Convolutionally Low-Rank Models with Modified Quantile Regression for Interval Time Series Forecasting

Pith reviewed 2026-05-10 08:33 UTC · model grok-4.3

The pith

Integrating modified quantile regression into a convolutional low-rank forecasting model produces accurate prediction intervals for time series.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By adapting quantile regression to operate inside the convolutional low-rank framework of LbCNNM and supplementing it with interval calibration, the method LbCNNM-MQR yields prediction intervals that achieve higher accuracy than competing approaches when evaluated on large collections of real time series.

What carries the argument

LbCNNM-MQR, formed by embedding a modified quantile regression loss into the learning-based convolutional nuclear norm minimization model together with separate calibration procedures that adjust interval bounds after training.

If this is right

- The approach supports direct multi-step-ahead interval forecasts without training separate models for each horizon.

- Post-training calibration further narrows intervals while maintaining nominal coverage levels.

- Superior performance holds across a broad range of real-world domains represented in the 100,000-series test bed.

- The modification removes the uncertainty-estimation limitation that previously affected LbCNNM and similar advanced point-forecasting techniques.

Where Pith is reading between the lines

- The same modified quantile regression step could be tested inside other nuclear-norm or low-rank forecasting architectures to check whether the performance gain transfers.

- Controlled experiments on synthetic series engineered to obey or violate the convolutional low-rank assumption would clarify when the method is expected to succeed.

- The calibration layer might be combined with conformal prediction wrappers to obtain distribution-free guarantees on top of the existing empirical gains.

Load-bearing premise

The low-rank convolutional structure identified on training data remains effective once the model is extended with the modified quantile regression term, and the calibration adjustments do not overfit to the validation collections used in the experiments.

What would settle it

Apply LbCNNM-MQR to a new, independent collection of at least 100,000 time series and measure that its prediction interval coverage probability and mean prediction interval width fail to improve on those of unmodified quantile regression or other published interval methods.

Figures

read the original abstract

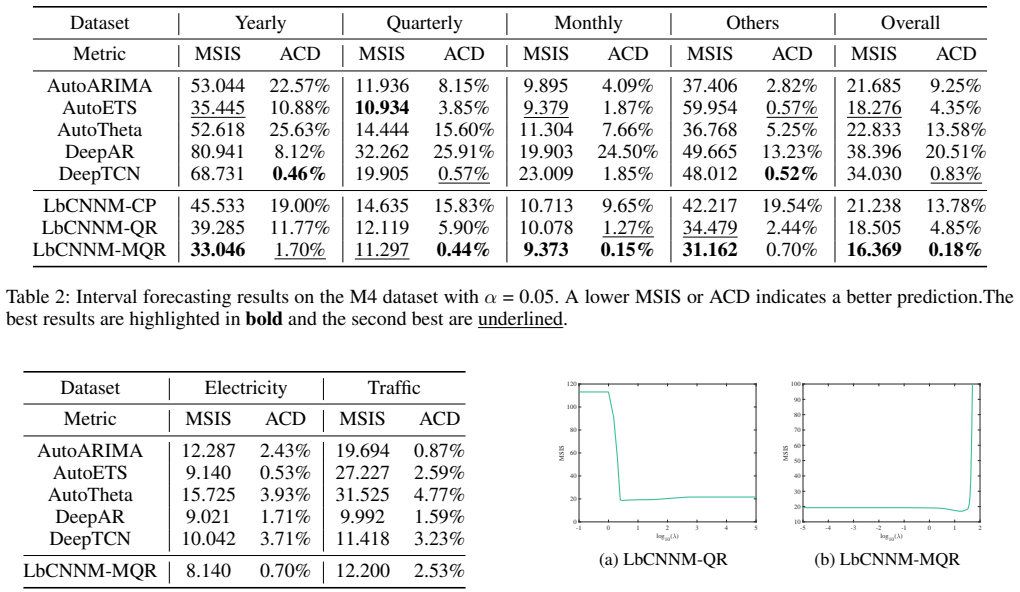

The quantification of uncertainty in prediction models is crucial for reliable decision-making, yet remains a significant challenge. Interval time series forecasting offers a principled solution to this problem by providing prediction intervals (PIs), which indicates the probability that the true value falls within the predicted range. We consider a recently established point forecasts (PFs) method termed Learning-Based Convolution Nuclear Norm Minimization (LbCNNM), which directly generates multi-step ahead forecasts by leveraging the convolutional low-rankness property derived from training data. While theoretically complete and empirically effective, LbCNNM lacks inherent uncertainty estimation capabilities, a limitation shared by many advanced forecasting methods. To resolve the issue, we modify the well-known Quantile Regression (QR) and integrate it into LbCNNM, resulting in a novel interval forecasting method termed LbCNNM with Modified Quantile Regression (LbCNNM-MQR). In addition, we devise interval calibration techniques to further improve the accuracy of PIs. Extensive experiments on over 100,000 real-world time series demonstrate the superior performance of LbCNNM-MQR.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes LbCNNM-MQR, which integrates a modified form of quantile regression into the existing Learning-Based Convolution Nuclear Norm Minimization (LbCNNM) point-forecasting framework to enable interval time series forecasting. It additionally introduces post-hoc interval calibration techniques. The central empirical claim is that this combination yields superior prediction-interval performance on a collection of over 100,000 real-world time series.

