Mean Field Game of Optimal Tracking Portfolio

Pith reviewed 2026-05-22 16:10 UTC · model grok-4.3

The pith

A mean field equilibrium exists for fund managers who minimize maximum wealth shortfalls relative to a benchmark mixing average population wealth and a market index.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

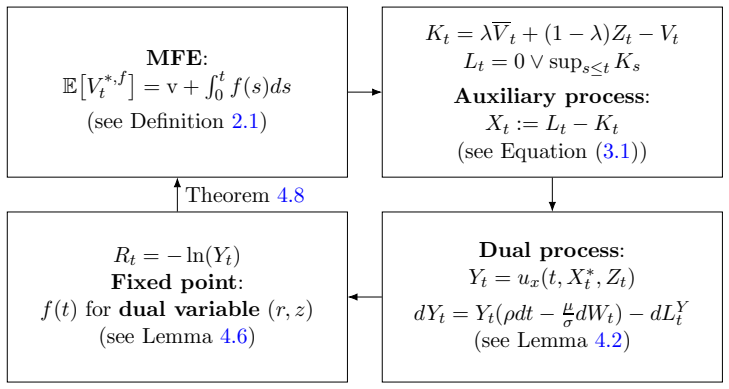

The paper establishes the existence of the mean field equilibrium for the optimal tracking portfolio problem in a large population of fund managers. Using the PDE approach and dual transform, the best response control is characterized in analytical form via a dual reflected diffusion process. The consistency condition of the mean field equilibrium is verified in separated domains with the help of the duality relationship and properties of the dual process, allowing the construction of an approximate Nash equilibrium for the n-player game when n is large.

What carries the argument

The dual reflected diffusion process obtained via dual transform, which analytically characterizes the representative agent's best response control and permits verification of the mean field consistency condition.

If this is right

- The equilibrium strategies derived from the mean field game form an approximate Nash equilibrium for the original finite-player game whenever the number of managers is sufficiently large.

- Optimal controls for each manager admit an explicit analytical expression in terms of the dual reflected diffusion.

- The reflected state dynamics arise directly from the maximum-shortfall objective with respect to the mixed benchmark.

- The verification of consistency succeeds in separated domains precisely because of the linear structure of the benchmark and the duality properties of the dual process.

Where Pith is reading between the lines

- The dual-transform technique could be adapted to other mean field games with state reflection or relative-performance objectives in stochastic control.

- Numerical solution of the associated PDEs would allow quantitative assessment of how closely finite-n strategies approach the mean field limit.

- The same consistency-verification approach may extend to models with additional market frictions such as transaction costs or borrowing constraints.

- This framework links competitive portfolio problems to broader classes of mean field games with endogenous benchmarks.

Load-bearing premise

The benchmark process is modeled by a linear combination of the population's average wealth process and a market index process, allowing the reflected state and dual transform to close the consistency condition.

What would settle it

A direct calculation or simulation showing that the dual reflected diffusion fails to satisfy the consistency condition when inserted back into the benchmark in the separated domains would disprove the existence of the mean field equilibrium.

Figures

read the original abstract

This paper studies the mean field game (MFG) problem arising from a large population competition in fund management, featuring a new type of relative performance via the benchmark tracking. In the $n$-player model, each agent aims to minimize the expected largest shortfall of the wealth with reference to the benchmark process, which is modeled by a linear combination of the population's average wealth process and a market index process. With a continuum of agents, we formulate the MFG problem with a reflected state process. We establish the existence of the mean field equilibrium (MFE) using the partial differential equation (PDE) approach. Firstly, by applying the dual transform, the best response control of the representative agent can be characterized in analytical form in terms of a dual reflected diffusion process. As a novel contribution, we verify the consistency condition of the MFE in separated domains with the help of the duality relationship and properties of the dual process. Moreover, based on the MFE, we construct an approximate Nash equilibrium for the $n$-player game when the number $n$ is sufficiently large.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies a mean field game (MFG) for optimal tracking portfolios in a large population of fund managers. Each agent minimizes the expected largest shortfall of their wealth relative to a benchmark process, modeled as a linear combination of the population's average wealth and a market index. The problem is formulated with a reflected state process. The authors establish the existence of the mean field equilibrium (MFE) using a PDE approach: they characterize the best-response control via dual transform in terms of a dual reflected diffusion process, verify the consistency condition of the MFE in separated domains using duality relationships, and construct an approximate Nash equilibrium for the finite n-player game when n is large.

