Faster Monotone Implied Volatility Solver

Pith reviewed 2026-06-30 16:28 UTC · model grok-4.3

The pith

ThiopheneIV inverts Black-Scholes implied volatility with a proven monotone core using a lower-bound seed plus six targeted iterations.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

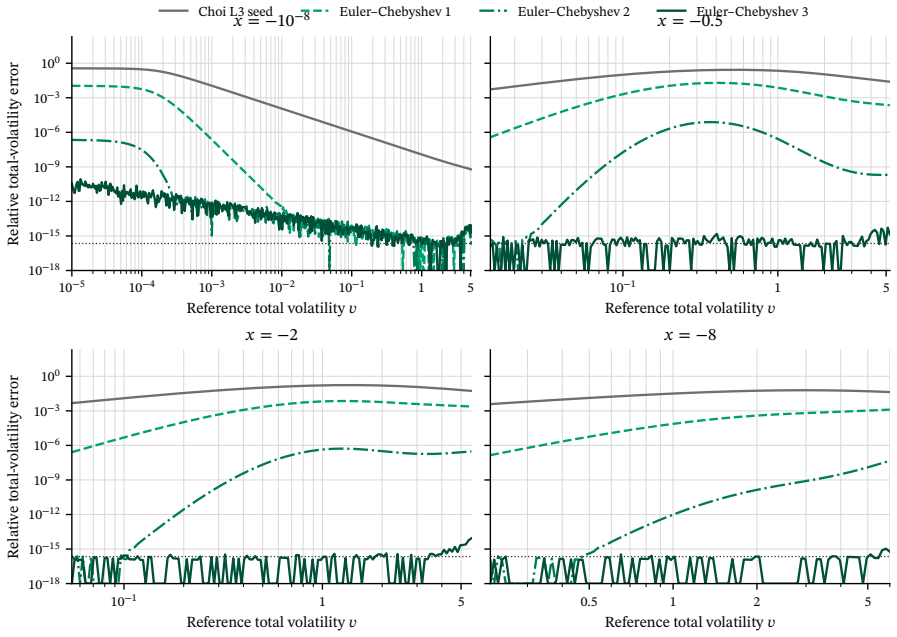

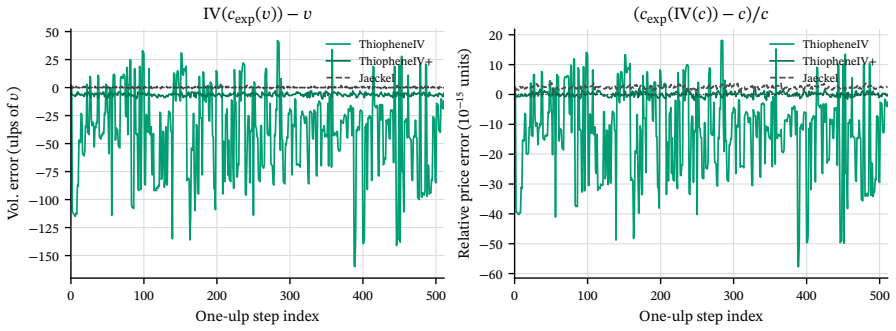

ThiopheneIV starts from the Choi-Huh-Su L3 lower-bound seed and applies three Euler-Chebyshev steps followed by three Halley steps; the paper proves that in exact arithmetic the seed lies below the root and both maps increase monotonically without overshooting, while the double-precision implementation adds explicit guards for parity, Bachelier limits, saturation, and optional polishing to match multiprecision Black reference prices at low latency.

What carries the argument

The monotone core formed by the Choi-Huh-Su L3 lower-bound seed together with the Euler-Chebyshev lower-branch map and the Halley upper-branch map, whose monotonicity without overshoot is proved in exact arithmetic.

If this is right

- The solver matches multiprecision Black reference prices across standard grids, market-like data, high-volatility regimes, and adversarial corners.

- It runs at low latency while providing explicit production guards for boundary cases.

- Direct comparisons place its accuracy and speed against Jäckel's Let's Be Rational and other recent solvers.

- A convergence proof supplies a clean iteration core, yet robust production use still requires careful boundary handling and choice of pricing objective.

Where Pith is reading between the lines

- The separation between the exact-arithmetic proof and the double-precision guards implies that similar monotone schemes for other pricing models would also need dedicated boundary logic before deployment.

