Dynamically optimal portfolios for monotone mean--variance preferences

Pith reviewed 2026-05-23 00:57 UTC · model grok-4.3

The pith

Monotone mean-variance utility admits a full dynamic portfolio characterization in independent-return models under assumptions weaker than an equivalent martingale measure.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

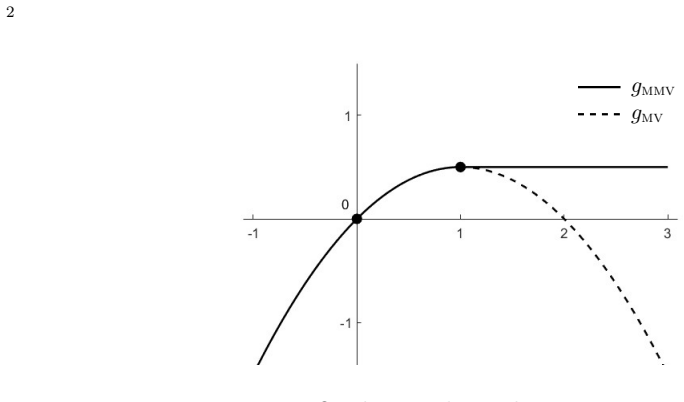

This paper provides, for the first time, a complete characterization of optimal dynamic portfolio choice for the MMV utility in asset price models with independent returns. The task is performed under minimal assumptions, weaker than the existence of an equivalent martingale measure and with no restrictions on the moments of asset returns. The maximal MMV utility is interpreted in terms of the monotone Sharpe ratio and the global squared MSR arises as the nominal yield from continuously compounding at the rate equal to the maximal local squared MSR. Simple necessary and sufficient conditions are given for mean-variance efficient portfolios to be MMV efficient.

What carries the argument

The monotone Sharpe ratio, which quantifies maximal MMV utility and enables separation of the global problem into local optimization steps via the independent-returns assumption.

If this is right

- The global squared monotone Sharpe ratio equals the compounded yield of successive local maximal squared ratios.

- Mean-variance efficient portfolios satisfy explicit necessary and sufficient conditions to remain efficient under the monotone criterion.

- Optimal MMV portfolios exist and can be constructed without invoking an equivalent martingale measure or finite-moment assumptions.

- The maximal MMV utility admits a direct interpretation as the monotone Sharpe ratio of the optimal strategy.

Where Pith is reading between the lines

- The independence assumption may allow similar separation results for other time-separable preference classes that admit a local-global decomposition.

- The compounding representation suggests that long-horizon MMV problems can be solved by iterating short-horizon local problems in discrete time.

- The absence of moment restrictions implies the characterization remains valid in models with heavy-tailed returns, provided independence holds.

Load-bearing premise

Asset returns are independent across time periods.

What would settle it

A counter-example in which returns lack independence yet the derived local-to-global compounding relation for the squared monotone Sharpe ratio still holds.

Figures

read the original abstract

Monotone mean-variance (MMV) utility is the minimal modification of the classical Markowitz utility that respects rational ordering of investment opportunities. This paper provides, for the first time, a complete characterization of optimal dynamic portfolio choice for the MMV utility in asset price models with independent returns. The task is performed under minimal assumptions, weaker than the existence of an equivalent martingale measure and with no restrictions on the moments of asset returns. We interpret the maximal MMV utility in terms of the monotone Sharpe ratio (MSR) and show that the global squared MSR arises as the nominal yield from continuously compounding at the rate equal to the maximal local squared MSR. The paper gives simple necessary and sufficient conditions for mean-variance (MV) efficient portfolios to be MMV efficient. Several illustrative examples contrasting the MV and MMV criteria are provided.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims to provide the first complete characterization of optimal dynamic portfolio choice for monotone mean-variance (MMV) utility in asset price models with independent returns. This is achieved under minimal assumptions weaker than the existence of an equivalent martingale measure and with no restrictions on the moments of asset returns. The maximal MMV utility is interpreted in terms of the monotone Sharpe ratio (MSR), and the global squared MSR is shown to arise as the nominal yield from continuously compounding at the maximal local squared MSR rate. Simple necessary and sufficient conditions are given for mean-variance efficient portfolios to also be MMV efficient, supported by illustrative examples contrasting the two criteria.

