Growth model with externalities for energetic transition via MFG with common external variable

Pith reviewed 2026-05-23 05:39 UTC · model grok-4.3

The pith

Reformulating equilibrium conditions as an FBSDE proves existence and uniqueness of a strong mean-field game equilibrium for multi-sector growth with evolving externalities and common noise.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that the mean-field game equilibrium conditions for the multi-sector growth model with dynamically evolving externality and common noise can be reformulated as a Forward-Backward Stochastic Differential Equation under the stochastic maximum principle, and a contraction argument then guarantees the existence and uniqueness of a strong solution.

What carries the argument

Reformulation of the mean-field game equilibrium conditions as a Forward-Backward Stochastic Differential Equation under the stochastic maximum principle, followed by a contraction mapping argument to obtain uniqueness.

If this is right

- A unique strong mean-field game equilibrium exists for the stated growth model.

- The equilibrium can be approximated numerically by a fixed-point scheme combined with neural network representations.

- The framework incorporates environmental considerations into classical multi-sector growth models under shared uncertainty.

- Policy analysis of energetic transition can be conducted inside this equilibrium setting.

Where Pith is reading between the lines

- The same FBSDE-plus-contraction technique might extend to other collective-externality problems such as climate policy models.

- If the contraction property survives modest changes in the functional forms, the method could apply beyond the specific utilities chosen here.

- Real-world calibration of the externality process against energy-sector data would test whether the predicted equilibrium trajectories match observed transition paths.

Load-bearing premise

The chosen functional forms for the externality dynamics, agent utilities, and common noise permit the FBSDE reformulation and the contraction mapping to hold.

What would settle it

An explicit counter-example, or a numerical run of the fixed-point iteration, in which the contraction mapping fails to converge or multiple solutions to the FBSDE appear.

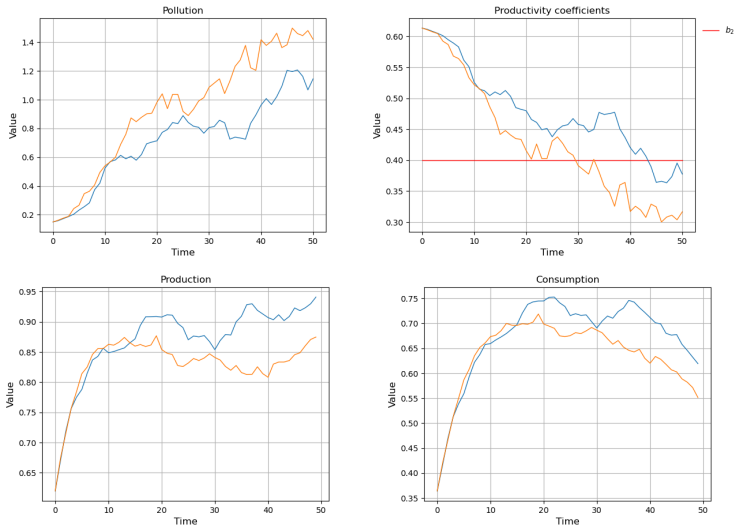

Figures

read the original abstract

This article introduces a novel mean-field game model for multi-sector economic growth in which a dynamically evolving externality, influenced by the collective actions of agents, plays a central role. Building on classical growth theories and integrating environmental considerations, the framework incorporates common noise to capture shared uncertainties among agents about the externality variable. We demonstrate the existence and uniqueness of a strong mean-field game equilibrium by reformulating the equilibrium conditions as a Forward-Backward Stochastic Differential Equation under the stochastic maximum principle and establishing a contraction argument to ensure a unique solution. We provide a numerical resolution for a specified model using a fixed-point approach combined with neural network approximations.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces a mean-field game model for multi-sector economic growth with a dynamically evolving externality driven by collective agent actions and common noise. It claims to prove existence and uniqueness of a strong MFG equilibrium by reformulating the equilibrium conditions as an FBSDE via the stochastic maximum principle, followed by a contraction mapping argument. A numerical scheme based on fixed-point iteration with neural-network approximations is presented for a concrete instance of the model.

Significance. If the existence/uniqueness result holds under the stated conditions, the work supplies a rigorous MFG framework that incorporates environmental externalities and common noise into multi-sector growth models, extending classical growth theory. The numerical component demonstrates practical solvability. These elements would be of interest to researchers working at the intersection of stochastic control, mean-field games, and economic modeling of energetic transitions.

major comments (2)

- [Existence and uniqueness argument (FBSDE reformulation and contraction)] The contraction-mapping step for FBSDE uniqueness (described in the abstract and the existence/uniqueness section) requires uniform Lipschitz continuity of the drift and cost coefficients together with a monotonicity condition whose constant produces a contraction factor strictly less than one. The manuscript supplies no explicit verification that the chosen multi-sector growth functionals, externality dynamics, and running/terminal costs satisfy these quantitative bounds; without such a check the uniqueness claim rests on an unverified assumption.