- The optional Jäckel-Newton polish suggests that the core six-step method may be tuned further for speed-accuracy trade-offs in specific market regimes.

- Emphasis on matching a chosen pricing objective rather than a universal reference points to potential differences in solver behaviour when pricing the same option under different conventions.

Load-bearing premise

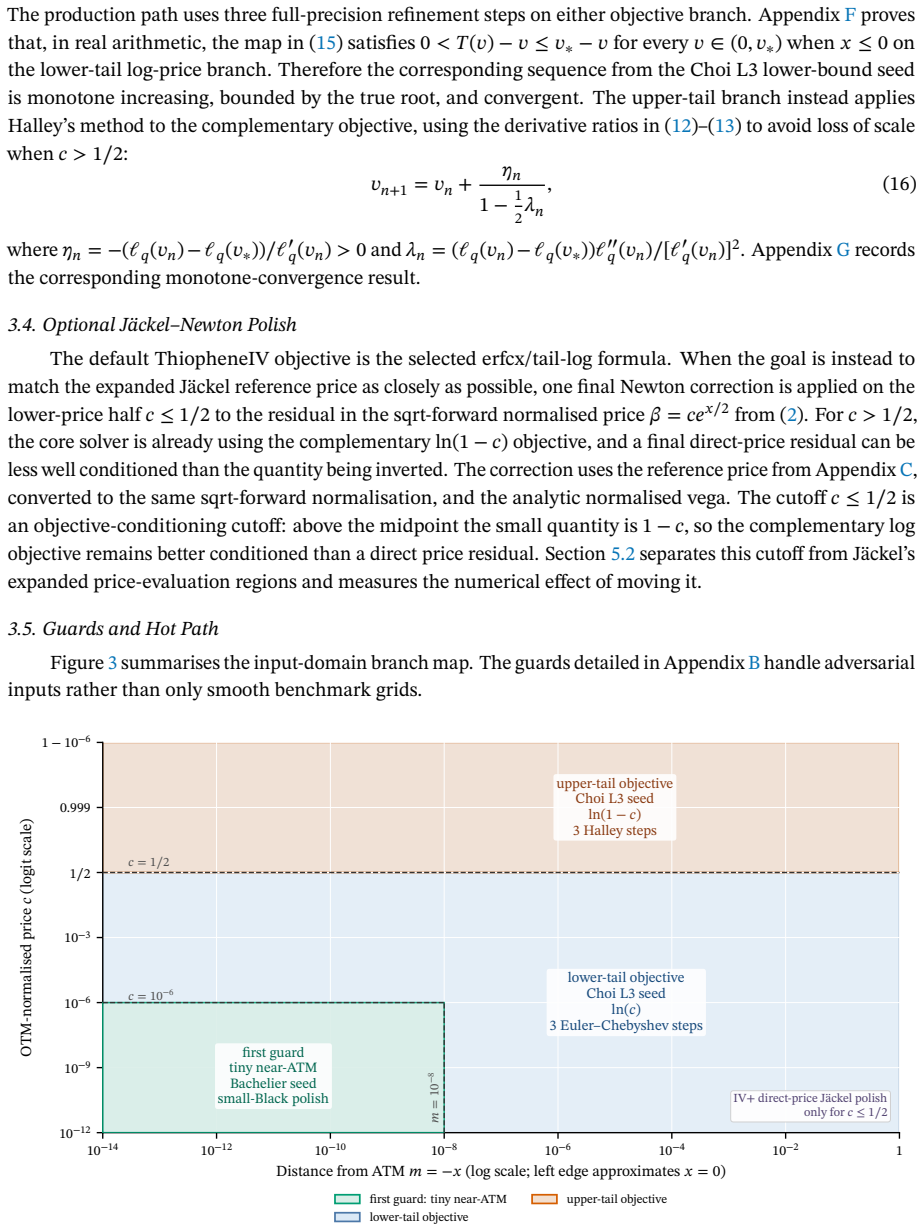

The double-precision implementation with its parity normalisation, Bachelier-limit handling, saturated-price treatment, and optional polish continues to respect the exact-arithmetic monotonicity and accuracy properties.

What would settle it

A single test point where the solver returns an implied volatility that, when substituted back into the Black-Scholes formula, produces a price differing from the input price by more than a few units in the last place of double precision.