Significance. If the central derivations and proofs hold, the result is significant for extending dynamic portfolio theory to MMV preferences under notably weak assumptions. The separation into local and global problems, together with the explicit compounding interpretation of the squared MSR, provides a clean link between periods that relies only on the stated independence of returns. The necessary and sufficient conditions for MV-to-MMV efficiency and the absence of moment restrictions or EMM strengthen the applicability relative to classical MV analysis.

minor comments (1)

- The abstract is dense; expanding the statement of the independence assumption and its precise role in the separation result would improve readability for readers outside the immediate subfield.

Simulated Author's Rebuttal

We thank the referee for their thorough reading and positive evaluation of the manuscript. We are pleased that the referee recognizes the significance of the results, particularly the complete characterization under minimal assumptions, the link to the monotone Sharpe ratio, and the conditions distinguishing MV and MMV efficiency.

Circularity Check

No significant circularity

full rationale

The derivation separates local and global optimization problems using the explicit assumption of independent returns, then interprets the global squared MSR as the compounded yield from the maximal local squared MSR. These relations are obtained from the model dynamics and the definition of MMV utility rather than by re-labeling fitted quantities or reducing to self-citations. The central characterization holds under the stated weaker-than-EMM assumptions without any load-bearing step shown to be definitionally equivalent to its inputs. The paper is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Asset returns are independent

Reference graph

Works this paper leans on

-

[1]

F. Bellini and M. Frittelli. On the existence of minimax martingale measures.Math. Finance, 12(1):1–21, 2002. MR1883783

work page 2002

-

[2]

C. Bender and C. R. Niethammer. Onq-optimal martingale measures in exponential L´ evy models.Finance Stoch., 12(3):381–410, 2008. MR2410843

work page 2008

-

[3]

S. Biagini and A. ˇCern´ y. Admissible strategies in semimartingale portfolio selection.SIAM J. Control Optim., 49(1):42–72, 2011. MR2765656

work page 2011

-

[4]

S. Biagini and A. ˇCern´ y. Convex duality and Orlicz spaces in expected utility maximization. Math. Finance, 30(1):85–127, 2020. MR4067071

work page 2020

-

[5]

F. Black and A. F. Perold. Theory of constant proportion portfolio insurance.J. Econom. Dynam. Control, 16(3):403–426, 1992

work page 1992

-

[6]

S. Cawston and L. Vostrikova. Anf-divergence approach for optimal portfolios in exponen- tial L´ evy models. In Y. Kabanov, M. Rutkowski, and T. Zariphopoulou, editors,Inspired by Finance, pages 83–101. Springer, Cham, 2014. The Musiela Festschrift. MR3204213

work page 2014

- [7]

- [8]

- [9]

-

[10]

A. ˇCern´ y and J. Kallsen. On the structure of general mean–variance hedging strategies. Ann. Probab., 35(4):1479–1531, 2007. MR2330978

work page 2007

-

[11]

A. ˇCern´ y and J. Ruf. Pure-jump semimartingales.Bernoulli, 27(4):2624–2648, 2021. MR4303898

work page 2021

-

[12]

A. ˇCern´ y and J. Ruf. Simplified stochastic calculus with applications in Economics and Finance.European J. Oper. Res., 293(2):547–560, 2021. MR4241583

work page 2021

-

[13]

A. ˇCern´ y and J. Ruf. Simplified stochastic calculus via semimartingale representations. Electron. J. Probab., 27:1–32, 2022. Paper No. 3. MR4362774

work page 2022

-

[14]

A. ˇCern´ y and J. Ruf. Simplified calculus for semimartingales: Multiplicative compensators and changes of measure.Stochastic Process. Appl., 161:572–602, 2023. MR4585465

work page 2023

-

[15]