- [Reformulation via stochastic maximum principle] Application of the stochastic maximum principle to obtain the FBSDE system is asserted without derivation of the necessary regularity conditions on the value function or adjoint processes, particularly in the presence of the common external variable and the multi-sector structure. No verification is given that the Hamiltonian satisfies the required convexity or differentiability hypotheses for the principle to hold in this setting.

minor comments (2)

- [Abstract] The abstract states the proof strategy but does not list the precise functional forms or the monotonicity/Lipschitz constants that are later used; adding a short statement of the key structural assumptions would improve readability.

- [Numerical resolution] The numerical section does not report quantitative bounds on the approximation error introduced by the neural-network solver or on the convergence rate of the fixed-point iteration; including such diagnostics would strengthen the computational results.

Simulated Author's Rebuttal

Dear Editor, We thank the referee for the thoughtful and detailed report. The two major comments correctly identify gaps in the explicit verification of technical conditions underlying the existence/uniqueness result. We will revise the manuscript to supply these verifications in a new dedicated subsection, thereby strengthening the rigor of the proofs without altering the model or main claims. Point-by-point responses follow.

read point-by-point responses

-

Referee: The contraction-mapping step for FBSDE uniqueness (described in the abstract and the existence/uniqueness section) requires uniform Lipschitz continuity of the drift and cost coefficients together with a monotonicity condition whose constant produces a contraction factor strictly less than one. The manuscript supplies no explicit verification that the chosen multi-sector growth functionals, externality dynamics, and running/terminal costs satisfy these quantitative bounds; without such a check the uniqueness claim rests on an unverified assumption.

Authors: We agree that an explicit verification is missing. In the revised manuscript we will add a new subsection (placed after the statement of the FBSDE system) that computes the relevant partial derivatives of the drift, running cost, and terminal cost with respect to the state, control, and externality variables. Under the standing parameter restrictions of the multi-sector growth model (positive but bounded marginal products, quadratic penalization of deviations, and linear externality dynamics), we will derive uniform Lipschitz constants and show that the monotonicity constant yields a contraction factor strictly less than one for sufficiently small time horizon or sufficiently strong mean-reversion in the externality. This verification will be model-specific but fully rigorous. revision: yes

-

Referee: Application of the stochastic maximum principle to obtain the FBSDE system is asserted without derivation of the necessary regularity conditions on the value function or adjoint processes, particularly in the presence of the common external variable and the multi-sector structure. No verification is given that the Hamiltonian satisfies the required convexity or differentiability hypotheses for the principle to hold in this setting.

Authors: We acknowledge the need for explicit regularity checks. In the revision we will insert a short preparatory lemma that verifies the required conditions: (i) the Hamiltonian is jointly convex in the control and linear in the adjoint variables under the quadratic cost structure; (ii) the value function is C^{1,2} in the state and externality variables by standard parabolic regularity for the associated HJB equation with common noise; (iii) the adjoint processes remain square-integrable because the externality dynamics are linear with bounded coefficients. These verifications rely on the same parameter bounds already used for the contraction argument and will be stated before invoking the stochastic maximum principle. revision: yes

Circularity Check

No significant circularity in the MFG equilibrium derivation

full rationale

The paper establishes existence and uniqueness of the strong MFG equilibrium by reformulating conditions as an FBSDE via the stochastic maximum principle followed by a contraction argument. This is a standard technique from the MFG literature and does not reduce the result to a self-definition, a fitted parameter renamed as prediction, or a load-bearing self-citation chain. No ansatz smuggling, uniqueness imported from authors, or renaming of known results is present in the abstract or described chain. The derivation remains independent of the specific model functionals once the abstract FBSDE setting is accepted.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

reformulating the equilibrium conditions as a Forward-Backward Stochastic Differential Equation under the stochastic maximum principle and establishing a contraction argument

-

IndisputableMonolith/Foundation/DimensionForcing.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

monotonicity regime which differs from the usual displacement monotonicity but is consistent with the framework identified in [7,8]

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

M. Abadi, A. Agarwal, P. Barham, E. Brevdo, Z. Chen, C. Citro, G. S. Corrado, A. Davis, J. Dean, M. Devin, S. Ghemawat, I. Goodfellow, A. Harp, G. Irving, M. Isard, Y. Jia, R. Jozefowicz, L. Kaiser, M. Kudlur, J. Levenberg, D. Mane, R. Monga, S. Moore, D. Mur- ray, C. Olah, M. Schuster, J. Shlens, B. Steiner, I. Sutskever, K. Talwar, P. Tucker, V. Van- ho...

work page 2015

- [2]

- [3]

-

[4]

S. Ahuja. Wellposedness of mean field games with common noise under a weak monotonicity condition.SIAM Journal on Control and Optimization, 54(1):30–48, 2016

work page 2016

- [5]

- [6]

-

[7]

C. Bertucci and C. Meynard. Noise through an additional variable for mean field games master equation on finite state space.arXiv preprint arXiv:2402.05635, 2024