Figures

read the original abstract

We present ThiopheneIV, a Black-Scholes implied-volatility solver with a monotone core and explicit production guards. The solver starts from the simple Choi-Huh-Su L3 lower-bound seed and applies three Euler-Chebyshev steps on a lower branch and three Halley steps on the remaining upper branch. We prove that, in exact arithmetic, the seed lies below the root and both maps increase monotonically without overshooting. We also detail the practical challenges encountered for a double-precision implementation: parity normalisation, microscopic Bachelier-limit handling, saturated price treatment, and an optional J\"ackel-Newton polish. Across standard grids, market-like data, high-volatility cases, and adversarial corners, ThiopheneIV agrees closely with multiprecision Black reference prices at low latency. We provide detailed comparisons with recent solvers, including J\"ackel's Let's Be Rational. The broader lesson is that a convergence proof gives a clean core, but robust production inversion still depends on boundary handling and on the pricing objective one chooses to match.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper presents ThiopheneIV, a Black-Scholes implied-volatility solver whose core begins with the Choi-Huh-Su L3 lower-bound seed and applies three Euler-Chebyshev steps on the lower branch followed by three Halley steps on the upper branch. It proves that, in exact arithmetic, the seed lies below the root and both iteration maps are strictly increasing and never overshoot. The manuscript also describes the additional machinery required for a double-precision implementation (parity normalisation, microscopic Bachelier-limit handling, saturated-price treatment, and an optional Jäckel-Newton polish) and reports close agreement with multiprecision reference prices across standard grids, market data, high-volatility regimes, and adversarial corners, together with comparisons against Jäckel’s Let’s Be Rational solver.

Significance. If the exact-arithmetic proof is correct and the floating-point implementation can be shown to inherit the monotonicity and no-overshoot guarantees, the work supplies a theoretically grounded, low-latency solver that is directly usable in production pricing engines. The explicit discussion of the boundary-handling interventions needed to move from the proved regime to double precision is itself a useful contribution to the literature on robust numerical inversion.

major comments (1)

- [double-precision implementation section] The section describing the double-precision implementation and production guards: the monotonicity and no-overshoot properties are proved only in exact arithmetic, yet the production solver introduces parity normalisation, Bachelier-limit handling, saturated-price treatment, and an optional Jäckel-Newton polish. No separate argument or exhaustive floating-point analysis is supplied showing that these interventions preserve the proved properties once rounding occurs. Because the headline accuracy and performance claims rest on the implemented solver behaving as the exact proof predicts, this transfer constitutes a load-bearing gap.

Simulated Author's Rebuttal

We thank the referee for highlighting this important point regarding the distinction between the exact-arithmetic proof and the floating-point implementation. We provide a point-by-point response below.

read point-by-point responses

-

Referee: [double-precision implementation section] The section describing the double-precision implementation and production guards: the monotonicity and no-overshoot properties are proved only in exact arithmetic, yet the production solver introduces parity normalisation, Bachelier-limit handling, saturated-price treatment, and an optional Jäckel-Newton polish. No separate argument or exhaustive floating-point analysis is supplied showing that these interventions preserve the proved properties once rounding occurs. Because the headline accuracy and performance claims rest on the implemented solver behaving as the exact proof predicts, this transfer constitutes a load-bearing gap.

Authors: We acknowledge that the monotonicity and no-overshoot properties are proved exclusively in exact arithmetic. The double-precision implementation includes several production guards—parity normalisation, Bachelier-limit handling, saturated-price treatment, and an optional Jäckel-Newton polish—to address numerical issues that arise in IEEE 754 floating-point arithmetic, such as underflow, overflow, and loss of precision near boundaries. These guards are necessary to ensure the solver remains robust and accurate in practice. We do not supply a formal floating-point analysis demonstrating that these interventions preserve the exact-arithmetic properties under all rounding conditions. Instead, the accuracy of the implemented solver is validated through extensive empirical testing against multiprecision reference Black-Scholes prices across a variety of test cases, including standard grids, market data, high-volatility regimes, and adversarial corners. In these tests, the solver exhibits the expected behavior without observed instances of non-monotonicity or overshooting. We agree that explicitly noting this distinction would improve the manuscript. We will revise the double-precision implementation section to clarify that the theoretical guarantees apply to the exact-arithmetic core, while the floating-point version relies on empirical validation for its practical performance and accuracy claims. The performance claims are supported by direct timing measurements, independent of the proof. revision: partial