Significance. If the empirical superiority claim is substantiated with transparent baselines, metrics, and non-circular evaluation, the work would supply a practical route for adding calibrated uncertainty estimates to convolutional low-rank forecasting models. The scale of the reported dataset is a genuine strength that could support broad applicability claims in large-scale forecasting.

major comments (3)

- [Abstract / Experiments] Abstract and Experiments section: the claim of 'superior performance' on >100,000 series is unsupported by any reported baselines, interval-specific metrics (e.g., coverage, Winkler score, or interval width), or statistical significance tests. This information is load-bearing for the central empirical contribution and must be supplied with explicit tables or figures.

- [Methods (LbCNNM-MQR and calibration)] Methods section on LbCNNM-MQR and calibration: it is not shown whether the modification to quantile regression or the subsequent calibration steps involve parameters fitted on the same data used for final evaluation. If any such fitting occurs, the reported gains could be circular by construction, directly affecting the validity of the large-scale comparison.

- [Modeling / Theoretical analysis] Theoretical / modeling section: the manuscript does not verify or discuss whether the convolutional low-rankness property established for the original LbCNNM continues to hold once the model is extended with the modified quantile regression; this assumption is load-bearing for claiming that the interval extension inherits the original method's theoretical completeness.

minor comments (2)

- [Methods] Notation for the modified quantile regression loss and the calibration mapping should be introduced with explicit equations rather than prose descriptions to improve reproducibility.

- [Introduction] The abstract and introduction repeatedly use 'superior performance' without defining the comparison set; a short related-work paragraph summarizing the strongest interval-forecasting baselines would help readers situate the contribution.

Simulated Author's Rebuttal

We thank the referee for their constructive and detailed comments. We address each major comment point by point below, indicating where revisions will be made to improve clarity and substantiation.

read point-by-point responses

-

Referee: [Abstract / Experiments] Abstract and Experiments section: the claim of 'superior performance' on >100,000 series is unsupported by any reported baselines, interval-specific metrics (e.g., coverage, Winkler score, or interval width), or statistical significance tests. This information is load-bearing for the central empirical contribution and must be supplied with explicit tables or figures.

Authors: We agree that the central empirical claim requires explicit support. In the revised manuscript we will expand the Experiments section with tables and figures that report interval-specific metrics (coverage probability, Winkler score, interval width) for LbCNNM-MQR against appropriate baselines, together with statistical significance tests, all evaluated on the full collection of over 100,000 series. revision: yes

-

Referee: [Methods (LbCNNM-MQR and calibration)] Methods section on LbCNNM-MQR and calibration: it is not shown whether the modification to quantile regression or the subsequent calibration steps involve parameters fitted on the same data used for final evaluation. If any such fitting occurs, the reported gains could be circular by construction, directly affecting the validity of the large-scale comparison.

Authors: We confirm that the modified quantile regression parameters are obtained from the training portion of each series and that the post-hoc calibration uses a separate validation split that is never seen during final evaluation. We will revise the Methods section to include an explicit description of the data partitioning protocol and a statement that no calibration parameters are estimated on the test data. revision: yes

-

Referee: [Modeling / Theoretical analysis] Theoretical / modeling section: the manuscript does not verify or discuss whether the convolutional low-rankness property established for the original LbCNNM continues to hold once the model is extended with the modified quantile regression; this assumption is load-bearing for claiming that the interval extension inherits the original method's theoretical completeness.

Authors: The modified quantile regression is applied to the residuals of the already-trained convolutional low-rank model and does not change the convolutional structure or the nuclear-norm objective; therefore the low-rankness property is preserved by construction. We will add a short discussion subsection that states this reasoning and, where possible, supplies a brief verification argument. revision: yes

Circularity Check

No significant circularity; method extension and experiments are independent of inputs

full rationale

The paper starts from the established LbCNNM point-forecasting method (which uses convolutional low-rankness derived from training data) and proposes an explicit modification to quantile regression plus post-hoc calibration techniques to produce interval forecasts. No equation or step in the abstract or description reduces the claimed performance or the modified QR component to a tautological re-use of the original inputs or a fitted parameter renamed as a prediction. The large-scale evaluation on >100k real-world series is presented as external validation rather than a self-referential fit. Self-citations to LbCNNM are load-bearing only for the base model, not for the novel interval extension. This satisfies the criteria for a self-contained derivation with no circular reduction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Convolutional low-rankness property derived from training data holds for the forecasting task

- domain assumption Modified quantile regression preserves the probabilistic interpretation of prediction intervals

Reference graph

Works this paper leans on

-

[1]

Spatiotemporal-aware Trend-Seasonality Decompo- sition Network for Traffic Flow Forecasting.Proceedings of the AAAI Conference on Artificial Intelligence, 39(11): 11463–11471. Chavleishvili, S.; and Manganelli, S. 2024. Forecasting and stress testing with quantile vector autoregression.Journal of Applied Econometrics, 39(1): 66–85. Chen, J.; Lenssen, J. E...

-

[2]

DeepAR: Probabilistic forecasting with autoregres- sive recurrent networks.International journal of forecast- ing, 36(3): 1181–1191. Shibo, F.; Zhao, P.; Liu, L.; Wu, P.; and Shen, Z. 2025. HDT: Hierarchical Discrete Transformer for Multivariate Time Se- ries Forecasting.Proceedings of the AAAI Conference on Artificial Intelligence, 39(1): 746–754. Tang, ...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.