-

[8]

C. Bertucci and C. Meynard. A study of common noise in mean field games.arXiv preprint arXiv:2412.12741, 2024

- [9]

-

[10]

W. A. Brock and M. S. Taylor. The green solow model.Journal of Economic Growth, 15:127–153, 2010

work page 2010

-

[11]

P. Cardaliaguet, F. Delarue, J.-M. Lasry, and P.-L. Lions.The master equation and the convergence problem in mean field games:(ams-201). Princeton University Press, 2019

work page 2019

-

[12]

P. Cardaliaguet and S. Hadikhanloo. Learning in mean field games: the fictitious play. ESAIM: Control, Optimisation and Calculus of Variations, 23(2):569–591, 2017

work page 2017

-

[13]

P. Cardaliaguet and C.-A. Lehalle. Mean field game of controls and an application to trade crowding.Mathematics and Financial Economics, 12:335–363, 2018

work page 2018

-

[14]

R. Carmona, F. Delarue, et al.Probabilistic theory of mean field games with applications I-II. Springer, 2018

work page 2018

-

[15]

R. Carmona, F. Delarue, and D. Lacker. Mean field games with common noise.The Annals of Probability, 44(6):3740 – 3803, 2016

work page 2016

-

[16]

R. Carmona and M. Lauri` ere. Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games: Ii—the finite horizon case.The Annals of Applied Probability, 32(6):4065–4105, 2022

work page 2022

-

[17]

Q. Chan-Wai-Nam, J. Mikael, and X. Warin. Machine learning for semi linear pdes.Journal of scientific computing, 79(3):1667–1712, 2019. 33

work page 2019

-

[18]

M. F. Djete. Large population games with interactions through controls and common noise: convergence results and equivalence between open-loop and closed-loop controls.ESAIM: Control, Optimisation and Calculus of Variations, 29:39, 2023

work page 2023

- [19]

-

[20]

W. Gangbo and A. R. M´ esz´ aros. Global well-posedness of master equations for deterministic displacement convex potential mean field games.Communications on Pure and Applied Mathematics, 75(12):2685–2801, 2022

work page 2022

-

[21]

M. Germain, J. Mikael, and X. Warin. Numerical resolution of mckean-vlasov fbsdes using neural networks.Methodology and Computing in Applied Probability, 24(4):2557–2586, 2022

work page 2022

- [22]

-

[23]

G. Hardin. The tragedy of the commons: the population problem has no technical solution; it requires a fundamental extension in morality.science, 162(3859):1243–1248, 1968

work page 1968

- [24]

-

[25]

D. Kingma and J. Ba. Adam: A method for stochastic optimization.International Con- ference on Learning Representations, 2014

work page 2014

-

[26]

Z. Kobeissi, I. Mazari-Fouquer, and D. Ruiz-Balet. The tragedy of the commons: A mean- field game approach to the reversal of travelling waves.Nonlinearity, 37(11):115010, 2024

work page 2024

-

[27]

J.-M. Lasry and P.-L. Lions. Mean field games.Japanese journal of mathematics, 2(1):229– 260, 2007

work page 2007

-

[28]

P. Lavigne and P. Tankov. Decarbonization of financial markets: a mean-field game ap- proach.arXiv preprint arXiv:2301.09163, 2023

-

[29]

A. R. M´ esz´ aros and C. Mou. Mean field games systems under displacement monotonicity. SIAM Journal on Mathematical Analysis, 56(1):529–553, 2024

work page 2024

-

[30]

Pham.Continuous-time stochastic control and optimization with financial applications, volume 61

H. Pham.Continuous-time stochastic control and optimization with financial applications, volume 61. Springer Science & Business Media, 2009

work page 2009

-

[31]

G. D. Sarto, M. Leocata, and G. Livieri. A mean field game approach for pollution regu- lation of competitive firms, 2024

work page 2024

-

[32]

S. Smulders, M. Toman, and C. Withagen. Growth theory and ‘green growth’.Oxford review of economic policy, 30(3):423–446, 2014

work page 2014

-

[33]

O. Tahvonen and J. Kuuluvainen. Economic growth, pollution, and renewable resources. Journal of Environmental Economics and Management, 24(2):101–118, 1993

work page 1993

-

[34]

L. Tangpi and S. Wang. Mean field games with common noise via malliavin calculus, 2025

work page 2025

-

[35]

H. Uzawa. On a two-sector model of economic growth.The Review of Economic Studies, 29(1):40–47, 1961

work page 1961

-

[36]

J. Weyant. Some contributions of integrated assessment models of global climate change. Review of Environmental Economics and Policy, 2017

work page 2017

-

[37]

Zhang.Backward stochastic differential equations

J. Zhang.Backward stochastic differential equations. Springer, 2017

work page 2017

-

[38]

M. Zhou and M. Huang. On a best response problem arising in mean field stochastic growth games with common noise.Asian Journal of Control, 2024. 34

work page 2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.