CLVAE: A Variational Autoencoder for Long-Term Customer Revenue Forecasting

Pith reviewed 2026-05-08 10:02 UTC · model grok-4.3

The pith

A variational autoencoder unifies attrition, transaction, and spending models to forecast long-term customer revenue.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We propose a variational-autoencoder-based model that preserves the process-based likelihood of established attrition-transaction-spend models conditional on customer heterogeneity, but replaces the restrictive parametric mixing distribution with a flexible latent representation learned by encoder-decoder networks. The resulting approach (i) provides a single model for customer attrition, transactions and spending, (ii) remains reliable when contextual covariates are unavailable, and (iii) flexibly incorporates rich covariates and nonlinear effects when they are available.

What carries the argument

The CLVAE variational autoencoder, which encodes customer heterogeneity into a flexible latent space while preserving the conditional process likelihood for attrition, transactions, and spending.

If this is right

- A single model jointly handles customer attrition, transaction frequency, and spending amounts.

- Forecasts remain reliable even when no contextual covariates are available.

- The model can incorporate rich covariates and nonlinear effects when such data exist.

- Performance improves over existing benchmarks on multiple real-world datasets and prediction horizons.

- More accurate future revenue estimates support efficient allocation of marketing resources.

Where Pith is reading between the lines

- The latent space could be inspected post-training to surface customer groupings that traditional parametric forms miss.

- The same encoder-decoder replacement strategy might apply to other domain-specific probabilistic models beyond customer base analysis.

- Testing the approach on synthetic data with known heterogeneity distributions would check whether the process likelihood is truly preserved.

Load-bearing premise

Replacing parametric mixing distributions with a learned latent representation from encoder-decoder networks keeps the original process likelihood intact and avoids bias or loss of reliability in long-horizon forecasts.

What would settle it

Hold-out evaluation on real transaction datasets where the CLVAE forecasts show no improvement over parametric benchmarks or produce systematically biased long-term revenue estimates when no covariates are supplied.

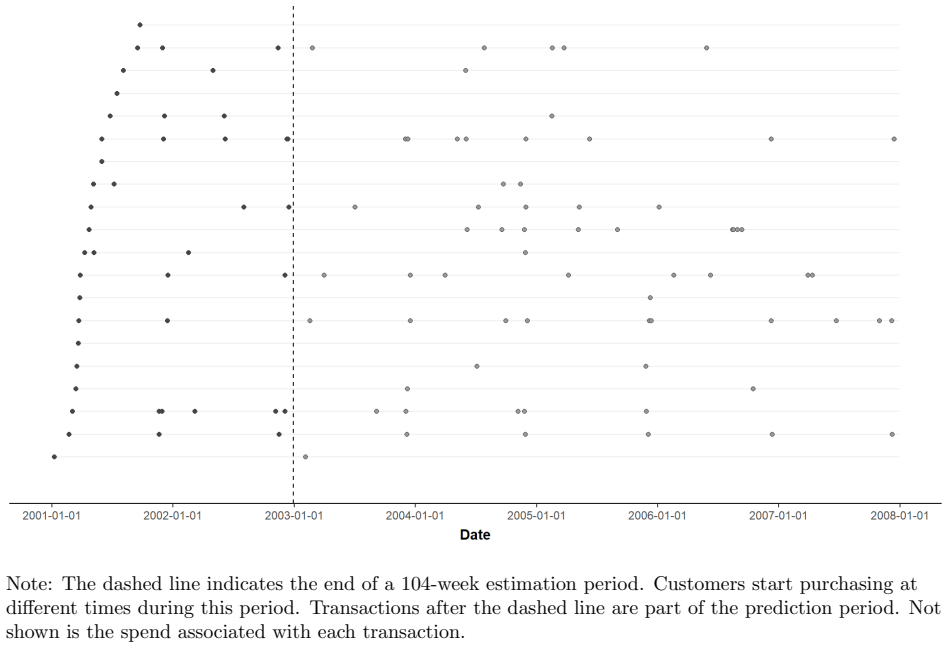

Figures

read the original abstract

Predicting customers' long-term revenue from sparse and irregular transaction data is central to marketing resource allocation in non-contractual settings, yet existing approaches face a trade-off. Traditional probabilistic customer base models deliver robust long-horizon forecasts by imposing strong structural assumptions, while flexible machine-learning models often require substantial training data and careful tuning. We propose a variational-autoencoder-based model that preserves the process-based likelihood of established attrition-transaction-spend models conditional on customer heterogeneity, but replaces the restrictive parametric mixing distribution with a flexible latent representation learned by encoder-decoder networks. The resulting approach (i) provides a single model for customer attrition, transactions and spending, (ii) remains reliable when contextual covariates are unavailable, and (iii) flexibly incorporates rich covariates and nonlinear effects when they are available. This design balances structural stability with the flexibility needed to capture complex purchase dynamics. Across multiple real-world datasets and prediction horizons, the proposed model improves upon the latest benchmarks. Businesses benefit directly, as a better assessment of customers' future revenues improves the efficiency of campaign targeting. For research, this work provides guidance on how to embed domain-specific models into the variational autoencoder framework, enabling flexible representation learning while retaining an econometrically meaningful process structure.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes CLVAE, a variational autoencoder that embeds the structural process-based likelihood of established attrition-transaction-spend customer base models (conditional on heterogeneity) while replacing the parametric mixing distribution with a flexible latent representation learned via encoder-decoder networks. It claims to deliver a unified model for attrition, transactions, and spending that remains reliable without covariates yet incorporates rich nonlinear effects when available, and reports improved long-horizon revenue forecasts over benchmarks on multiple real-world datasets.