A. ˇCern´ y, F. Maccheroni, M. Marinacci, and A. Rustichini. On the computation of optimal monotone mean–variance portfolios via truncated quadratic utility.J. Math. Econom., 48 (6):386–395, 2012. MR2988098

work page 2012

-

[16]

X. Cui, D. Li, S. Wang, and S. Zhu. Better than dynamic mean–variance: Time inconsis- tency and free cash flow stream.Math. Finance, 22(2):346–378, 2012. MR2897388

work page 2012

-

[17]

C. Dol´ eans-Dade. Quelques applications de la formule de changement de variables pour les semimartingales.Z. Wahrsch. verw. Gebiete, 16:181–194, 1970. MR283883

work page 1970

-

[18]

E. Eberlein and J. Jacod. On the range of options prices.Finance Stoch., 1(2):131–140, 1997

work page 1997

-

[19]

M. ´Emery. Stabilit´ e des solutions des ´ equations diff´ erentielles stochastiques application aux int´ egrales multiplicatives stochastiques.Z. Wahrsch. verw. Gebiete, 41(3):241–262, 1978. MR0464400

work page 1978

-

[20]

F. Esche and M. Schweizer. Minimal entropy preserves the L´ evy property: how and why. Stochastic Process. Appl., 115(2):299–327, 2005. MR2111196 37

work page 2005

-

[21]

D. Filipovi´ c and M. Kupper. Monotone and cash-invariant convex functions and hulls. Insurance Math. Econom., 41(1):1–16, 2007. MR2324561

work page 2007

- [22]

-

[23]

T. Fujiwara and Y. Miyahara. The minimal entropy martingale measures for geometric L´ evy processes.Finance Stoch., 7(4):509–531, 2003. MR2014248

work page 2003

-

[24]

T. Goll and L. R¨ uschendorf. Minimax and minimal distance martingale measures and their relationship to portfolio optimization.Finance Stoch., 5(4):557–581, 2001. MR1862002

work page 2001

-

[25]

S. Hodges. A generalization of the Sharpe Ratio and its application to valuation bounds and risk measures. Available from warwick.ac.uk. Accessed 27/12/2024. FORC Preprint 98/88, University of Warwick, 1998

work page 2024

-

[26]

Y. Hu, X. Shi, and Z. Q. Xu. Constrained monotone mean–variance problem with random coefficients.SIAM J. Financial Math., 14(3):838–854, 2023. MR4621927

work page 2023

-

[27]

J. Jacod and A. N. Shiryaev.Limit Theorems for Stochastic Processes, volume 288 of Comprehensive Studies in Mathematics. Springer, Berlin, 2nd edition, 2003. MR1943877

work page 2003

-

[28]

P. Jakub˙ enas. On option pricing in certain incomplete markets. In A. N. Shiryaev and E. F. Mishchenko, editors,Stochastic Financial Mathematics, volume 237 ofTr. Mat. Inst. Steklova, pages 123–142. Nauka, Moscow, 2002. MR1976510

work page 2002

-

[29]

M. Jeanblanc, S. Kl¨ oppel, and Y. Miyahara. Minimalf q-martingale measures of exponen- tial L´ evy processes.Ann. Appl. Probab., 17(5-6):1615–1638, 2007. MR2358636

work page 2007

-

[30]

J. Kallsen. A utility maximization approach to hedging in incomplete markets.Math. Methods Oper. Res., 50(2):321–338, 1999. MR1732402

work page 1999

-

[31]

J. Kallsen. Optimal portfolios for exponential L´ evy processes.Math. Methods Oper. Res., 51(3):357–374, 2000. MR1778648

work page 2000

-

[32]

Kallsen.σ-localization andσ-martingales.Theory Probab

J. Kallsen.σ-localization andσ-martingales.Theory Probab. Appl., 48(1):152–163, 2004. MR2013413

work page 2004

-

[33]

