6 displays the true impulse response functions alongside the average estimates from the V AR and LP estimators ( T = 200). 45 0 2 4 6 8 10 12 Horizon h 0 1 2 3 4 5 6 True VAR LP (a) SV AR(4) 0 2 4 6 8 10 12 Horizon h 0 0.2 0.4 0.6 0.8 1 1.2 1.4 True VAR LP (b) SV ARMA(4,1) Fi...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.