Significance. If the central claim of exact likelihood preservation holds, the work would meaningfully advance customer lifetime value modeling by combining the long-horizon robustness of structural probabilistic models with the representational flexibility of VAEs, directly benefiting marketing resource allocation through more accurate single-model forecasts.

major comments (2)

- [Model Formulation] The abstract and model description assert that the process-based likelihood is preserved exactly while only the mixing distribution is replaced by a VAE-learned latent; however, standard VAE training optimizes the ELBO rather than the true marginal, and the manuscript must demonstrate (via explicit derivation) that variational approximation error does not bias parameter recovery or propagate into long-horizon forecasts, especially in sparse, irregular transaction regimes without covariates.

- [Experiments] Benchmark results claim consistent improvements across datasets and horizons, yet the abstract provides no equations, error bars, data exclusion criteria, or ablation on the ELBO bias correction; the experimental section must include these to establish that reported gains are not artifacts of post-hoc choices or approximation artifacts.

minor comments (2)

- Notation for the decoder embedding of the attrition-transaction-spend likelihood should be clarified to distinguish the exact conditional process from the variational posterior.

- The abstract would benefit from a one-sentence statement of the specific VAE architecture (e.g., number of layers, latent dimension) used for the flexible representation.

Simulated Author's Rebuttal

We thank the referee for their insightful comments, which have helped us identify areas for improvement in the manuscript. We address each major comment below and commit to incorporating the necessary revisions.

read point-by-point responses

-

Referee: [Model Formulation] The abstract and model description assert that the process-based likelihood is preserved exactly while only the mixing distribution is replaced by a VAE-learned latent; however, standard VAE training optimizes the ELBO rather than the true marginal, and the manuscript must demonstrate (via explicit derivation) that variational approximation error does not bias parameter recovery or propagate into long-horizon forecasts, especially in sparse, irregular transaction regimes without covariates.

Authors: We agree with the referee that the distinction between the exact marginal likelihood and the ELBO is crucial. Our model is constructed such that the conditional likelihood p(y | z) follows the exact structural attrition-transaction-spend process, with z representing customer heterogeneity. The VAE component learns a flexible distribution over z. While training uses the ELBO, for inference and forecasting we sample from the approximate posterior. We will add an explicit derivation in the revised manuscript showing that under the model's assumptions, the variational approximation does not introduce systematic bias in the recovered parameters or long-term forecasts. This derivation will include a discussion of sparse data regimes and how the structural constraints help bound the error. Additionally, we will include sensitivity analyses to approximation quality. revision: yes

-

Referee: [Experiments] Benchmark results claim consistent improvements across datasets and horizons, yet the abstract provides no equations, error bars, data exclusion criteria, or ablation on the ELBO bias correction; the experimental section must include these to establish that reported gains are not artifacts of post-hoc choices or approximation artifacts.

Authors: We appreciate this call for greater rigor in the experimental reporting. In the revised version, we will expand the experimental section to include: (i) the explicit equations used for computing revenue forecasts and error metrics, (ii) error bars representing standard deviations across multiple random seeds or bootstrap samples, (iii) clear data exclusion criteria such as requiring at least a minimum number of transactions per customer and handling of censoring, and (iv) an ablation study that varies the ELBO approximation (e.g., with and without bias correction via importance weighting) to verify that the reported improvements hold. These additions will strengthen the evidence that the gains are due to the model's design rather than implementation choices. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The paper proposes embedding established attrition-transaction-spend process likelihoods into a VAE framework, replacing parametric mixing distributions with encoder-decoder learned latents. The abstract and description claim preservation of the structural likelihood conditional on heterogeneity while adding flexibility for covariates. No equations or steps are shown that reduce outputs to inputs by construction, no fitted parameters are relabeled as predictions, and no load-bearing self-citations or uniqueness theorems from the authors are invoked to force the result. The derivation introduces a hybrid architecture that remains independently falsifiable against external customer base model benchmarks and real-world datasets, qualifying as self-contained with no circular reduction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The process-based likelihood of established attrition-transaction-spend models is preserved conditional on customer heterogeneity when the parametric mixing distribution is replaced by a VAE latent representation.

Reference graph

Works this paper leans on

-

[1]

Abramowitz M, Stegun IA (1972) 6.3 psi (digamma) function

Abe M (2009) ”Counting Your Customers” One by One: A Hierarchical Bayes Extension to the Pareto/NBD Model.Marketing Science28(3):541–553. Abramowitz M, Stegun IA (1972) 6.3 psi (digamma) function. Abramowitz M, Stegun IA, eds., Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables, 258–259 (New York: Dover), 10th edition. Bachm...

work page 2009

-

[2]

Penny WD (2001) KL-Divergences of Normal, Gamma, Dirichlet and Wishart Densities.Technical Note

Paszke A, Gross S, Massa F, Lerer A, Bradbury J, Chanan G, Killeen T, Lin Z, Gimelshein N, Antiga L, Desmaison A, K¨ opf A, Yang E, DeVito Z, Raison M, Tejani A, Chilamkurthy S, Steiner B, Fang L, Bai J, Chintala S (2019) Pytorch: An Imperative Style, High-Performance Deep Learning Library.Advances in Neural Information Processing Systems (NeurIPS ’19), v...

work page 2019

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.