J. Kallsen and J. Muhle-Karbe. Utility maximization in models with conditionally inde- pendent increments.Ann. Appl. Probab., 20(6):2162–2177, 2010. MR2759731

work page 2010

-

[34]

I. Karatzas and C. Kardaras. The num´ eraire portfolio in semimartingale financial models. Finance Stoch., 11(4):447–493, 2007. MR2335830

work page 2007

- [35]

-

[36]

B. Li, J. Guo, and L. Tian. Optimal investment and reinsurance policies for the Cram´ er– Lundberg risk model under monotone mean–variance preference.Internat. J. Control, 97 (6):1296–1310, 2024. MR4742973

work page 2024

- [37]

-

[38]

Y. Li, Z. Liang, and S. Pang. Comparison between mean–variance and monotone mean– variance preferences under jump diffusion and stochastic factor model.Math. Oper. Res., 50(3):2405–2432, 2025. MR4949476

work page 2025

-

[39]

Y. Li, Z. Liang, and S. Pang. Comparison between mean–variance and monotone mean– variance preferences in general markets: a new perspective.Oper. Res. Lett., 61:Paper No. 107298, 7, 2025. MR4896371

work page 2025

-

[40]

F. Maccheroni, M. Marinacci, and A. Rustichini. Ambiguity aversion, robustness, and the variational representation of preferences.Econometrica, 74(6):1447–1498, 2006. MR2268407 38

work page 2006

-

[41]

F. Maccheroni, M. Marinacci, A. Rustichini, and M. Taboga. Portfolio selection with monotone mean–variance preferences.Math. Finance, 19(3):487–521, 2009. MR2536871

work page 2009

-

[42]

M. Nutz. Power utility maximization in constrained exponential L´ evy models.Math. Finance, 22(4):690–709, 2012. MR2968281

work page 2012

-

[43]

T. Pennanen and A.-P. Perkki¨ o.Convex Stochastic Optimization, volume 107 ofProbability Theory and Stochastic Modelling. Springer Cham, 2024

work page 2024

-

[44]

P. E. Protter.Stochastic Integration and Differential Equations, volume 21 ofStochastic Modelling and Applied Probability. Springer, Berlin, 2nd edition, 2005. MR2273672

work page 2005

-

[45]

R. T. Rockafellar.Convex Analysis. Princeton Mathematical Series, No. 28. Princeton University Press, Princeton, N.J., 1970. MR0274683

work page 1970

-

[46]

R. T. Rockafellar and R. J.-B. Wets.Variational Analysis, volume 317 ofGrundlehren der mathematischen Wissenschaften. Springer-Verlag, Berlin, 1998. MR1491362

work page 1998

-

[47]

Rudin.Real and Complex Analysis

W. Rudin.Real and Complex Analysis. McGraw-Hill Book Co., New York, 3rd edition,

- [48]

- [49]

-

[50]

Y. Shen and B. Zou. Short communication: Cone-constrained monotone mean–variance portfolio selection under diffusion models.SIAM J. Financial Math., 13(4):SC99–SC112,

- [51]

-

[52]

A. N. Shiryaev and A. S. Cherny. A vector stochastic integral and the fundamental theorem of asset pricing.Proc. Steklov Inst. Math., 237:6–49, 2002. MR1975582

work page 2002

-

[53]

M. S. Strub and D. Li. A note on monotone mean–variance preferences for continuous processes.Oper. Res. Lett., 48(4):0–3, 2020. MR4100873

work page 2020

-

[54]

J. Trybu la and D. Zawisza. Continuous-time portfolio choice under monotone mean– variance preferences—stochastic factor case.Math. Oper. Res., 44(3):966–987, 2019. MR3996654

work page 2019

-

[55]

M. Zhitlukhin. Monotone Sharpe ratios and related measures of investment performance. In 2017 MATRIX Annals, volume 2 ofMATRIX Book Ser., pages 637–665. Springer, Cham,

work page 2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.