Significance. If the technical details hold, this contributes to mean field games in mathematical finance by incorporating relative performance through benchmark tracking with state reflection. The dual-transform characterization of the best response and the verification of consistency in separated domains are strengths, as is the construction of approximate Nash equilibria linking to the finite-player setting. The paper provides an analytical form for the control and a direct consistency check rather than relying solely on abstract fixed-point arguments.

major comments (1)

- [Section describing consistency verification of the MFE (following the dual-transform characterization)] The central existence argument (PDE approach and consistency verification) proceeds by dual-transform characterization yielding an explicit best-response control in terms of a dual reflected diffusion, followed by direct verification of the mean-field consistency condition inside separated domains. For this verification to close without an auxiliary fixed-point argument, the dual process must preserve reflection and the linear benchmark must decouple across domains. The manuscript does not explicitly derive or cite the required boundary conditions at the separation interface or confirm that the dual reflection maps back to the original state constraint uniformly. This is load-bearing for the claimed existence result.

minor comments (2)

- [Abstract] The abstract refers to 'separated domains' without a brief definition or forward reference; adding one sentence linking to the relevant section would improve accessibility.

- [Notation and model setup] Notation for the reflected state process, dual process, and benchmark coefficients should be checked for consistency between the n-player formulation and the MFG limit.

Simulated Author's Rebuttal

We thank the referee for the thorough review and constructive feedback on our manuscript. The major comment raises an important point about the explicitness of certain technical details in the existence argument, which we address below. We will incorporate clarifications in a revised version to strengthen the presentation.

read point-by-point responses

-

Referee: [Section describing consistency verification of the MFE (following the dual-transform characterization)] The central existence argument (PDE approach and consistency verification) proceeds by dual-transform characterization yielding an explicit best-response control in terms of a dual reflected diffusion, followed by direct verification of the mean-field consistency condition inside separated domains. For this verification to close without an auxiliary fixed-point argument, the dual process must preserve reflection and the linear benchmark must decouple across domains. The manuscript does not explicitly derive or cite the required boundary conditions at the separation interface or confirm that the dual reflection maps back to the original state constraint uniformly. This is load-bearing for the claimed existence result.

Authors: We appreciate the referee's observation that greater explicitness would strengthen the central existence argument. The dual reflected diffusion is constructed via the dual transform to preserve the reflection mechanism of the original state process by design, drawing on standard properties of duality for reflected diffusions. The linear form of the benchmark permits decoupling across the separated domains, enabling direct verification of the consistency condition through the duality relationship without an auxiliary fixed-point argument. We acknowledge, however, that the manuscript would benefit from more detailed derivations of the interface boundary conditions and a uniform confirmation of the state-constraint mapping. In the revised manuscript we will insert a dedicated paragraph immediately after the dual-transform characterization, deriving the required boundary conditions from the continuity of the value function and its first derivatives across the separation interface, and confirming uniform preservation of the reflection by establishing a direct correspondence between the local-time processes of the primal and dual diffusions. revision: yes

Circularity Check

No significant circularity; MFE existence proof relies on standard duality for reflected processes

full rationale

The paper establishes MFE existence via a PDE approach: dual transform yields an explicit best-response control in terms of a dual reflected diffusion, after which the consistency condition (mean-field term matching population average) is verified directly in separated domains using duality relationships and dual-process properties. This chain depends on external mathematical structure for reflected diffusions and the given linear benchmark dynamics rather than any self-definitional loop, fitted parameter renamed as prediction, or load-bearing self-citation. The verification step is presented as novel but does not reduce by construction to the paper's own inputs; the benchmark is modeled externally and the dual transform is a standard tool. No equations or claims in the provided derivation chain exhibit the enumerated circularity patterns. The result is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Wealth processes follow linear dynamics driven by controlled drift and diffusion terms with non-negative reflection.

- domain assumption The dual reflected diffusion process satisfies the necessary martingale and boundary properties for consistency verification.

Reference graph

Works this paper leans on

-

[1]

Abraham, R (2000): Reflecting Brownian snake and a Neumann Dirich let problem. Stoch. Process. Appl. 89(2), 239-260

work page 2000

-

[2]

(2019): Rate control un der heavy traffic with strategic servers

Bayraktar, E., Budhiraja, A., Cohen, A. (2019): Rate control un der heavy traffic with strategic servers. Ann. Appl. Probab. 29(1), 1-35

work page 2019

- [3]

-

[4]

(2025): Mean field game of controls with stat e reflections: Existence and limit theory

Bo, L., Wang, J., Yu, X. (2025): Mean field game of controls with stat e reflections: Existence and limit theory. Preprint, available at https://arxiv.org/abs/2503.03253

-

[5]

(2000): Risk-constrained dynamic active portfolio man agement Manag

Browne, S. (2000): Risk-constrained dynamic active portfolio man agement Manag. Sci. 6(9), 1188-1199

work page 2000

-

[6]

(2009): Optimal control of capital injec tions by reinsurance in a diffusion approximation