Circularity Check

No significant circularity; mathematical proof stands independently of implementation details

full rationale

The paper's core contribution is an explicit proof in exact arithmetic that the Choi-Huh-Su L3 seed lies below the root and that the three Euler-Chebyshev steps (lower branch) plus three Halley steps (upper branch) are strictly increasing and non-overshooting. This proof is presented as a self-contained mathematical argument and does not rely on any fitted parameters renamed as predictions, self-citations that bear the central load, or definitions that smuggle the result into the inputs. The double-precision guards (parity normalisation, Bachelier-limit handling, saturated-price treatment, optional Jäckel-Newton polish) are described separately as practical additions outside the proved regime; they do not retroactively alter or define the exact-arithmetic claim. The manuscript further anchors its accuracy claims to external multiprecision Black reference prices and comparisons with other solvers, keeping the derivation independent of its own outputs.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Black-Scholes call/put price is strictly increasing in volatility for fixed strike and maturity

Forward citations

Cited by 3 Pith papers

-

A Practical Guide to Strip Caplet Volatilities

Interpolation scheme and node placement drive instability in caplet stripping; continuous flat-linear kernels, midpoint nodes, and exponential reparametrization or Hyman splines deliver stable positive curves with neg...

-

A Practical Guide to Strip Caplet Volatilities

Constructive algorithm for arbitrage-free caplet volatility stripping via time-value interpolation, data outlier correction, and new compact-kernel bootstrap interpolants.

-

Implying Volatility: How Fast Can We Go?

FlashIV is a new Black-Scholes implied volatility solver using input normalization, erfcx residual, and fixed Householder refinement that runs faster than Jäckel's Let's Be Rational while staying close to its reference price.

Reference graph

Works this paper leans on

-

[1]

The Pricing of Commodity Contracts.J

Black, F. The Pricing of Commodity Contracts.J. Financ. Econ.1976,3, 167–179. https://doi.org/10.1016/0304- 405X(76)90024-6. 25

-

[2]

https://doi.org/10.1002/fut.70024

Cui,Z.;Liu,Y.;Yao,Y.TighterBoundsforImpliedVolatilityWiththeDiracDeltaFamilyMethod.J.FuturesMarkets 2025,45,e70024. https://doi.org/10.1002/fut.70024

-

[3]

Jäckel,P.Let’sBeRational.Wilmott2017,2015,40–53. https://doi.org/10.1002/wilm.10395

-

[4]

Availableonline: https://chasethedevil

LeFloc’h,F.MonotonicityoftheBlack–ScholesOptionPricesinPractice. Availableonline: https://chasethedevil. github.io/post/vol_monotonicity_in_practice/(accessedon19May2026)

-

[5]

Choi, J.; Huh, J.; Su, N. Tighter ‘Uniform Bounds for Black–Scholes Implied Volatility’ and the Applications to Root-Finding.Oper. Res. Lett.2024,57,107189. https://doi.org/10.1016/j.orl.2024.107189

-

[6]

Birnbaum,Z.W.AnInequalityforMill’sRatio.Ann. Math. Statist.1942,13,245–246. https://doi.org/10.1214/aoms/ 1177731611

-

[7]

On Information and Sufficiency,

Sampford, M.R. Some Inequalities on Mill’s Ratio and Related Functions.Ann. Math. Statist.1953,24, 130–132. https://doi.org/10.1214/aoms/1177729093

-

[8]

Abramowitz,M.;Stegun,I.A.HandbookofMathematicalFunctions;NationalBureauofStandards,AppliedMathe- maticsSeries55: Washington,DC,USA,1964

1964

-

[9]

Traub,J.F.IterativeMethodsfortheSolutionofEquations;ChelseaPublishingCompany: NewYork,NY,USA,1982

1982

-

[10]

Householder,A.S.TheNumericalTreatmentofaSingleNonlinearEquation;McGraw-Hill: NewYork,NY,USA,1970

1970

-

[11]

Healy,J.AppliedQuantitativeFinanceforEquityDerivatives,4thed.;self-published,2024

2024

-

[12]

Availableonline: https://ssrn.com/abstract=2420757 (accessedon16May2026)

LeFloc’h,F.FastandAccurateAnalyticBasisPointVolatility. Availableonline: https://ssrn.com/abstract=2420757 (accessedon16May2026). 26

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.