Eisenberg, J., Schmidli, H. (2009): Optimal control of capital injec tions by reinsurance in a diffusion approximation. Bl¨ atter der DGVFM30(1), 1-13

work page 2009

-

[7]

(2015): Optimal investment under relative p erformance concerns

Espinosa, G., Touzi, N. (2015): Optimal investment under relative p erformance concerns. Math. Finan. 25(2), 221–257. W. Farkas, L. Mathys and N. Vasiljevi´ c (2021): Intra-Horizon e xpected shortfall and risk structure in models with jumps. Math. Finance 31(2), 772-823

work page 2015

-

[8]

(2019): On a class of singular stochastic control prob lems for reflected diffusions

Ferrari, G. (2019): On a class of singular stochastic control prob lems for reflected diffusions. J. Math. Anal. Appl. 473(2), 952-979

work page 2019

-

[9]

(2023): Mean field portfolio games

Fu, G., Zhou, C. (2023): Mean field portfolio games. Finan. Stoch. 27(1), 189-231

work page 2023

-

[10]

(2005): Optimal portfolio selec tion and dynamic benchmark tracking

Gaivoronski, A., Krylov, S., Wijst, N. (2005): Optimal portfolio selec tion and dynamic benchmark tracking. Euro. J. Oper. Res. 163, 115-131

work page 2005

-

[11]

(2016): Optimal pricing barriers in a regulate d market using reflected diffusion processes

Han, Z., Hu, Y., Lee, C. (2016): Optimal pricing barriers in a regulate d market using reflected diffusion processes. Quant. Finance 16(4), 639-647

work page 2016

-

[12]

Huang, M., Malham´ e, R., Caines, P. E. (2006): Large population sto chastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence princip le. Commun. Inf. Syst. 6(3), 221-252

work page 2006

-

[13]

(2020): Many-player games of optimal cons umption and investment under relative performance criteria

Lacker, D., Soret, A. (2020): Many-player games of optimal cons umption and investment under relative performance criteria. Math. Finan. Econ. 14(2), 263–281

work page 2020

-

[14]

(2019): Mean field and n-agent games for optimal investment under relative performance criteria

Lacker, D., Zariphopoulou, T. (2019): Mean field and n-agent games for optimal investment under relative performance criteria. Math. Finance 29(4), 1003–1038

work page 2019

-

[15]

Lasry, J.M., Lions, P.L. (2007): Mean field games. Jpn. J. Math. 2(1), 229-260

work page 2007

-

[16]

(2008): Optimal dividend and issuance of equ ity policies in the presence of propor- tional costs

Lokka, A., Zervos, M. (2008): Optimal dividend and issuance of equ ity policies in the presence of propor- tional costs. Insur. Math. Econ. 42(3), 954-961

work page 2008

-

[17]

(2022): Optimal asset allocation for outperforming a stochastic benchmark target

Ni, C., Li, Y., Forsyth, P., Carroll, R. (2022): Optimal asset allocation for outperforming a stochastic benchmark target. Quant. Finan. 22(9): 1595-1626

work page 2022

-

[18]

(2002): Minimizing shortfall risk and applications to finance and insurance problems

Pham, H. (2002): Minimizing shortfall risk and applications to finance and insurance problems. Ann. Appl. Probab. 12(1), 143-172

work page 2002

-

[19]

(2023): The convergence problem in mean field games wit h Neumann boundary conditions

Ricciardi, M. (2023): The convergence problem in mean field games wit h Neumann boundary conditions. SIAM J. Math. Anal. 55(4), 3316-3343

work page 2023

-

[20]

Souganidis, P. E., Zariphopoulou, T. (2024): Mean field games with un bounded controlled common noise in portfolio management with relative performance criteria. Math. Finan. Econ. 18(2), 429-456. 35

work page 2024

-

[21]

Baumann (2018): Optimal construction and rebalanc ing of index-tracking portfolios

Strub, O., P. Baumann (2018): Optimal construction and rebalanc ing of index-tracking portfolios. Euro. J. Oper. Res. 264, 370-387

work page 2018

-

[22]

(2004): The conditional probability density func tion for a reflected Brownian motion

Veestraeten, D. (2004): The conditional probability density func tion for a reflected Brownian motion. Comput. Econ. 24(2), 185-207-2380

work page 2004

-

[23]

(2016): Optimal inventory control with p ath-dependent cost criteria

Weerasinghe, A., Zhu, C. (2016): Optimal inventory control with p ath-dependent cost criteria. Stoch. Process. Appl. 126(6), 1585-1621

work page 2016

-

[24]

(2006): Tracking a financial benchma rk using a few assets

Yao, D., Zhang, S., Zhou, X.Y. (2006): Tracking a financial benchma rk using a few assets. Oper. Res. 54(2), 232-246. 36

work page 2006

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.